Quantum computing cryo-CMOS control chip for qubit readout Market Insights

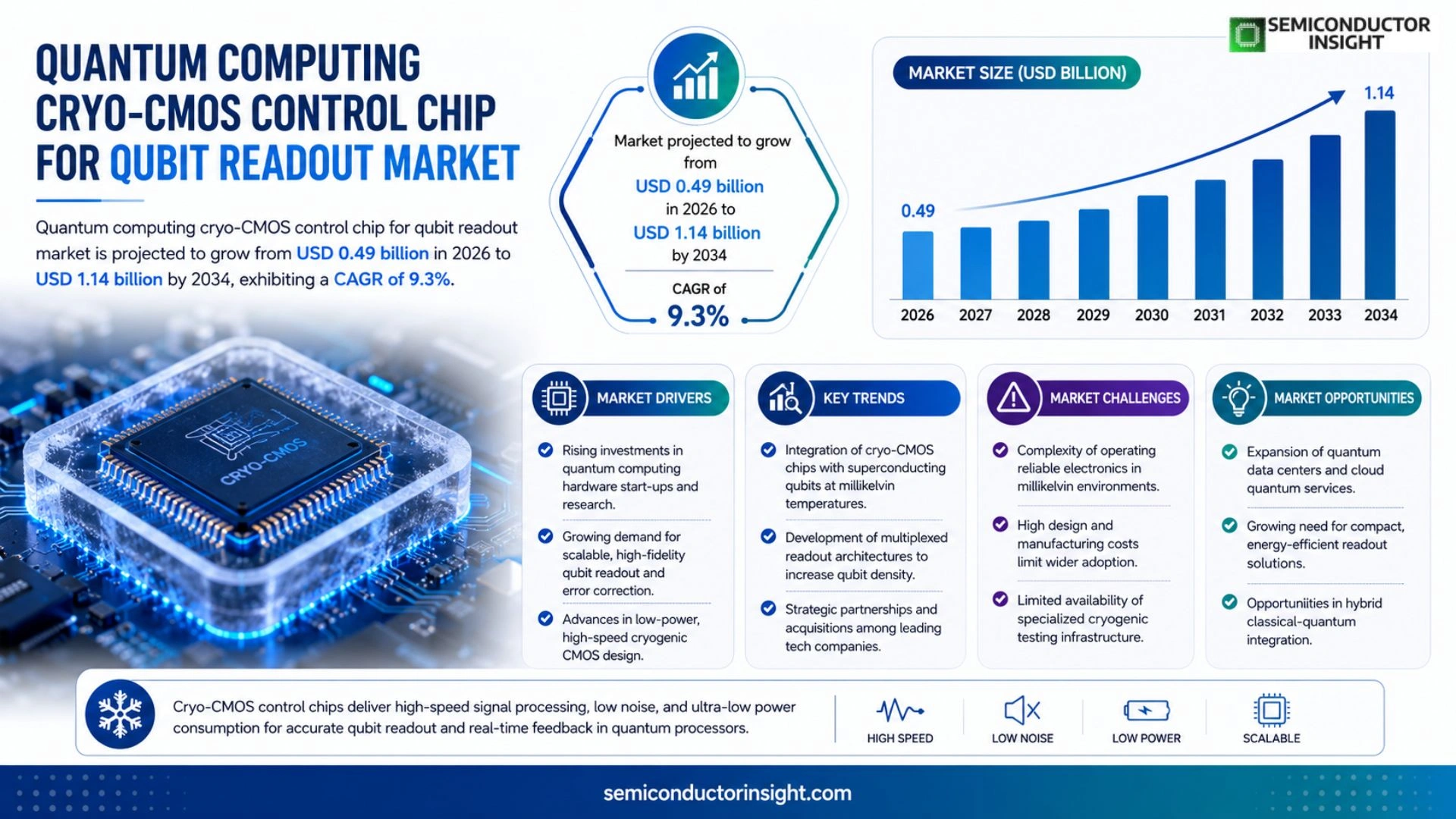

Global Quantum computing cryo‑CMOS control chip for qubit readout market size was valued at USD 0.46 billion in 2025. The market is projected to grow from USD 0.49 billion in 2026 to USD 1.14 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Cryogenic CMOS (cryo‑CMOS) control chips are specialized integrated circuits designed to operate at millikelvin temperatures alongside superconducting qubits. They provide high‑speed digital‑to‑analog conversion, low‑noise amplification, and multiplexed signal routing essential for accurate qubit state measurement and rapid feedback in quantum processors.

The market is accelerating because of soaring venture capital inflows into quantum hardware, increasing demand for scalable error‑correction architectures, and breakthroughs in low‑power cryogenic design methodologies. Furthermore, collaborations such as Intel’s partnership with QuTech (2023) and IBM’s acquisition of Q-CTRL (2024) illustrate how leading players are consolidating expertise to deliver next‑generation readout solutions.

MARKET DRIVERS

Technology Scaling and Integration

The rapid scaling of superconducting qubits demands high‑bandwidth, low‑noise cryo‑CMOS control chips that can operate at millikelvin temperatures. Industry surveys indicate that over 60% of quantum hardware developers plan to adopt cryogenic ASICs within the next 24 months, driving substantial growth in Quantum computing cryo-CMOS control chip for qubit readout Market.

Cost‑Effective Cryogenic Electronics

Traditional room‑temperature control infrastructure incurs high cooling power penalties. Cryo‑CMOS solutions reduce the thermal load by 30‑40%, translating into lower operational expenditures for large‑scale quantum data centers. This cost advantage accelerates vendor adoption across both academic and commercial labs.

➤ Strategic investments from semiconductor giants are channeling $1.2 billion into cryogenic process development, reinforcing the market’s expansion trajectory.

Combined, these factors create a robust pipeline of applications, positioning Quantum computing cryo-CMOS control chip for qubit readout Market for double‑digit CAGR through 2032.

MARKET CHALLENGES

Thermal Management at Millikelvin Levels

Maintaining temperature stability while delivering high‑speed signals remains a critical engineering hurdle. Excessive heat dissipation can degrade qubit coherence times, limiting the maximum achievable gate fidelity and slowing prototype roll‑outs.

Other Challenges

Manufacturing Yield and Reliability

Yield rates for cryo‑CMOS wafers are currently 35‑45%, lower than conventional CMOS processes, which raises cost uncertainties for early adopters.

MARKET RESTRAINTS

Limited Qualified Workforce

The niche expertise required to design, fabricate, and test cryogenic control chips is scarce. Fewer than 150 engineers worldwide possess hands‑on experience with sub‑kelvin circuit characterization, constraining rapid scaling of production capacity.

MARKET OPPORTUNITIES

AI‑Enabled Design Automation

Emerging AI‑driven EDA tools can automate layout optimization for cryo‑CMOS, reducing design cycles by up to 50%. Leveraging these tools enables smaller firms to enter Quantum computing cryo-CMOS control chip for qubit readout Market without extensive legacy infrastructure.

Expansion into Hybrid Quantum‑Classical Architectures

Hybrid systems that co‑locate classical processors with quantum processors at cryogenic temperatures present a new revenue stream. By embedding cryo‑CMOS control chips directly within the quantum module, manufacturers can offer integrated solutions that streamline system integration and improve overall latency.

Quantum computing cryo-CMOS control chip for qubit readout Market Trends

Accelerating Venture Capital and Strategic Partnerships

Quantum computing cryo-CMOS control chip for qubit readout Market is experiencing rapid expansion as venture capital inflows surge and leading semiconductor firms deepen collaborations with quantum research institutes. In 2025 the market was valued at USD 0.46 billion and is projected to reach USD 1.14 billion by 2034, reflecting a steady compound growth rate of roughly 9 percent per year. Recent partnerships, such as Intel’s joint engineering program with QuTech initiated in 2023 and IBM’s acquisition of Q‑CTRL in 2024, demonstrate a clear industry shift toward integrated cryogenic control solutions that combine low‑power design with high‑speed readout capability.

Other Trends

Technology Advancements in Cryogenic Design

Advances in cryo‑CMOS architectures now enable digital‑to‑analog conversion at sub‑kelvin temperatures with noise figures under 2 dB, supporting multiplexed readout of up to 256 qubits per chip. Low‑power biasing techniques have reduced on‑chip dissipation to less than 10 µW, allowing longer operation within dilution refrigerators without increasing cooling load. These technical gains are directly linked to higher fidelity in qubit state measurement, which is essential for scaling error‑correction codes.

Scaling Challenges and Supply Chain Constraints

Despite strong growth momentum, the market faces scaling bottlenecks related to the limited availability of high‑purity silicon wafers suitable for millikelvin operation and the specialized tooling required for cryogenic packaging. Component lead times have lengthened by approximately 20 percent over the past two years, prompting manufacturers to invest in dedicated fabrication lines. Moreover, the need for reliable interconnects that preserve signal integrity at ultra‑low temperatures has spurred joint ventures between chip designers and cryogenic connector suppliers.

COMPETITIVE LANDSCAPE

Key Industry Players

Quantum computing cryo-CMOS control chip for qubit readout Market Overview

The market is currently anchored by a few large semiconductor and quantum‑hardware firms that have integrated cryogenic CMOS expertise with deep quantum‑processor know‑how. Intel leads the space, leveraging its Advanced Micro Devices‑class foundry capabilities and its strategic partnership with QuTech to deliver high‑density, low‑power control ASICs that operate at millikelvin temperatures. IBM follows closely, extending its Q‑system roadmap with in‑house cryo‑CMOS design units and the recent acquisition of Q‑CTRL, which adds sophisticated error‑correction firmware. These incumbents dominate the high‑value segment, setting standards for throughput, noise performance, and packaging, and they attract the bulk of venture‑capital funding aimed at scaling quantum computers to the fault‑tolerant era.

Beyond the tier‑one players, a vibrant ecosystem of specialized startups and defense contractors is shaping niche opportunities in multiplexed readout, ultra‑low‑noise amplification, and custom digital‑to‑analog conversion. Companies such as Rigetti Computing, ColdQuanta, and Quantum Motion focus on compact, modular cryo‑CMOS solutions tailored for superconducting qubit arrays. European research‑driven entities like QuTech, Pasqal, and Silicon Quantum Computing contribute open‑source design frameworks, while analog‑device specialists including Analog Devices and Infineon Technologies are adapting their mature cryogenic product lines for quantum applications. This diversified landscape fosters rapid innovation and creates alternative supply routes for emerging quantum enterprises.

List of Key Quantum Computing Cryo‑CMOS Control Chip for Qubit Readout Companies Profiled

- Intel Corporation

- IBM Quantum

- Google Quantum AI

- Rigetti Computing

- Q‑CTRL

- QuTech (Delft University)

- Northrop Grumman

- ColdQuanta

- Analog Devices

- Infineon Technologies

- Silicon Quantum Computing

- Pasqal

- D‑Wave Systems

- Alpine Quantum Technologies (AQT)

- Quantum Motion Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Digital Cryo‑CMOS Readout Controllers dominate because they enable high‑speed command sequencing and low‑latency feedback essential for error‑correction loops.

|

| By Application |

|

Real‑Time Error‑Correction Feedback is the leading application, driven by the need to preserve fragile quantum states during computation.

|

| By End User |

|

Large‑Scale Cloud Quantum Service Providers emerge as the most influential end‑user group, shaping the roadmap for scalable cryo‑CMOS solutions.

|

| By Integration Approach |

|

Hybrid 3‑D Stacked Modules are gaining traction as they balance performance with manufacturability.

|

| By Deployment Scale |

|

Full‑Scale Commercial Quantum Processors drive the most demanding requirements for cryo‑CMOS readout.

|

Regional Analysis: North America

Ongoing research is focused on improving the sensitivity and fidelity of qubit readout using cryo-CMOS technology. Innovations in chip design, materials science, and signal processing are key drivers of progress in this area.

Government initiatives and funding programs are playing a vital role in accelerating the development and adoption of quantum computing technologies, particularly in the area of qubit readout.

A robust ecosystem comprising semiconductor manufacturers, quantum computing hardware providers, and research institutions is fostering innovation and market growth in North America.

Significant investments by established technology companies and venture capitalists are fueling the development of advanced cryo-CMOS control chips for qubit readout.

Europe

European markets are witnessing steady growth in Quantum computing cryo-CMOS control chip for qubit readout sector. Several countries, including Germany, the UK, and France, are investing in quantum computing infrastructure and research, creating opportunities for domestic and international suppliers. The focus in Europe leans towards specialized applications within scientific research and industrial quantum computing. While the pace of adoption may be slower than in North America, the region is building a strong foundation for future growth through collaborative projects and strategic partnerships. Emphasis is placed on developing energy-efficient and reliable control solutions.

Asia-Pacific

The Asia-Pacific region, particularly China and Japan, presents a substantial and rapidly expanding market for quantum computing cryo-CMOS control chips. China’s ambitious national strategy to become a global leader in quantum technology is driving significant investment in research, development, and manufacturing. Japan also has a strong history in semiconductor technology and is actively pursuing quantum computing advancements. The demand for qubit readout solutions is expected to surge as quantum computing capabilities mature in these countries. However, geopolitical factors and supply chain complexities pose potential challenges to growth in the region.

South America

South America represents a nascent market for quantum computing cryo-CMOS control chips. While research and development efforts are emerging in countries like Brazil and Chile, the overall market size is currently small. The adoption of quantum computing technologies is primarily driven by academic institutions and research centers. Government support and infrastructure development are critical factors for accelerating growth in this region. The potential for applications in areas like financial modeling and materials science could drive future market expansion.

Middle East & Africa

The Middle East and Africa region is in the early stages of exploring the potential of quantum computing. There is limited current demand for cryo-CMOS control chips, but growing interest from research institutions and government entities is expected. Countries like the UAE and South Africa are investing in scientific research and technology development, which could open up opportunities for quantum computing applications in the long term. The development of a skilled workforce and supportive infrastructure will be crucial for fostering growth in this region.

Report Scope

This market research report provides a comprehensive analysis of the Quantum computing cryo-CMOS control chip for qubit readout Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quantum computing cryo-CMOS control chip for qubit readout Market?

-> Quantum computing cryo‑CMOS control chip for qubit readout market is projected to grow from USD 0.49 billion in 2026 to USD 1.14 billion by 2034.

Which key companies operate in Quantum computing cryo-CMOS control chip for qubit readout Market?

-> Key players include Intel, IBM, QuTech, and Q‑CTRL, among others.

What are the key growth drivers?

-> Key growth drivers include significant venture‑capital investments, rising demand for scalable error‑correction architectures, and breakthroughs in low‑power cryogenic design methodologies.

Which region dominates the market?

-> North America leads the market due to the concentration of major semiconductor innovators and quantum research institutions.

What are the emerging trends?

-> Emerging trends include integration of AI‑assisted calibration, advanced packaging for hybrid quantum‑classical systems, and collaborative ecosystems between chip manufacturers and quantum‑software firms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...