MARKET INSIGHTS

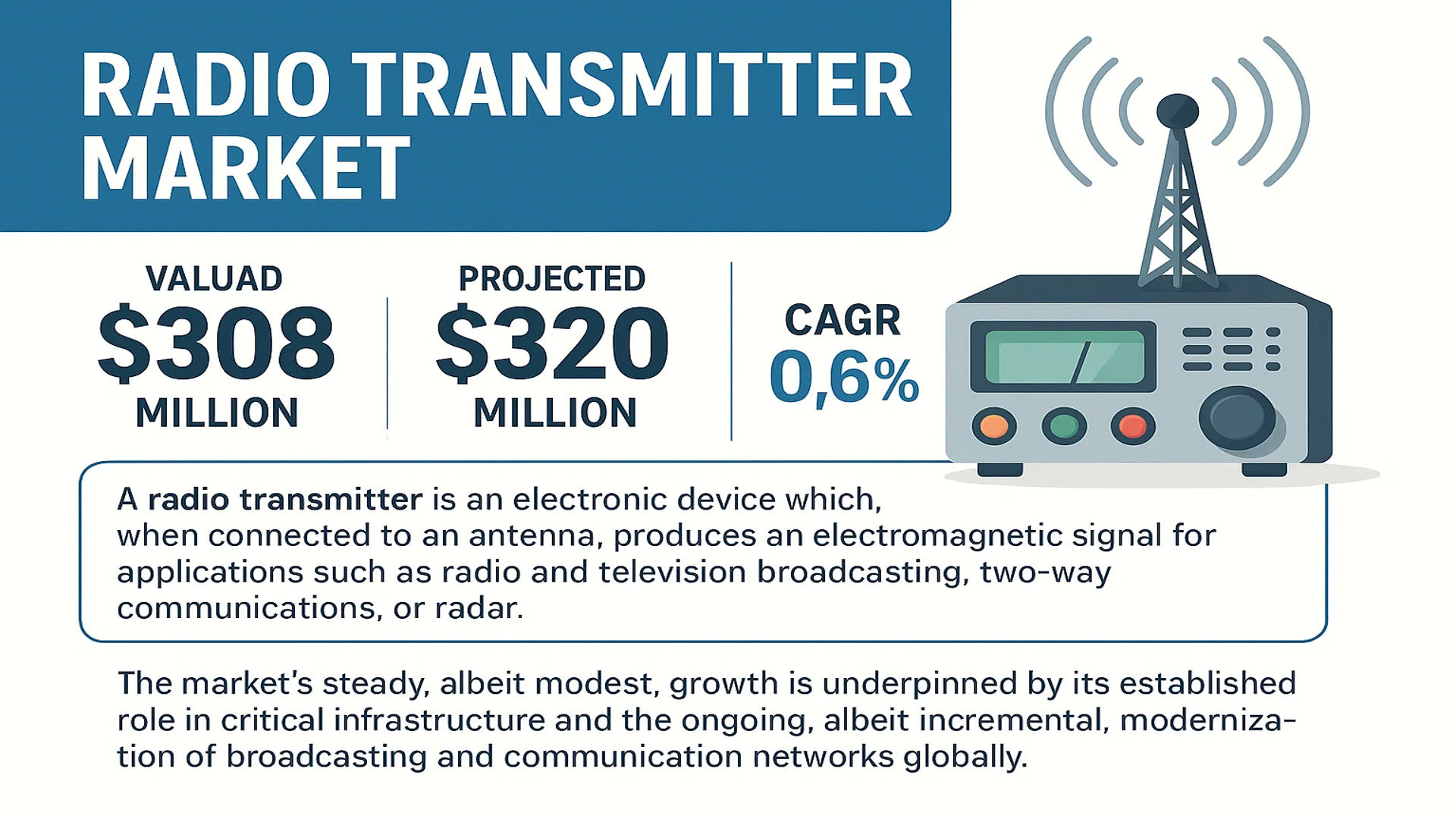

The global Radio Transmitter Market was valued at 308 million in 2024 and is projected to reach US$ 320 million by 2032, at a CAGR of 0.6% during the forecast period.

A radio transmitter is an electronic device which, when connected to an antenna, produces an electromagnetic signal for applications such as radio and television broadcasting, two-way communications, or radar. These devices are fundamental components of radio communication systems, using electromagnetic waves to transport information over a distance. It is important to note that while heating devices like microwave ovens share a similar design principle, they are not classified as transmitters because they utilize electromagnetic energy locally rather than transmitting it to a remote location.

The market’s steady, albeit modest, growth is underpinned by its established role in critical infrastructure and the ongoing, albeit incremental, modernization of broadcasting and communication networks globally. The Asia-Pacific region dominates the market, holding approximately 40% of the global share, largely due to extensive broadcasting infrastructure development and a large automotive manufacturing base. In terms of product segmentation, FM radio transmitters are the largest category, accounting for roughly 50% of the market. The automobile application segment is the largest end-user, representing over 45% of demand, driven by the integration of advanced communication systems in modern vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Digital Broadcasting Infrastructure to Drive Radio Transmitter Demand

The global transition from analog to digital broadcasting continues to be a primary driver for radio transmitter market growth. Digital radio broadcasting offers superior sound quality, more efficient spectrum utilization, and additional data services that analog systems cannot provide. Countries worldwide are implementing digital radio standards such as DAB+ (Digital Audio Broadcasting), HD Radio, and DRM (Digital Radio Mondiale), creating substantial demand for modern transmission equipment. The European Broadcasting Union reports that over 40 countries have implemented DAB/DAB+ services, with Norway completing its full FM network shutdown in 2017. This digital migration requires broadcasters to invest in new transmission systems capable of handling digital signals, driving replacement cycles and new installations. The superior coverage and efficiency of digital transmitters also enable broadcasters to reduce operational costs while improving service quality, creating a compelling business case for infrastructure upgrades.

Growing Automotive Integration and In-Vehicle Infotainment Systems to Boost Market Growth

The automotive sector’s increasing integration of advanced infotainment systems represents a significant growth driver for radio transmitters. Modern vehicles increasingly feature sophisticated entertainment systems that include multiple radio receivers alongside streaming services and connectivity features. The automobile application segment accounts for over 45% of the global radio transmitter market, driven by consumer demand for uninterrupted entertainment during commutes. Vehicle production volumes have been recovering post-pandemic, with global automotive output exceeding 85 million units annually. This substantial manufacturing base ensures consistent demand for radio transmission components integrated into vehicle entertainment systems. Furthermore, the development of autonomous vehicles is expected to maintain radio as a fundamental entertainment and information source, ensuring long-term demand stability in this critical application segment.

Emergency and Public Safety Communications Requirements to Fuel Market Expansion

Increasing focus on emergency broadcasting and public safety communications is driving demand for reliable radio transmission systems. Governments worldwide are strengthening their emergency alert systems following natural disasters and public safety incidents, recognizing radio’s crucial role in disseminating critical information. Radio transmitters form the backbone of these alert systems due to their widespread coverage and reliability compared to cellular networks that can become overloaded during emergencies. Many countries have mandated emergency alert capabilities for broadcasters, requiring transmitter upgrades to support digital emergency warning functionality. This regulatory push, combined with increasing climate-related disasters and security concerns, has created sustained demand for robust transmission infrastructure capable of delivering emergency messages reliably to the population.

MARKET RESTRAINTS

Rising Competition from Streaming Services and Digital Media to Constrain Market Growth

The radio transmitter market faces significant pressure from the rapid growth of digital streaming services and alternative media platforms. Audio streaming services have experienced explosive growth, with millions of users shifting from traditional broadcast radio to on-demand and internet-based audio content. This transition reduces the audience share for conventional radio broadcasting, potentially limiting new investments in transmission infrastructure. While radio remains dominant in automotive settings and emergency communications, the competitive landscape has fundamentally changed. Broadcasters must now justify transmitter investments against competing digital distribution methods that often require lower capital expenditure. This market dynamic creates hesitation among broadcasters considering significant infrastructure upgrades, particularly in markets with high internet penetration and mature digital media ecosystems.

High Capital and Operational Costs of Transmission Infrastructure to Limit Market Expansion

The substantial investment required for radio transmission infrastructure presents a significant barrier to market growth. High-power transmitters represent major capital expenditures for broadcasters, with costs increasing substantially for higher power units and tower systems. Operational expenses including electricity consumption, site rental fees, and maintenance further contribute to the total cost of ownership. A 50kW FM transmitter can consume over 100,000 kWh annually in electricity alone, creating ongoing operational expenses that broadcasters must justify against audience reach and advertising revenue. These economic considerations become particularly challenging in developing markets and for smaller broadcasters with limited capital resources. The high cost structure also makes it difficult to achieve satisfactory return on investment in competitive media markets, potentially delaying transmitter replacement cycles and new installations.

Spectrum Allocation Challenges and Regulatory Constraints to Hinder Market Development

Radio frequency spectrum scarcity and complex regulatory environments create significant challenges for transmitter market growth. The electromagnetic spectrum represents a finite resource with increasing competition from various services including mobile communications, satellite systems, and other wireless technologies. Broadcasters face pressure to justify their spectrum usage as regulatory bodies consider reallocating frequencies for other services. The complex licensing processes and technical requirements for transmitter installations create additional barriers, particularly for new market entrants. Regulatory compliance often requires extensive documentation, frequency coordination studies, and environmental assessments that can delay projects and increase costs. These regulatory hurdles combined with spectrum scarcity issues create an environment where expansion of radio transmission networks becomes increasingly challenging, particularly in urban areas with congested spectrum availability.

MARKET CHALLENGES

Technical Complexity and Maintenance Requirements to Challenge Market Participants

The radio transmitter market faces significant technical challenges related to system complexity and maintenance requirements. Modern transmitters incorporate sophisticated digital signal processing, cooling systems, and monitoring capabilities that require specialized technical knowledge for proper operation and maintenance. The industry experiences a growing skills gap as experienced technicians retire without adequate replacement by younger professionals familiar with these complex systems. Transmitter manufacturers must invest substantially in training and support services to ensure proper operation of their equipment. The remote location of many transmitter sites further complicates maintenance activities, requiring robust remote monitoring systems and rapid response capabilities when issues arise. These technical challenges increase the total cost of ownership and create operational risks for broadcasters relying on transmission infrastructure for continuous service delivery.

Other Challenges

Interference Management

Managing electromagnetic interference represents an ongoing challenge for transmitter operators. The increasingly crowded radio spectrum creates interference issues that can degrade broadcast quality and violate regulatory requirements. Transmitter systems must incorporate advanced filtering and interference mitigation techniques to maintain signal purity while avoiding interference with other services. This technical requirement adds complexity and cost to transmitter designs while requiring continuous monitoring and adjustment to maintain compliance with regulatory standards.

Environmental and Community Concerns

Transmitter installations often face opposition from local communities concerned about visual impact, property values, and perceived health effects. While scientific evidence confirms radio transmissions at licensed power levels pose no health risks, public perception challenges remain. The siting process for new transmitter installations increasingly involves lengthy community consultations and environmental assessments, creating project delays and additional costs that challenge market growth and infrastructure expansion.

MARKET OPPORTUNITIES

Modernization of Aging Transmission Infrastructure to Create Significant Growth Opportunities

The substantial installed base of aging transmitter infrastructure presents significant replacement opportunities across global markets. Many broadcasting facilities operate equipment that has exceeded its expected service life, creating pent-up demand for modernization. Older analog transmitters particularly require replacement to support digital broadcasting standards and improved efficiency. The replacement cycle is accelerating as broadcasters seek to reduce operating costs through more efficient solid-state transmitters that offer superior power efficiency and reliability compared to older tube-based systems. This infrastructure modernization trend creates sustained demand for transmitter manufacturers, particularly in developed markets where existing equipment reaches end-of-life. The economic benefits of modern transmitters, including reduced energy consumption and maintenance requirements, provide compelling business cases for broadcasters to invest in replacement systems despite budget constraints.

Emerging Market Expansion and Digital Transition Initiatives to Drive Future Growth

Developing regions represent substantial growth opportunities as they initiate digital broadcasting transitions and expand radio coverage. Many countries in Asia, Africa, and Latin America are in early stages of digital migration, creating new demand for transmission equipment. Government initiatives to expand broadcast coverage to rural and remote communities further drive market growth in these regions. The Asia-Pacific region already accounts for approximately 40% of the global market and continues to show strong growth potential. International development organizations often support broadcasting infrastructure projects in emerging markets to improve information access and emergency communication capabilities. These initiatives combined with growing advertising markets and increasing vehicle ownership create favorable conditions for transmitter market expansion in developing economies where radio remains a primary information source for large population segments.

Integration of Advanced Technologies and Smart Broadcasting Solutions to Open New Opportunities

Technological advancements in transmitter design and broadcasting systems create new market opportunities through enhanced functionality and efficiency. Modern transmitters increasingly incorporate Internet of Things connectivity, remote monitoring capabilities, and advanced diagnostics that improve operational efficiency and reduce maintenance costs. The integration of artificial intelligence for predictive maintenance and optimization represents another emerging opportunity. Transmitter manufacturers that can offer smart broadcasting solutions with reduced total cost of ownership gain competitive advantage in the market. Additionally, the development of more compact and efficient transmitter designs enables new installation opportunities in urban environments and shared tower situations. These technological innovations allow broadcasters to achieve better coverage with lower power consumption and reduced physical footprint, addressing several market constraints while creating new application possibilities for radio transmission technology.

RADIO TRANSMITTER MARKET TRENDS

Integration of Digital and IP-Based Technologies to Emerge as a Dominant Trend

The global radio transmitter market is undergoing a significant transformation driven by the integration of digital and Internet Protocol (IP)-based technologies. While the market is projected to grow modestly from 308 million in 2024 to 320 million by 2032, this evolution is crucial for future-proofing broadcasting infrastructure. The transition from traditional analog systems to Digital Audio Broadcasting (DAB/DAB+) and HD Radio is a primary catalyst, demanding transmitters capable of handling complex digital modulation schemes and robust error correction. This shift is not merely about audio quality; it enables broadcasters to transmit additional data services, such as traffic information and song metadata, creating new revenue streams. Furthermore, the adoption of IP networking for studio-to-transmitter links (STLs) and remote control systems enhances operational flexibility, reduces maintenance costs, and allows for more sophisticated network-wide management and monitoring from centralized locations.

Other Trends

Energy Efficiency and Solid-State Technology Adoption

The push for operational cost reduction and sustainability is accelerating the adoption of highly efficient, solid-state radio transmitters. Modern solid-state power amplifiers (SSPAs) are increasingly replacing older tube-based systems because they offer superior power efficiency, often exceeding 40% efficiency compared to the 25-30% typical of tube amplifiers. This directly translates to a substantial reduction in electricity consumption and cooling requirements, a critical factor given that energy can constitute over 50% of a broadcast station’s operational expenditure. The inherent reliability and longer lifespan of solid-state components also minimize downtime and maintenance costs, making them an economically compelling choice for both new installations and infrastructure upgrades, particularly in the dominant FM segment which holds approximately 50% of the market.

Expansion in Automotive and Emergency Communication Applications

The automobile sector, which accounts for over 45% of the market application, continues to be a powerful driver for radio transmitter demand. The integration of advanced infotainment systems in vehicles, including those with hybrid and digital radio capabilities, sustains a steady need for transmitter infrastructure to ensure coverage and signal quality. Beyond entertainment, there is a growing emphasis on robust emergency communication systems. Governments and public safety organizations worldwide are investing in modernizing their alert and warning systems, which rely heavily on high-power, highly reliable AM and FM transmitters to broadcast critical information to the public during crises. This dual demand from consumer automotive and public safety sectors provides a stable foundation for market growth, even as other segments face increased competition from streaming services.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Technological Innovation and Global Expansion to Maintain Market Position

The global radio transmitter market exhibits a semi-consolidated competitive structure, characterized by the presence of established multinational corporations, specialized medium-sized enterprises, and niche regional players. GatesAir and Broadcast Electronics are dominant forces, collectively accounting for a significant portion of the market share. Their leadership is underpinned by extensive product portfolios that span FM, shortwave, and medium wave transmitters, coupled with robust distribution networks across key regions like North America and Asia-Pacific.

Rohde & Schwarz (R&S) and Nautel also command considerable market influence, particularly in the high-power transmitter segment and digital broadcasting solutions. These companies have strengthened their positions through continuous innovation, such as the development of energy-efficient transmitters and advanced solid-state technologies, which resonate with the industry’s shift towards sustainable broadcasting infrastructure.

Moreover, strategic initiatives like mergers, acquisitions, and partnerships are prevalent among top players aiming to enhance their technological capabilities and geographic reach. For instance, several leading companies have recently expanded their manufacturing facilities in Asia to capitalize on the region’s growing demand, which constitutes approximately 40% of the global market.

Meanwhile, emerging players and regional specialists, such as Egatel (COMSA) in Europe and Beijing BBEF in Asia, are increasingly competing through cost-effective solutions and tailored products for local market requirements. Their growth is further fueled by investments in research and development focused on next-generation broadcasting technologies, ensuring the overall market remains dynamic and competitive.

List of Key Radio Transmitter Companies Profiled

- GatesAir (U.S.)

- Broadcast Electronics (U.S.)

- Rohde & Schwarz (R&S) (Germany)

- Syes (China)

- Egatel (COMSA) (Spain)

- Nautel (Canada)

- Thomson Broadcast (France)

- RIZ Transmitters (Croatia)

- Continental (Germany)

- Beijing BBEF (China)

- Tongfang Gigamega (China)

- Chengdu ChengGuang (China)

- Elenos (Italy)

Segment Analysis:

By Type

FM Radio Transmitter Segment Dominates the Market Due to its Pervasive Use in Broadcasting and Automotive Applications

The market is segmented based on type into:

- FM Radio Transmitter

- Shortwave Radio Transmitter

- Medium Wave Transmitter

By Application

Automobile Segment Leads Due to High Integration in In-Vehicle Infotainment and Communication Systems

The market is segmented based on application into:

- Aerospace

- Automobile

- Electronics Industry

- Others

By Power Output

Medium Power Transmitters (10kW – 100kW) Hold Significant Market Share for Regional Broadcasting

The market is segmented based on power output into:

- Low Power (1kW – 10kW)

- Medium Power (10kW – 100kW)

- High Power (100kW – 500kW)

By End User

Broadcasting Corporations Represent the Core End User Segment for High-Power Transmission Infrastructure

The market is segmented based on end user into:

- Broadcasting Corporations

- Telecommunication Service Providers

- Government and Defense

- Industrial and Commercial Enterprises

Regional Analysis: Radio Transmitter Market

Asia-Pacific

Asia-Pacific dominates the global radio transmitter market, accounting for approximately 40% of the total market share. This leadership is driven by extensive infrastructure development, particularly in China and India, where massive investments in broadcasting and telecommunications are underway. China’s ongoing expansion of its national broadcasting network and India’s push for digitalization in radio, including the proliferation of community radio stations, are significant contributors. Furthermore, the region’s large automotive sector, which consumes over 45% of transmitters for applications like in-car entertainment and communication systems, fuels consistent demand. While cost sensitivity keeps demand strong for conventional FM transmitters, there is a noticeable shift towards more advanced digital and HD radio systems, especially in urban centers aiming to improve signal quality and spectrum efficiency.

North America

North America represents a mature yet technologically advanced market for radio transmitters, characterized by a strong focus on innovation and the transition to digital broadcasting standards. The region is a key hub for leading manufacturers like GatesAir and Broadcast Electronics. Market dynamics are heavily influenced by the need for spectrum repurposing and infrastructure upgrades, particularly with the ongoing deployment of ATSC 3.0 (NextGen TV) in the United States, which requires new transmitter installations. Regulatory bodies like the FCC continue to shape the market through spectrum allocation policies. While the terrestrial radio broadcasting segment remains stable, growth is increasingly driven by niche applications, including emergency alert systems and specialized two-way communication networks for public safety and industrial use.

Europe

The European market is defined by stringent regulatory standards and a strong push for energy efficiency and modernization. The region’s aging transmitter infrastructure is undergoing a significant refresh cycle, with broadcasters and network operators replacing older analog systems with solid-state and DRM (Digital Radio Mondiale) compatible transmitters. The European Union’s directives on energy-related products drive demand for more efficient transmitter designs with lower power consumption. Countries like Germany, the UK, and France are at the forefront of adopting DAB+ (Digital Audio Broadcasting) technology, creating a steady demand for new transmitters. However, market growth is tempered by the high saturation of broadcasting services and the competitive pressure from streaming platforms, leading to cautious capital investment from traditional broadcasters.

South America

The South American radio transmitter market presents a landscape of gradual growth and untapped potential. Countries like Brazil and Argentina are focusing on expanding broadcast coverage to rural and remote areas, driving demand for reliable medium-wave and FM transmitters. The market is highly price-sensitive, which favors local manufacturers and suppliers offering cost-effective solutions. However, economic volatility and inconsistent regulatory enforcement often delay large-scale infrastructure projects and hinder the widespread adoption of cutting-edge digital transmission technologies. Despite these challenges, the region’s growing automotive industry and the persistent popularity of traditional radio as a primary media source provide a stable foundation for market development.

Middle East & Africa

This region is an emerging market with growth primarily fueled by national projects aimed at modernizing broadcast infrastructure and improving public communication networks. Gulf Cooperation Council (GCC) countries, such as the UAE and Saudi Arabia, are investing heavily in state-of-the-art broadcasting facilities as part of broader economic diversification plans. In contrast, many African nations are in the early stages of building out their transmission networks, with a focus on basic FM coverage to reach larger populations. A major challenge across the region is securing funding for large-scale projects. While there is a clear need for durable and reliable transmitter equipment, progress is often incremental, focusing on essential coverage expansion rather than technological leapfrogging.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Radio Transmitter markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Radio Transmitter Market?

-> Radio Transmitter Market was valued at 308 million in 2024 and is projected to reach US$ 320 million by 2032, at a CAGR of 0.6% during the forecast period.

Which key companies operate in Global Radio Transmitter Market?

-> Key players include GatesAir, Broadcast Electronics, R&S, Syes, and Egatel(COMSA), among others.

What are the key growth drivers?

-> Key growth drivers include automotive industry demand, broadcasting infrastructure upgrades, and increasing adoption in aerospace applications.

Which region dominates the market?

-> Asia-Pacific is the largest market with approximately 40% share, followed by North America and Europe.

What are the emerging trends?

-> Emerging trends include digital broadcasting transition, integration of IoT capabilities, and development of energy-efficient transmitters.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...