MARKET INSIGHTS

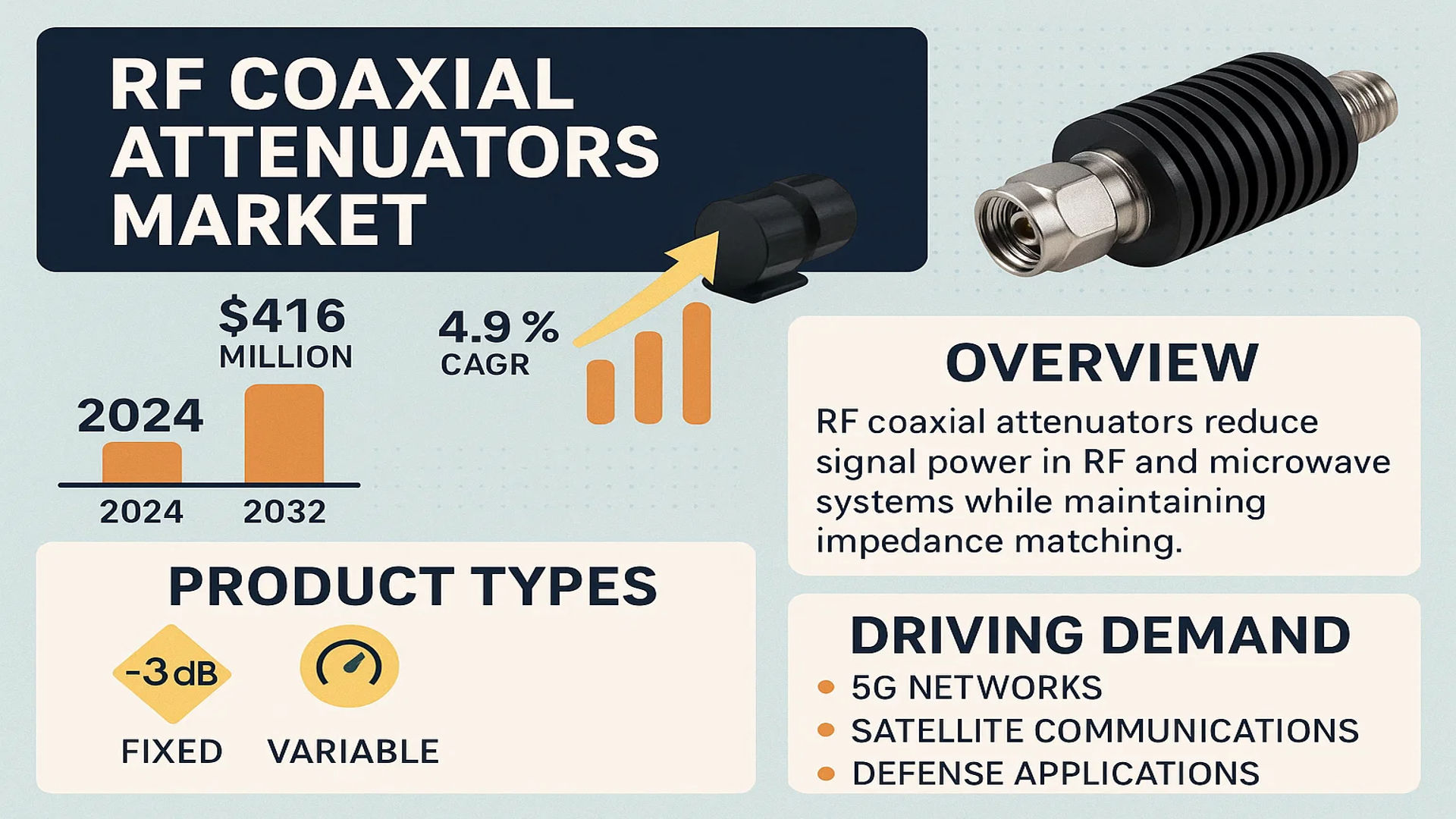

The global RF Coaxial Attenuators Market was valued at 416 million in 2024 and is projected to reach US$ 578 million by 2032, at a CAGR of 4.9% during the forecast period.

RF coaxial attenuators are passive components designed to reduce signal power in radio frequency (RF) and microwave systems while maintaining impedance matching. These devices contain precisely engineered resistive materials within a coaxial structure to ensure minimal signal distortion. Key applications include protecting sensitive equipment from excessive signal levels, improving signal-to-noise ratios, and matching impedances between different circuit components. The market offers two primary product types: fixed attenuators with constant attenuation values and variable attenuators offering adjustable signal reduction.

The market growth is driven by increasing demand for high-frequency communication systems, particularly in 5G networks, satellite communications, and defense applications. The U.S. currently dominates the market, while China is emerging as the fastest-growing region due to rapid telecommunications infrastructure development. Leading players like Infinite Electronics, Huber+Suhner, and Radiall collectively hold significant market share, continuously innovating to meet evolving industry requirements for higher frequency ranges and lower insertion losses.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Telecommunications Infrastructure to Accelerate Market Growth

The global telecommunications industry is undergoing massive transformation with the rollout of 5G networks and the increasing adoption of IoT devices. RF coaxial attenuators play a critical role in maintaining signal integrity across these networks, driving demand across both developed and emerging markets. With over 1.5 billion 5G subscriptions projected globally by 2025, the need for high-performance RF components like coaxial attenuators continues to surge. These components help manage power levels in base stations and antenna systems, ensuring optimal network performance despite growing data traffic and spectrum complexity.

Increasing Defense Budgets Worldwide to Propel RF Attenuator Adoption

Defense applications account for a significant portion of RF coaxial attenuator demand due to their use in radar systems, electronic warfare, and secure communications. Global military expenditures surpassed $2 trillion for the first time, with major economies prioritizing modernization of defense electronics. RF attenuators provide crucial signal conditioning in these systems, protecting sensitive components from power surges while maintaining signal clarity. The shift toward software-defined radio (SDR) technologies in military communications further amplifies the need for precision attenuators that can operate across multiple frequency bands.

Furthermore, growing investments in satellite communications and space technologies create additional demand. Modern satellite constellations require robust RF components that can withstand extreme environmental conditions while delivering consistent performance. RF coaxial attenuators meet these rigorous requirements, making them indispensable for both commercial and military space applications.

MARKET RESTRAINTS

Performance Limitations at Millimeter-Wave Frequencies Challenge Market Expansion

While RF coaxial attenuators perform exceptionally well in traditional microwave bands, their effectiveness diminishes at higher millimeter-wave (mmWave) frequencies above 30 GHz. This presents a significant constraint as 5G networks increasingly utilize these higher frequency bands to deliver ultra-fast data rates. The physical constraints of coaxial design make it challenging to maintain consistent attenuation levels and impedance matching at these elevated frequencies, often requiring more complex and expensive solutions.

Additionally, thermal management becomes problematic at mmWave frequencies due to increased power dissipation. These technical limitations force system designers to explore alternative solutions such as waveguide attenuators in certain applications, potentially restricting market growth for coaxial variants in cutting-edge deployments.

MARKET CHALLENGES

Supply Chain Disruptions and Material Shortages Impact Production Capacity

The RF coaxial attenuator market faces persistent challenges from global supply chain volatility and material shortages. Critical components such as specialized resistive materials, precision connectors, and high-performance dielectric substrates have experienced extended lead times and price fluctuations. These disruptions particularly affect custom attenuator designs that require specific material properties for niche applications.

Other Challenges

Skill Gap in RF Engineering

The industry struggles with a shortage of experienced RF engineers capable of designing and testing advanced attenuator solutions. As technologies evolve toward higher frequencies and broader bandwidths, the need for specialized expertise intensifies, yet educational pipelines fail to produce sufficient qualified professionals.

Miniaturization Demands

Increasing requirements for compact, lightweight attenuators strain traditional manufacturing processes. The push for smaller form factors while maintaining thermal performance and power handling creates complex engineering trade-offs that challenge product development timelines.

MARKET OPPORTUNITIES

Emerging Automotive Radar Applications Present Significant Growth Potential

The automotive sector represents a rapidly growing opportunity for RF coaxial attenuator manufacturers. Advanced driver assistance systems (ADAS) and autonomous vehicle technologies rely heavily on millimeter-wave radar systems that require precision signal conditioning. With automotive radar shipments expected to exceed 70 million units annually by 2027, the demand for rugged, temperature-stable attenuators continues to surge. These applications demand components that can maintain performance across extreme environmental conditions while meeting stringent automotive reliability standards.

Furthermore, the expansion of connected vehicle technologies and vehicle-to-everything (V2X) communications creates additional requirements for RF signal management solutions. Manufacturers developing attenuators specifically optimized for automotive applications stand to capture significant market share as these technologies achieve broader adoption.

RF COAXIAL ATTENUATORS MARKET TRENDS

5G Network Expansion Driving Adoption of High-Frequency RF Coaxial Attenuators

The rapid global rollout of 5G networks is significantly boosting demand for high-frequency RF coaxial attenuators that operate in millimeter-wave bands (24-100 GHz). With telecom operators investing heavily in 5G infrastructure, the market for attenuators capable of handling these frequencies is projected to grow at 6.2% CAGR through 2032. Modern attenuators now incorporate advanced materials like beryllium oxide and aluminum nitride to maintain signal integrity while dissipating heat efficiently in compact 5G base station designs. Furthermore, the development of Surface Mount Technology (SMT) attenuators that enable automated PCB assembly is reducing manufacturing costs by approximately 15-20% compared to traditional threaded connector models.

Other Trends

Military Modernization Programs

Defense applications now account for nearly 30% of the global RF attenuator market revenue as nations upgrade radar systems and electronic warfare capabilities. The U.S. Department of Defense’s FY2024 budget allocates $12 billion for C4ISR systems that extensively utilize ruggedized coaxial attenuators. Manufacturers are responding with mil-spec products featuring extended temperature ranges (-55°C to 125°C) and improved VSWR characteristics below 1.5:1 across multi-octave bandwidths. This military-driven innovation is spilling over into commercial aerospace applications, particularly in satellite communication payloads where signal conditioning is critical.

Miniaturization and Integration Reshaping Product Development

The industry trend toward compact, integrated RF subsystems is compelling attenuator manufacturers to develop chip-scale packages and embedded solutions. Leading suppliers now offer attenuator ICs measuring just 2×2 mm that combine multiple attenuation values in a single package. This miniaturization supports the Internet of Things (IoT) revolution, where space-constrained devices require precise RF power management. The automotive sector is witnessing particular growth, with radar-based ADAS systems using micro-attenuators to calibrate 77 GHz frequencies. Recent product launches indicate average size reductions of 40% compared to 2020 form factors while maintaining insertion loss below 0.5 dB across operating bands.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Strategic Expansions Drive Market Competition

The global RF coaxial attenuators market features a dynamic competitive landscape dominated by established players and emerging manufacturers. Infinite Electronics leads the market with its extensive product portfolio and strong foothold in North America and Europe. The company specializes in high-performance fixed and variable attenuators, catering to critical applications in aerospace, defense, and telecommunications sectors.

Huber+Suhner and Radiall follow closely, leveraging their expertise in precision RF components and global distribution networks. These companies have been actively expanding their production capacities to meet growing demand, particularly in Asia-Pacific where 5G deployment and military modernization programs are accelerating market growth.

Meanwhile, SHF Communication Technologies has gained significant traction through its innovative product designs capable of handling ultra-high frequencies up to 40 GHz. Their recent partnership with a leading European defense contractor demonstrates how strategic collaborations are shaping the competitive environment.

Regionally, Shenzhen RF ONE and Qiyuan Microwave Technology are emerging as formidable players in the Asian market, offering cost-effective solutions without compromising on technical specifications. Their ability to combine competitive pricing with reliable performance makes them preferred suppliers for mid-range applications.

List of Key RF Coaxial Attenuator Manufacturers

- Infinite Electronics (U.S.)

- Huber+Suhner (Switzerland)

- Radiall (France)

- SHF Communication Technologies (Germany)

- Narda-Miteq (U.S.)

- SV Microwave (U.S.)

- Molex (U.S.)

- Hirose Electric (Japan)

- RF Lambda (Taiwan)

- Shenzhen RF ONE (China)

- Qiyuan Microwave Technology (China)

- Keysight Technologies (U.S.)

- Mini-Circuits (U.S.)

- Qorvo (U.S.)

- Marki Microwave (U.S.)

The market continues to witness strategic movements including mergers, acquisitions, and R&D investments as companies position themselves for the projected 4.9% CAGR growth through 2032. With increasing demand from both commercial and defense sectors, manufacturers are focusing on developing ruggedized attenuators capable of withstanding extreme environmental conditions while maintaining signal integrity.

Segment Analysis:

By Type

Fixed Attenuator Segment Leads Due to High Stability and Cost-Effectiveness

The market is segmented based on type into:

- Fixed Attenuator

- Subtypes: Surface Mount, Connectorized, and others

- Variable Attenuator

- Subtypes: Step Attenuator, Continuously Variable, and others

By Application

Communication Segment Dominates with Increasing Demand for High-Frequency Signal Management

The market is segmented based on application into:

- Communication

- Subtypes: 5G Networks, Satellite Communication, and others

- Aerospace

- National Defense

- Others

By Frequency Range

High-Frequency Segment Expands with Advanced RF Communication Systems

The market is segmented based on frequency range into:

- Low Frequency (DC-1 GHz)

- Medium Frequency (1-20 GHz)

- High Frequency (Above 20 GHz)

By End-User Industry

Telecommunications Sector Holds Major Share Due to Broadband Expansion

The market is segmented based on end-user industry into:

- Telecommunications

- Military & Defense

- Aerospace & Aviation

- Others

Regional Analysis: RF Coaxial Attenuators Market

North America

The North American RF coaxial attenuators market is driven by advanced telecommunications infrastructure, military modernization programs, and increasing satellite communication demands. The U.S. accounts for the largest share due to extensive 5G deployments, with telecom operators investing over $30 billion annually in network upgrades. Fixed attenuators dominate applications in aerospace & defense, where precision signal control is critical for radar and electronic warfare systems. However, supply chain disruptions and trade restrictions on specialized components remain key challenges. Leading manufacturers like Infinite Electronics and Narda-Miteq focus on high-frequency attenuators (up to 40 GHz) for next-gen applications.

Asia-Pacific

This region exhibits the highest growth rate, propelled by China’s 5G expansion and India’s defense electronics sector. China consumes over 35% of global RF components, with domestic players like Shenzhen RF ONE capturing market share through cost-competitive solutions. While fixed attenuators lead in volume due to mass production for consumer electronics, variable attenuators gain traction in R&D labs and aerospace testing. Japan and South Korea contribute significantly through innovations in millimeter-wave attenuators for automotive radar and IoT devices. However, intellectual property concerns and uneven quality standards hinder full market potential.

Europe

Stringent EU regulations on electromagnetic compatibility (EMC Directive 2014/30/EU) shape product development, with firms like Huber+Suhner and Radiall emphasizing low-noise, high-isolation attenuators. The automotive sector drives demand for ruggedized attenuators in vehicle-to-everything (V2X) communication, while aerospace applications prioritize ultra-wideband designs. Germany leads in industrial RF solutions, though Brexit-induced trade complexities affect U.K. supply chains. The region sees increasing mergers, such as Molex’s acquisition of Radio Frequency Systems, to strengthen technological capabilities.

Middle East & Africa

Market growth stems from oil & gas sector investments in wireless monitoring systems and government initiatives for telecom infrastructure. The UAE and Saudi Arabia are key adopters of military-grade attenuators for surveillance and satellite applications. Limited local manufacturing results in heavy imports, primarily from Europe and North America. While 5G rollouts present opportunities, political instability in certain areas delays large-scale projects. Vendors focus on providing EMI/RFI-shielded attenuators for harsh desert environments.

South America

Brazil and Argentina show moderate growth, driven by broadcast equipment upgrades and expanding mobile networks. Economic volatility leads to preference for refurbished or lower-cost attenuators, particularly in the commercial sector. The lack of indigenous component manufacturers creates reliance on Chinese and U.S. suppliers. Notably, defense modernization programs in Chile and Colombia are fostering niche demand for high-power RF attenuators in electronic countermeasure systems.

Report Scope

This market research report provides a comprehensive analysis of the Global RF Coaxial Attenuators Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 416 million in 2024 and is projected to reach USD 578 million by 2032 at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (Fixed Attenuator, Variable Attenuator), application (Communication, Aerospace, National Defense, Others), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Infinite Electronics, SHF Communication Technologies, Huber+Suhner, Radiall, and Narda-Miteq, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging RF technologies, miniaturization trends, and advancements in signal attenuation solutions.

- Market Drivers & Restraints: Evaluation of factors such as increasing 5G deployment, defense spending, and space applications driving growth, along with challenges like supply chain constraints and material costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, system integrators, telecom providers, and defense contractors operating in this space.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Coaxial Attenuators Market?

-> RF Coaxial Attenuators Market was valued at 416 million in 2024 and is projected to reach US$ 578 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global RF Coaxial Attenuators Market?

-> Key players include Infinite Electronics, SHF Communication Technologies, Huber+Suhner, Radiall, Narda-Miteq, SV Microwave, and MECA Electronics, among others.

What are the key growth drivers?

-> Primary growth drivers include 5G network expansion, increasing defense electronics spending, and growth in satellite communication systems.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include development of ultra-wideband attenuators, integration of MEMS technology, and demand for compact, high-frequency solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...