MARKET INSIGHTS

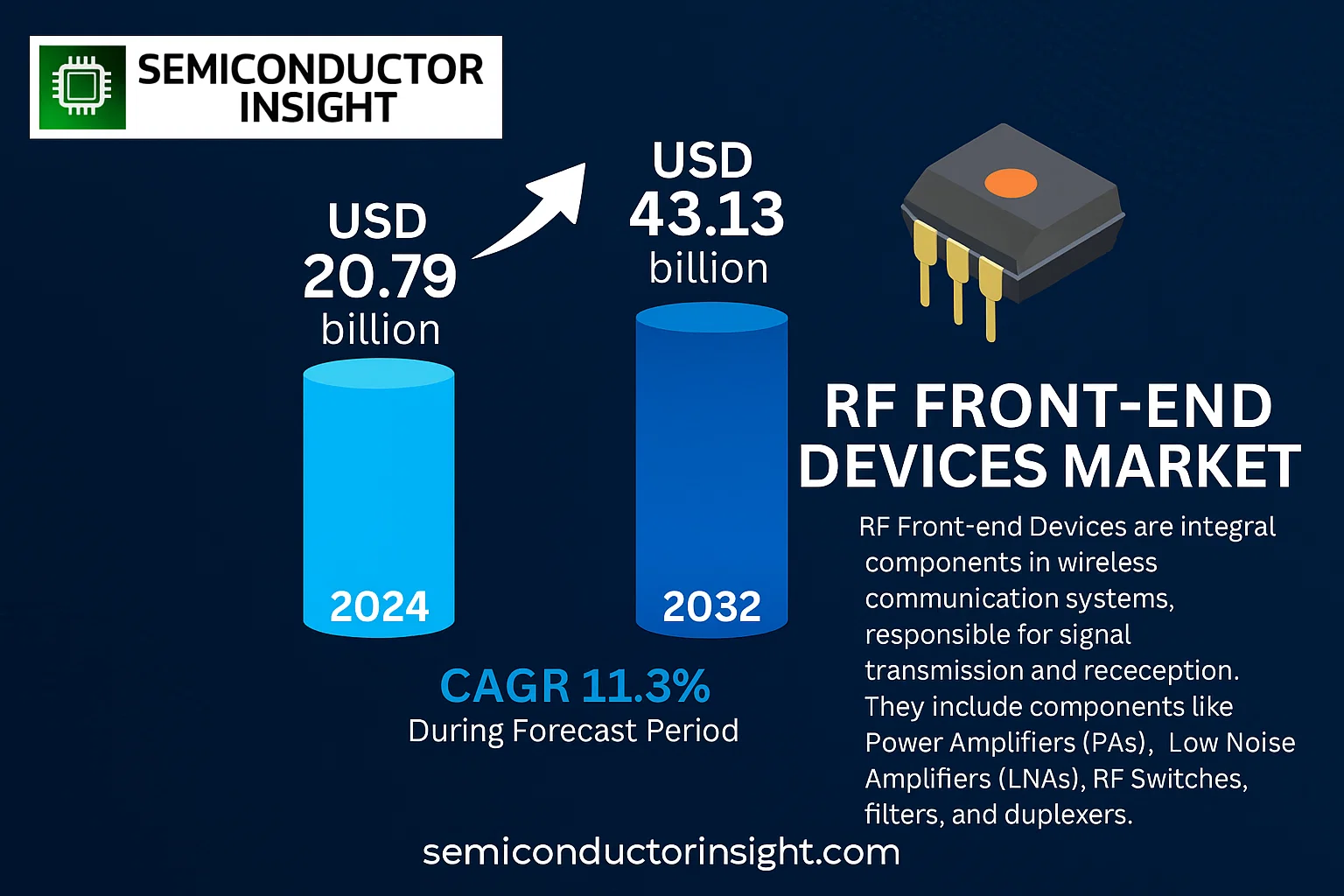

Global RF Front-end Devices Market was valued at USD 20.79 billion in 2024 and is projected to reach USD 43.13 billion by 2032, exhibiting a CAGR of 11.3% during the forecast period.

RF Front-end Devices are integral components in wireless communication systems, responsible for signal transmission and reception. They include components like Power Amplifiers (PAs), Low Noise Amplifiers (LNAs), RF switches, filters, and duplexers. The market is experiencing significant growth due to the proliferation of 5G networks, the Internet of Things (IoT), and the increasing adoption of advanced consumer electronics. The rising demand for high-speed data transmission, coupled with advancements in semiconductor technology, is a key driver. However, the market faces challenges such as design complexity, high research and development costs, and the need for miniaturization.

Geographically, the Asia-Pacific region, particularly China, is the largest market due to its massive electronics manufacturing industry and high consumer electronics adoption. North America follows, driven by advanced communication infrastructure and high R&D investments. The market is highly competitive, with key players including Murata Manufacturing Co., Ltd., Broadcom Inc., Qualcomm, Qorvo, Skyworks Solutions Inc., NXP, TDK, and Texas Instruments.

MARKET DRIVERS

Proliferation of 5G Infrastructure and Smartphones

The global rollout of 5G networks is a primary catalyst for the RF front-end (RFFE) market. The transition to 5G requires smartphones and network infrastructure to support new frequency bands, including Sub-6 GHz and millimeter-wave (mmWave), which in turn drives demand for more complex RFFE modules containing power amplifiers, filters, switches, and low-noise amplifiers. The increasing number of 5G-capable device launches from major manufacturers is a significant and continuous source of demand.

Expansion of IoT and Connected Devices

The explosive growth of the Internet of Things (IoT) across consumer, industrial, and automotive applications is a major driver. Billions of new connected devices—from smart home sensors to industrial monitors and vehicle telematics—require robust and often miniaturized RFFE components to enable wireless connectivity standards like Wi-Fi 6/6E, Bluetooth, NB-IoT, and LoRaWAN.

➤ The integration of advanced RFFE components is crucial for enabling high-speed, low-latency communication in modern mobile and IoT ecosystems.

Furthermore, the automotive industry’s shift toward connected and autonomous vehicles is creating a new, high-growth segment for RFFE devices, which are essential for cellular vehicle-to-everything (C-V2X) communication, advanced driver-assistance systems (ADAS), and in-car infotainment.

MARKET CHALLENGES

Design Complexity and Performance Demands

Designing RFFE modules for modern communication standards is increasingly complex. Engineers must balance conflicting demands for higher performance (e.g., greater bandwidth, improved efficiency), smaller form factors, and lower power consumption, all while managing signal integrity and avoiding interference in devices packed with multiple radios.

Other Challenges

Supply Chain and Geopolitical Pressures

The RFFE market is susceptible to semiconductor supply chain disruptions and geopolitical tensions, which can affect the availability and cost of critical materials and manufacturing capacity. Reliance on a limited number of specialized foundries for advanced semiconductor processes adds to the vulnerability.

Cost and Price Pressure

Despite their increasing complexity, RFFE components face intense price pressure from smartphone OEMs and other device manufacturers, especially in highly competitive market segments. This pressure challenges vendors to innovate while maintaining cost-effectiveness.

MARKET RESTRAINTS

High Research and Development Costs

The significant investment required for research and development acts as a major restraint. Developing next-generation RFFE solutions that support new standards and integrate more functions into a single module requires substantial capital and specialized engineering talent, creating a high barrier to entry for new players and pressuring profitability.

Technical Limitations of Semiconductor Materials

While Gallium Arsenide (GaAs) and Silicon Germanium (SiGe) are well-established, pushing performance limits—especially for high-frequency mmWave applications—presents challenges. The adoption of newer materials like Gallium Nitride (GaN) is growing but involves higher costs and manufacturing complexities that can slow widespread implementation in cost-sensitive consumer devices.

MARKET OPPORTUNITIES

Advancements in Front-End Module Integration

There is a significant opportunity in the development of highly integrated modules, such as PaMiDs (PAs + Modules integrated Duplexers) and LNA-Filter modules. These integrated solutions reduce the overall footprint, simplify handset design, and improve performance, offering a strong value proposition for smartphone OEMs striving for thinner and more feature-rich devices.

Growth in Non-Handset Applications

Beyond smartphones, substantial growth is anticipated in markets such as automotive radar systems, wireless infrastructure for 5G small cells, and ultra-reliable low-latency communication (URLLC) for industrial IoT. These applications often have less stringent cost constraints than consumer electronics and require high-performance, ruggedized RFFE components.

Global RF Front-end Devices Market Trends

Sustained Growth Driven by Proliferation of Connected Devices

The global RF Front-end Devices market is on a significant growth trajectory, with its value projected to rise from $20,790 million in 2024 to $43,130 million by 2032, representing a compound annual growth rate (CAGR) of 11.3%. This expansion is fundamentally linked to the ever-increasing demand for consumer electronics and the global rollout of advanced wireless communication standards, including 5G. The market’s dynamism is underpinned by the critical role RF front-end components play in enabling connectivity, signal processing, and data transmission in modern devices.

Other Trends

Market Consolidation and Regional Dominance

The competitive landscape is characterized by a high degree of consolidation, with the top five players—Murata Manufacturing Co., Ltd., Broadcom Inc., Qualcomm, Qorvo, and Skyworks Solutions Inc.—collectively holding approximately 66% of the market share. Geographically, China stands as the largest market, accounting for about 45% of the global share, followed by North America and Southeast Asia. This regional concentration reflects the hubs of consumer electronics manufacturing and the rapid adoption of new communication technologies in these areas.

Product and Application Segmentation

In terms of product type, Radio Frequency Filters constitute the largest segment, commanding over 47% of the market. This dominance is due to the critical need for effective signal filtering to manage interference in increasingly crowded frequency bands. On the application front, Consumer Electronic Products, such as smartphones and tablets, are the primary drivers, representing over 81% of the market. The wireless communication products segment also contributes substantially to market volume.

Technological Advancements and Future Outlook

The industry is continuously evolving with advancements aimed at improving power efficiency, supporting higher frequency bands for 5G mmWave applications, and enabling the integration of multiple components into compact modules. As the Internet of Things (IoT) and automotive connectivity gain momentum, new application areas are expected to emerge, further fueling market growth. However, manufacturers face challenges related to design complexity, supply chain stability, and intense price competition. The ongoing innovation and expansion into new sectors position the RF front-end market for robust long-term development.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Consolidated Amongst Global Semiconductor Giants

The global RF Front-end Devices market is characterized by a high level of consolidation, with the top five players, led by Murata Manufacturing Co., Ltd., Broadcom Inc., Qualcomm, Qorvo, and Skyworks Solutions Inc., collectively accounting for approximately 66% of the market share. This dominance is built on extensive intellectual property portfolios, significant R&D investments, and strong relationships with major consumer electronics and telecommunications equipment manufacturers worldwide. These leaders compete intensely on technological innovation, particularly in developing integrated modules for 5G and Wi-Fi 6/6E applications. The market is primarily driven by the demand for advanced smartphones and wireless infrastructure, with China being the largest regional market, accounting for about 45% of the global share. The largest product segment is the Radio Frequency Filter, holding over 47% of the market, as filters are critical for managing spectrum congestion and ensuring signal integrity in multi-band devices.

Beyond the dominant players, a number of other significant companies hold important positions in niche segments or regional markets. Companies like NXP, TDK, and Texas Instruments offer robust portfolios of discrete components and integrated solutions for automotive and industrial applications. European semiconductor leader Infineon Technologies AG is a key player, especially in power semiconductors that interface with RF systems. A cohort of specialized Chinese companies, including Maxscend, UNISOC, and VANCHIP, are rapidly growing, supported by domestic market demand and government initiatives. These firms are increasingly competing in the mid-range smartphone segment and specific wireless communication applications, contributing to the dynamic and competitive nature of the global landscape. Other notable players like Ampleon focus on high-performance RF power for infrastructure, while STMicroelectronics and Analog Devices Inc. (ADI) provide critical components for a broad range of markets.

List of Key RF Front-end Devices Companies Profiled

- Murata Manufacturing Co., Ltd.

- Broadcom Inc.

- Qualcomm

- Qorvo

- Skyworks Solutions Inc.

- NXP Semiconductors N.V.

- TDK Corporation

- Texas Instruments Incorporated

- Infineon Technologies AG

- Maxscend Microelectronics Co., Ltd.

- STMicroelectronics N.V.

- Ampleon Netherlands B.V.

- TAIYO YUDEN CO., LTD.

- UNISOC (Shanghai) Technologies Co., Ltd.

- VANCHIP (Tianjin) Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

RF Filter represents the leading product segment, driven by its critical function in managing signal integrity and eliminating interference across a vast range of wireless devices. Its fundamental role in enabling clear communication in the increasingly congested radio frequency spectrum ensures sustained demand. The continuous evolution of communication standards, which require more sophisticated filtering solutions, further solidifies the dominance of this segment within the broader device ecosystem. |

| By Application |

|

Consumer Electronic Products is the dominant application segment, fueled by the pervasive integration of wireless connectivity in everyday devices like smartphones, tablets, wearables, and smart home appliances. The sheer volume of production and the constant demand for upgraded features in these consumer goods create a massive and consistent market for RF front-end components. Innovations in this space directly translate into requirements for more advanced, power-efficient, and compact RF solutions. |

| By End User |

|

Consumer Electronics OEMs constitute the leading end-user segment due to their role as the primary integrators of RF front-end modules into final products for the mass market. These OEMs drive innovation and volume requirements, demanding components that offer superior performance, miniaturization, and cost-effectiveness to remain competitive. Their supply chain relationships and purchasing power significantly influence the direction and priorities of RF front-end device manufacturers. |

| By Frequency Band |

|

Sub-6 GHz is the leading frequency segment, serving as the backbone for the vast majority of current wireless communication standards including 4G LTE and the foundational layer of 5G networks. This band offers an optimal balance between coverage area and data capacity, making it the most widely deployed and utilized spectrum globally. The ongoing global rollout of 5NR in these frequencies ensures its continued dominance, driving demand for RF front-end devices optimized for this range. |

| By Integration Level |

|

Integrated Modules/FEMiD represent the dominant segment in terms of integration level, as they offer a compelling combination of performance, size reduction, and design simplification for OEMs. These modules, which combine multiple front-end components like power amplifiers, switches, and filters into a single package, are increasingly favored in space-constrained applications like smartphones. The trend towards higher integration is a key technological driver, balancing performance optimization with the pressing need for miniaturization in modern electronics. |

Regional Analysis: RF Front-end Devices Market

Asia-Pacific’s dominance is rooted in its world-leading electronics manufacturing capabilities, with a deep and mature supply chain for semiconductor components. This ecosystem enables rapid prototyping, large-scale production, and cost leadership, making it the primary global hub for sourcing RF front-end modules for everything from budget to premium smartphones and other connected devices, ensuring market leadership.

The aggressive and widespread deployment of 5G networks across major economies in the region serves as a primary catalyst for market growth. This expansion necessitates a massive influx of sophisticated RF front-end components capable of handling higher frequencies and complex signal modulation, driving innovation and volume demand that keeps the regional market at the forefront of global developments.

An enormous and tech-savvy consumer base fuels continuous demand for the latest smartphones, tablets, and wearable devices, all of which require advanced RF front-end solutions. Local Original Equipment Manufacturers (OEMs) are key drivers, constantly pushing for more efficient and powerful RF components to differentiate their products in a highly competitive market.

Strong governmental initiatives and significant private sector investment in research and development foster a continuous cycle of innovation. This environment supports the advancement of critical technologies like RF filters for spectrum crowding and power amplifiers for energy efficiency, ensuring the region’s products remain competitive and aligned with future wireless communication standards.

North America

North America remains a critical and highly advanced market for RF front-end devices, characterized by early adoption of new wireless technologies and a concentration of leading fabless semiconductor companies that design cutting-edge components. The region’s market is propelled by substantial investments in 5G infrastructure by major telecommunications carriers, demanding high-performance devices for network equipment and flagship smartphones. A strong focus on defense and aerospace applications also provides a steady, high-value demand for specialized, ruggedized RF components. The presence of major technology giants and a robust ecosystem for innovation in areas like automotive radar and IoT ensures that North America continues to be a key center for high-value design and early-stage deployment, influencing global specifications and standards.

Europe

The European market for RF front-end devices is driven by a strong automotive industry, significant investments in industrial IoT, and coordinated efforts for 5G deployment across the European Union. The region exhibits a strong demand for reliable and high-quality components, particularly for automotive radar systems, smart manufacturing, and telecommunications infrastructure. Strict regulatory standards and a focus on energy efficiency shape the demand for RF solutions that meet specific performance and environmental criteria. Collaborative research initiatives and the presence of several key industrial and telecommunications equipment manufacturers ensure that Europe maintains a significant, innovation-focused segment within the global RF front-end landscape, with a particular emphasis on quality and specialized applications.

South America

The South American market for RF front-end devices is in a growth phase, primarily driven by the gradual expansion of 4G LTE networks and the nascent rollout of 5G services in larger economies like Brazil. Market dynamics are influenced by the increasing smartphone penetration and a growing demand for mobile data services. The region presents opportunities tied to the need for cost-effective solutions that can cater to price-sensitive consumers while supporting network modernization. While the market is smaller compared to other regions, its growth potential is significant, with development closely linked to economic stability and infrastructure investments by telecommunications operators aiming to bridge the digital divide.

Middle East & Africa

The Middle East & Africa region shows a diverse and evolving market for RF front-end devices. Wealthier Gulf Cooperation Council countries are actively deploying advanced 5G networks, creating demand for high-end components. In contrast, many African nations are focused on expanding basic 3G and 4G coverage, driving demand for more fundamental RF solutions. The market is characterized by a strong need for robust components capable of operating in challenging environmental conditions. Growth is fueled by urbanization, rising mobile subscription rates, and investments in digital infrastructure, making it a region of long-term potential, albeit with varying levels of maturity and investment across its vast geography.

Report Scope

This market research report provides a comprehensive analysis of the RF Front-end Devices Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Front-end Devices Market?

-> RF Front-end Devices Market was valued at USD 20.79 billion in 2024 and is projected to reach USD 43.13 billion by 2032, exhibiting a CAGR of 11.3% during the forecast period.

Which key companies operate in RF Front-end Devices Market?

-> Key players include Murata Manufacturing Co., Ltd., Broadcom Inc., Qualcomm, Qorvo, Skyworks Solutions Inc., NXP, TDK, and Texas Instruments, among others. The top five players occupy a market share of approximately 66%.

What are the key growth drivers?

-> Key growth drivers include the expansion of 5G networks, increasing demand for consumer electronic products, and advancements in wireless communication technologies.

Which region dominates the market?

-> China is the largest market, with a share of about 45%, followed by North America and Southeast Asia.

What are the emerging trends?

-> Emerging trends include the rising dominance of Radio Frequency Filters, integration of RF components for IoT devices, and development of advanced solutions for automotive and industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...