Robotics Processor Market Insights

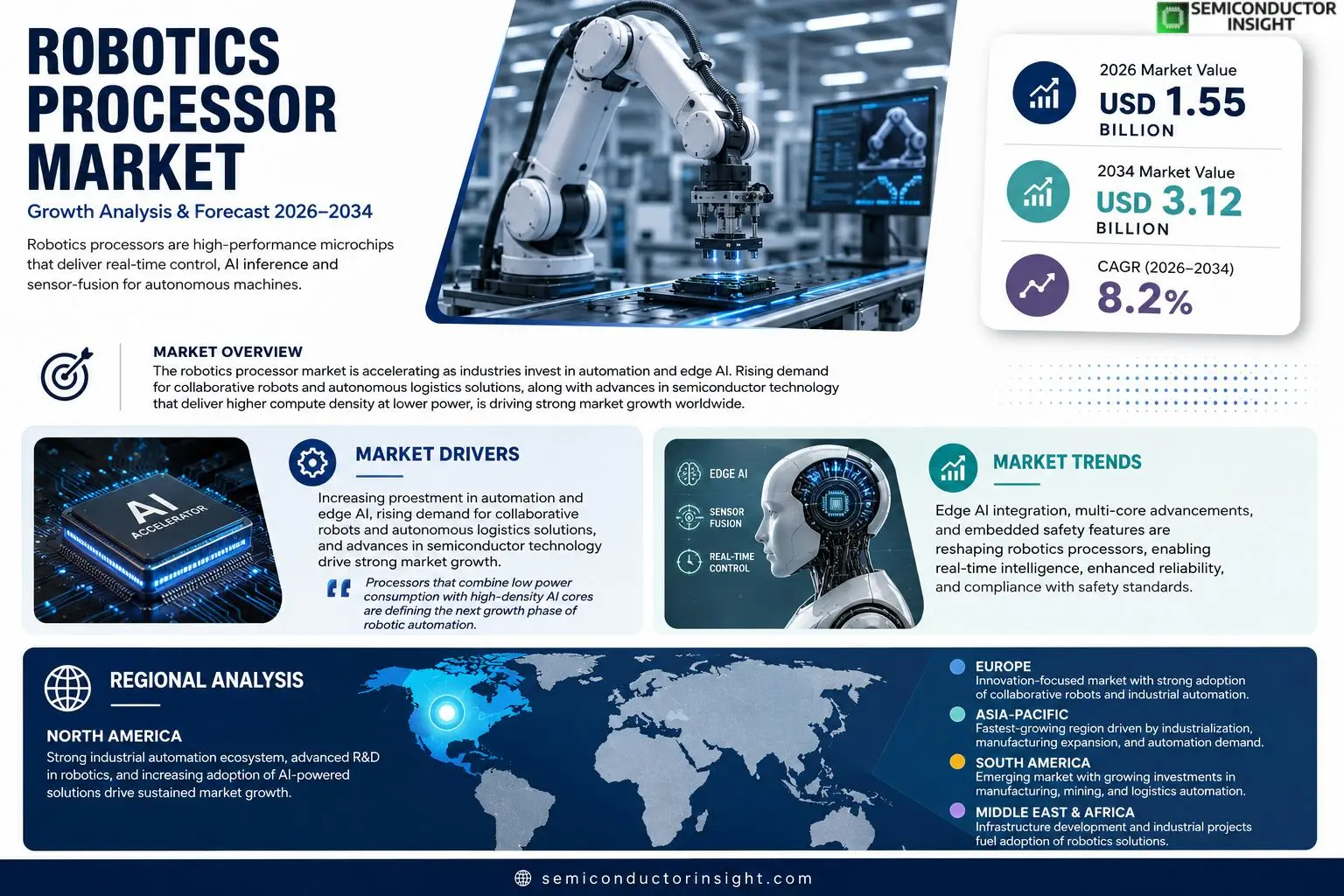

Robotics Processor market size was valued at USD 1.42 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 8.2% during the forecast period.

Robotics processors are high‑performance microchips engineered for real‑time control, AI inference and sensor‑fusion tasks within autonomous machines. They combine multi‑core CPUs, GPUs or dedicated AI accelerators with low‑latency I/O interfaces and rugged packaging to satisfy the intensive computational demands of industrial robots, service robots and autonomous vehicles.The market is accelerating because manufacturers are investing heavily in automation and edge AI while demand for collaborative robots and autonomous logistics solutions keeps rising. Furthermore, advances in semiconductor technology enable higher compute density at lower power consumption, prompting key players such as NVIDIA, Intel (Mobileye), Qualcomm, Texas Instruments and STMicroelectronics to expand their robotics‑processor portfolios.

MARKET DRIVERS

Growing Automation Demand Across Industries

The increasing adoption of collaborative robots in manufacturing, logistics, and healthcare is fueling demand for high‑performance compute units. As factories shift toward flexible production lines, Robotics Processor Market benefits from sustained capital investment aimed at improving throughput and reducing labor costs.

Advancements in AI and Edge Computing

Modern robotics processors now embed AI inference engines that enable real‑time decision making at the edge. This capability reduces latency and bandwidth requirements, making intelligent automation more viable for on‑site deployments. Consequently, vendors are accelerating product roadmaps to capture this technological shift.

➤ “Processors that combine low power consumption with high‑density AI cores are defining the next growth phase of robotic automation.”

In addition, the convergence of 5G connectivity with edge‑optimized processors is expanding the scope of autonomous mobile robots, further propelling Robotics Processor Market into new service‑oriented segments.

MARKET CHALLENGES

Technical Integration Barriers

Integrating sophisticated processors into legacy robot platforms often requires extensive firmware redesign and validation cycles. These engineering complexities can delay time‑to‑market and increase development costs, posing a challenge for smaller system integrators.

Other Challenges

Cost Constraints

The premium pricing of advanced AI‑enabled chips can deter adoption in cost‑sensitive applications such as consumer robotics, limiting market penetration despite clear performance benefits.

MARKET RESTRAINTS

Regulatory and Safety Standards

Robotic systems operating in safety‑critical environments must comply with stringent standards (e.g., ISO 10218, ANSI/RIA R15.06). Certification processes can prolong product launches and increase compliance costs, acting as a restraint on rapid market expansion.

MARKET OPPORTUNITIES

Emerging Applications in Service Robotics

The growing demand for service robots in retail, hospitality, and eldercare creates a sizable opportunity for specialized processors optimized for low‑power, high‑reliability operation. Companies that tailor their silicon to these niche workloads can capture premium pricing and differentiate from generic industrial solutions.

Robotics Processor Market Trends

Edge AI Integration Accelerates Processor Demand

The emergence of edge artificial intelligence has reshaped the design priorities for robotics processors. Manufacturers now require chips that can execute AI inference locally, reducing latency and dependence on cloud connectivity. This shift is evident in the growing adoption of heterogeneous architectures that blend CPU cores with dedicated neural engines. By processing sensor data and decision‑making algorithms on‑board, robots achieve more reliable real‑time performance in collaborative and logistics applications. The convergence of edge AI and robotics creates a feedback loop: as processors become more capable, robot manufacturers expand autonomous functionalities, further driving demand for high‑throughput, low‑power chips.

Other Trends

Advances in Multi‑Core Architectures

Recent semiconductor roadmaps emphasize the scaling of core counts without proportionally increasing power draw. Multi‑core designs enable parallel execution of motion control, vision processing, and AI workloads, which is critical for complex industrial robots operating in dynamic environments. Chip vendors are integrating tightly coupled cores that share high‑speed caches, allowing deterministic response times essential for safety‑critical tasks. The result is a noticeable migration from single‑core legacy parts to scalable, modular processor families that can be customized for specific robotic applications.

Integration of Safety‑Critical Features

Regulatory scrutiny surrounding collaborative robots has prompted processor makers to embed safety functions directly into silicon. Features such as fault detection, watchdog timers, and functional safety monitors are now standard in many new processor families. By offering certified safety‑critical blocks, vendors reduce the need for external safety controllers, simplifying system architecture and lowering overall system cost. This integration also shortens development cycles for robot manufacturers, who can rely on built‑in compliance with international safety standards while still delivering high computational performance.

COMPETITIVE LANDSCAPEKey Industry Players

Robotics Processor Market: Competitive Overview

The robotics processor sector is dominated by a handful of semiconductor giants that leverage deep AI‑inference expertise and mature manufacturing footprints. NVIDIA leads with its Jetson family, offering GPU‑centric compute platforms that enable real‑time vision and reinforcement‑learning workloads in collaborative robots and autonomous mobile units. Intel, through its Mobileye acquisition and Xeon‑based edge processors, provides a strong CPU‑AI hybrid architecture favored by manufacturers seeking tight integration with autonomous‑vehicle stacks. Qualcomm’s Snapdragon Robotics line combines high‑performance ARM cores with dedicated AI accelerators, targeting low‑power collaborative and service robots. Texas Instruments continues to differentiate with robust, industrial‑grade DSPs and mixed‑signal solutions that excel in deterministic control loops, while STMicroelectronics supplies a broad portfolio of microcontrollers and safety‑rated processors for safety‑critical robotic applications. Collectively, these leaders shape a market structure where revenue concentration exceeds 55 % and product roadmaps are increasingly aligned with edge‑AI trends, driving a competitive emphasis on power efficiency, thermal management, and software ecosystem support.Beyond the dominant tier, a vibrant cohort of niche innovators supplies specialized capabilities that address emerging segments such as swarm robotics, medical assistive devices, and high‑precision automation. AMD’s acquisition of Xilinx has introduced reconfigurable FPGA‑based processors that enable on‑the‑fly hardware acceleration for adaptable robotic workloads. Samsung Electronics brings advanced System‑in‑Package (SiP) technologies that shrink form factors for wearable and small‑scale robots. NXP Semiconductors focuses on secure, automotive‑grade processors that cater to safety‑critical logistics robots. Renesas Electronics and Infineon Technologies provide ultra‑low‑latency MCUs optimized for motor‑control and sensor‑fusion, while MediaTek is expanding into edge‑AI chips for consumer‑grade service robots. These players enrich the competitive landscape by fostering differentiation through custom silicon, rigorous functional safety compliance, and cost‑effective solutions for mid‑market deployments.

List of Key Robotics Processor Companies Profiled

- NVIDIA

- Intel (Mobileye)

- Qualcomm

- Texas Instruments

- STMicroelectronics

- AMD

- Samsung Electronics

- NXP Semiconductors

- Renesas Electronics

- Infineon Technologies

- MediaTek

- Microchip Technology

- Apple

- Google (Coral Edge TPU)

- Huawei (HiSilicon Robotics)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI Accelerators dominate due to their capacity to handle intensive AI inference and sensor‑fusion workloads; they enable real‑time decision making essential for collaborative and autonomous robots; manufacturers prioritize low‑latency architectures that integrate tightly with vision and perception modules. |

| By Application |

|

Industrial Automation remains the leading application as manufacturers embed processors to realize high‑speed precision control; collaborative robots benefit from processors that blend safety‑centric logic with AI‑driven adaptability; logistics platforms prioritize rugged processors capable of sustaining continuous operation in dynamic warehouse environments. |

| By End User |

|

System integrators drive adoption by tailoring processor solutions to diverse robotic platforms; automotive manufacturers focus on processors that support safety‑critical autonomous functions; electronics integrators emphasize modularity and ease of integration within larger automation ecosystems. |

| By Technology |

|

Edge AI processing emerges as the leading technology because it reduces reliance on cloud latency, allowing robots to make instantaneous decisions; sensor‑fusion engines are valued for their ability to combine visual, tactile, and proprioceptive data into coherent action plans; real‑time control loops are essential for precision motion and safety compliance. |

| By Deployment Scenario |

|

Mobile autonomous platforms lead the scenario space as they demand processors that balance compute density with power efficiency for prolonged operation; fixed manufacturing cells rely on highly deterministic processors to guarantee repeatable cycle times; cloud‑connected service fleets prioritize secure, upgradable processor architectures to enable over‑the‑air enhancements. |

Regional Analysis: North America

North America

The industrial sector in North America is a major driver for robotics processor demand, with increasing adoption in manufacturing, logistics, and warehousing. The need for automation in these sectors to improve efficiency, reduce costs, and enhance safety is propelling the growth of advanced robotics solutions.

The healthcare industry is witnessing a growing integration of robotics processors in surgical robots, rehabilitation robots, and automated dispensing systems. The increasing demand for minimally invasive procedures and personalized patient care is driving innovation in this segment.

North America has a significant defense sector that utilizes robotics processors in unmanned aerial vehicles (UAVs), ground robots, and surveillance systems. The need for enhanced capabilities in autonomous operations and data analysis fuels the demand for high-performance processors in this area.

The e-commerce boom and the increasing complexity of supply chains are driving the adoption of robots in warehouses and logistics centers. Robotics processors are crucial for enabling autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) to navigate and perform tasks efficiently.

Europe

Europe presents a diverse robotics processor market, with significant growth opportunities in manufacturing, healthcare, and logistics. The region is characterized by a strong emphasis on innovation, particularly in areas like collaborative robotics and AI-powered solutions. Government initiatives supporting automation and industrial digitalization are further boosting the market. Key trends include the development of energy-efficient processors and the increasing use of robotics in elder care. Business strategies often focus on collaboration with research institutions and participation in European Union-funded projects to drive innovation. The European market is also sensitive to data privacy regulations, influencing the design and deployment of robotics processors.

Asia-Pacific

Asia-Pacific is poised for the fastest growth in Robotics Processor Market, driven by rapid industrialization in countries like China, Japan, and South Korea. The region’s manufacturing sector is a major consumer of robotics solutions, and the increasing adoption of automation across various industries is fueling demand for these processors. Key trends include the rise of service robots, the growth of the logistics sector, and the development of advanced robotics applications in agriculture and mining. Business strategies in Asia-Pacific often focus on cost-effectiveness and localization to meet the specific needs of regional markets. The strong government support for technological advancements and the availability of a large, skilled workforce are key factors driving market growth.

South America

Robotics Processor Market in South America is an emerging market with significant potential. The region’s manufacturing and agricultural sectors are increasingly adopting automation technologies to improve efficiency and productivity. The demand for robotics processors is expected to grow steadily in the coming years, driven by investments in infrastructure and technological upgrades. Key trends include the adoption of robots in mining operations, the development of agricultural robots, and the use of robotics in logistics and warehousing. Business strategies in South America often focus on providing cost-effective solutions and building strong relationships with local partners.

Middle East & Africa

Robotics Processor Market in the Middle East & Africa is a developing market with growing opportunities. The region’s investments in infrastructure development, particularly in logistics and construction, are driving the adoption of robotics solutions. The demand for robotics processors is expected to increase in the coming years, with a focus on applications in warehousing, agriculture, and defense. Key trends include the deployment of robots in oil and gas operations and the development of autonomous vehicles. Business strategies in the Middle East & Africa often involve partnerships with international technology providers and a focus on meeting the specific needs of the region’s industries.

Report Scope

This market research report provides a comprehensive analysis of the Robotics Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Robotics Processor Market?

-> Robotics Processor Market was valued at USD 1.42 billion in 2025 and is expected to reach USD 3.12 billion by 2034.

Which key companies operate in Robotics Processor Market?

-> Key players include NVIDIA, Intel (Mobileye), Qualcomm, Texas Instruments, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing investment in automation and edge AI, rising demand for collaborative robots and autonomous logistics solutions, and advances in semiconductor technology that deliver higher compute density at lower power consumption.

Which region dominates the market?

-> The reference does not specify a single dominant region; it describes the market as , driven by worldwide adoption of robotics and AI technologies.

What are the emerging trends?

-> Emerging trends include the integration of AI inference within robotics processors, sensor‑fusion capabilities for real‑time decision making, and the development of rugged, low‑latency microchips tailored for industrial, service and autonomous vehicle applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...