MARKET INSIGHTS

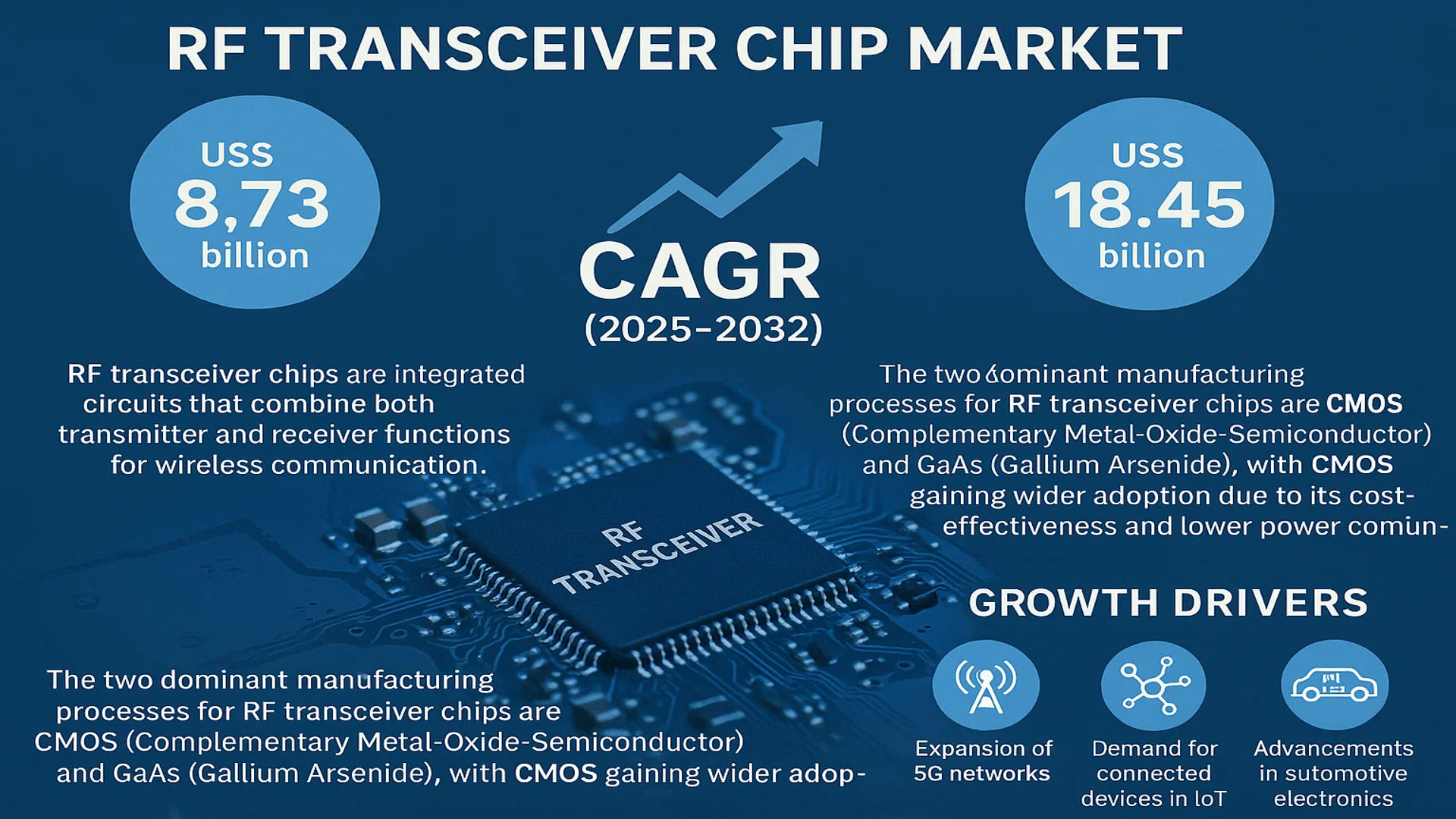

The global RF Transceiver Chip Market size was valued at US$ 8.73 billion in 2024 and is projected to reach US$ 18.45 billion by 2032, at a CAGR of 11.3% during the forecast period 2025-2032.

RF transceiver chips are integrated circuits that combine both transmitter and receiver functions for wireless communication. These chips are essential components in modern wireless systems, facilitating the transmission and reception of radio frequency signals across various applications. The two dominant manufacturing processes for RF transceiver chips are CMOS (Complementary Metal-Oxide-Semiconductor) and GaAs (Gallium Arsenide), with CMOS gaining wider adoption due to its cost-effectiveness and lower power consumption.

The market growth is primarily driven by the rapid expansion of 5G networks, increasing demand for connected devices in IoT applications, and advancements in automotive electronics. However, challenges such as design complexity and rising production costs may temporarily restrain growth in certain segments. Key players like Qualcomm, Broadcom, and NXP Semiconductors are investing heavily in next-generation RF solutions to capitalize on emerging opportunities in 5G infrastructure and smart city applications.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Accelerates RF Transceiver Chip Demand

The global rollout of 5G networks has become a significant catalyst for RF transceiver chip adoption. With over 300 commercial 5G networks now deployed worldwide, the requirement for high-performance RF solutions has intensified. These chips form the backbone of 5G infrastructure, enabling faster data transmission and lower latency. The transition from 4G to 5G requires sophisticated RF front-end modules where transceiver chips play a pivotal role in signal processing and modulation. Mobile operators are investing heavily in network upgrades, with capital expenditures projected to grow annually by approximately 8% through 2027, directly benefiting RF component suppliers.

Proliferation of IoT Devices Fuels Market Expansion

Internet of Things (IoT) applications are driving unprecedented demand for wireless connectivity solutions. RF transceiver chips enable communication between billions of IoT devices across industrial automation, smart cities, and consumer electronics. The global IoT market is expected to exceed 30 billion connected devices by 2030, with each requiring RF components for wireless operation. Smart home applications alone account for nearly half of all consumer IoT installations, creating sustained demand for cost-effective RF solutions that balance performance with power efficiency.

Automotive Connectivity Revolution Creates New Growth Avenues

The automotive industry’s shift toward connected and autonomous vehicles presents a major opportunity for RF transceiver manufacturers. Modern vehicles incorporate multiple wireless systems including cellular V2X, Wi-Fi, Bluetooth, and GNSS – each requiring specialized RF chips. The average new car now contains over 30 RF components, a number expected to double by 2028 as vehicle-to-everything (V2X) communication becomes standard. Electric vehicle adoption further accelerates this trend, as smart charging infrastructure relies on robust wireless communication links enabled by advanced RF transceivers.

MARKET RESTRAINTS

Semiconductor Supply Chain Disruptions Impact Production Capacity

The RF transceiver market faces significant headwinds from ongoing semiconductor supply chain challenges. Chip shortages that began during the pandemic continue to affect production schedules, with lead times for some RF components extending beyond 40 weeks. This volatility stems from complex factors including geopolitical tensions, raw material scarcity, and concentrated manufacturing capacity. Over 70% of advanced semiconductor manufacturing occurs in a single region, creating vulnerability to trade restrictions and natural disasters.

Design Complexity Increases Development Costs

As wireless standards evolve, RF transceiver chips must support an expanding range of frequencies and protocols within shrinking form factors. Developing multi-band, multi-protocol solutions requires substantial R&D investment, with advanced node designs costing upwards of $10 million per project. Smaller geometry processes (below 28nm) necessary for cutting-edge performance carry yield challenges that impact profitability. Many manufacturers struggle to recoup these investments amid intense price competition, particularly in consumer electronics applications.

MARKET CHALLENGES

Thermal Management Issues in Compact Designs

Miniaturization trends in electronics create significant thermal challenges for RF transceiver chips. As package sizes shrink, heat dissipation becomes increasingly problematic – a critical issue since RF components are particularly sensitive to temperature variations. Performance degradation at elevated temperatures can reduce signal integrity by up to 30%, impacting overall system reliability. Designers must implement sophisticated thermal management solutions, adding complexity and cost to end products.

RF Spectrum Congestion Creates Interference Issues

The explosive growth of wireless devices has led to severe spectrum congestion, particularly in the 2.4GHz and 5GHz bands. This environment demands increasingly sophisticated filtering and interference mitigation capabilities in transceiver designs. Coexistence between competing wireless standards (Wi-Fi 6, 5G, Bluetooth Low Energy) requires advanced adaptive algorithms that add design complexity. Regulatory requirements for spurious emissions continue to tighten, forcing manufacturers to implement more stringent testing protocols that extend development timelines.

MARKET OPPORTUNITIES

Emerging 6G Research Opens New Frontiers

While 5G deployments continue, research into 6G technologies presents exciting opportunities for RF transceiver innovation. Early development focuses on terahertz frequency bands (100GHz-3THz) that promise staggering data rates. Prototype 6G transceivers already demonstrate performance benchmarks 50 times faster than current 5G solutions. Governments worldwide have committed over $4 billion to 6G research initiatives, creating a pipeline for next-generation RF component development.

Integration of AI in RF Systems Enhances Performance

Artificial intelligence integration represents a transformative opportunity for RF transceiver technology. Machine learning algorithms enable real-time optimization of signal parameters, improving spectral efficiency by up to 40% in field trials. AI-powered transceivers can autonomously adjust to changing environmental conditions, reducing interference and power consumption. Major chipmakers are actively developing AI-accelerated RF solutions, with prototypes demonstrating significant improvements in beamforming accuracy and channel estimation.

Medical IoT Applications Drive Specialized Demand

The healthcare sector’s digital transformation creates specialized opportunities for RF transceiver applications. Wireless medical devices require ultra-reliable, low-power RF solutions with stringent regulatory compliance. Emerging applications like implantable monitors and smart drug delivery systems demand customized transceivers with enhanced security features. The medical IoT segment is projected to grow at 25% CAGR through 2030, presenting a high-value niche for RF component suppliers.

RF TRANSCEIVER CHIP MARKET TRENDS

5G Rollout Drives Exponential Growth in RF Transceiver Chip Demand

The global RF transceiver chip market is experiencing unprecedented growth due to large-scale 5G network deployments across multiple regions. Millimeter-wave (mmWave) and sub-6GHz frequency bands require highly efficient RF transceivers capable of handling increased data throughput with minimal latency. While traditional 4G LTE chips operated below 6GHz, modern 5G transceivers must support frequencies up to 52GHz, necessitating significant technological advancements in power efficiency and thermal management. The market for sub-6GHz RF transceivers alone is projected to grow at a CAGR of approximately 18% through 2028, with mmWave chips following closely behind.

Other Trends

Integration of AI Enables Smart RF Communication

The integration of artificial intelligence into RF transceiver chips has emerged as a key market differentiator, enabling dynamic frequency selection and adaptive signal processing. These AI-powered chips optimize power consumption in real-time based on network conditions, extending battery life in IoT devices by up to 30% compared to conventional designs. Furthermore, machine learning algorithms help mitigate interference in congested spectrum environments, significantly improving signal quality in dense urban deployments.

Automotive Sector Accelerates Chip Innovation

The automotive industry’s transition towards vehicle-to-everything (V2X) communication has created substantial demand for specialized RF transceivers supporting DSRC and C-V2X protocols. With modern vehicles requiring up to 15 separate RF modules for various functions including navigation, collision avoidance, and infotainment systems, the automotive segment now accounts for over 20% of the total RF transceiver market. The development of integrated radar and communication transceivers in the 76-81GHz band represents one of the most significant technical breakthroughs, enabling simultaneous object detection and high-speed data transmission.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Accelerate Innovation to Capture 5G and IoT Opportunities

The global RF transceiver chip market exhibits a dynamic competitive landscape dominated by semiconductor giants, while emerging players focus on niche applications. Broadcom and Qualcomm (via its RF front-end divisions) lead with nearly 30% combined market share in 2024, attributed to their end-to-end 5G solutions and established relationships with smartphone OEMs. Their dominance is further reinforced by extensive R&D budgets—Broadcom alone invested $4.9 billion in semiconductor R&D last fiscal year.

Analog Devices and Texas Instruments maintain strong positions in industrial and automotive segments, leveraging their expertise in low-power designs for IoT applications. Both companies recently launched ultra-wideband (UWB) transceivers, capitalizing on the growing demand for precise indoor positioning systems.

Meanwhile, Qorvo and Skyworks Solutions are aggressively expanding beyond mobile into automotive RADAR and infrastructure, with Qorvo’s recent $3 billion acquisition of a GaN specialist strengthening its base station chip portfolio. Their vertically integrated manufacturing allows tighter control over GaAs-based RF performance—a critical advantage as 5G mmWave deployments accelerate.

Chinese players like Great Microwave Technology and Shenzhen Hope Microelectronics are gaining traction in cost-sensitive consumer markets, supported by domestic semiconductor subsidies. However, geopolitical tensions have prompted Western firms like NXP Semiconductors to diversify supply chains, with new factories announced in Singapore and Austin to ensure resilience.

List of Key RF Transceiver Chip Manufacturers

- Broadcom Inc. (U.S.) – 5G integrated FEMs and mmWave modules

- Qualcomm Technologies, Inc. (U.S.) – Snapdragon RF systems

- Analog Devices, Inc. (U.S.) – High-performance transceivers for industrial IoT

- Texas Instruments (U.S.) – Low-power sub-GHz solutions

- Qorvo, Inc. (U.S.) – GaAs/GaN-based RF front-end modules

- Skyworks Solutions, Inc. (U.S.) – Mobile and automotive RFICs

- NXP Semiconductors (Netherlands) – Automotive V2X transceivers

- Infineon Technologies (Germany) – Radar and power-efficient designs

- Microchip Technology (U.S.) – Sub-6GHz IoT connectivity chips

- Great Microwave Technology (China) – Cost-optimized 4G/LTE transceivers

Segment Analysis:

By Type

Sub-1GHz Segment Dominates Due to Long-Range and Low-Power Consumption Advantages

The market is segmented based on type into:

- Sub-1GHz

- 2.4GHz

- 5GHz

- Dual-band

- Subtypes: 2.4GHz/5GHz, Sub-1GHz/2.4GHz, and others

- Multi-band

By Application

Consumer Electronics Segment Leads Owing to Proliferation of Smart Devices

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphones, Wearables, Smart TVs, and others

- Automotive Electronics

- Medical Equipment

- Communication Systems

- Industrial IoT

By Process Technology

CMOS Process Segment Holds Majority Share Due to Cost-Effectiveness

The market is segmented based on process technology into:

- CMOS

- GaAs

- SiGe

By Integration

Highly Integrated SoCs Gain Traction in Compact Device Designs

The market is segmented based on integration level into:

- Discrete RF Transceivers

- Integrated RF Transceivers

- System-on-Chip (SoC)

Regional Analysis: RF Transceiver Chip Market

Asia-Pacific

The Asia-Pacific region dominates the RF Transceiver Chip market, accounting for over 45% of global demand in 2024. This growth is fueled by China’s aggressive 5G rollout, with over 3.3 million 5G base stations deployed as of 2024, alongside India’s expanding telecommunications infrastructure. Japan and South Korea lead in automotive electronics adoption, where RF transceivers are critical for V2X (Vehicle-to-Everything) communication systems. The region benefits from established semiconductor manufacturing ecosystems in Taiwan and China, with foundries like TSMC and SMIC supporting localized production. However, increasing trade tensions and export controls on advanced chips present supply chain challenges for some markets.

North America

North America maintains technological leadership in RF transceiver innovation, driven by major players like Qorvo, Broadcom, and Analog Devices investing heavily in 6G research and mmWave technologies. The U.S. accounts for 60% of regional demand, with automotive (particularly EV charging communication systems) and aerospace/defense applications growing at 12% CAGR. Regulatory support through initiatives like the CHIPS Act has spurred domestic manufacturing, though high production costs compared to Asia remain a competitive disadvantage. Canada’s focus on IoT networks and Mexico’s growing automotive sector present complementary demand opportunities.

Europe

Europe’s market is characterized by stringent EM compliance standards (ETSI EN 300 328) driving demand for high-performance RF transceivers in industrial IoT and smart city applications. Germany leads with 28% market share in the region, supported by its automotive OEMs integrating advanced RF solutions for connected vehicles. The EU’s emphasis on Open RAN (Radio Access Network) deployments is creating new opportunities in telecom infrastructure, while the Nordic countries continue innovating in low-power RF designs for wearable medical devices. Brexit-related trade complexities have marginally impacted UK semiconductor imports, with local firms increasingly sourcing from EU-based suppliers.

South America

Market growth in South America remains constrained by economic instability, though Brazil shows promising adoption in smart utility meters using sub-1GHz RF transceivers. Argentina’s recent investments in satellite communication infrastructure have increased demand for space-grade RF solutions. The lack of local semiconductor manufacturing forces complete reliance on imports, with Chinese suppliers gaining market share through competitive pricing. Regulatory harmonization efforts under Mercosur could potentially improve market conditions, but progress remains slow compared to other regions.

Middle East & Africa

The UAE and Saudi Arabia are driving regional growth through smart city projects, with Dubai’s USD 8 billion IoT investment plan creating demand for 5G-compatible RF transceivers. Israel’s thriving defense sector utilizes specialized military-grade RF chips, while South Africa’s mining sector adopts RFID-based asset tracking solutions. Limited local technical expertise and high import duties hinder broader adoption, though partnerships with Asian manufacturers are gradually improving supply chain reliability. Sub-Saharan Africa’s mobile payment revolution continues to fuel demand for low-cost RF solutions in basic feature phones and POS terminals.

Report Scope

This market research report provides a comprehensive analysis of the global and regional RF Transceiver Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, frequency range, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, including CMOS and GaAs processes, 5G integration, IoT applications, and evolving wireless communication standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Transceiver Chip Market?

-> RF Transceiver Chip Market size was valued at US$ 8.73 billion in 2024 and is projected to reach US$ 18.45 billion by 2032, at a CAGR of 11.3% during the forecast period 2025-2032.

Which key companies operate in Global RF Transceiver Chip Market?

-> Key players include Broadcom, Qorvo, Analog Devices, NXP Semiconductors, Infineon Technologies, STMicroelectronics, Microchip Technology, and Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing adoption of IoT devices, automotive connectivity solutions, and growing demand for smart home technologies.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 45% share in 2024, driven by semiconductor manufacturing hubs in China, South Korea, and Taiwan, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration of AI in RF chips, development of mmWave transceivers for 5G applications, energy-efficient designs, and increasing adoption in automotive radar systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...