RISC-V Microprocessor Market Insights

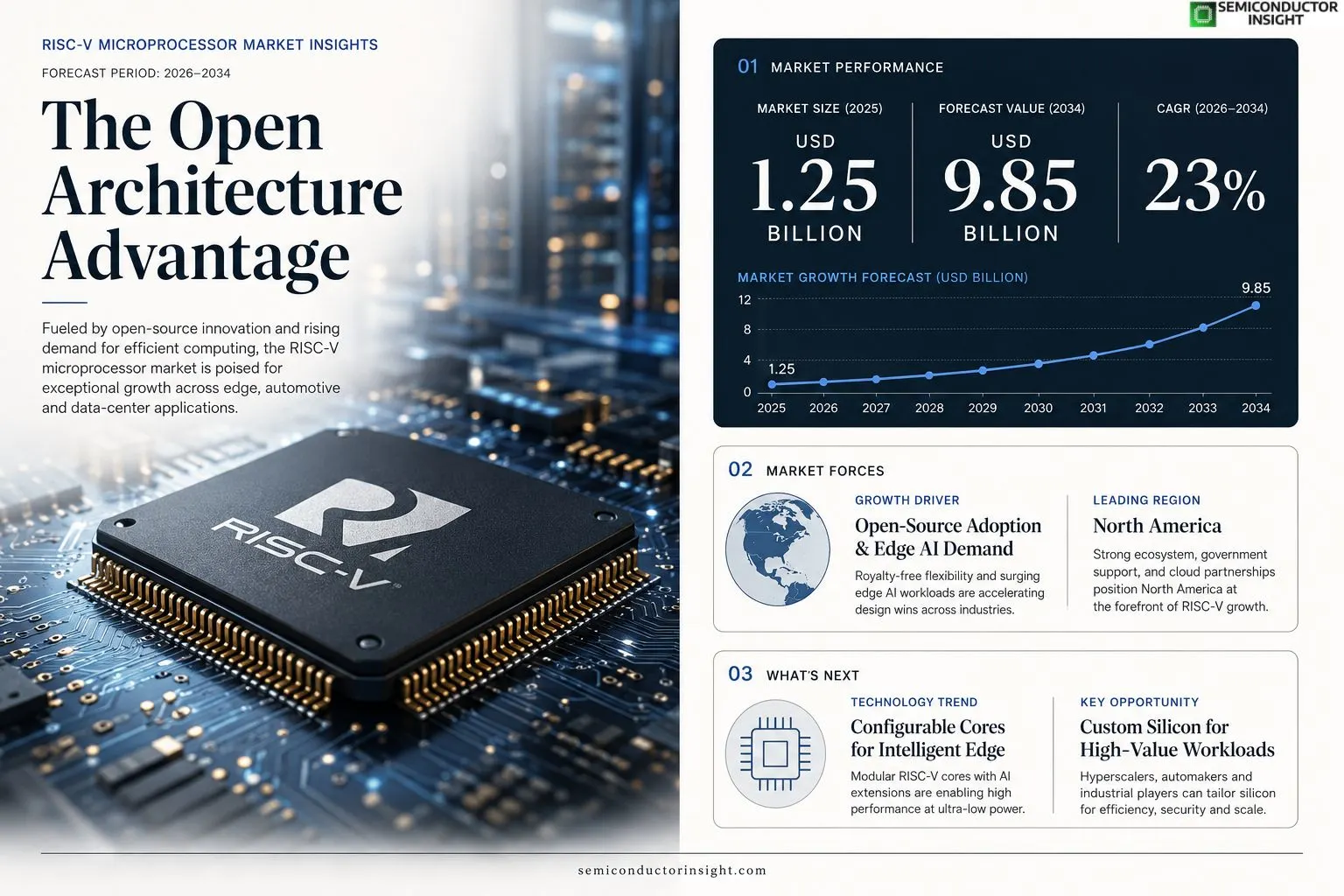

RISC-V microprocessor market size was valued at USD 1.25 billion in 2025. The market is projected to grow from USD 1.25 billion in 2025 to USD 9.85 billion by 2034, exhibiting a CAGR of 23% during the forecast period.

RISC-V microprocessors are open‑source instruction set architecture (ISA) based chips that enable highly customizable hardware designs across embedded systems, automotive electronics, edge AI devices and data‑center accelerators. Because the ISA is royalty‑free, designers can tailor core implementations while preserving software compatibility.The market is accelerating due to expanding open‑source ecosystems, increased semiconductor fab capacity dedicated to RISC-V designs, and strategic alliances among silicon vendors and cloud providers.

For instance, SiFive announced a partnership with Google Cloud in early 2024 to deliver pre‑validated RISC-V cores for edge compute services.

Other notable players such as Western Digital, Alibaba’s T-Head, Qualcomm and NVIDIA are actively developing or integrating RISC-V IP into their product roadmaps.

MARKET DRIVERS

Open‑Source Architecture Adoption

The rising interest in open‑source silicon enables chip designers to bypass costly licensing fees, accelerating time‑to‑market for new products. Companies across the semiconductor value chain are integrating the RISC‑V instruction set to reduce development costs while maintaining design flexibility.

Emerging Edge AI Demand

Edge AI workloads require energy‑efficient processors, and the modular nature of RISC‑V cores offers tailored power/performance trade‑offs. This has led to a surge in deployments for smart sensors, autonomous drones, and low‑latency inference devices.

➤ “RISC‑V’s flexibility fuels innovation across sectors, creating a virtuous cycle of adoption and ecosystem growth.”

These drivers collectively boost the adoption curve, positioning the RISC‑V Microprocessor Market for sustained expansion over the next five years.

MARKET CHALLENGES

IP Licensing and Ecosystem Fragmentation

Despite its open nature, the market faces fragmented IP portfolios, making integration across heterogeneous toolchains complex. Companies often encounter compatibility issues when combining third‑party extensions, which can delay product launches.

Other Challenges

Supply Chain Constraints

Global semiconductor shortages limit the availability of fab capacity for custom RISC‑V silicon, driving up lead times and compelling firms to rely on legacy processes for interim production.

MARKET RESTRAINTS

Standardization Uncertainty

The absence of a universally accepted RISC‑V compliance suite creates hesitation among large OEMs, who prefer mature, fully standardized instruction sets for mission‑critical applications.Toolchain maturity is still evolving; while major EDA vendors have introduced RISC‑V support, many advanced verification features lag behind those available for established architectures.Security concerns also linger, as the openness of the architecture can expose potential attack vectors if robust verification and certification processes are not uniformly applied.

MARKET OPPORTUNITIES

Growth in Automotive and IoT

Automakers are increasingly adopting RISC‑V cores for next‑generation infotainment and advanced driver‑assistance systems, capitalizing on the architecture’s ability to support custom safety extensions. Simultaneously, the IoT sector benefits from low‑cost, low‑power designs that can be rapidly customized for diverse device classes.Custom silicon for data centers presents a lucrative avenue, as hyperscale operators seek energy‑efficient processors that can be fine‑tuned for specific workloads, reducing total cost of ownership.Government initiatives in several regions provide funding and policy incentives for open‑source hardware development, fostering startups and academic collaborations that enrich the RISC‑V ecosystem.

RISC-V Microprocessor Market Trends

Open‑Source Ecosystem Expansion

RISC-V Microprocessor Market is being driven by a rapidly maturing open‑source ecosystem. Designers are attracted to the royalty‑free instruction set, which enables them to modify core implementations without licensing constraints. Recent contributions from academic institutions, startups, and large silicon vendors have enriched available IP libraries, verification tools, and software stacks. This collaborative environment reduces time‑to‑market for custom silicon, especially in embedded and edge applications. As more development boards and reference designs become publicly available, the barrier to entry lowers, encouraging a broader base of engineers to adopt RISC‑V solutions. The result is a self‑reinforcing cycle of innovation that sustains demand across multiple verticals.

Other Trends

Strategic Partnerships with Cloud Platforms

Leading cloud providers are integrating RISC‑V cores into their edge‑compute services, creating a direct pathway for developers to deploy workloads on open‑source hardware. A notable collaboration announced in early 2024 linked pre‑validated RISC‑V cores with a major cloud ecosystem, offering users a turnkey solution for low‑latency inference and data processing at the network edge. These alliances not only validate the technology stack but also provide scalability through elastic cloud resources. As more enterprises seek cost‑effective, customizable compute nodes, the synergy between cloud platforms and RISC‑V hardware is expected to accelerate adoption across AI, IoT, and real‑time analytics use cases.

Diversification into Edge AI and Automotive

The RISC‑V Microprocessor Market is extending its reach into edge AI and automotive electronics, where power efficiency and deterministic performance are critical. Chip manufacturers are delivering specialized RISC‑V cores that embed vector extensions and safety‑critical features required for autonomous driving systems and sensor fusion. Simultaneously, AI accelerators built on RISC‑V ISA are emerging to handle inference workloads directly on devices, reducing reliance on centralized cloud processing. This diversification is supported by increased fab capacity dedicated to RISC‑V designs, enabling volume production at competitive cost points. Collectively, these trends position the market for sustained growth as system architects prioritize flexibility, security, and low total cost of ownership.

COMPETITIVE LANDSCAPEKey Industry Players

RISC‑V Microprocessor Market: Competitive Dynamics and Growth Outlook

The RISC‑V ecosystem is anchored by SiFive, the first commercial provider of open‑source RISC‑V cores, which commands a dominant IP licensing share and drives the reference‑design market. SiFive’s strategic partnership with Google Cloud enables pre‑validated edge compute solutions, reinforcing a tiered market structure where a few IP vendors supply base architectures to a broad set of fabless and IDM manufacturers. Western Digital’s in‑house RISC‑V development for storage‑class processors and Alibaba’s T‑Head division, delivering the “Xuantie” family, illustrate how large silicon players are integrating open‑source cores to diversify product portfolios while leveraging royalty‑free ISA benefits. Qualcomm and NVIDIA have entered the space, announcing exploratory RISC‑V IP roadmaps that signal a gradual convergence of traditional processor vendors with the open‑source model, potentially reshaping competitive dynamics over the next decade.Beyond the headline makers, a vibrant cohort of niche innovators sustains the depth of the RISC‑V supply chain. Andes Technology supplies ultra‑low‑power cores for IoT and automotive edge nodes, while Codasip offers customizable processor generators for security‑critical applications. Esperanto Technologies focuses on high‑performance AI accelerators, and Microchip provides 8‑bit and 32‑bit RISC‑V MCUs for embedded control. Horizon Robotics and StarFive target AI‑driven vision and edge‑server markets respectively, and Bluespec delivers high‑productivity hardware design tools that accelerate RISC‑V core creation. This diverse set of specialized players expands the ecosystem, fostering rapid innovation and enabling customers to source tailored silicon solutions across multiple verticals.

List of Key RISC‑V Microprocessor Companies Profiled

- SiFive

- SiFive

- Western Digital

- Western Digital

- Alibaba T‑Head

- Alibaba T‑Head

- Qualcomm

- Qualcomm

- NVIDIA

- Andes Technology

- Codasip

- Esperanto Technologies

- Microchip Technology

- Horizon Robotics

- StarFive

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

General‑Purpose Cores are emerging as the leading segment because they provide a versatile foundation that can be easily extended for diverse workloads. • Designers value the open‑source nature that enables rapid iteration without licensing friction. • Compatibility with existing software stacks accelerates adoption across startups and established firms. • The flexibility to integrate custom extensions fosters innovation in emerging device categories. |

| By Application |

|

Edge AI and IoT Devices dominate this dimension as developers seek low‑power, highly configurable compute that can be tailored to sensor fusion and on‑device inference. • The royalty‑free ISA encourages integration into cost‑sensitive consumer products. • Strong collaboration with cloud providers ensures seamless model deployment at the edge. • Robust open‑source toolchains lower the barrier for smaller teams to bring differentiated solutions to market. |

| By End User |

|

Semiconductor Companies are the primary drivers because they can embed RISC‑V cores directly into silicon, leveraging design freedom to differentiate product portfolios. • Access to a shared ecosystem reduces development risk and time‑to‑market. • Collaborative development models enable joint innovation with software partners. • The ability to offer differentiated extensions meets niche market demands while preserving a common software base. |

| By Ecosystem Partnerships |

|

Open‑Source Community Initiatives lead this segment by fostering a vibrant pool of shared IP, verification suites, and documentation. • Continuous contributions accelerate feature evolution without centralized control. • Partnerships with cloud platforms provide validated edge compute offerings that showcase RISC‑V capabilities. • Foundry collaborations ensure manufacturing readiness, reducing time and cost for early adopters. |

| By Design Flexibility |

|

Configurable Core Templates dominate this category as they empower developers to tailor instruction sets, cache hierarchies, and peripheral interfaces to exact use‑case requirements. • Modular extensions enable rapid adaptation for specialized workloads. • The absence of royalty constraints encourages deep customization. • Seamless integration with existing software ecosystems sustains developer productivity while delivering differentiated hardware performance. |

Regional Analysis: North America

United States

Government support for RISC-V adoption through funding and strategic partnerships is a major driver of growth in the United States. This includes initiatives aimed at promoting open-source hardware and fostering innovation in semiconductor design.

The increasing demand for AI and edge computing solutions is creating significant opportunities for RISC-V processors in the United States. The flexibility and customizability of RISC-V are well-suited to these demanding applications.

The United States boasts a mature and highly developed semiconductor industry ecosystem, providing a strong foundation for RISC-V growth. This includes a network of design houses, foundries, and equipment suppliers.

Numerous universities and research institutions across the United States are actively engaged in RISC-V research and development, contributing to advancements in the technology.

Europe

Europe represents a significant and steadily growing market for RISC-V Microprocessors. Driven by a strong emphasis on data privacy, security, and industrial automation, European nations are actively exploring and adopting RISC-V as an alternative to proprietary processor architectures. The region’s commitment to technological sovereignty is a key factor fueling this trend, with governments encouraging the development of domestic semiconductor capabilities. Focus areas include automotive, industrial IoT, and specialized computing. The emphasis on open standards aligns well with European values and promotes interoperability. The market is characterized by a blend of established semiconductor players and innovative startups.

Asia-Pacific

Asia-Pacific is emerging as a dynamic and rapidly expanding market for RISC-V Microprocessors. Led by countries like China, Japan, and South Korea, the region’s robust manufacturing base, large consumer electronics market, and increasing demand for IoT devices are driving adoption. China’s strategic focus on self-sufficiency in semiconductors is a major catalyst, with RISC-V being viewed as a critical technology for achieving this goal. The region’s competitive landscape includes both established players and a surge of new entrants. Key applications include telecommunications infrastructure, automotive electronics, and consumer devices. The emphasis on cost-effectiveness and scalability is particularly important in this market.

South America

South America presents a nascent but promising market for RISC-V Microprocessors. The region’s growing industrial sector, increasing digital connectivity, and expanding IoT deployments are creating opportunities for RISC-V adoption. While the market is currently smaller than in North America or Asia-Pacific, there is increasing interest from telecommunications companies and industrial automation providers. Government initiatives aimed at promoting technological development are also contributing to market growth. The focus is on cost-effective solutions for various applications, particularly in areas like agriculture and logistics.

Middle East & Africa

The Middle East and Africa represent a relatively untapped market for RISC-V Microprocessors, but with significant potential for future growth. The region’s increasing investments in smart city initiatives, industrial digitalization, and telecommunications infrastructure are driving demand for advanced processor solutions. Several countries are exploring RISC-V for applications such as smart grids, connected vehicles, and industrial automation. The focus is on building resilient and secure digital infrastructure. Government support for technological innovation and diversification of economies is expected to further spur RISC-V adoption in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the RISC-V Microprocessor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RISC-V Microprocessor Market?

-> RISC-V Microprocessor Market was valued at USD 1.25 billion in 2025 and is expected to reach USD 9.85 billion by 2034.

Which key companies operate in RISC-V Microprocessor Market?

-> Key players include SiFive, Western Digital, Alibaba’s T‑Head, Qualcomm, and NVIDIA, among others.

What are the key growth drivers?

-> Key growth drivers include expanding open‑source ecosystems, increased semiconductor fab capacity dedicated to RISC‑V designs, and strategic alliances among silicon vendors and cloud providers.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include greater adoption of open‑source ISA, collaboration between chipmakers and cloud platforms, and the rise of edge‑AI accelerators built on RISC‑V.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...