RF SoC with integrated DSP for phased array beamforming Market Insights

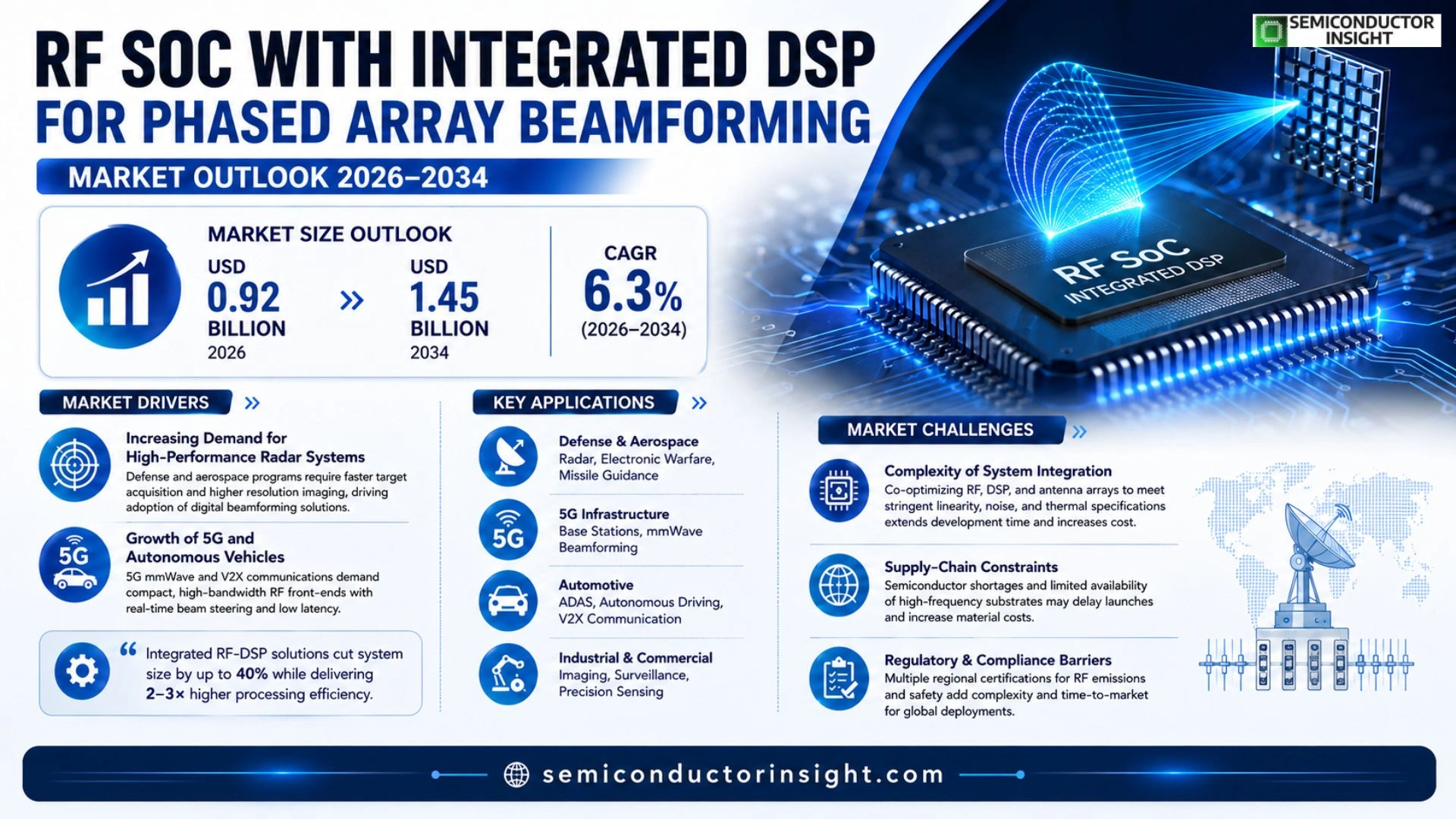

Global RF SoC with integrated DSP for phased array beamforming market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

RF System‑on‑Chip (SoC) devices combine radio‑frequency front‑end components, high‑speed analog blocks, and a dedicated digital signal processor (DSP) on a single silicon substrate. This integration enables real‑time phased‑array beamforming, allowing antenna arrays to steer beams electronically without mechanical movement,crucial for radar, satellite communications, and emerging 5G/6G applications.

The market is accelerating because defense budgets are increasing for advanced radar systems, while commercial sectors demand compact, power‑efficient solutions for autonomous vehicles and high‑frequency wireless links. Furthermore, the rollout of mmWave spectrum in next‑generation networks drives adoption of highly integrated RF SoCs. Key players such as AMD/Xilinx, Intel (Altera), NXP Semiconductors, Texas Instruments, and Analog Devices are expanding their portfolios through aggressive R&D and strategic partnerships to meet the growing performance requirements.

MARKET DRIVERS

Increasing Demand for High‑Performance Radar Systems

RF SoC with integrated DSP for phased array beamforming Market is being propelled by defense and aerospace programs that require faster target acquisition and higher resolution imaging. Modern radar platforms are shifting from legacy analog solutions to digital beamforming, which offers greater agility and lower power consumption.

Growth of 5G and Autonomous Vehicles

Commercial deployments of 5G mmWave and vehicle‑to‑infrastructure communication are expanding the need for compact, high‑bandwidth RF front‑ends. Integrated DSP blocks enable real‑time beam steering, reducing latency for critical applications such as autonomous navigation.

➤ “Integrated RF‑DSP solutions cut system size by up to 40 % while delivering 2‑3 × higher processing efficiency.”

Manufacturers are also benefitting from economies of scale as semiconductor fabs adopt advanced CMOS processes, resulting in lower unit costs and faster time‑to‑market for new phased‑array products.

MARKET CHALLENGES

Complexity of System Integration

Designing a unified RF‑SoC that meets stringent linearity, noise, and thermal specifications is technically demanding. Engineers must co‑optimize antenna arrays, power amplifiers, and DSP algorithms, which can extend development cycles.

Other Challenges

Supply‑Chain Constraints

Semiconductor shortages and limited availability of high‑frequency substrates pose sourcing risks, potentially delaying product launches and inflating costs.

Regulatory compliance across multiple regions adds further complexity, as each market may require distinct certification processes for RF emissions and safety.

MARKET RESTRAINTS

High Initial Capital Expenditure

Investing in advanced fabrication lines and design tools for RF SoC development involves substantial upfront spending. Small and medium‑sized enterprises often lack the financial resources to compete with larger incumbents.

Additionally, the learning curve associated with mixed‑signal verification and verification of beamforming algorithms can deter entry, limiting the pool of qualified vendors.

MARKET OPPORTUNITIES

Emerging Satellite Constellations

Rapidly deployable low‑Earth‑orbit (LEO) constellations require compact phased‑array antennas for on‑board communication and earth‑observation. Integrated RF‑DSP chips provide the necessary beam agility while meeting strict mass and power budgets.

Furthermore, the rise of AI‑driven signal processing opens avenues for smarter, adaptive beamforming solutions that can be embedded directly within the SoC, creating new revenue streams for vendors.

RF SoC with integrated DSP for phased array beamforming Market Trends

Growing Defense Investment in Advanced Radar Systems

The defense sector continues to allocate larger budgets toward next‑generation radar platforms that require rapid electronic beam steering. Integrated RF SoC devices with on‑chip DSP enable high‑resolution phased‑array beamforming while reducing footprint, weight, and power consumption. This capability aligns with the operational demands of modern air‑defense and missile‑tracking radars, where faster target acquisition and lower latency are critical. As a result, procurement programs are increasingly specifying RF SoC with integrated DSP for phased array beamforming Market solutions that can meet ruggedness standards and support a wide frequency range.

Other Trends

Commercial Adoption in Autonomous Vehicles

Automakers are integrating high‑frequency radar modules to enable short‑range sensing for collision avoidance and adaptive cruise control. The shift from discrete component architectures to a single‑chip RF SoC reduces board complexity and improves signal‑to‑noise performance, a decisive factor for safety‑critical applications. Recent vehicle platforms have demonstrated reliable operation of beam‑steered radars at 77 GHz, showcasing the commercial viability of the technology in mass‑produced models.

mmWave 5G/6G Rollout Accelerates Integration

Telecommunications operators are deploying extensive millimeter‑wave (mmWave) networks to meet the bandwidth demands of 5G and emerging 6G services. RF SoC with integrated DSP for phased array beamforming Market is responding to this demand by delivering compact, power‑efficient solutions that support dynamic beam management across multiple carriers. Network equipment manufacturers benefit from the ability to perform real‑time beamforming on a single silicon die, which shortens time‑to‑market for advanced antenna arrays in dense urban deployments.

Key semiconductor vendors,including AMD/Xilinx, Intel (Altera), NXP Semiconductors, Texas Instruments, and Analog Devices,are expanding their portfolios through aggressive research and strategic collaborations. Their roadmaps emphasize higher integration density, broader frequency coverage, and enhanced thermal management, all of which are essential to sustain the momentum in defense, automotive, and telecom segments. Collectively, these developments illustrate a clear trajectory toward greater system‑level integration, positioning RF SoC with integrated DSP for phased array beamforming Market as a cornerstone technology for next‑generation high‑performance wireless solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

RF SoC with Integrated DSP for Phased‑Array Beamforming – Competitive Overview

RF SoC market for phased‑array beamforming is currently led by a handful of large semiconductor families that combine high‑performance RF front‑ends with dedicated DSP blocks on a single die. AMD/Xilinx’s Versal ACAP platform, Intel’s Agilex series (formerly Altera), NXP’s RFSoC portfolio, Texas Instruments’ mmWave SoCs, and Analog Devices’ ADRES series dominate the revenue pool, each leveraging extensive design‑win ecosystems and deep connections with defense prime contractors. Their scale enables aggressive price‑performance improvements that support the rapid growth projected to $1.45 billion by 2034. These incumbents shape market structure through tiered product families, ranging from entry‑level 28 GHz components to 120 GHz high‑gain solutions for next‑generation radar and satellite communications.

Beyond the Tier‑1 leaders, a diverse set of niche innovators adds depth to the competitive landscape. Qorvo and Skyworks focus on high‑power PA integration for automotive radar, while Infineon and STMicroelectronics provide silicon‑based beamforming ASICs for industrial IoT. Broadcom and MediaTek leverage their telecom heritage to embed RF SoC blocks into 5G/6G base‑station modules. Qualcomm’s Snapdragon X series begins to explore mmWave on‑chip DSP, and Murata, Nexperia, and Renesas contribute specialized RF front‑ends and mixed‑signal IP that complement the larger platforms. Together, these players foster a vibrant ecosystem that accelerates technology adoption across defense, aerospace, and commercial sectors.

List of Key RF SoC with Integrated DSP Companies Profiled

- AMD/Xilinx

- AMD

- Intel (Altera)

- Intel

- NXP Semiconductors

- Texas Instruments

- Texas Instruments

- Analog Devices

- Analog Devices

- Qorvo

- Skyworks Solutions

- Infineon Technologies

- STMicroelectronics

- Broadcom Inc.

- MediaTek Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Monolithic RF SoC drives the market because it delivers the highest integration density and lowest latency for beamforming algorithms.

|

| By Application |

|

Advanced Radar Systems remain the primary catalyst, as phased‑array beamforming is essential for high‑resolution target detection and tracking.

|

| By End User |

|

Defense & Aerospace dominate usage due to stringent performance and reliability requirements.

|

| By Integration Architecture |

|

Single‑Chip Integration is favored for its compact footprint and superior signal coherence.

|

| By Functional Focus |

|

Adaptive Interference Mitigation emerges as a critical capability for congested spectrum environments.

|

Regional Analysis: North America

North America

The adoption of RF SoCs with integrated DSP is accelerating as these chips offer enhanced performance, reduced size, and lower power consumption compared to discrete components. This trend is particularly advantageous for applications requiring compact and energy-efficient solutions, such as portable radar devices and advanced communication systems. The competitive landscape is characterized by established semiconductor companies and specialized RF chip manufacturers, all vying for market share. Future growth will be shaped by advancements in beamforming algorithms and the integration of AI/ML capabilities within RF SoCs.

The defense sector is a major driver for RF SoC adoption, particularly in radar systems for aircraft, naval platforms, and ground-based surveillance. The need for advanced electronic warfare and threat detection capabilities fuels the demand for high-performance beamforming solutions.

The integration of RF SoCs allows for smaller, lighter, and more power-efficient radar modules, enhancing the performance and operational capabilities of military equipment.

The automotive industry is witnessing a surge in the adoption of radar systems for advanced driver-assistance systems (ADAS) and autonomous driving. RF SoCs with integrated DSP are crucial for enabling high-resolution radar with extended range and improved accuracy.

The demand for these chips is driven by the increasing complexity of ADAS features, such as adaptive cruise control, blind-spot monitoring, and collision avoidance.

The rollout of 5G networks is generating significant demand for RF SoCs with integrated DSP for beamforming in base stations. These chips are essential for enabling high data rates, increased network capacity, and improved coverage.

The ability to dynamically steer and shape radio beams is crucial for optimizing network performance and mitigating interference in dense urban environments.

Applications in industrial automation, weather forecasting, and security systems are also contributing to the growth of RF SoC market. These applications benefit from the compact size, low power consumption, and cost-effectiveness of integrated solutions.

Radar systems are used for object detection, ranging, and velocity measurement in various industrial processes and commercial applications.

North America

The North American market is characterized by a strong emphasis on technological innovation and high-end applications. The region’s robust R&D infrastructure and a skilled workforce contribute to the development of advanced RF SoC solutions for phased array beamforming. Government funding and private investments are fostering breakthroughs in areas such as artificial intelligence and machine learning, which are being integrated into RF SoC designs to enhance beamforming performance and system intelligence. The competitive landscape features a mix of established semiconductor giants and nimble startups focused on specific application segments. The overall outlook for the North American RF SoC market remains positive, with continued growth expected in the coming years.

Europe

Europe presents a substantial market for RF SoC with integrated DSP for phased array beamforming, driven by strong demand from the defense, automotive, and telecommunications sectors. The region’s focus on sustainability and energy efficiency is influencing the development of low-power RF SoCs. Key players in Europe are actively investing in R&D to develop advanced beamforming algorithms and integrate AI capabilities. The automotive industry in Europe is particularly focused on developing advanced driver-assistance systems (ADAS) and autonomous driving technologies, creating a significant demand for high-performance radar systems.

The European market is also benefiting from government initiatives promoting technological innovation and industrial competitiveness.

Asia-Pacific

The Asia-Pacific region is anticipated to be the fastest-growing market for RF SoC with integrated DSP for phased array beamforming, propelled by rapid industrialization, increasing investments in 5G infrastructure, and growing automotive production. China, in particular, represents a significant opportunity, with large-scale deployments of 5G networks and a burgeoning domestic automotive industry. The region is witnessing a surge in demand for radar systems for autonomous vehicles and advanced driver-assistance systems (ADAS).

The increasing adoption of IoT devices and the expansion of industrial automation are also contributing to the growth of RF SoC market in Asia-Pacific.

South America

South America’s RF SoC market is in an early stage of development, with growth driven by increasing investments in telecommunications infrastructure and the gradual adoption of automotive technologies. The telecommunications sector is undergoing significant expansion, particularly in areas with limited existing network coverage. The region’s growing automotive industry is creating demand for advanced driver-assistance systems (ADAS) and radar systems.

Government initiatives aimed at promoting technological development and infrastructure investments are expected to stimulate market growth.

Middle East & Africa

The Middle East and Africa represent a relatively small but growing market for RF SoC with integrated DSP for phased array beamforming. The region’s increasing investments in defense and security, coupled with the expansion of telecommunications networks, are driving demand for advanced radar systems and communication infrastructure. The automotive sector is also experiencing growth, particularly in countries with expanding urban areas.

Government initiatives promoting technological development and economic diversification are expected to contribute to the market’s growth trajectory.

Report Scope

This market research report provides a comprehensive analysis of the RF SoC with integrated DSP for phased array beamforming Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF SoC with integrated DSP for phased array beamforming Market?

-> RF SoC with integrated DSP for phased array beamforming Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034, representing a CAGR of 6.3% over the forecast period.

Which key companies operate in RF SoC with integrated DSP for phased array beamforming Market?

-> Key players include AMD/Xilinx, Intel (Altera), NXP Semiconductors, Texas Instruments, and Analog Devices, among others.

What are the key growth drivers?

-> Key growth drivers include increasing defense budgets for advanced radar systems, rising demand for compact and power‑efficient solutions in autonomous vehicles, and the rollout of mmWave spectrum for next‑generation 5G/6G networks.

Which region dominates the market?

-> The reference material does not specify a single dominant region; the market is described in global terms.

What are the emerging trends?

-> Emerging trends include greater adoption of mmWave technologies in 5G/6G deployments and increasing integration of high‑performance DSP cores within RF SoCs to enable real‑time phased‑array beamforming.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...