MARKET INSIGHTS

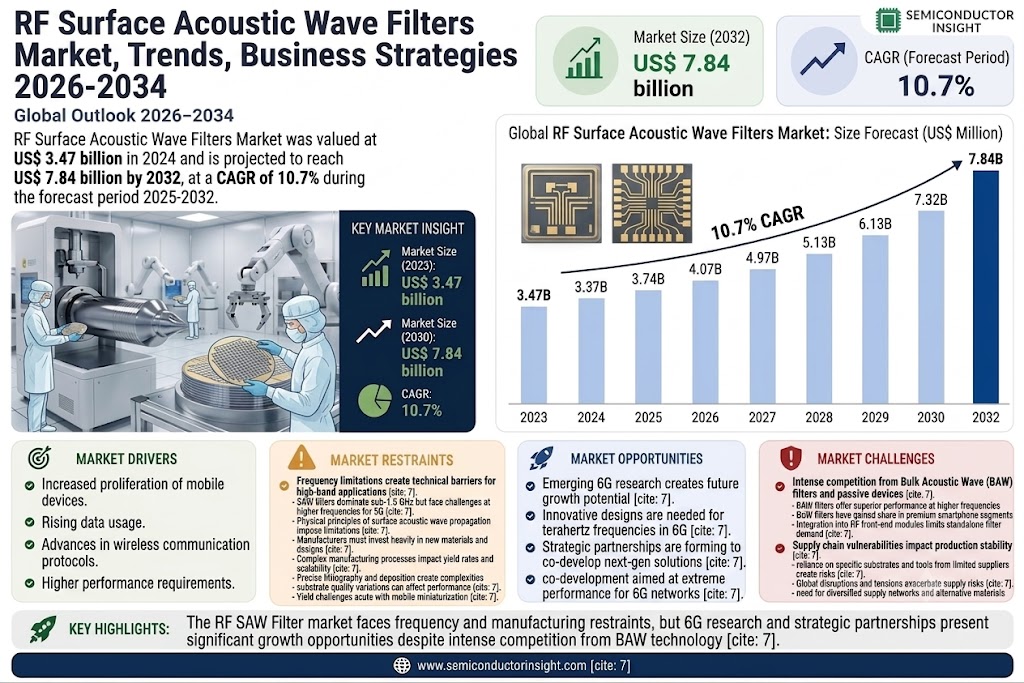

The global RF Surface Acoustic Wave Filters Market was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 7.84 billion by 2032, at a CAGR of 10.7% during the forecast period 2025-2032.

RF Surface Acoustic Wave (SAW) filters are specialized electronic components that use piezoelectric materials to convert electrical signals into acoustic waves and filter unwanted frequencies. These filters are critical for signal processing in wireless communication systems, enabling efficient frequency selection and noise reduction. The two primary types include transversal filters and resonator filters, each serving distinct applications across industries.

Market growth is driven by increasing demand for high-frequency communication technologies, including 5G networks and IoT devices. While the telecommunications sector dominates applications, consumer electronics and automotive industries are emerging as key growth areas due to rising adoption of connected devices. Leading players like Qualcomm, Murata Manufacturing, and TDK are investing in advanced SAW filter designs to meet the evolving requirements of next-generation wireless systems.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Driving Exponential Demand for RF SAW Filters

The rapid global rollout of 5G infrastructure represents the single largest growth driver for RF Surface Acoustic Wave Filters. With telecom operators investing heavily in 5G deployment, the demand for high-frequency RF components has surged exponentially. RF SAW filters are critical components in 5G-enabled devices, providing essential frequency selection and interference rejection capabilities. The global 5G smartphone penetration rate surpassed 50% in 2023, creating massive demand for these filters in mobile devices. Furthermore, the transition to millimeter-wave frequencies in advanced 5G networks requires specialized SAW filter designs capable of handling higher frequencies while maintaining signal integrity.

Proliferation of IoT Devices Creating New Application Verticals

The explosive growth of Internet of Things (IoT) devices across industrial, commercial, and consumer sectors is generating substantial opportunities for RF SAW filter manufacturers. Smart home devices, industrial sensors, wearable technology, and connected automotive systems all require reliable RF filtering solutions. The automotive sector alone is projected to account for over 25% of industrial IoT connections by 2025, with each connected vehicle containing multiple RF filtering components. This diversification of applications beyond traditional telecommunications is creating new revenue streams for market players.

Advancements in Material Science Enhancing Filter Performance

Recent breakthroughs in piezoelectric materials and lithography techniques have significantly improved the performance characteristics of SAW filters. The development of temperature-compensated SAW (TC-SAW) and ultra-wideband SAW filters has enabled their use in more demanding applications where stability and bandwidth are critical. These technological improvements are allowing SAW filters to compete effectively against bulk acoustic wave (BAW) filters in certain frequency ranges, particularly in cost-sensitive consumer electronics markets.

MARKET RESTRAINTS

Frequency Limitations Creating Technical Barriers for High-Band Applications

While SAW filters dominate the sub-1.5 GHz frequency range, they face significant technical challenges at higher frequencies required for advanced 5G applications. The physical principles governing surface acoustic wave propagation impose inherent limitations on maximum operating frequencies, making BAW filters more suitable for certain high-frequency applications. This technical constraint is forcing SAW filter manufacturers to invest heavily in new materials and designs to remain competitive across all frequency bands.

Complex Manufacturing Processes Leading to Yield Challenges

The precise lithography and thin-film deposition processes required for SAW filter production create manufacturing complexities that impact yield rates and production scalability. Even minor variations in substrate quality or patterning accuracy can significantly affect filter performance, leading to higher production costs compared to simpler discrete components. These manufacturing challenges become particularly acute as device sizes shrink to accommodate mobile device miniaturization trends.

MARKET CHALLENGES

Intense Competition from Alternative Filter Technologies

The RF SAW filter market faces mounting pressure from competing technologies like Bulk Acoustic Wave (BAW) filters and passive integrated devices. BAW filters offer superior performance at higher frequencies and have gained significant market share in premium smartphone segments. Additionally, the industry trend toward highly integrated RF front-end modules poses challenges for standalone SAW filter suppliers, as module manufacturers increasingly seek complete subsystem solutions.

Supply Chain Vulnerabilities Impacting Production Stability

The specialized materials and equipment required for SAW filter manufacturing create supply chain risks that have been exacerbated by recent global disruptions. The industry’s reliance on specific piezoelectric substrates and precision manufacturing tools from limited suppliers makes production vulnerable to geopolitical tensions and trade restrictions. These vulnerabilities are prompting manufacturers to diversify their supply networks and invest in alternative material sources.

MARKET OPPORTUNITIES

Emerging 6G Research Creating Future Growth Potential

While still in early development stages, 6G technology research is opening new frontiers for advanced RF filter technologies. SAW filter manufacturers are positioning themselves for future 6G applications by developing innovative designs capable of operating in terahertz frequency ranges. Strategic partnerships between filter suppliers and telecom equipment manufacturers are forming to co-develop next-generation solutions that will meet the extreme performance requirements of 6G networks.

Automotive Radar Applications Driving Demand for Specialized Filters

The rapid adoption of advanced driver assistance systems (ADAS) and autonomous vehicle technologies is creating strong demand for SAW filters optimized for automotive radar applications. These filters must meet stringent reliability standards while operating in harsh environmental conditions. The automotive radar market is projected to show particularly strong growth, with SAW filters playing a critical role in interference mitigation and signal conditioning for collision avoidance systems.

Medical IoT Applications Presenting Niche Growth Segments

The healthcare sector’s increasing adoption of connected medical devices and remote patient monitoring systems is generating specialized opportunities for RF SAW filters. Implantable devices, wearable health monitors, and hospital equipment all require robust RF filtering to ensure reliable operation in electromagnetically complex environments. This healthcare vertical represents a high-value niche market where performance and reliability take precedence over cost considerations.

RF SURFACE ACOUSTIC WAVE FILTERS MARKET TRENDS

5G Network Expansion Driving Demand for Advanced RF SAW Filters

The rapid global rollout of 5G networks has significantly increased demand for high-performance RF Surface Acoustic Wave (SAW) filters. With mobile operators investing heavily in next-generation infrastructure, component manufacturers are seeing unprecedented orders for filters capable of handling higher frequencies while maintaining signal integrity. The need for reduced signal attenuation in 5G applications has led to innovations in SAW filter design, including temperature-compensated variants that deliver superior performance in base stations and mobile devices. In 2024 alone, over 250 million 5G-capable smartphones shipped with advanced SAW filter configurations, representing a 35% increase from the previous year.

Other Trends

Miniaturization in Consumer Electronics

The continuing trend toward smaller, more powerful mobile devices is pushing SAW filter manufacturers to develop increasingly compact solutions without sacrificing performance. Modern smartphones now incorporate up to 60 RF filters per device, with leading manufacturers achieving component size reductions of 20-30% compared to 2020 designs. This miniaturization extends beyond smartphones, influencing product development in wearables, IoT devices, and automotive electronics where space constraints demand innovative filtering solutions.

Automotive Radar Applications Creating New Opportunities

Advanced driver assistance systems (ADAS) and autonomous vehicle technologies are creating substantial demand for SAW filters in the 24GHz and 77GHz frequency bands. The automotive sector now accounts for nearly 15% of the SAW filter market, with projections indicating this segment will grow at a CAGR of 8-10% through 2030. These applications require filters with exceptional temperature stability and vibration resistance – qualities that have driven manufacturers to develop specialized automotive-grade SAW components featuring enhanced durability and signal processing capabilities.

Material Science Breakthroughs Enhancing Filter Performance

Recent advancements in piezoelectric materials have unlocked new possibilities for SAW filter performance. Lithium niobate and lithium tantalate substrates now feature improved crystal structures that allow for better temperature stability and lower insertion loss. Manufacturers are experimenting with novel deposition techniques to create multilayer structures that can handle higher power levels while maintaining frequency selectivity. These material innovations are particularly valuable in defense and aerospace applications where components must perform reliably in extreme environmental conditions.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Intensify Innovation to Capture RF SAW Filter Market Share

The global RF Surface Acoustic Wave (SAW) Filters market exhibits a competitive yet fragmented structure, with established semiconductor giants competing alongside specialized component manufacturers. Murata Manufacturing currently leads the market with approximately 18% revenue share as of 2024, leveraging its vertically integrated production capabilities and extensive patent portfolio covering advanced filter designs.

Qualcomm and Skyworks Solutions have significantly expanded their RF front-end module businesses, incorporating SAW filters into integrated solutions for 5G smartphones. Their system-level expertise provides competitive differentiation, with Skyworks reporting a 12% year-over-year growth in RF filter sales in their latest earnings.

Japanese component specialists Taiyo Yuden and TDK maintain strong positions through precision manufacturing capabilities, particularly in high-frequency applications. Their recent investments in temperature-compensated (TC-SAW) and ultra-wideband filters demonstrate the industry’s shift toward more sophisticated solutions.

The competitive intensity is further amplified by strategic movements:

- Murata’s acquisition of Resonant Inc. (2023) enhanced its IP portfolio in elastic wave technology

- Qorvo’s $400 million investment in BAW filter capacity signals cross-technology competition

- Taiyo Yuden’s new Malaysian production facility (2024) addresses growing Southeast Asian demand

List of Key RF SAW Filter Manufacturers

- Qualcomm Technologies, Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Taiyo Yuden Co., Ltd. (Japan)

- Skyworks Solutions, Inc. (U.S.)

- TDK Corporation (Japan)

- Abracon LLC (U.S.)

- AVX Corporation (U.S.)

- Qorvo, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Akoustis Technologies (U.S.)

Segment Analysis:

By Type

Transversal Filters Dominate the Market Owing to High Adoption in 5G and Wireless Communication Applications

The RF Surface Acoustic Wave (SAW) Filters market is segmented based on type into:

- Transversal Filters

- Subtypes: Single-phase unidirectional transducer (SPUDT), multi-phase unidirectional transducer (MPUDT), and others

- Resonator Filters

By Application

Telecommunication Sector Remains Key Growth Driver Due to Expanding 5G Infrastructure Deployment

The market is segmented based on application into:

- Telecommunication

- Consumer Electronics

- Aerospace and Defense

- Automotive

- Healthcare

By End User

Original Equipment Manufacturers (OEMs) Lead Market Adoption for Device Integration

The market is segmented based on end user into:

- Original Equipment Manufacturers (OEMs)

- Aftermarket

- Research and Development Entities

Regional Analysis: RF Surface Acoustic Wave Filters Market

North America

The North American RF Surface Acoustic Wave (SAW) Filters market is driven by significant investments in 5G infrastructure and advanced telecommunications networks, particularly in the U.S. and Canada. With the U.S. estimated to account for $X million in SAW filter revenue in 2024, the region remains a critical hub for semiconductor innovation. High-performance SAW filters are in demand for 5G base stations, IoT devices, and defense applications, with key players like Qualcomm and Skyworks Solutions Inc leading production. Regulatory compliance with FCC standards and increasing adoption of RF components in automotive electronics further propel the market, though supply chain disruptions pose challenges.

Europe

Europe’s market thrives on strict quality standards and a strong push toward 5G deployment, particularly in Germany, France, and the U.K. The EU’s Horizon Europe program supports R&D in next-gen RF components, accelerating demand for SAW filters in automotive radar and smart city infrastructure. However, the region faces intense competition from Asia-Pacific manufacturers, leading to pricing pressures. While Taiyo Yuden and TDK hold significant market shares, European OEMs prioritize environmentally sustainable manufacturing processes. Aerospace and healthcare applications also contribute to steady demand, though economic volatility in Eastern Europe may slow growth.

Asia-Pacific

Asia-Pacific dominates global SAW filter consumption, driven by China’s telecom expansion and India’s growing electronics sector. China alone is projected to reach $X million in market value by 2032, fueled by domestic production from Murata Manufacturing and local players. The region benefits from cost-effective manufacturing and rapid adoption of consumer electronics, though IP theft concerns linger. Japan and South Korea emphasize miniaturized SAW filters for smartphones and wearables, while Southeast Asian markets show potential due to rising FDI in semiconductor fabrication. However, geopolitical tensions and raw material shortages present risks.

South America

Market growth in South America is gradual, centered on Brazil and Argentina, where expanding 4G/LTE networks drive demand. The automotive industry’s gradual shift toward connected vehicles offers opportunities, but currency fluctuations and limited local production hinder competitiveness. Most SAW filters are imported from Asia, though partnerships with Abracon LLC and AVX aim to strengthen regional supply chains. Investment in smart infrastructure could unlock future potential, but political instability and low R&D expenditure remain obstacles.

Middle East & Africa

This emerging market sees nascent demand for SAW filters, primarily for telecom base stations in the UAE, Saudi Arabia, and Turkey. Government-led digital transformation initiatives, such as Saudi Arabia’s Vision 2030, support RF component adoption, though dependency on imports persists. Africa’s growth is sporadic, with South Africa and Egypt leading in industrial and medical applications. High costs of deployment and scarce technical expertise limit expansion, but partnerships with Qorvo and Broadcom signal long-term opportunities as 5G penetration increases.

Report Scope

This market research report provides a comprehensive analysis of the global and regional RF Surface Acoustic Wave Filters market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global RF Surface Acoustic Wave Filters market was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 7.84 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Transversal Filters, Resonator Filters), application (Telecommunication, Consumer Electronics, Aerospace & Defense, Automotive, Environmental & Industrial, Healthcare), and end-user industry.

- Regional Outlook: Insights into market performance across North America (U.S. market size estimated at USD million in 2024), Europe, Asia-Pacific (China to reach USD million), Latin America, and Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants including Qualcomm, Taiyo Yuden, Skyworks Solutions, Murata Manufacturing, and TDK, covering their product portfolios, market share (top five players held % share in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging RF filter technologies, miniaturization trends, and integration with 5G/6G networks.

- Market Drivers & Restraints: Evaluation of 5G rollout, IoT expansion, and automotive electronics growth versus supply chain challenges and material constraints.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, component suppliers, OEMs, and investors in the RF components ecosystem.

Primary and secondary research methods are employed, including manufacturer surveys, expert interviews, and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Surface Acoustic Wave Filters Market?

-> RF Surface Acoustic Wave Filters Market was valued at US$ 3.47 billion in 2024 and is projected to reach US$ 7.84 billion by 2032, at a CAGR of 10.7% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Qualcomm, Taiyo Yuden, Skyworks Solutions, Murata Manufacturing, TDK, Qorvo, and Broadcom, among others.

What are the key growth drivers?

-> Growth is driven by 5G network expansion, increasing smartphone penetration, and rising demand for RF components in automotive electronics.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, while North America remains strong in R&D and advanced applications.

What are the emerging trends?

-> Emerging trends include higher frequency SAW filters for 5G, integration with IoT devices, and advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...