MARKET INSIGHTS

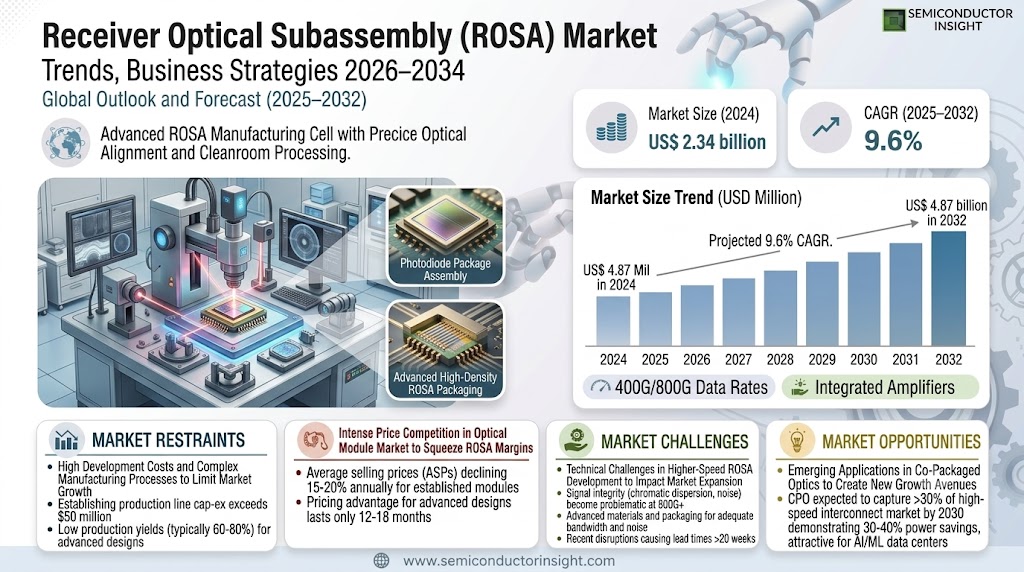

The global Receiver Optical Subassembly (ROSA) Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 4.87 billion by 2032, at a CAGR of 9.6% during the forecast period 2025-2032.

A Receiver Optical Subassembly (ROSA) is a critical component in fiber optic transceivers responsible for converting optical signals back to electrical signals. It consists of a photodiode, housing, and electrical interface, forming a key part of the optical communication chain. ROSAs are often paired with Transmitter Optical Subassemblies (TOSA) to create complete transceiver modules. The technology includes both APD (Avalanche Photodiode) and PIN photodiode variants, with APD ROSAs showing faster growth due to their superior sensitivity in high-speed applications.

The market growth is driven by escalating demand for high-speed data transmission, particularly in 5G infrastructure and data centers. While North America currently leads in market share, Asia-Pacific is experiencing the fastest growth due to expanding telecommunications networks. Recent developments include the introduction of compact ROSAs for 400G/800G optical modules by key players like Sumitomo Electric and MACOM. The competitive landscape remains intense, with the top five manufacturers holding approximately 45% of global market revenue in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Speed Data Transmission to Fuel ROSA Market Growth

The exponential growth in data traffic driven by 5G networks, cloud computing, and IoT applications is creating unprecedented demand for high-speed optical communication components like ROSAs. With global IP traffic projected to surpass 4.8 zettabytes annually by 2025, network operators are aggressively upgrading infrastructure to handle this load. ROSAs enable this transition by providing the critical photoelectric conversion capability in optical modules ranging from 10G to 800G speeds. The market for 100G and above optical modules using advanced ROSA components is experiencing particularly strong growth, exceeding 30% CAGR in recent years as hyperscale data centers expand globally.

Increasing Adoption of Cloud Services to Accelerate Market Expansion

Cloud service providers are driving significant investments in data center infrastructure, with cloud data center traffic expected to account for over 95% of total data center traffic by 2025. This rapid cloud migration is creating substantial demand for high-performance optical transceivers incorporating advanced ROSA technology. Major cloud providers are transitioning to 400G optical modules in their data centers, with deployments expected to grow at nearly 50% CAGR through 2030. The ROSA market benefits directly from this shift as each optical module requires precisely engineered receiver subassemblies to maintain signal integrity at higher data rates.

Technological Advancements in Photodiode Design to Enhance Market Potential

Recent innovations in avalanche photodiode (APD) and PIN photodiode technologies are significantly improving the performance characteristics of ROSA components. Advanced APD-ROSA designs now offer enhanced sensitivity (>-22 dBm for 25G applications) and lower noise figures, enabling longer reach in optical networks. These improvements are particularly crucial for emerging applications in fiber-to-the-home (FTTH) and 5G fronthaul/backhaul networks where receiver performance directly impacts network quality. Manufacturers are also achieving cost reductions through wafer-level packaging techniques and automated assembly processes, making high-performance ROSAs more accessible across various market segments.

MARKET RESTRAINTS

High Development Costs and Complex Manufacturing Processes to Limit Market Growth

The specialized nature of ROSA manufacturing presents significant barriers to market expansion. Developing and producing high-performance photodiode packages with precise optical alignment requires expensive cleanroom facilities and highly specialized equipment. The capital expenditure for establishing a production line capable of manufacturing ROSAs at competitive yields often exceeds $50 million, creating high barriers to entry. Additionally, the complex assembly process involving sub-micron alignment tolerances leads to relatively low production yields (typically 60-80%) for advanced designs, further increasing unit costs.

Intense Price Competition in Optical Module Market to Squeeze ROSA Margins

The optical transceiver market has become increasingly commoditized, with average selling prices declining approximately 15-20% annually for established form factors. This pricing pressure cascades to ROSA suppliers as module manufacturers demand consistent cost reductions from component vendors. While advanced ROSA designs for 400G and 800G applications currently command premium pricing, this advantage typically lasts only 12-18 months before significant price erosion begins. This dynamic makes it challenging for manufacturers to recoup R&D investments and maintain profitability over product lifecycles.

MARKET CHALLENGES

Technical Challenges in Higher-Speed ROSA Development to Impact Market Expansion

As data rates increase beyond 400G, ROSA designers face mounting technical challenges in maintaining signal integrity and receiver sensitivity. At 800G and 1.6T data rates, signal degradation from chromatic dispersion, polarization mode dispersion, and photon-electron conversion noise become increasingly problematic. Achieving adequate bandwidth in the photodiode and amplifier components while maintaining acceptable noise figures requires advanced materials and innovative packaging approaches. These technical hurdles have delayed the commercialization of some next-generation ROSA designs by 6-12 months beyond original projections, potentially slowing overall market growth.

Other Challenges

Supply Chain Vulnerabilities

The ROSA market faces ongoing supply chain risks, particularly for specialized semiconductors and optical components. Many critical materials and subcomponents come from limited sources, creating potential bottlenecks during periods of strong demand. Recent disruptions have caused lead times for certain ROSA variants to extend beyond 20 weeks, forcing module manufacturers to redesign products for available components.

Thermal Management Issues

Higher-power optical modules generate substantial heat that can degrade ROSA performance. Managing thermal loads while maintaining compact form factors requires innovative packaging solutions, often adding cost and complexity. This challenge grows more acute as data rates increase and module power budgets tighten.

MARKET OPPORTUNITIES

Emerging Applications in Co-Packaged Optics to Create New Growth Avenues

The development of co-packaged optics (CPO) architectures presents significant opportunities for ROSA technology providers. CPO solutions, which integrate optical engines directly with switching ASICs, are expected to capture over 30% of the high-speed interconnect market by 2030. This emerging application requires innovative ROSA designs that can operate in close proximity to high-power processors while maintaining signal integrity. Early CPO implementations are demonstrating 30-40% power savings compared to traditional pluggable modules, making them particularly attractive for next-generation AI/ML data centers. ROSA suppliers that can deliver thermally efficient, high-density solutions stand to gain substantial market share in this rapidly developing segment.

Expansion of Silicon Photonics to Offer Integration Opportunities

Silicon photonics technology is reshaping optical component markets by enabling higher levels of integration at lower costs. ROSA functionality is increasingly being incorporated into silicon photonic integrated circuits, offering potential size and performance advantages. This convergence creates opportunities for manufacturers to develop hybrid solutions that combine the best attributes of traditional ROSA designs with silicon photonics technology. The market for silicon photonic-based optical components is projected to grow at over 25% CAGR through 2030, representing a significant expansion opportunity for innovative ROSA providers.

Growing Demand for Optical Sensing Applications to Open New Markets

Beyond communications, ROSA technology is finding new applications in lidar systems, medical imaging, and industrial sensing. The automotive lidar market alone is expected to require millions of high-performance optical receivers annually as autonomous vehicle technology matures. These applications often demand different performance characteristics than telecom ROSAs – notably higher sensitivity and wider dynamic ranges – creating opportunities for product diversification. Companies able to adapt their receiver technologies for these emerging applications can access growth markets less susceptible to the pricing pressures of the telecom sector.

RECEIVER OPTICAL SUBASSEMBLY (ROSA) MARKET TRENDS

Increasing Demand for High-Speed Data Transmission Driving ROSA Adoption

The global ROSA market is experiencing robust growth, primarily fueled by the exponential rise in data traffic and the need for faster optical communication networks. With the global market projected to reach millions of USD by 2032 at a significant CAGR, ROSAs are becoming indispensable in modern fiber optic systems. The transition toward 100G and 400G optical modules across data centers and telecom networks has accelerated adoption, with APD ROSAs alone expected to capture a substantial market share due to their superior sensitivity in high-speed applications. Furthermore, advancements in photodiode technology have enhanced signal reception efficiency, making ROSAs more reliable for next-generation optical modules.

Other Trends

5G Network Deployment Accelerating Market Growth

The rapid rollout of 5G infrastructure worldwide is significantly boosting ROSA demand, particularly for 25G and 100G optical modules required in fronthaul and midhaul networks. Telecom operators are investing heavily in fiber optic backbones to support 5G’s low-latency requirements, creating a surge in ROSA procurement. Countries like China, the U.S., and Japan are leading this expansion, with estimations suggesting that 5G-related optical module shipments will grow at a double-digit CAGR over the next five years. This trend is further complemented by innovations in compact ROSA designs that meet the stringent power and space constraints of 5G base stations.

Competitive Landscape and Regional Market Dynamics

The ROSA market features intense competition among key players such as WOORIRO, Semtech, and Mitsubishi Electric, who collectively hold a notable share of the global revenue. Regional dynamics show Asia-Pacific, particularly China, emerging as the fastest-growing market due to localized manufacturing and government initiatives supporting optical communication infrastructure. Meanwhile, North America maintains strong demand driven by hyperscale data center expansions, with major tech companies investing billions annually in network upgrades. Strategic partnerships between ROSA manufacturers and optical module developers are becoming increasingly common, aiming to optimize performance for specific applications like cloud computing and AI-driven data centers.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in ROSA Segment

The global Receiver Optical Subassembly (ROSA) market features a competitive ecosystem with both established industry giants and agile regional competitors striving for technological dominance. With demand for high-speed optical communication surging, companies are aggressively investing in product differentiation and supply chain optimization.

SUMITOMO ELECTRIC and Mitsubishi Electric currently lead the market with their vertically integrated manufacturing capabilities. These Japanese conglomerates hold approximately 28% combined market share in 2024, benefiting from long-standing relationships with telecom equipment manufacturers and Tier-1 hyperscale data center operators.

Meanwhile, South Korea’s WOORIRO has emerged as a disruptive force, specializing in cost-effective ROSA solutions for 100G-and-above optical modules. Their patented photodiode packaging technology granted in Q3 2023 gives them significant leverage in price-sensitive Asian markets, particularly in China’s booming 5G infrastructure projects.

North American players face stiffer competition, but MACOM and Semtech maintain strong positions through strategic acquisitions. MACOM’s 2022 purchase of a leading indium phosphide chip designer directly enhanced their ROSA performance metrics, while Semtech’s recent partnership with a major cloud service provider ensures stable demand for their avalanche photodiode (APD) based receivers.

List of Key Receiver Optical Subassembly (ROSA) Manufacturers

- WOORIRO (South Korea)

- NTT Electronics Corporation (Japan)

- Semtech (U.S.)

- Mitsubishi Electric (Japan)

- SUMITOMO ELECTRIC (Japan)

- MACOM (U.S.)

- Advanced Photonix (U.S.)

- Vitex LLC (U.S.)

- Wuhan Yusheng Optoelectronic (China)

- Hangzhou XY Technology (China)

- XTRONIX (China)

- Optoplex Corporation (U.S.)

- Eoptolink (China)

- HUBER+SUHNER (Switzerland)

- Broadex Technologies (China)

Segment Analysis:

By Type

APD ROSA Segment Leads Due to High-Sensitivity Applications in Data Centers and Telecommunications

The market is segmented based on type into:

- APD ROSA (Avalanche Photodiode ROSA)

- PIN ROSA (Positive-Intrinsic-Negative Photodiode ROSA)

- Others

By Application

100G Optical Module Segment Dominates Owing to Rising Demand for High-Speed Data Transmission

The market is segmented based on application into:

- 10G Optical Module

- 25G Optical Module

- 100G Optical Module

- Other Optical Modules

By End-User

Telecommunications Sector Holds Majority Share Due to Expanding 5G Infrastructure

The market is segmented based on end-user into:

- Telecommunications

- Data Centers

- Enterprise Networks

- Others

Regional Analysis: Receiver Optical Subassembly (ROSA) Market

North America

The North American ROSA market is driven by advanced telecommunications infrastructure and increasing demand for high-speed data transmission in data centers. The U.S. dominates regional demand, with APD ROSA adoption growing at a strong CAGR due to 5G network expansions and cloud computing needs. However, strict regulatory compliance and higher component costs pose challenges for manufacturers. Partnerships between semiconductor firms and telecom providers are accelerating innovations in 100G/400G optical modules, particularly for hyperscale data centers. Canada and Mexico exhibit steady growth, supported by cross-border fiber optic network projects but lag behind U.S. technological adoption rates.

Europe

European ROSA demand stems from robust investments in fiber-to-the-home (FTTH) deployments and industrial automation. Germany and France lead in precision optical components, with stringent EU quality standards pushing manufacturers toward low-noise, high-sensitivity ROSA designs. The region shows strong preference for PIN ROSA in medium-speed applications (10G-25G), while APD variants gain traction in long-haul communications. Brexit-induced supply chain disruptions have prompted local sourcing strategies, with Eastern European facilities emerging as cost-effective production hubs. Environmental regulations on electronic waste also influence ROSA material selection and recycling processes.

Asia-Pacific

As the largest and fastest-growing ROSA market, Asia-Pacific benefits from China’s dominance in optical component manufacturing and India’s expanding telecom infrastructure. Chinese suppliers like Wuhan Yipeng and Eoptolink control ~35% of global ROSA production capacity, leveraging vertical integration. Japan and South Korea focus on high-end APD ROSAs for submarine cable systems, while Southeast Asian nations prioritize cost-effective PIN ROSAs for consumer-grade optics. The region faces pricing pressures due to intense competition, but government initiatives like India’s National Digital Communications Policy fuel sustained demand. Taiwan plays a critical role in bridging supply chains amid U.S.-China trade tensions.

South America

Market growth here is constrained by limited local manufacturing and reliance on imports from Asia. Brazil accounts for over 50% of regional ROSA consumption, driven by mobile network upgrades and smart city projects. Economic instability in Argentina and Venezuela hinders consistent investment in optical networks. While 10G ROSAs dominate current deployments, upcoming data center projects in Chile and Colombia are expected to boost demand for 25G+ modules. The lack of component standardization and skilled labor remains a bottleneck for technical support and maintenance services.

Middle East & Africa

Gulf Cooperation Council (GCC) nations lead ROSA adoption through mega-projects like Saudi Arabia’s NEOM smart city and UAE’s 5G rollouts. Israel’s thriving tech ecosystem fosters niche applications in military and medical optics. However, Africa’s market remains underpenetrated due to inadequate fiber backbones, though initiatives like Google’s Equiano cable project signal long-term potential. Price sensitivity favors Chinese suppliers, while European and American brands target high-margin oil/gas sector applications. Political instability and foreign exchange volatility create procurement challenges for telecom operators across the region.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Receiver Optical Subassembly (ROSA) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the fiber optic communication industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global ROSA market is projected to grow at a CAGR of 9.6 % from 2024 to 2032.

- Segmentation Analysis: Detailed breakdown by product type (APD ROSA, PIN ROSA), application (10G/25G/100G optical modules), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with China and U.S. as key markets.

- Competitive Landscape: Profiles of 25+ leading manufacturers including WOORIRO, NTT Electronics, Mitsubishi Electric, and SUMITOMO ELECTRIC, with their market share analysis.

- Technology Trends & Innovation: Assessment of emerging technologies in photodiode sensitivity, packaging techniques, and integration with advanced optical modules.

- Market Drivers & Restraints: Evaluation of 5G deployment, data center expansion, fiber optic network upgrades, alongside supply chain challenges and component shortages.

- Stakeholder Analysis: Strategic insights for optical component suppliers, transceiver manufacturers, telecom operators, and investors in the photonics ecosystem.

The research employs primary interviews with industry leaders and analysis of 50+ verified data sources to ensure accuracy and reliability of market projections and trends.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Receiver Optical Subassembly (ROSA) Market?

-> Receiver Optical Subassembly (ROSA) Market size was valued at US$ 2.34 billion in 2024 and is projected to reach US$ 4.87 billion by 2032, at a CAGR of 9.6% during the forecast period 2025-2032.

Which key companies operate in Global ROSA Market?

-> Key players include WOORIRO, NTT Electronics, Mitsubishi Electric, SUMITOMO ELECTRIC, Macom, and Advanced Photonix, collectively holding % market share.

What are the key growth drivers?

-> Growth is driven by 5G infrastructure rollout, hyperscale data center demand, and increasing adoption of high-speed optical communication networks.

Which region dominates the market?

-> Asia-Pacific leads in both production and consumption, with China accounting for % of global ROSA demand.

What are the emerging trends?

-> Emerging trends include miniaturization of components, higher integration with DSP chips, and development of 400G/800G compatible ROSAs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...