MARKET INSIGHTS

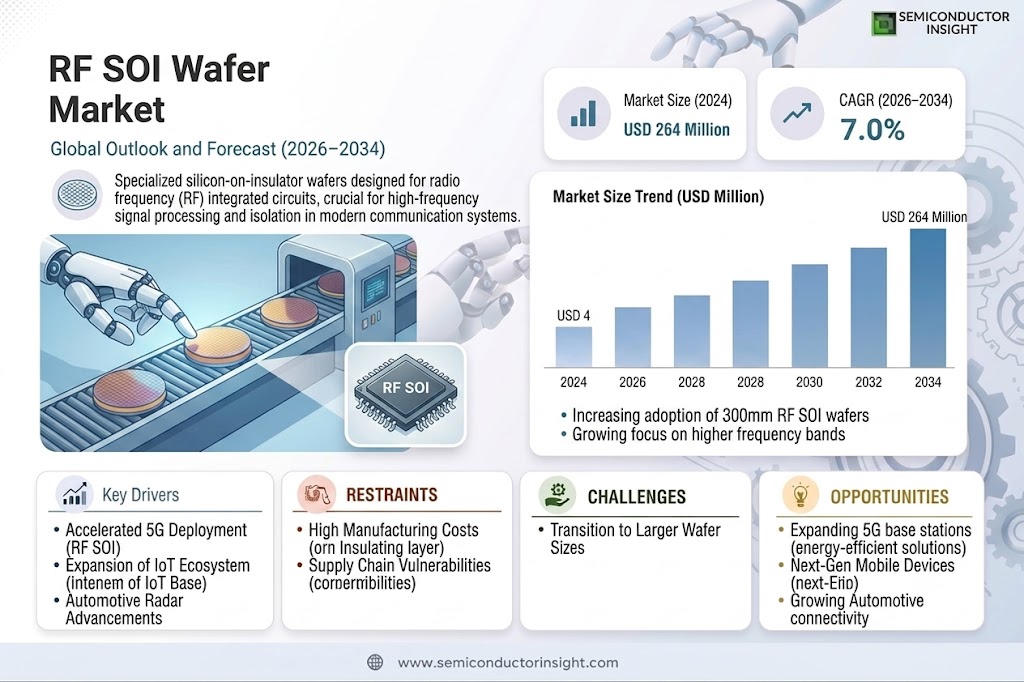

The global RF SOI Wafer Market was valued at 264 million in 2024 and is projected to reach US$ 422 million by 2032, at a CAGR of 7.0% during the forecast period.

RF SOI (Radio Frequency Silicon-on-Insulator) wafers are specialized semiconductor substrates engineered for high-frequency applications. These wafers feature a thin layer of silicon separated from the bulk silicon substrate by an insulating layer, which significantly enhances performance in RF applications by reducing signal loss and improving power efficiency. They are critical components in 5G infrastructure, smartphones, IoT devices, and automotive radar systems, where high-frequency signal processing is paramount.

The market growth is driven by rapid 5G network deployment globally, increasing smartphone adoption with advanced RF capabilities, and growing demand for energy-efficient semiconductor solutions. However, high production costs and complex manufacturing processes pose challenges. Leading manufacturers like Soitec and Shin-Etsu are investing in larger 300mm wafer production to meet rising demand, while Chinese players are expanding their 200mm wafer capacities to cater to mid-range applications.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated 5G Deployment Driving Demand for RF SOI Wafers

The global rollout of 5G networks is creating unprecedented demand for RF SOI wafers, as these specialized components are essential for high-frequency signal processing in smartphones and base stations. With over 100 million 5G subscriptions added globally in just the second quarter of 2024, mobile device manufacturers are under intense pressure to integrate more advanced RF components into their designs. RF SOI technology enables better power efficiency and signal isolation compared to traditional silicon substrates, making it ideal for 5G’s high-performance requirements. Major chipmakers are increasingly adopting 300mm RF SOI wafers to meet this surging demand while improving manufacturing efficiency.

Expansion of IoT Ecosystem Creating New Application Segments

The Internet of Things market continues to expand rapidly, with projections indicating over 30 billion connected devices by 2030, many requiring reliable RF components. RF SOI wafers are becoming the substrate of choice for IoT applications because they offer superior performance in power-sensitive devices while reducing signal interference. Smart home technologies, industrial sensors, and wearable devices increasingly incorporate RF SOI-based chips to achieve lower power consumption and better signal integrity. This broad market expansion is driving wafer manufacturers to increase production capacity, particularly for 200mm wafers which remain popular for many IoT applications.

Automotive Radar Advancements Fueling Market Growth

Advanced driver assistance systems (ADAS) and autonomous vehicle development are creating strong demand for RF SOI wafers in automotive radar applications. The average modern vehicle now incorporates multiple radar modules for collision avoidance and adaptive cruise control, each requiring high-performance RF components. RF SOI’s ability to maintain signal integrity while minimizing power consumption makes it particularly valuable as automakers push for greater electric vehicle range. With the automotive radar market projected to surpass 85 million units annually by 2030, this represents one of the fastest-growing segments for RF SOI technology.

➤ Leading automotive suppliers are now collaborating with wafer manufacturers to develop automotive-grade RF SOI solutions that meet stringent reliability requirements for vehicle applications.

MARKET RESTRAINTS

High Manufacturing Costs Limiting Market Penetration

The specialized fabrication processes required for RF SOI wafers result in significantly higher production costs compared to conventional silicon wafers. These elevated costs pose a substantial barrier for price-sensitive applications and emerging markets. The complex manufacturing flow, which includes advanced bonding and layer transfer techniques, requires specialized equipment and clean room facilities that represent substantial capital investments. While market leaders continue to optimize production processes, the cost premium remains a limiting factor for widespread adoption, particularly in consumer electronics where profit margins are increasingly constrained.

Supply Chain Vulnerabilities Creating Market Uncertainty

The RF SOI wafer market faces ongoing challenges from global semiconductor supply chain disruptions that have persisted since 2022. Critical raw materials, including high-purity silicon and specialized insulating layers, remain subject to price volatility and supply constraints. Geopolitical factors have further complicated the supply situation, with export controls affecting equipment availability in some regions. These supply chain issues create uncertainty for manufacturers planning capacity expansions, as lead times for key fabrication equipment have extended beyond 12 months in some cases.

MARKET CHALLENGES

Transition to Larger Wafer Sizes Creating Technical Hurdles

While the industry continues its migration toward 300mm wafer production, this transition presents significant technical challenges for RF SOI manufacturers. Maintaining uniform layer thickness and crystal quality across larger wafer diameters requires substantial process refinement. Many existing fabrication facilities need expensive upgrades to handle larger wafers, while new entrants face steep learning curves in achieving acceptable yields. These technical hurdles are particularly acute for RF applications where performance specifications are extremely demanding.

Additional Market Challenges

Intellectual Property Barriers

The RF SOI sector features complex patent landscapes with overlapping claims among major players, creating potential obstacles for new market entrants. Licensing requirements and potential litigation risks may slow innovation and adoption in some market segments.

Design Complexity

As RF systems continue to integrate more functionality, the design complexity of RF SOI-based circuits is increasing dramatically. This requires close collaboration between wafer manufacturers and chip designers, potentially slowing development cycles for new products.

MARKET OPPORTUNITIES

Emerging 6G Development Opening New Possibilities

Early research and development efforts for 6G communications networks are creating new opportunities for RF SOI technology. The extremely high frequencies anticipated for 6G (potentially reaching terahertz ranges) will require innovative semiconductor solutions where RF SOI substrates may provide critical performance advantages. While commercial 6G deployment remains years away, strategic investments in materials research and device architecture today could position RF SOI as a foundational technology for future networks.

Defense and Aerospace Applications Presenting Growth Potential

The defense and aerospace sectors represent promising growth areas for RF SOI wafers, particularly for radar, electronic warfare, and satellite communications applications. These markets value performance over cost considerations, making them ideal for premium RF SOI solutions. Increasing defense budgets in multiple regions and growing demand for more sophisticated electronic systems are driving investment in advanced RF technologies that can operate reliably in harsh environments.

Medical IoT Creating Niche Opportunities

The expanding market for medical IoT devices, including implantable and wearable health monitors, is creating specialized opportunities for RF SOI technology. These applications require ultra-low power consumption and reliable wireless connectivity in compact form factors – characteristics where RF SOI excels. As regulatory approvals for medical devices continue to increase, this represents a high-value niche market with strong growth potential through the decade.

RF SOI WAFER MARKET TRENDS

5G Expansion and Smart Device Proliferation Drive Strong Demand

The rapid global deployment of 5G networks continues to be the primary growth catalyst for RF SOI wafers, with their specialized ability to enhance signal isolation and power efficiency in high-frequency applications. The market saw approximately 310 million units of 5G-capable smartphones shipped in Q1 2024 alone, each requiring multiple RF SOI components for antenna switching and power amplification. This surge is further amplified by widening adoption in IoT ecosystems, where 35 billion connected devices are projected by 2030. Manufacturers are responding with wafer-level innovations that reduce insertion losses below 0.5dB while improving thermal stability in compact form factors.

Other Trends

Automotive Radar Advancements

Autonomous vehicle development has emerged as a high-growth segment, with RF SOI wafers becoming essential for next-generation 77GHz and 79GHz radar systems. These applications demand exceptional linearity and phase noise performance in harsh environments, pushing wafer suppliers to develop specialized buried oxide layers with defect densities below 1/cm². The automotive radar market is projected to consume 8 million 200mm equivalent wafers annually by 2026, with Tier 1 suppliers increasingly qualifying SOI solutions over traditional bulk silicon.

Foundry Technology Transitions Reshape Competitive Landscape

The ongoing migration from 150mm to 200mm and 300mm wafer platforms is creating significant market churn, with leading manufacturers investing over $2 billion collectively in capacity expansions through 2025. This transition enables 30% cost reductions per die while meeting the throughput requirements of high-volume RF front-end module production. While 200mm remains dominant at 58% market share currently, 300mm adoption in advanced smartphone PA modules is accelerating with foundry partners qualifying new SOI processes at 22nm nodes. Concurrently, heterogenous integration techniques using wafer-to-wafer bonding are enabling novel 3D RF architectures that combine SOI substrates with III-V materials.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Compete for Market Share in High-Growth RF SOI Segment

The global RF SOI wafer market features a diverse competitive landscape with established semiconductor manufacturers, specialized foundries, and emerging regional players. Leading companies are actively investing in research and development to enhance wafer quality, improve manufacturing processes, and expand production capacities to meet growing demand from 5G and IoT applications.

Soitec dominates the market with its advanced engineered substrate solutions, holding approximately 25% share of the 2024 market revenue. The company’s SmartCut™ technology enables superior RF performance, making it the preferred supplier for many leading fabless semiconductor companies and foundries. Its strong position is further reinforced by strategic partnerships with major smartphone chipset manufacturers.

Shin-Etsu and SUMCO follow closely, combining their extensive experience in silicon wafer production with specialized RF SOI capabilities. These Japanese manufacturers benefit from vertical integration and stable raw material supplies, allowing them to maintain competitive pricing while meeting stringent quality requirements for automotive and industrial applications.

Meanwhile, GlobalWafers and NSIG (Okmetic) are expanding their market presence through capacity expansions and technology acquisitions. GlobalWafers’ acquisition of Siltronic (pending regulatory approval) could significantly strengthen its position in the RF SOI segment, particularly in European and North American markets.

Chinese manufacturers like Shenyang Silicon Technology and Shanghai Advanced Silicon Technology are rapidly gaining traction, supported by government initiatives to develop domestic semiconductor supply chains. These companies are focusing on cost-effective solutions for mid-range RF applications while gradually moving up the value chain.

List of Key RF SOI Wafer Manufacturers Profiled

- Soitec (France)

- Shin-Etsu (Japan)

- SUMCO (Japan)

- GlobalWafers (Taiwan)

- NSIG (Okmetic) (Finland)

- IceMos Technology (UK)

- Wafer Works Corporation (Taiwan)

- Shenyang Silicon Technology (China)

- Zhonghuan Advanced (China)

- Shanghai Advanced Silicon Technology (China)

- WaferPro (U.S.)

- SEIREN KST (Japan)

- PlutoSemi (South Korea)

Segment Analysis:

By Type

150mm and Below Segment Leads Due to Cost-Effectiveness in Mass Production

The market is segmented based on type into:

- 150mm and Below

- 200 mm

- 300 mm

By Application

Mobile Communications Segment Dominates with Rising 5G Infrastructure Development

The market is segmented based on application into:

- Mobile Communications

- Vehicle Electronics

- Others

By Wafer Material

High-Resistivity Silicon Segment Preferred for Superior RF Performance

The market is segmented based on wafer material into:

- High-Resistivity Silicon

- Low-Resistivity Silicon

By Fabrication Technology

Smart Cut Technology Segment Gains Traction for High Quality Wafers

The market is segmented based on fabrication technology into:

- Smart Cut Technology

- Bonded SOI Technology

- SIMOX Technology

Regional Analysis: RF SOI Wafer Market

Asia-Pacific

The Asia-Pacific region dominates the RF SOI wafer market, with China, Japan, and South Korea leading production and consumption. This dominance stems from the concentration of semiconductor manufacturing giants and rapid 5G infrastructure deployment. China’s semiconductor self-sufficiency initiatives have particularly fueled demand, with domestic players like Shanghai Advanced Silicon Technology expanding capacities. The mobile communications sector accounts for over 60% of regional consumption, driven by smartphone OEMs requiring advanced RF components. While Japan maintains technological leadership in 200mm wafer production, China is rapidly catching up with significant investments in 300mm RF SOI capabilities to support next-generation wireless applications.

North America

North America’s RF SOI market thrives on innovation and defense applications, with the U.S. accounting for nearly 80% of regional demand. The presence of leading fabless semiconductor companies and robust R&D ecosystems has positioned 150mm and below wafers for IoT and 5G mmWave applications as high-growth segments. Automotive radar systems are emerging as a key driver, with major automakers incorporating RF SOI-based solutions for ADAS. Supply chain localization efforts and CHIPS Act funding are reshaping the competitive landscape, encouraging partnerships between domestic foundries and RF SOI suppliers to reduce dependence on Asian wafer sources.

Europe

Europe’s market is characterized by specialist applications in automotive and industrial IoT, with Germany and France representing over half of regional consumption. Stricter RF performance requirements for connected vehicles under EU regulations have accelerated adoption of high-quality 200mm RF SOI wafers. The region benefits from strong academic-industrial collaborations, particularly in developing RF SOI solutions for satellite communications and aerospace. However, limited domestic wafer production capacity creates dependence on imports, though initiatives like the European Chips Act aim to strengthen local semiconductor ecosystems including specialty wafer manufacturing.

Middle East & Africa

This emerging market shows potential through strategic technology transfer initiatives in countries like Israel and the UAE. While current demand remains limited primarily to telecom infrastructure projects, growing smart city deployments are creating niche opportunities for RF SOI wafers in base station applications. The lack of local manufacturing means nearly all supply is imported, but regional governments are beginning to prioritize semiconductor ecosystem development as part of broader technology diversification strategies, particularly in Gulf Cooperation Council countries.

South America

The region presents untapped potential with Brazil as the primary market, though adoption remains constrained by economic volatility and limited high-tech manufacturing. Most demand comes from telecom operators upgrading networks rather than local device manufacturers. While some progress is visible in establishing local semiconductor design capabilities, particularly for IoT applications, the absence of domestic wafer production and currency fluctuations continue to hinder market growth. Strategic partnerships with Asian suppliers offer the most viable path for regional market development in the medium term.

Report Scope

This market research report provides a comprehensive analysis of the global RF SOI Wafer market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global RF SOI Wafer market was valued at USD 264 million in 2024 and is projected to reach USD 422 million by 2032, growing at a CAGR of 7.0%.

- Segmentation Analysis: Detailed breakdown by product type (150mm and Below, 200mm, 300mm), application (Mobile Communications, Vehicle Electronics, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets, with Asia-Pacific leading in growth.

- Competitive Landscape: Profiles of leading market participants, including Soitec, Shin-Etsu, SUMCO, GlobalWafers, NSIG (Okmetic), IceMos Technology, Wafer Works Corporation, and others, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in RF SOI wafers, including advancements in 5G applications, IoT integration, and automotive radar systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as increasing demand for 5G technology and IoT devices, along with challenges like supply chain constraints and high fabrication costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF SOI Wafer Market?

-> RF SOI Wafer Market was valued at 264 million in 2024 and is projected to reach US$ 422 million by 2032, at a CAGR of 7.0% during the forecast period.

Which key companies operate in Global RF SOI Wafer Market?

-> Key players include Soitec, Shin-Etsu, SUMCO, GlobalWafers, NSIG (Okmetic), IceMos Technology, Wafer Works Corporation, Shenyang Silicon Technology, Zhonghuan Advanced, and Shanghai Advanced Silicon Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for 5G technology, expansion of IoT applications, and increasing adoption in automotive radar systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China, Japan, and South Korea, while North America remains a significant market due to advanced 5G infrastructure.

What are the emerging trends?

-> Emerging trends include adoption of 300mm wafers for higher efficiency, integration with AI-driven RF systems, and advancements in SOI fabrication techniques.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...