Quantum Semiconductor Device Market Insights

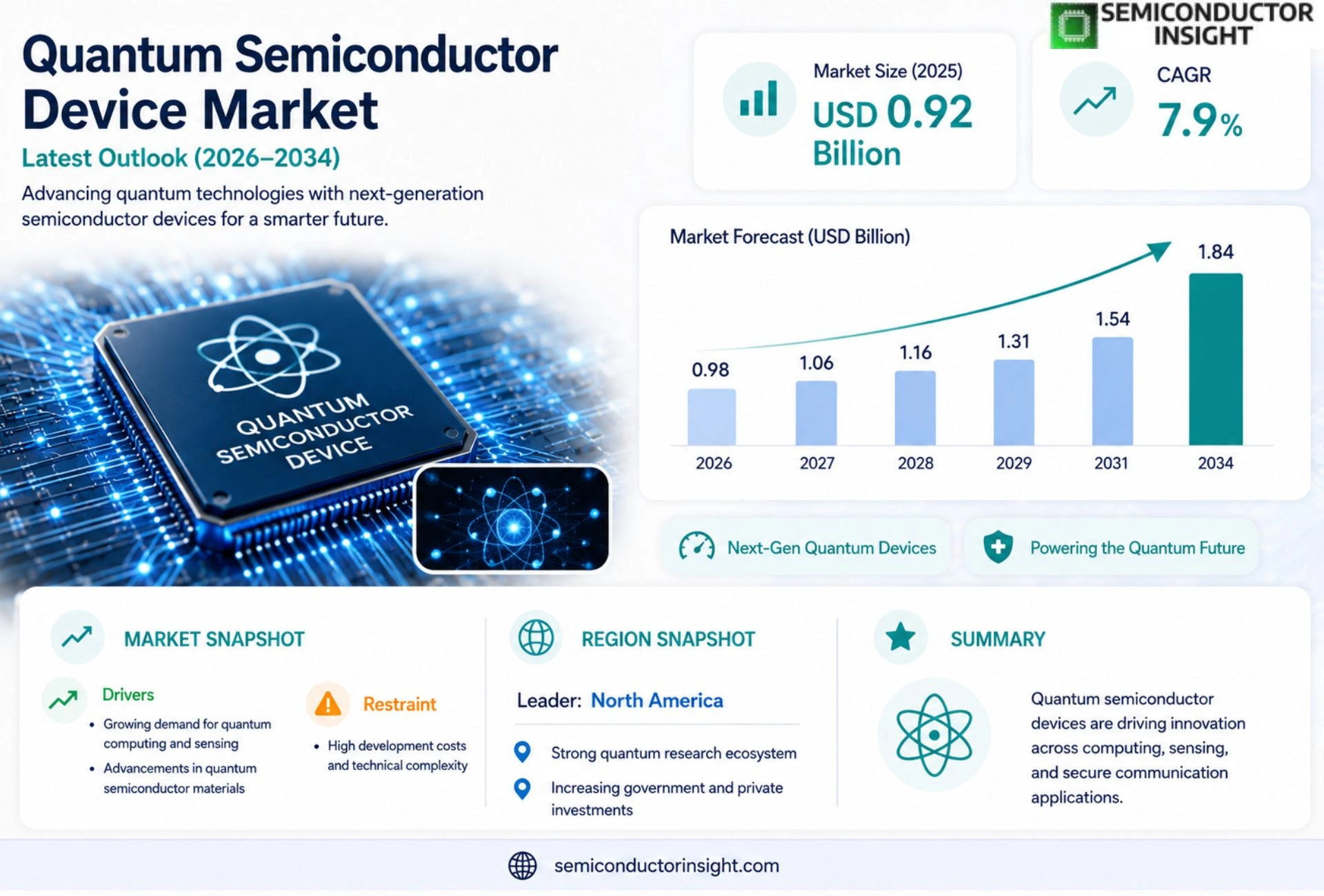

Global Quantum Semiconductor Device market size was valued at USD 0.92 billion in 2025. The market is projected to grow from USD 0.98 billion in 2026 to USD 1.84 billion by 2034, exhibiting a CAGR of 7.9 % during the forecast period.

Quantum semiconductor devices are engineered components that exploit quantum mechanical effects,such as superposition, tunneling and discrete energy levels,to perform functions beyond classical semiconductors. These devices include quantum dots, single‑electron transistors, superconducting qubits on silicon platforms and resonant tunneling diodes used in ultra‑low‑power logic and sensing applications.

The market is accelerating because of heightened government funding for quantum research, rising demand for high‑performance computing workloads, and rapid advances in nanofabrication techniques that lower production costs. Furthermore, strategic collaborations are fueling growth; for example, in January 2024 Intel announced a joint development agreement with QuTech to co‑design silicon‑based qubit architectures for scalable processors. Other key players such as IBM, Google (Alphabet), and Qorvo are expanding their portfolios through investments and partnerships that broaden the ecosystem.

MARKET DRIVERS

Growing Demand for Quantum Computing

Quantum Semiconductor Device Market is being propelled by accelerating adoption of quantum processors in research laboratories and emerging commercial applications. Enterprises are allocating budget to prototype quantum‑accelerated workloads, creating a steady pipeline of orders for advanced semiconductor components.

Advances in Materials and Fabrication

Breakthroughs in silicon‑based qubits, superconducting circuits, and low‑loss photonic platforms have reduced error rates and improved coherence times. These technical gains enable manufacturers to offer higher‑performance devices, reinforcing confidence across the supply chain.

➤ Industry analysts note that collaborative research programs are shortening development cycles, allowing new quantum semiconductor products to reach pilot production within three to five years.

In addition, increasing venture capital participation provides the financial depth required for long‑term R&D, ensuring Quantum Semiconductor Device Market can sustain growth beyond the early adoption phase.

MARKET CHALLENGES

Technical Complexity and Integration

Designing quantum‑grade semiconductor devices demands sub‑nanometer precision and stringent material purity. Integrating these components with existing classical control electronics introduces thermal management and signal‑noise challenges that can delay product launches.

Other Challenges

Manufacturing Yield

Achieving consistent yield across wafer lots remains difficult due to sensitivity to minute defects. Low yield drives up unit costs and can deter early‑stage adopters who require cost‑effective solutions.

MARKET RESTRAINTS

High Capital Expenditure

Establishing clean‑room facilities and cryogenic testing infrastructure requires multi‑hundred‑million dollar investments. This financial barrier limits the number of players that can viably enter Quantum Semiconductor Device Market.

The long payback horizon associated with quantum hardware further discourages traditional semiconductor investors who seek quicker returns, narrowing the funding pool to specialized venture funds and government programs.

Regulatory uncertainty surrounding export controls for advanced quantum technologies adds another layer of risk, potentially restricting cross‑border collaborations and market expansion.

MARKET OPPORTUNITIES

Strategic Partnerships and Government Initiatives

National quantum strategies in the United States, Europe, and Asia allocate billions of dollars to support quantum semiconductor research, creating co‑funded projects that lower entry costs for manufacturers.

Collaboration between semiconductor foundries and quantum‑focused startups accelerates technology transfer, enabling faster scaling of production volumes and diversification of product portfolios.

Emerging applications in secure communications, quantum‑enhanced sensing, and high‑performance computing open niche markets where premium pricing can offset high manufacturing expenses, offering attractive margins for early movers.

Quantum Semiconductor Device Market Trends

Government Funding and Collaboration Surge

In recent years Quantum Semiconductor Device Market has been propelled by a pronounced increase in public research budgets across North America, Europe, and Asia‑Pacific. National programs are allocating billions of dollars to quantum‑focused initiatives, which creates a predictable pipeline for technology developers. Simultaneously, strategic alliances between chip manufacturers and academic labs are maturing into joint development projects. Notably, the early‑2024 agreement between a leading silicon‑chip producer and a European quantum‑technology institute to co‑design silicon‑based qubit architectures exemplifies this trend. These collaborations accelerate knowledge transfer, reduce time‑to‑market, and enable shared risk in the creation of next‑generation quantum devices.

Other Trends

Advances in Nanofabrication

Progress in extreme‑ultraviolet lithography, atomic‑layer deposition, and low‑temperature annealing has lowered the cost barrier for fabricating quantum‑grade structures such as quantum dots and resonant tunneling diodes. Engineers now routinely achieve sub‑nanometer control of feature dimensions, which improves device uniformity and yields. The result is a more reliable supply chain for quantum semiconductor components, allowing OEMs to transition from prototype to low‑volume production with greater confidence.

Shift Toward Silicon‑Based Qubit Architectures

The market is observing a decisive movement away from exotic material systems toward silicon‑compatible qubit designs. Silicon offers a mature manufacturing ecosystem, established defect‑control processes, and inherent scalability. Companies that traditionally focused on classical logic are repurposing existing fabs to host superconducting and spin‑based qubits integrated on silicon wafers. This convergence reduces capital expenditures for new facilities and aligns quantum device development with existing supply‑chain logistics, thereby strengthening the overall health of Quantum Semiconductor Device Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape Overview of Quantum Semiconductor Devices

Quantum Semiconductor Device Market is dominated by a handful of large integrated‑device manufacturers that have leveraged deep silicon‑fab expertise to transition quantum research into production‑grade components. Intel, for instance, has become the de‑facto leader in silicon‑based qubit development, capitalising on its 2024 joint agreement with QuTech to co‑design scalable silicon quantum processors. This collaboration not only accelerates Intel’s roadmap but also sets a benchmark for wafer‑scale integration, allowing the company to capture a growing share of the high‑performance computing segment. IBM’s Quantum System Two platform similarly builds on superconducting qubits integrated with advanced packaging, reinforcing its position in the enterprise‑level quantum cloud services market. The market structure therefore reflects a tiered ecosystem where a few global foundries provide the manufacturing backbone, while specialised start‑ups and research consortia supply niche devices such as resonant tunneling diodes and quantum‑dot photonic components.

Beyond the tier‑one players, a vibrant cohort of niche innovators contributes critical capabilities that broaden the overall value chain. Companies like Qorvo and Rohm are expanding into quantum‑compatible RF and power‑management solutions, while Qatium focuses on quantum‑dot lasers for photonic interconnects. Rigetti Computing and IonQ drive the ecosystem with proprietary superconducting and trapped‑ion qubit architectures respectively, fostering differentiation in quantum algorithm performance. Emerging firms such as QuEra Computing and Xanadu specialise in photonic quantum processors, targeting low‑power, room‑temperature operation. Meanwhile, D‑Wave continues to dominate the quantum‑annealing niche, providing distinct hardware for optimisation problems. This diversity of players creates a competitive yet collaborative environment that accelerates standardisation, reduces cost, and widens adoption across sectors ranging from aerospace to pharmaceutical research.

List of Key Quantum Semiconductor Device Companies Profiled

- Intel

- IBM

- Google (Alphabet)

- Qorvo

- Rohm Semiconductor

- Qatium

- Rigetti Computing

- IonQ

- QuEra Computing

- Xanadu

- D‑Wave Systems

- Honeywell Quantum Solutions

- Samsung Electronics

- Microsoft Azure Quantum

- Hewlett Packard Enterprise (HPE)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Superconducting Qubits

|

| By Application |

|

High‑Performance Computing

|

| By End User |

|

Research Laboratories

|

| By Technology Platform |

|

Silicon‑Based Platforms

|

| By Development Phase |

|

Prototype

|

Regional Analysis: North America

The technology landscape in the US is characterized by continuous innovation in areas like superconducting qubits, trapped ion qubits, and photonic qubits. Significant investments are being made in developing more stable and scalable quantum devices.

Investment trends in the US are indicating a sustained upward trajectory, with venture capital funding and government grants playing a crucial role in propelling the growth of quantum semiconductor companies.

Major players in the US Quantum Semiconductor Device Market include Intel, IBM, Google, and various startups focused on niche applications and technologies.

The future outlook for the US Quantum Semiconductor Device Market remains highly promising, with anticipated advancements in device performance, coherence times, and scalability paving the way for wider adoption.

Europe

Europe is emerging as a significant player Quantum Semiconductor Device Market, driven by strong government initiatives and a growing ecosystem of research institutions and startups. The European Union’s Quantum Flagship program is fostering collaboration and investment in quantum technologies across the continent. Key areas of focus include developing superconducting and silicon-based qubits, as well as quantum photonic devices. Business strategies here emphasize fostering strong partnerships between academia, industry, and national research centers. There’s a keen focus on developing specialized quantum devices for applications in drug discovery, materials science, and financial modeling.

Asia-Pacific

Asia-Pacific, particularly countries like China, Japan, and South Korea, is witnessing rapid growth Quantum Semiconductor Device Market. These nations are investing heavily in quantum computing research and development, aiming to become global leaders in this field. China’s government has set ambitious targets for quantum technology development, leading to substantial investments in hardware, software, and infrastructure. Japan and South Korea are leveraging their strengths in semiconductor manufacturing and materials science to develop advanced quantum devices. The demand for these devices is primarily driven by the growing needs of telecommunications, artificial intelligence, and high-performance computing industries.

South America

South America presents a nascent market for Quantum Semiconductor Devices, with early-stage research and development activities primarily concentrated in universities and research institutions. While investment levels are currently modest, the long-term potential is significant, particularly in areas such as financial modeling, logistics optimization, and scientific research. The region’s strong focus on data analytics and digital transformation could drive future demand for quantum-enhanced computing solutions.

Middle East & Africa

The Middle East and Africa represent a relatively untapped market for Quantum Semiconductor Devices. However, with increasing investments in technology and a growing emphasis on innovation, the region is poised for future growth. Initial applications are likely to be in areas such as cybersecurity, finance, and precision navigation. Government initiatives aimed at diversifying economies and fostering technological advancement could play a crucial role in accelerating the adoption of quantum technologies.

Report Scope

This market research report provides a comprehensive analysis of the Quantum Semiconductor Device Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quantum Semiconductor Device Market?

-> Quantum Semiconductor Device Market was valued at USD 0.92 billion in 2025 and is expected to reach USD 1.84 billion by 2034, representing a CAGR of 7.9 %.

Which key companies operate Quantum Semiconductor Device Market?

-> Key players include Intel, IBM, Google (Alphabet), Qorvo, and QuTech, among others.

What are the key growth drivers?

-> Key growth drivers include heightened government funding for quantum research, rising demand for high‑performance computing workloads, and rapid advances in nanofabrication techniques that lower production costs.

Which region dominates the market?

-> The global market remains the primary focus, with North America and Asia‑Pacific showing the strongest investment activity and adoption rates.

What are the emerging trends?

-> Emerging trends include development of quantum dots, single‑electron transistors, superconducting qubits on silicon platforms, and resonant tunneling diodes for ultra‑low‑power logic and sensing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...