MARKET INSIGHTS

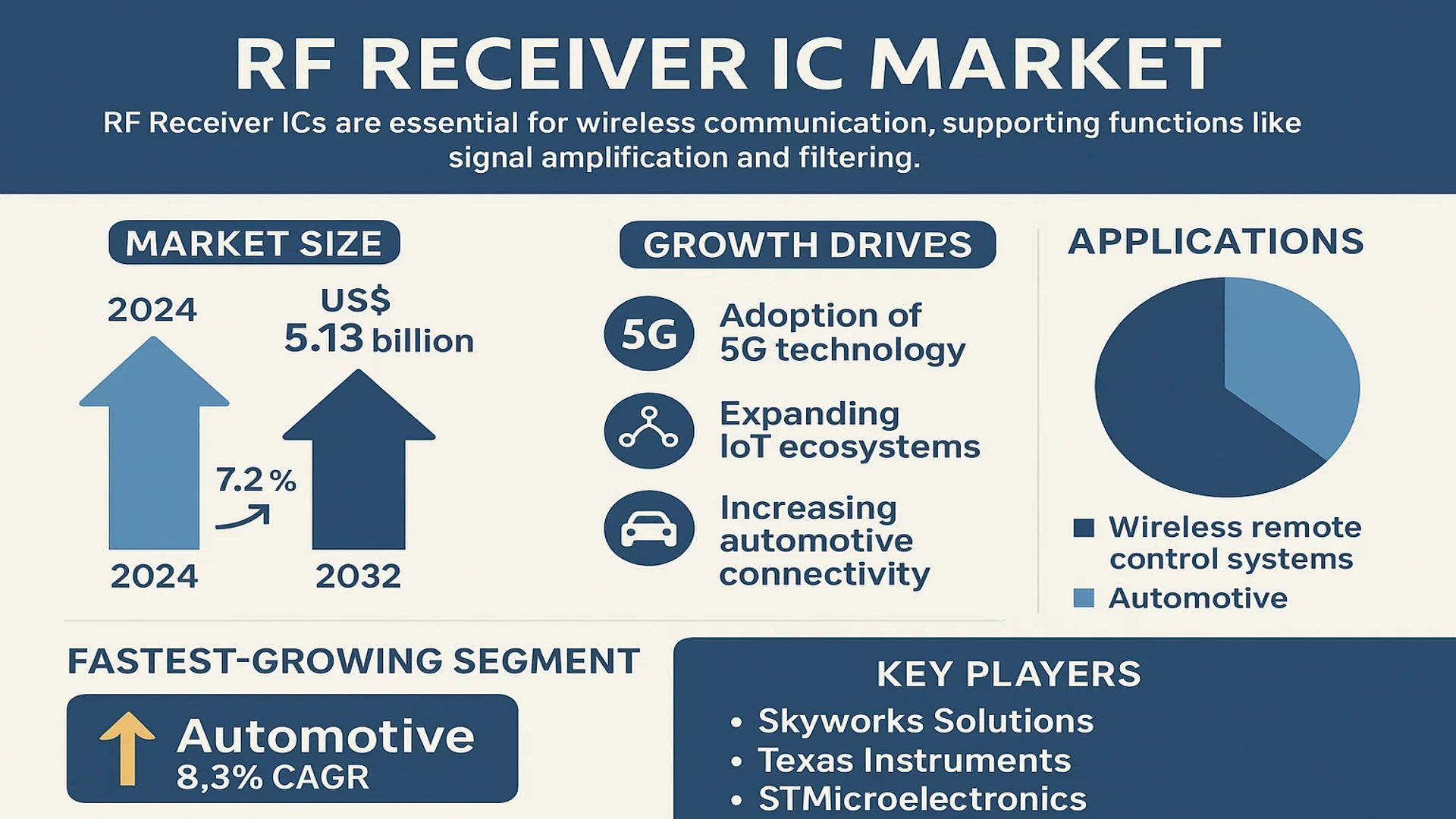

The global RF Receiver IC Market size was valued at US$ 2.94 billion in 2024 and is projected to reach US$ 5.13 billion by 2032, at a CAGR of 7.2% during the forecast period 2025-2032. While growth expectations are moderate compared to other semiconductor segments, the market remains resilient due to increasing demand for wireless communication across industries.

RF Receiver ICs (Radio Frequency Integrated Circuits) are specialized semiconductor components designed to receive and process radio frequency signals in wireless communication systems. These chips form a critical part of modern connectivity solutions, enabling functions such as signal amplification, filtering, and frequency conversion across applications including 5G networks, IoT devices, and automotive communication systems.

The market growth is being driven by several key factors: accelerated adoption of 5G technology, expanding IoT ecosystems, and increasing automotive connectivity requirements. However, supply chain challenges in the semiconductor industry and inflationary pressures present headwinds. The wireless remote control system segment currently dominates applications, while automotive adoption is growing fastest with a projected 8.3% CAGR through 2032. Leading players like Skyworks Solutions, Texas Instruments, and STMicroelectronics are investing heavily in advanced RF solutions to capitalize on these emerging opportunities.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and Connected Devices to Accelerate Market Growth

The global RF Receiver IC market is experiencing substantial growth due to the rapid expansion of Internet of Things (IoT) applications across industries. With over 15 billion active IoT devices worldwide currently, the demand for reliable wireless communication components has surged exponentially. RF receiver ICs serve as critical components in these connected devices, enabling seamless data transmission across various protocols including Wi-Fi, Bluetooth, and Zigbee. The automotive sector alone is projected to account for over 30% of this demand as vehicles incorporate more advanced infotainment and telematics systems.

Advancements in 5G Infrastructure to Drive Demand for High-Performance ICs

The ongoing global rollout of 5G networks is creating significant opportunities for RF receiver IC manufacturers. These next-generation networks require ICs with superior sensitivity and noise performance to handle higher frequency bands up to mmWave spectrum. The telecommunications industry’s investment in 5G infrastructure, valued at over $200 billion annually, directly benefits the RF component market. Furthermore, the increasing adoption of Massive MIMO technology in base stations necessitates more sophisticated receiver solutions, further propelling market growth.

Rising Demand for Smart Consumer Electronics to Fuel Market Expansion

Consumer electronics represent one of the largest application segments for RF receiver ICs. The growing popularity of smart home devices, wearables, and wireless audio solutions continues to drive innovation in receiver IC design. In particular, the wireless earbuds market alone is expected to surpass 500 million units annually by 2025, each containing multiple RF receivers. Additionally, the integration of AI-powered voice assistants in home automation systems creates further demand for advanced receiver ICs capable of handling multiple wireless protocols simultaneously.

MARKET RESTRAINTS

Complex Design Challenges at Higher Frequencies to Limit Market Growth

As wireless systems transition to higher frequencies such as mmWave bands, RF receiver IC manufacturers face significant technical hurdles. Signal integrity becomes increasingly difficult to maintain due to higher path loss and atmospheric absorption. Additionally, designing low-noise amplifiers (LNAs) and mixers that can operate effectively at these frequencies requires advanced semiconductor processes and packaging techniques. These technical challenges often lead to longer development cycles and higher failure rates during prototyping, potentially delaying time-to-market for new products.

Global Semiconductor Shortage to Impact Production Capacity

The ongoing semiconductor supply chain disruptions continue to affect the RF receiver IC market. The industry-wide chip shortage has led to extended lead times and allocation constraints for many key materials, including silicon wafers and specialty substrates. This situation is particularly challenging for RF components which often require specialized fabrication processes not easily transferred between foundries. Manufacturers are facing intense pressure to secure adequate production capacity while maintaining quality standards, potentially slowing overall market expansion.

Increasing Design Complexity to Raise Development Costs

Modern RF receiver IC designs must accommodate a growing number of communication standards while maintaining high performance metrics. This convergence requires increasingly complex system-on-chip (SoC) architectures that integrate multiple receiver chains. The R&D expenditure for such advanced designs can exceed $50 million per project, creating significant barriers to entry for smaller players. Additionally, the need for extensive regulatory certifications in different geographical markets further increases time and cost investments, potentially restraining market growth.

MARKET OPPORTUNITIES

Emerging Automotive Connectivity Solutions to Create New Growth Avenues

The automotive industry’s rapid adoption of vehicle-to-everything (V2X) communication presents significant opportunities. RF receiver ICs form the backbone of these next-generation safety and navigation systems, with the market expected to grow at over 25% CAGR in the coming years. As governments worldwide mandate advanced driver assistance systems (ADAS), automakers are integrating multiple RF receivers to support dedicated short-range communications (DSRC) and cellular-V2X technologies. This trend is creating demand for highly reliable receiver ICs capable of operating in harsh automotive environments.

Development of Ultra-Low-Power Receiver ICs for IoT applications

The proliferation of battery-operated IoT devices is driving innovation in ultra-low-power RF receiver design. Emerging receiver architectures using techniques like wake-up radios and adaptive duty cycling can reduce power consumption by over 80% compared to conventional designs. This breakthrough enables years of operation from small coin-cell batteries, opening new markets in industrial sensors, asset tracking, and remote monitoring applications. Companies developing these energy-efficient solutions are well-positioned to capitalize on the growing demand from IoT device manufacturers.

Expansion of Satellite Communication Networks to Drive Specialized IC Demand

The growing global deployment of low-earth orbit (LEO) satellite constellations is creating opportunities for specialized RF receiver ICs. These next-generation satellite networks require receivers with exceptional phase noise performance and frequency agility to maintain reliable links in dynamic environments. The satellite communication equipment market is projected to exceed $30 billion annually within five years, with ground terminal receivers representing a significant portion of this value. IC manufacturers developing radiation-hardened and software-defined receiver solutions stand to benefit substantially from this emerging opportunity.

MARKET CHALLENGES

Stringent Spectrum Regulations to Impact Product Development Cycles

The RF receiver IC market faces significant challenges from evolving spectrum allocation policies worldwide. Regulatory bodies frequently update requirements for out-of-band emissions and receiver selectivity, often requiring expensive design modifications. In some regions, new regulations mandate spectrum sharing capabilities that complicate receiver architectures. These changing requirements can significantly extend product development timelines and increase costs, particularly for global product offerings that must comply with multiple regulatory regimes.

Other Challenges

Increasing Competition from Integrated Solutions

The trend toward highly integrated RF front-end modules poses a challenge for discrete RF receiver IC suppliers. Many system manufacturers now prefer complete RF sub-systems that combine receivers with transmitters and antenna interfaces, making discrete solutions less attractive. This integration trend requires receiver IC vendors to either develop more comprehensive solutions or form strategic partnerships to maintain market relevance.

Cybersecurity Concerns in Wireless Systems

Growing awareness of RF vulnerability in wireless systems is prompting more rigorous security requirements for receiver ICs. Manufacturers now need to implement features like signal authentication and interference detection to protect against spoofing and jamming attacks. These additional security measures increase design complexity and may impact key performance metrics such as power consumption and latency.

RF RECEIVER IC MARKET TRENDS

5G Network Expansion Accelerates Demand for High-Performance RF Receiver ICs

The global rollout of 5G technology is driving substantial growth in the RF Receiver IC market, with the component segment projected to account for over 30% of total 5G infrastructure costs. Advanced RF solutions capable of handling mmWave frequencies (24-100GHz) and sub-6GHz bands are seeing particularly strong adoption. Recent technological advancements have enabled RF ICs to achieve 40% better power efficiency compared to previous generations, while supporting ultra-low latency communication critical for autonomous vehicles and industrial IoT applications. The increasing complexity of 5G standards is also pushing manufacturers to develop highly integrated System-on-Chip (SoC) solutions that combine multiple radio functions in compact form factors.

Other Trends

Automotive Sector Integration

The automotive industry’s rapid shift toward connected vehicle technologies is creating significant opportunities for RF Receiver IC manufacturers. Modern vehicles now incorporate an average of 15-20 RF modules for applications ranging from tire pressure monitoring to V2X (vehicle-to-everything) communication. The growth of autonomous driving systems, expected to reach 30% market penetration by 2030, particularly demands high-sensitivity receivers capable of operating in challenging electromagnetic environments. This trend is further amplified by regulatory mandates for advanced driver-assistance systems (ADAS) and the proliferation of in-vehicle infotainment systems with satellite radio capabilities.

Advancements in Low-Power Design and Miniaturization

Power efficiency has become a critical differentiator in the RF Receiver IC market, especially for battery-dependent IoT devices. Leading manufacturers have achieved 50% reductions in standby power consumption through innovative circuit designs and advanced semiconductor materials. The miniaturization trend has also accelerated, with surface-mount package sizes shrinking below 2mm² while maintaining full functionality. This evolution supports the development of wearable medical devices and smart home sensors that require years of operation on single batteries. Emerging energy harvesting technologies are being integrated with RF receivers to create completely battery-free solutions for industrial monitoring applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Compete Through RF Innovation Amidst Shifting Market Conditions

The global RF Receiver IC market demonstrates a semi-consolidated structure, dominated by established semiconductor players while accommodating specialized mid-size innovators. Texas Instruments leads the segment with its comprehensive RF portfolio, capturing significant market share through its widespread adoption in automotive and industrial applications. The company’s 2022 revenue of $20.03 billion reflects its robust position in analog semiconductors, where RF solutions contribute substantially.

Analog Devices and NXP Semiconductors emerge as close competitors, collectively holding about 28% of the market share. These companies benefit from strong design capabilities in high-performance RF ICs, particularly for 5G infrastructure and IoT devices. The recent acquisition of Maxim Integrated by Analog Devices (completed July 2021) notably strengthened its RF product lineup, enhancing its competitive positioning.

Meanwhile, Skyworks Solutions maintains leadership in smartphone RF front-end modules, with its FY2022 revenue reaching $5.46 billion. The company continues to invest in filter technologies for spectrum-congested 5G bands, addressing the growing demand for high-selectivity receiver ICs. Their specialized focus gives them an edge in mobile applications despite broader market consolidation.

Emerging competition comes from Asian manufacturers like Hoperf and AKM Semiconductor, who compete through aggressive pricing strategies and localized support networks. These players are gaining traction in cost-sensitive markets, particularly for consumer electronics and industrial remote control systems.

List of Key RF Receiver IC Companies Profiled

- Texas Instruments (U.S.)

- Analog Devices (U.S.)

- NXP Semiconductors (Netherlands)

- Skyworks Solutions (U.S.)

- Infineon Technologies (Germany)

- STMicroelectronics (Switzerland)

- Broadcom Inc. (U.S.)

- ON Semiconductor (U.S.)

- Renesas Electronics (Japan)

- Microchip Technology (U.S.)

- AKM Semiconductor (Japan)

- Hoperf Electronic (China)

Segment Analysis:

By Type

Digital Output Segment Leads Due to Expanding Wireless and IoT Applications

The market is segmented based on type into:

- Digital Output

- Subtypes: Low-frequency, High-frequency, Ultra-wideband (UWB)

- Analog Output

- Others

By Application

Automotive Segment Shows Strong Growth Driven by Connectivity Trends

The market is segmented based on application into:

- Automotive

- Wireless Remote Control Systems

- Data Communication

- Consumer Electronics

- Industrial Automation

By Frequency Range

Sub-1 GHz Remains Dominant Due to Long-Range Capabilities

The market is segmented based on frequency range into:

- Sub-1 GHz

- 1-6 GHz

- Above 6 GHz

By End User

Telecommunications Sector Shows Rapid Adoption for 5G Infrastructure

The market is segmented based on end user into:

- Telecommunications

- Automotive OEMs

- Consumer Electronics Manufacturers

- Industrial Equipment Producers

Regional Analysis: RF Receiver IC Market

Asia-Pacific

The Asia-Pacific region dominates the global RF Receiver IC market due to rapid technological adoption and robust electronics manufacturing capabilities. Countries like China, Japan, and South Korea account for over 42% of the worldwide semiconductor market demand, driven by their strong consumer electronics and automotive industries. China’s push towards 5G infrastructure and IoT applications has significantly increased RF IC consumption, with local players like Hoperf expanding production capacities. Meanwhile, Japan maintains leadership in high-precision RF components for automotive and industrial applications. However, recent supply chain disruptions and export restrictions have caused short-term volatility in the region’s semiconductor trade flows.

North America

North America remains a key innovation hub for RF Receiver ICs, with the U.S. accounting for 28% of global RF semiconductor revenues. The region benefits from concentrated R&D investments by companies like Skyworks Solutions and Texas Instruments, particularly in mmWave and ultra-wideband technologies for defense and aerospace applications. The CHIPS Act’s $52 billion funding allocation is accelerating domestic semiconductor production, including RF components. Automotive applications are growing at 14% CAGR owing to increasing ADAS adoption, though market maturity in consumer electronics has led to slower growth in traditional RF segments.

Europe

European demand for RF Receiver ICs is primarily driven by industrial automation and automotive applications, with Germany and France leading adoption. Strict EMC regulations and emphasis on energy-efficient designs have pushed companies like Infineon and STMicroelectronics to develop low-power RF solutions. The region shows particular strength in sub-GHz RF ICs for smart metering and industrial IoT, though market growth is constrained by the slower rollout of 5G infrastructure compared to Asia and North America. Recent EU semiconductor legislation aims to double Europe’s global market share to 20% by 2030 through strategic investments.

South America

South America’s RF IC market is emerging, with Brazil representing over 60% of regional demand for consumer electronics and basic wireless infrastructure applications. Price sensitivity drives preference for mid-range RF solutions, though increasing smart city projects in Chile and Colombia are creating opportunities for advanced RF receivers. The lack of local semiconductor fabrication limits value addition, with most components being imported from Asia. Economic instability and import dependencies continue to hinder market expansion despite growing wireless communication needs.

Middle East & Africa

This region shows nascent but promising growth in RF Receiver IC adoption, primarily fueled by telecommunications infrastructure development in GCC countries. The UAE and Saudi Arabia are investing heavily in 5G networks and smart city projects, creating demand for high-frequency RF components. However, the market remains constrained by limited local technical expertise and reliance on foreign suppliers. South Africa serves as the manufacturing and distribution hub for RF ICs in Sub-Saharan Africa, though political and economic challenges slow broader market penetration across the continent.

Report Scope

This market research report provides a comprehensive analysis of the global and regional RF Receiver IC markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global RF Receiver IC market was valued at US$ 2.94 billion in 2024 and is projected to reach US$ 5.13 billion by 2032, growing at a CAGR of 7.2%.

- Segmentation Analysis: Detailed breakdown by product type (Digital Output, Analog Output), application (Automotive, Wireless Remote Control Systems, Data Communication, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific accounted for 42% of the global market share in 2024.

- Competitive Landscape: Profiles of 14 leading market participants including Skyworks Solutions, Texas Instruments, NXP, and STMicroelectronics, covering their market share (top 5 companies held 48% share in 2024), product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including 5G integration, IoT connectivity solutions, and advanced semiconductor fabrication techniques (7nm and below nodes).

- Market Drivers & Restraints: Evaluation of growth drivers (5G deployment, automotive electronics demand) and challenges (supply chain constraints, geopolitical factors affecting semiconductor trade).

- Stakeholder Analysis: Strategic insights for IC designers, fabless semiconductor companies, OEMs, and investors regarding emerging opportunities in wireless communication markets.

The research methodology combines primary interviews with industry experts and analysis of verified market data from semiconductor industry reports, company financial disclosures, and trade association statistics.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Receiver IC Market?

-> RF Receiver IC Market size was valued at US$ 2.94 billion in 2024 and is projected to reach US$ 5.13 billion by 2032, at a CAGR of 7.2% during the forecast period 2025-2032.

Which key companies operate in Global RF Receiver IC Market?

-> Key players include Skyworks Solutions, Texas Instruments, NXP, STMicroelectronics, Analog Devices, Infineon, and Renesas Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing automotive electronics adoption, and growth in IoT-connected devices.

Which region dominates the market?

-> Asia-Pacific dominates with 42% market share, driven by semiconductor manufacturing in China, South Korea, and Taiwan.

What are the emerging trends?

-> Emerging trends include integration of AI in RF signal processing, development of ultra-low-power receivers for IoT, and advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...