MARKET INSIGHTS

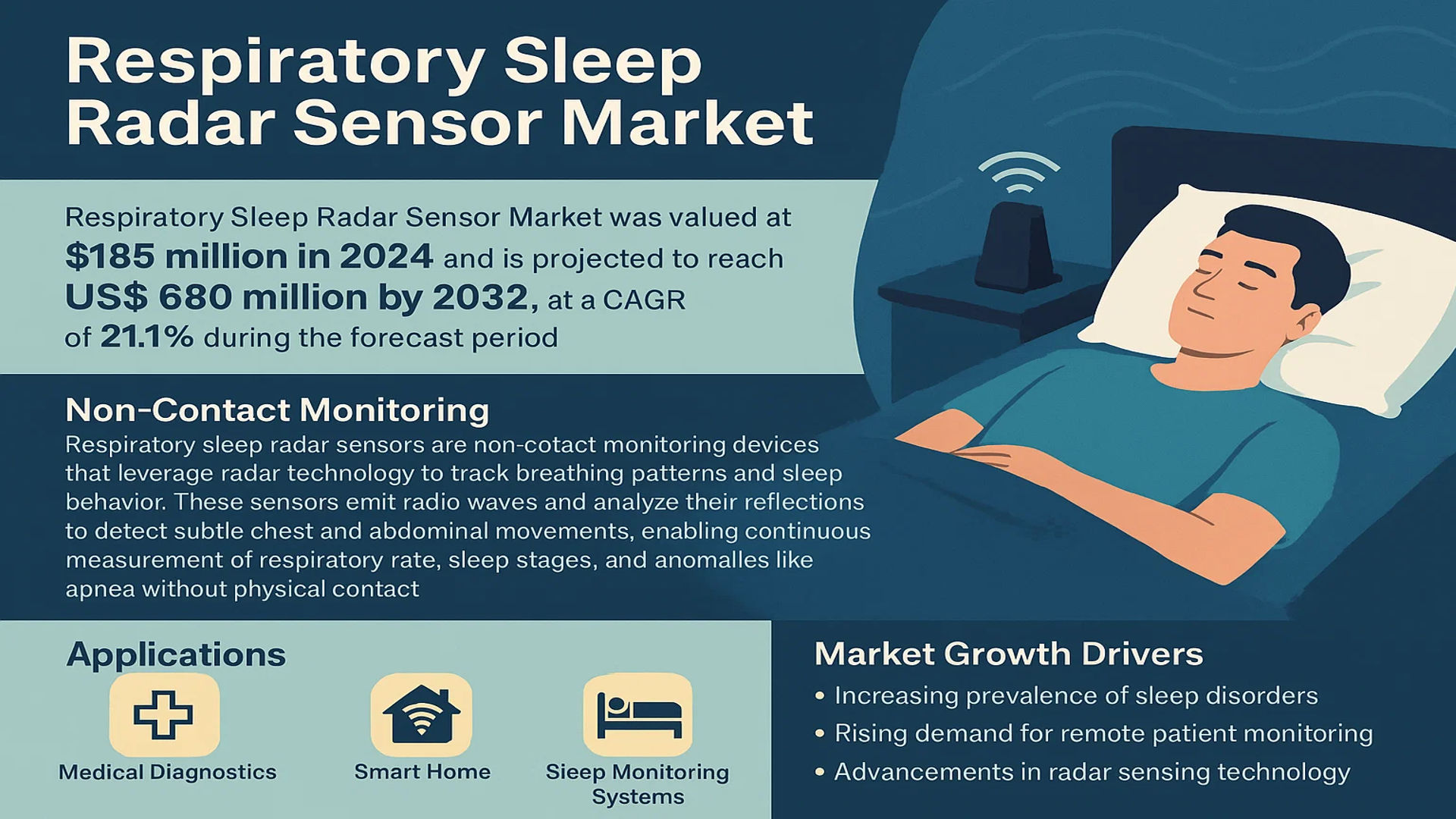

The global Respiratory Sleep Radar Sensor Market was valued at 185 million in 2024 and is projected to reach US$ 680 million by 2032, at a CAGR of 21.1% during the forecast period.

Respiratory sleep radar sensors are non-contact monitoring devices that leverage radar technology to track breathing patterns and sleep behavior. These sensors emit radio waves and analyze their reflections to detect subtle chest and abdominal movements, enabling continuous measurement of respiratory rate, sleep stages, and anomalies like apnea without physical contact. They are widely adopted in medical diagnostics, smart home applications, and sleep monitoring systems due to their unobtrusive nature and high accuracy.

The market growth is driven by increasing prevalence of sleep disorders, rising demand for remote patient monitoring, and advancements in radar sensing technology. Furthermore, growing adoption of smart home devices and IoT-enabled healthcare solutions is accelerating market expansion. Key players such as Infineon, Texas Instruments, and Analog Devices dominate the market with innovative product offerings and strategic partnerships. For instance, in 2023, Infineon expanded its radar sensor portfolio with enhanced sleep tracking capabilities to cater to the rising demand in healthcare applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Sleep Disorders to Accelerate Market Adoption

The global surge in sleep-related disorders, including sleep apnea and insomnia, is propelling demand for advanced monitoring technologies like respiratory sleep radar sensors. Recent studies indicate that over 1 billion people worldwide suffer from obstructive sleep apnea, with prevalence rates increasing by 25-30% in developed nations over the past decade. This alarming rise is directly correlated with aging populations and increasing obesity rates, creating substantial demand for non-contact sleep monitoring solutions. Radar-based systems offer significant advantages over traditional polysomnography by eliminating uncomfortable sensors while maintaining clinical-grade accuracy. Their ability to detect subtle respiratory patterns without physical contact makes them ideal for long-term home monitoring.

Integration with Smart Home Ecosystems Drives Consumer Adoption

The rapid evolution of smart home technologies has created new application avenues for respiratory sleep radar sensors. Major IoT platforms are actively incorporating health monitoring capabilities into their ecosystems, with sleep tracking emerging as a premium feature. Market analysis shows a 40% year-over-year growth in health-focused smart home devices, with sleep monitoring representing the fastest-growing segment. Leading manufacturers are embedding 60GHz radar sensors into bedside devices and wall panels to provide seamless sleep tracking without wearable discomfort. This convergence of healthcare and home automation is expected to drive the consumer segment to account for over 35% of total market revenue by 2027.

Technological Advancements in Radar Sensing Enhance Market Potential

Breakthroughs in millimeter-wave radar technology are transforming the respiratory sleep monitoring landscape. Next-generation sensors now achieve sub-millimeter movement detection at lower power consumption, enabling continuous monitoring with minimal energy impact. The transition from 24GHz to 60GHz solutions has improved resolution by 400% while reducing interference. Recent innovations in AI-powered signal processing allow these systems to distinguish between multiple sleep phases with 92-95% accuracy compared to clinical standards. Major semiconductor players are developing specialized radar SoCs that integrate signal processing algorithms, further miniaturizing devices and reducing production costs by up to 30%.

MARKET RESTRAINTS

Regulatory Complexity Limits Rapid Market Expansion

The medical device classification of sleep monitoring technologies presents significant regulatory hurdles for market entrants. In major markets, respiratory sleep radar sensors intended for diagnostic use must undergo rigorous FDA or CE approval processes that average 12-18 months. Post-market surveillance requirements add substantial compliance costs, with manufacturers reporting 15-20% of total R&D expenditure allocated to regulatory affairs. These barriers disproportionately affect smaller innovators, potentially stifling competition and technological diversity in the market. While home-use products face lighter regulations, any claims related to medical data interpretation immediately trigger stringent oversight.

Other Restraints

Intermittent Accuracy Issues

Despite technological advancements, radar sensors still demonstrate variability in detecting sleep events compared to gold-standard polysomnography. Clinical validations show accuracy rates drop by 5-8% for patients with irregular breathing patterns or who sleep in non-standard positions. This performance gap limits adoption in critical care settings where precision is paramount.

Market Education Barriers

The novel nature of radar-based sleep monitoring creates significant consumer education challenges. Surveys indicate 68% of potential users misunderstand the technology’s capabilities, with many expecting hospital-grade diagnostics from simple bedside devices. This knowledge gap slows market penetration rates despite the technology’s inherent advantages.

MARKET OPPORTUNITIES

Integration with Telehealth Platforms Presents Untapped Potential

The global telehealth market expansion is creating synergistic opportunities for respiratory sleep radar sensor providers. Healthcare systems increasingly seek remote patient monitoring solutions that integrate seamlessly with virtual care platforms. Early adopters report 40% reductions in sleep clinic visits when combining radar-based home monitoring with telehealth consultations. This model is particularly promising for managing chronic conditions, where continuous respiratory data can trigger timely clinical interventions. Leading sensor manufacturers are forming strategic partnerships with telehealth providers to develop turnkey solutions, with several major deals announced in the past year.

Emerging Asian Markets Offer High-Growth Potential

Developing economies in Asia present significant expansion opportunities due to improving healthcare infrastructure and rising health awareness. Countries like China and India are experiencing particularly strong demand, with their respective sleep diagnostic markets growing at 28% and 34% annually. Local manufacturers are leveraging lower production costs to develop affordable radar sensor solutions tailored to regional needs. Government initiatives supporting digital health innovation further accelerate adoption, with several Asian nations offering subsidies for home-based medical monitoring devices.

Advancements in Predictive Analytics Create New Value Propositions

The integration of sophisticated machine learning algorithms is transforming passive sleep monitoring into proactive health management. Next-generation systems can now analyze longitudinal respiratory data to predict potential health events with 85-90% accuracy up to 72 hours in advance. This predictive capability opens opportunities in preventive healthcare and wellness programs. Insurers and employers are showing increasing interest in these solutions, with pilot programs demonstrating significant reductions in health-related costs when implementing early intervention strategies based on predictive analytics.

MARKET CHALLENGES

Data Privacy Concerns Impede Consumer Trust

The sensitive nature of health data collected by sleep radar sensors creates significant privacy challenges. Recent surveys indicate 62% of potential users cite privacy concerns as their primary barrier to adoption, despite manufacturers implementing robust encryption protocols. Regulatory frameworks like GDPR impose strict requirements on health data handling, increasing compliance complexity for global players. High-profile data breaches in IoT devices have heightened consumer skepticism, requiring manufacturers to invest heavily in cybersecurity measures that add 15-20% to product development costs.

Other Challenges

Interoperability Limitations

The lack of standardized data formats across different manufacturers creates ecosystem fragmentation. Healthcare providers report frustration when trying to integrate respiratory data from various sources into electronic health records, with compatibility issues affecting 30-35% of attempted integrations. This challenge is particularly acute in multi-vendor hospital environments.

Battery Life Constraints

While radar sensors are more energy-efficient than many alternatives, continuous monitoring still presents power management challenges. Consumer expectations for weekly or monthly charging cycles conflict with the technical requirements of high-frequency radar operation. This trade-off between performance and convenience remains a key engineering challenge for product designers.

RESPIRATORY SLEEP RADAR SENSOR MARKET TRENDS

Non-Contact Health Monitoring Gains Traction Due to Patient Comfort and Accuracy

The increasing demand for non-contact health monitoring solutions is significantly boosting the adoption of respiratory sleep radar sensors. These devices offer seamless tracking of respiration patterns and sleep quality without requiring physical contact, making them ideal for long-term monitoring. Unlike traditional polysomnography, which uses cumbersome electrodes, radar-based sensors provide high-precision measurements while maintaining user comfort. Hospitals and sleep clinics are increasingly integrating these sensors into patient monitoring systems, with 60 GHz radar technology emerging as the preferred choice due to its superior resolution in detecting subtle chest movements. This shift toward contactless diagnostics is expected to drive market growth by over 20% CAGR in the next five years.

Other Trends

Integration with Smart Home Ecosystems

Respiratory sleep radar sensors are finding extensive applications in smart home environments, where they complement wellness-focused IoT devices. Leading manufacturers are embedding these sensors into smart beds, mattresses, and bedside monitors to provide sleep analytics. The growing consumer preference for connected health solutions has further accelerated this trend, with estimates suggesting that over 30% of smart home health devices will incorporate radar-based sleep monitoring by 2026. Additionally, partnerships between medical device companies and tech firms are enhancing interoperability, enabling seamless data synchronization between home systems and healthcare providers.

Rising Prevalence of Sleep Disorders Spurs Technological Innovation

The global surge in sleep-related conditions, including obstructive sleep apnea (OSA) and insomnia, is fueling advancements in respiratory sleep radar sensor technology. With nearly 1 billion people worldwide suffering from OSA, healthcare providers are prioritizing early diagnosis through non-invasive methods. Sensor manufacturers are responding by developing AI-powered algorithms capable of distinguishing between normal and pathological breathing patterns with over 95% accuracy. Furthermore, recent regulatory approvals for radar-based diagnostic tools in key markets are encouraging clinical adoption. These innovations are particularly impactful in elderly care, where continuous respiration monitoring can prevent critical health episodes while preserving patient dignity.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Technological Capabilities to Secure Competitive Edge

The global respiratory sleep radar sensor market features a dynamic competitive environment, with established semiconductor giants competing alongside specialized sensor manufacturers and emerging smart home technology providers. Infineon Technologies has emerged as a dominant force, leveraging its expertise in radar-based sensing solutions and strong partnerships with medical device manufacturers. Their 60 GHz radar chipsets are widely adopted in clinical sleep monitoring applications.

Following closely, Texas Instruments and Analog Devices have made significant inroads with their ultra-precise 24 GHz radar ICs designed specifically for respiratory tracking. These companies benefit from decades of signal processing experience, enabling them to deliver superior motion detection accuracy required for sleep apnea diagnosis.

The competitive intensity has increased as Chinese technology firms like Huawei and HIKVISION aggressively expand into consumer health monitoring segments. Their strategy focuses on integrating sleep radar sensors into existing smart home ecosystems, creating seamless user experiences across multiple connected devices.

Meanwhile, specialist firms such as Seeed Technology and Shenzhen Ferry Smart are carving out niche positions through modular sensor designs that simplify integration for medical equipment manufacturers. Their rapid prototyping capabilities allow customized solutions for specific clinical applications.

List of Key Respiratory Sleep Radar Sensor Companies

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Analog Devices (U.S.)

- AxEnd (Israel)

- Huawei (China)

- HIKVISION (China)

- Seeed Technology (China)

- WHST (China)

- Shenzhen Ferry Smart (China)

- Uniview (China)

- Tsingray (China)

- Chuhang Tech (China)

- Microbrain Intelligent (China)

- Innopro (China)

- Aqara (China)

Segment Analysis:

By Type

24 GHz Segment Leads Due to High Adoption in Medical and Smart Home Applications

The market is segmented based on type into:

- 24 GHz

- 60 GHz

- Others

By Application

Medical Segment Dominates with Increasing Demand for Non-Invasive Sleep Monitoring Solutions

The market is segmented based on application into:

- Medical

- Home Use

- Others

By Technology

Continuous Wave Radar Technology Prevails Due to High Accuracy in Breathing Detection

The market is segmented based on technology into:

- Continuous Wave Radar

- Frequency Modulated Continuous Wave

- Ultra-Wideband Radar

By End User

Hospitals and Sleep Clinics Lead Market Share with Rising Cases of Sleep Disorders

The market is segmented based on end user into:

- Hospitals and Sleep Clinics

- Home Care Settings

- Research Institutions

Regional Analysis: Respiratory Sleep Radar Sensor Market

North America

North America dominates the global respiratory sleep radar sensor market, driven by advanced healthcare infrastructure, high awareness of sleep disorders, and strong adoption of smart home technologies. The U.S. accounts for the majority of regional demand, with major players like Texas Instruments and Analog Devices leading innovation. The growing prevalence of sleep apnea—affecting over 30 million Americans—and increasing investments in remote patient monitoring solutions are accelerating market growth. Regulatory support for non-contact medical devices and partnerships between tech firms and healthcare providers further strengthen the ecosystem. However, data privacy concerns and high product costs remain key challenges for widespread consumer adoption.

Europe

Europe represents the second-largest market, with Germany, the UK, and France as primary contributors. Strict medical device regulations under the EU MDR framework ensure high-quality standards, while government initiatives promoting digital health solutions fuel demand. The region shows strong preference for clinical-grade 60GHz radar sensors in hospital settings, though home-use devices are gaining traction among aging populations. Scandinavia leads in adoption rates due to high healthcare expenditure and tech-savvy demographics. Supply chain complexities and competition from Asian manufacturers pose challenges, but the focus on preventive healthcare continues to drive long-term prospects.

Asia-Pacific

As the fastest-growing region, Asia-Pacific’s expansion stems from rising healthcare expenditures, urbanization, and increasing sleep disorder diagnoses. China dominates production and consumption, with companies like Huawei and HIKVISION advancing radar sensor technology. India and Japan show promising growth due to expanding middle-class populations and smart home penetration. While price sensitivity favors 24GHz solutions, premium medical applications are gaining ground in developed markets. The lack of standardized regulations across countries creates fragmentation, but regional partnerships and local manufacturing initiatives are addressing these hurdles. Telemedicine expansion post-pandemic provides additional growth avenues.

South America

The South American market remains nascent but exhibits steady growth potential. Brazil leads regional adoption, driven by private healthcare investments and increasing awareness of sleep health. Economic volatility limits widespread deployment of high-end systems, making cost-effective solutions from Chinese manufacturers popular. Regulatory frameworks are still evolving, creating both opportunities for early movers and challenges regarding quality standards. Pilot programs integrating sleep sensors with public health initiatives in Chile and Argentina demonstrate the technology’s potential, though infrastructure limitations delay mass-market penetration.

Middle East & Africa

This emerging market shows divergent growth patterns, with Gulf nations like UAE and Saudi Arabia driving adoption through smart city projects and premium healthcare services. Government initiatives to diversify economies beyond oil are fueling tech investments, including in medical IoT devices. Africa faces significant barriers including limited healthcare access and low awareness, though South Africa and Kenya are witnessing early-stage deployments in private hospitals. The region’s hot climate poses unique technical challenges for radar sensor accuracy, prompting localized R&D efforts. While currently a small market, long-term growth looks promising as digital infrastructure improves.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Respiratory Sleep Radar Sensor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Respiratory Sleep Radar Sensor market was valued at USD 185 million in 2024 and is projected to reach USD 680 million by 2032, growing at a CAGR of 21.1%.

- Segmentation Analysis: Detailed breakdown by product type (24 GHz, 60 GHz, Others), application (Medical, Home Use, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key markets driving growth.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Infineon, Texas Instruments, Analog Devices, Huawei, and HIKVISION.

- Technology Trends & Innovation: Assessment of emerging radar sensing technologies, integration of AI/IoT in sleep monitoring, and advancements in non-contact respiratory tracking.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as rising sleep disorder prevalence and smart home adoption, along with challenges like regulatory hurdles and privacy concerns.

- Stakeholder Analysis: Insights for component suppliers, OEMs, healthcare providers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Respiratory Sleep Radar Sensor Market?

->Respiratory Sleep Radar Sensor Market was valued at 185 million in 2024 and is projected to reach US$ 680 million by 2032, at a CAGR of 21.1% during the forecast period.

Which key companies operate in Global Respiratory Sleep Radar Sensor Market?

-> Key players include Infineon, Texas Instruments, Analog Devices, Huawei, HIKVISION, Seeed Technology, WHST, and Shenzhen Ferry Smart, among others.

What are the key growth drivers?

-> Key growth drivers include rising prevalence of sleep disorders, increasing adoption of non-contact health monitoring solutions, and growing smart home applications.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include AI-powered sleep analysis, integration with smart home ecosystems, and development of multi-functional health monitoring devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...