MARKET INSIGHTS

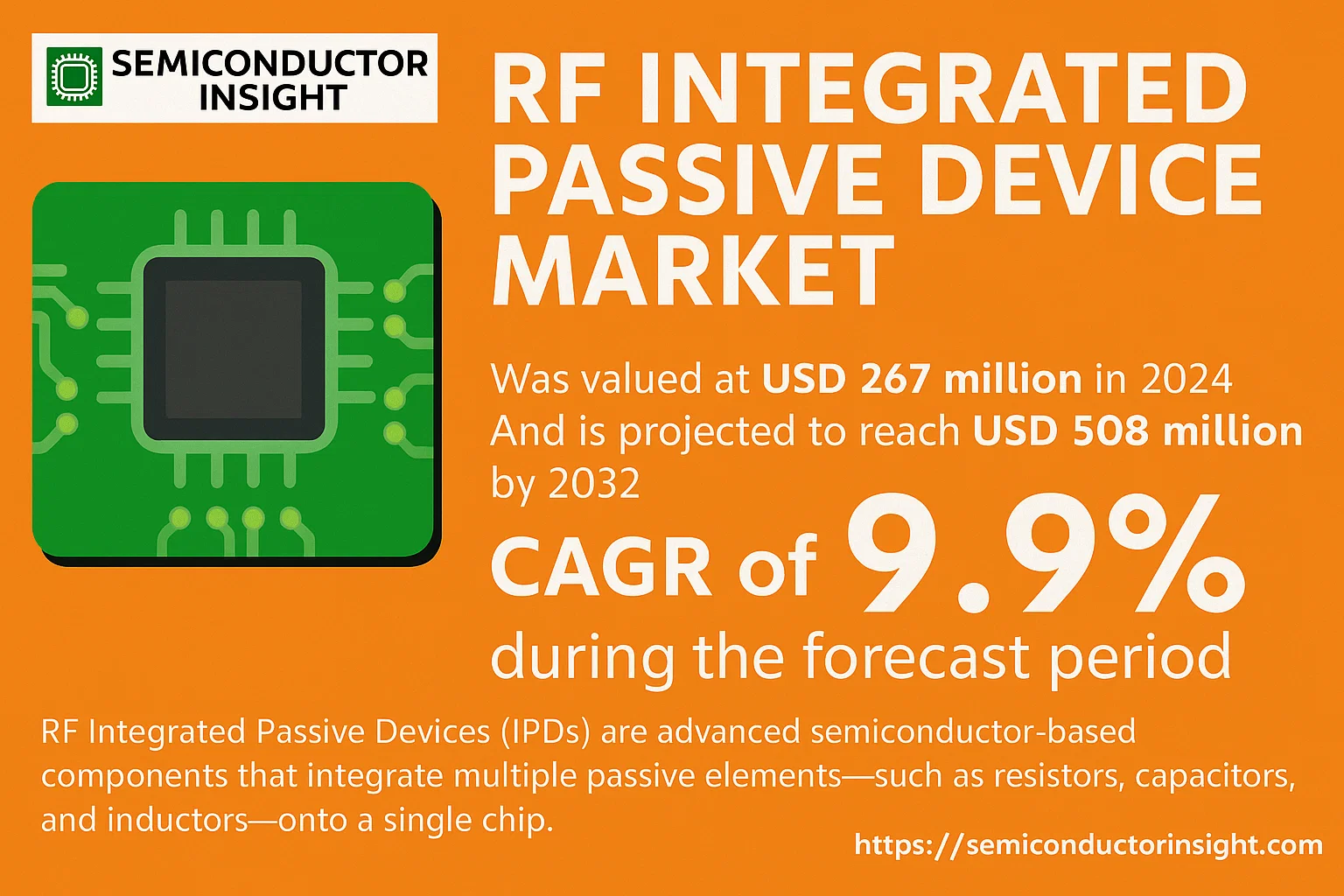

Global RF Integrated Passive Device Market was valued at USD 267 million in 2024 and is projected to reach USD 508 million by 2032, exhibiting a CAGR of 9.9% during the forecast period.

RF Integrated Passive Devices (IPDs) are advanced semiconductor-based components that integrate multiple passive elements—such as resistors, capacitors, and inductors—onto a single chip. This integration significantly reduces the size, weight, and cost of electronic circuits while improving performance and reliability. These devices are crucial for high-frequency applications in wireless communication, including 5G infrastructure, Internet of Things (IoT) devices, and advanced automotive systems. The market’s growth is primarily driven by the increasing demand for miniaturization in electronics, the rapid expansion of 5G networks, and the proliferation of IoT devices across the globe.

Key manufacturers such as Broadcom, Murata, and Skyworks are focusing on innovation to enhance the performance of these devices, particularly in reducing power loss and improving signal integrity. The Asia-Pacific region dominates the market due to its large electronics manufacturing base and the presence of major market players. However, the market faces challenges such as the complexity of design and integration, which require significant R&D investment. Recent developments include collaborations between semiconductor companies and material scientists to develop next-generation IPDs with higher efficiency and lower costs.

MARKET DRIVERS

Proliferation of 5G Infrastructure and Smartphones

The global rollout of 5G networks and the corresponding demand for 5G-enabled smartphones are primary drivers for the RF Integrated Passive Device (IPD) market. These devices are essential for creating compact, high-performance filters, baluns, and couplers in 5G transceivers and antenna modules. The need for increased bandwidth and lower latency necessitates advanced RF components that can operate efficiently at higher frequencies, a key strength of IPD technology.

Demand for Miniaturization in Consumer Electronics

The relentless trend towards smaller, thinner, and more powerful consumer electronics, such as wearables and Internet of Things (IoT) devices, fuels the adoption of RF IPDs. By integrating multiple passive components into a single package, IPDs significantly reduce the overall footprint on a printed circuit board (PCB). This miniaturization is critical for modern device design without compromising performance, enabling sleeker form factors.

➤ The global market for RF IPDs is projected to grow at a compound annual growth rate of approximately 9% over the next five years, largely driven by the automotive and telecommunications sectors.

Furthermore, the expansion of automotive radar systems for advanced driver-assistance systems (ADAS) and vehicle-to-everything (V2X) communication represents a significant growth vector. RF IPDs provide the necessary reliability and performance in harsh automotive environments, supporting features like collision avoidance and autonomous driving.

MARKET CHALLENGES

High Initial Development and Fabrication Costs

The design and fabrication of RF IPDs require specialized processes, such as thin-film technology on high-resistivity substrates, which involve significant upfront investment. This creates a high barrier to entry for new players and can deter widespread adoption in extremely cost-sensitive applications. The need for custom design and validation for each application further adds to the overall cost structure.

Other Challenges

Performance Limitations at Extremely High Frequencies

While RF IPDs perform well in sub-6 GHz and mmWave bands up to a point, achieving consistent performance and high Q-factors at the upper end of the mmWave spectrum (e.g., above 40 GHz) remains technically challenging. Competing technologies like Low-Temperature Co-fired Ceramic (LTCC) can sometimes offer better performance in these extreme frequency ranges.

Integration Complexity with Advanced Semiconductor Nodes

Integrating RF IPDs with advanced system-on-chip (SoC) designs based on sub-10nm nodes presents complexities. Managing thermal dissipation, electromagnetic interference (EMI), and ensuring signal integrity in such highly integrated environments requires sophisticated co-design and packaging expertise.

MARKET RESTRAINTS

Competition from Alternative Integrated Passive Technologies

The RF IPD market faces strong competition from other integrated passive technologies, such as LTCC and semiconductor-based integrated passive and active devices (IPADs). These alternatives often have established supply chains and can be more cost-effective for certain high-volume, lower-performance applications, limiting the addressable market for RF IPDs.

Supply Chain Vulnerabilities for Specialty Materials

The production of high-performance RF IPDs relies on specialty substrates like high-resistivity silicon or glass. Disruptions in the supply chain for these niche materials can lead to production delays and increased costs, acting as a restraint on market growth. Geopolitical factors and limited supplier bases exacerbate this vulnerability.

Additionally, the long design and qualification cycles for applications in automotive and medical sectors can slow down time-to-market. The rigorous reliability testing and certification requirements mean that adoption in these industries is a slow process, restraining short-term revenue growth.

MARKET OPPORTUNITIES

Expansion in Millimeter-Wave Applications for 6G and Satellite Communication

The ongoing research and development for 6G cellular technology and the rapid growth of low-earth orbit (LEO) satellite communication networks (e.g., Starlink) present substantial opportunities. These applications operate in high-frequency mmWave and terahertz bands, where the small form factor and excellent performance of RF IPDs are highly advantageous for phased-array antennas and beamforming networks.

Growth of the Internet of Things (IoT) and Wireless Sensor Networks

The proliferation of IoT devices and industrial wireless sensor networks requires compact, low-power, and reliable RF front-end components. RF IPDs are ideal for integrating matching networks, filters, and baluns in these applications, enabling longer battery life and smaller device sizes. This market segment is expected to be a major source of volume demand.

Emerging applications in medical devices, such as implantable sensors and wireless monitoring systems, also offer niche but high-value opportunities. The biocompatibility and reliability of RF IPD technology make it suitable for critical healthcare applications where miniaturization and performance are paramount.

RF Integrated Passive Device Market Trends

Robust Growth Fueled by Miniaturization and Wireless Connectivity

The global RF Integrated Passive Device (IPD) market is experiencing significant expansion, with its valuation projected to surge from US$ 267 million in 2024 to US$ 508 million by 2032, representing a compound annual growth rate (CAGR) of 9.9%. This robust growth is primarily driven by the relentless demand for smaller, more efficient electronic devices. RF IPD technology is fundamental to this trend, as it embeds essential passive components like capacitors, inductors, filters, baluns, and combiners into a single monolithic device. This integration drastically reduces the component footprint and energy consumption while simultaneously enhancing overall RF performance, making it indispensable for modern wireless applications.

Other Trends

Dominance of Consumer Electronics and Automotive Applications

The application landscape is heavily concentrated in consumer electronics, which accounts for the largest market segment. The proliferation of smartphones, tablets, wearables, and IoT devices that require connectivity standards like Bluetooth, Wi-Fi (WLAN), LTE, UWB, and ZigBee is a key driver. Concurrently, the automobile sector is a rapidly growing segment, with increasing integration of advanced driver-assistance systems (ADAS), infotainment, and vehicle-to-everything (V2X) communication, all demanding high-performance RF components that IPDs provide. These applications leverage IPDs to minimize power loss and enhance signal transmission across a wide frequency spectrum, from 168 MHz and above.

Consolidated Market and Regional Dynamics

The competitive landscape is characterized by a high degree of consolidation, with the top five manufacturers—including Broadcom, Murata, and Skyworks—holding approximately 75% of the global market share. Geographically, the Asia-Pacific region is the dominant force, accounting for roughly 70% of the market. This dominance is attributed to the region’s vast electronics manufacturing base and strong consumer demand. North America and Europe collectively hold a share of about 20%, with their markets being driven by advanced technological adoption in sectors like aerospace, defense, and high-end automotive. The market is further segmented by substrate material, with Silicon-based, Glass-based, and GaAs-based IPDs catering to different performance and cost requirements across these diverse applications and regions.

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidated Market Led by Semiconductor and Component Giants

The global RF Integrated Passive Device (IPD) market is characterized by a high degree of consolidation, with the top five companies collectively holding approximately 75% of the market share. This dominance is led by established semiconductor and electronic component manufacturers such as Broadcom, Murata, and Skyworks Solutions. These industry behemoths leverage their extensive R&D capabilities, global manufacturing scale, and strong relationships with major consumer electronics and telecommunications equipment manufacturers to maintain their leading positions. Their product portfolios encompass a wide range of IPD technologies, including silicon-based, glass-based, and GaAs-based solutions, catering to diverse applications from smartphones and Wi-Fi routers to automotive radar systems.

Beyond the top-tier leaders, a number of other significant players compete effectively by specializing in particular technologies or market niches. Companies like Johanson Technology and AVX/Kyocera are recognized for their expertise in high-performance passive components, which they have extended into integrated solutions. Specialized firms such as 3D Glass Solutions (3DGS) focus on innovative glass-based IPD substrates, offering unique benefits for high-frequency applications. Chinese players, including Xpeedic, are gaining traction by providing cost-competitive design solutions and supporting the robust electronics manufacturing ecosystem in the Asia-Pacific region, which itself accounts for about 70% of the global market.

List of Key RF Integrated Passive Device Companies Profiled

- Broadcom Inc.

- Murata Manufacturing Co., Ltd.

- Skyworks Solutions, Inc.

- ON Semiconductor

- STMicroelectronics N.V.

- AVX Corporation (Kyocera Group)

- Johanson Technology, Inc.

- 3D Glass Solutions (3DGS)

- Xpeedic Technology Inc.

- Taiyo Yuden Co., Ltd.

- Qorvo, Inc.

- TDK Corporation

- Infineon Technologies AG

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon-based IPDs are dominant due to their superior cost-effectiveness and high-volume manufacturing scalability, which aligns with the demands of the consumer electronics industry. While GaAs-based devices offer excellent high-frequency performance, the established infrastructure for silicon processing gives it a significant advantage. The versatility of silicon substrates in integrating complex passive networks while maintaining a competitive cost structure solidifies its leading position. |

| By Application |

|

Consumer Electronics is the most significant application segment, driven by the pervasive integration of wireless connectivity features like Bluetooth, Wi-Fi, and cellular into smartphones, tablets, and wearables. The relentless drive for device miniaturization and improved power efficiency makes the small form factor and reduced power losses of RF IPDs essential. The high-volume nature of this sector creates sustained and substantial demand, making it the clear market leader. |

| By End User |

|

Original Equipment Manufacturers (OEMs) represent the primary end-user segment, as they are the direct integrators of RF IPDs into final products such as smartphones and automotive infotainment systems. These manufacturers have a strong focus on maintaining supply chain control and ensuring component performance and reliability for their branded products. Their direct, high-volume purchasing power and strategic partnerships with key IPD suppliers cement their leading role in the market. |

| By Technology Function |

|

Filters and Baluns are the cornerstone functions within the RF IPD market, as signal integrity is paramount in all wireless applications. Filters are critical for selecting desired frequency bands and rejecting interference, while baluns are essential for converting between single-ended and differential signals in modern RF circuits. The consistent need for these functions across a vast range of devices, from simple connectivity modules to complex 5G systems, underpins the dominance of this functional segment. |

| By Integration Level |

|

Subsystem IPD Modules are gaining significant traction as they offer an optimal balance between performance, design flexibility, and time-to-market. While discrete IPDs offer maximum design freedom, and fully integrated FEMs provide a turnkey solution, subsystem modules that combine several passive functions into a single device are leading. They provide substantial space savings and performance optimization over discrete solutions without the design lock-in of a full FEM, making them highly attractive for a wide array of applications. |

Regional Analysis: RF Integrated Passive Device Market

The region’s dominance is underpinned by its integrated supply chain, from raw wafer production to advanced packaging. This proximity allows for rapid prototyping and volume manufacturing, reducing time-to-market for new RF IPD designs and enabling close collaboration between device makers and component suppliers to meet the specific performance and size requirements of next-generation electronics.

Aggressive nationwide 5G rollout strategies, particularly in China and South Korea, are creating immense demand for RF IPDs used in infrastructure and user equipment. Concurrently, the explosion of IoT applications across industrial, automotive, and smart home sectors in the region drives the need for compact, reliable passive integration for connectivity modules, further solidifying market growth.

Significant investments in research and development are focused on enhancing RF IPD performance for higher frequency bands required by 5G mmWave and advanced WiFi standards. Regional players are leaders in developing IPDs with improved quality factors, lower insertion losses, and greater integration capabilities, often leveraging novel substrate materials like glass or high-resistivity silicon.

The high-volume, cost-sensitive nature of the consumer electronics market in Asia-Pacific pressures RF IPD manufacturers to achieve economies of scale while maintaining quality. This environment fosters intense competition and innovation in manufacturing processes, leading to highly optimized production that delivers performance at a cost point that is challenging for other regions to match.

North America

North America remains a critical and technologically advanced market for RF IPDs, characterized by strong demand from the aerospace, defense, and high-end telecommunications sectors. The presence of major semiconductor companies and demanding applications in areas like satellite communications, radar systems, and test and measurement equipment drives the need for high-performance, ruggedized RF IPDs. Innovation is a key differentiator, with a focus on custom-designed IPDs for specialized applications that require exceptional reliability and performance under extreme conditions. The region’s early adoption of new wireless standards also fuels demand for advanced IPD solutions.

Europe

The European market for RF IPDs is mature and stable, with significant activity in the automotive and industrial IoT sectors. The strong automotive industry, particularly in Germany, demands robust RF IPDs for vehicle connectivity, advanced driver-assistance systems (ADAS), and infotainment. Stringent European regulations regarding electromagnetic compatibility (EMC) and spectral efficiency also influence IPD design, favoring solutions that offer superior filtering and signal integrity. Collaboration between academic institutions and industry players supports ongoing R&D in areas like RF energy harvesting and sensors.

South America

The South American RF IPD market is emerging, with growth primarily driven by the gradual expansion of 4G LTE networks and the early stages of 5G deployment, particularly in Brazil. Demand is centered on consumer mobile devices and basic telecommunications infrastructure. The market faces challenges related to economic volatility and infrastructure development, but increasing mobile penetration and government initiatives to improve digital connectivity present long-term growth opportunities for RF IPD adoption in consumer electronics and network equipment.

Middle East & Africa

This region shows diverse and developing demand for RF IPDs. Wealthier Gulf Cooperation Council (GCC) nations are investing heavily in smart city projects and 5G infrastructure, creating demand for advanced components. In other parts of Africa, market growth is linked to the expansion of basic mobile networks and the increasing affordability of smartphones. The market is fragmented, with demand ranging from high-end infrastructure components in urban centers to cost-effective solutions for entry-level devices in expanding mobile markets.

Report Scope

This market research report provides a comprehensive analysis of the RF Integrated Passive Device Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Integrated Passive Device Market?

-> RF Integrated Passive Device Market was valued at USD 267 million in 2024 and is projected to reach USD 508 million by 2032, exhibiting a CAGR of 9.9% during the forecast period.

Which key companies operate in RF Integrated Passive Device Market?

-> Key players include Broadcom, Murata, Skyworks, ON Semiconductor, and STMicroelectronics, among others. These top players hold a combined market share of about 75%.

What are the key growth drivers?

-> Key growth drivers include the demand for miniaturized electronic devices, reduced power consumption, and enhanced RF performance in applications like Bluetooth, WLAN, LTE, UWB, and ZigBee.

Which region dominates the market?

-> Asia-Pacific is the largest market, with a share of about 70%, followed by North America and Europe, which each hold a share of about 20%.

What are the emerging trends?

-> Emerging trends include the integration of passive elements into monolithic devices for smaller form factors, competitive cost structures, and the expansion of RF applications across various wireless communication standards.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...