MARKET INSIGHTS

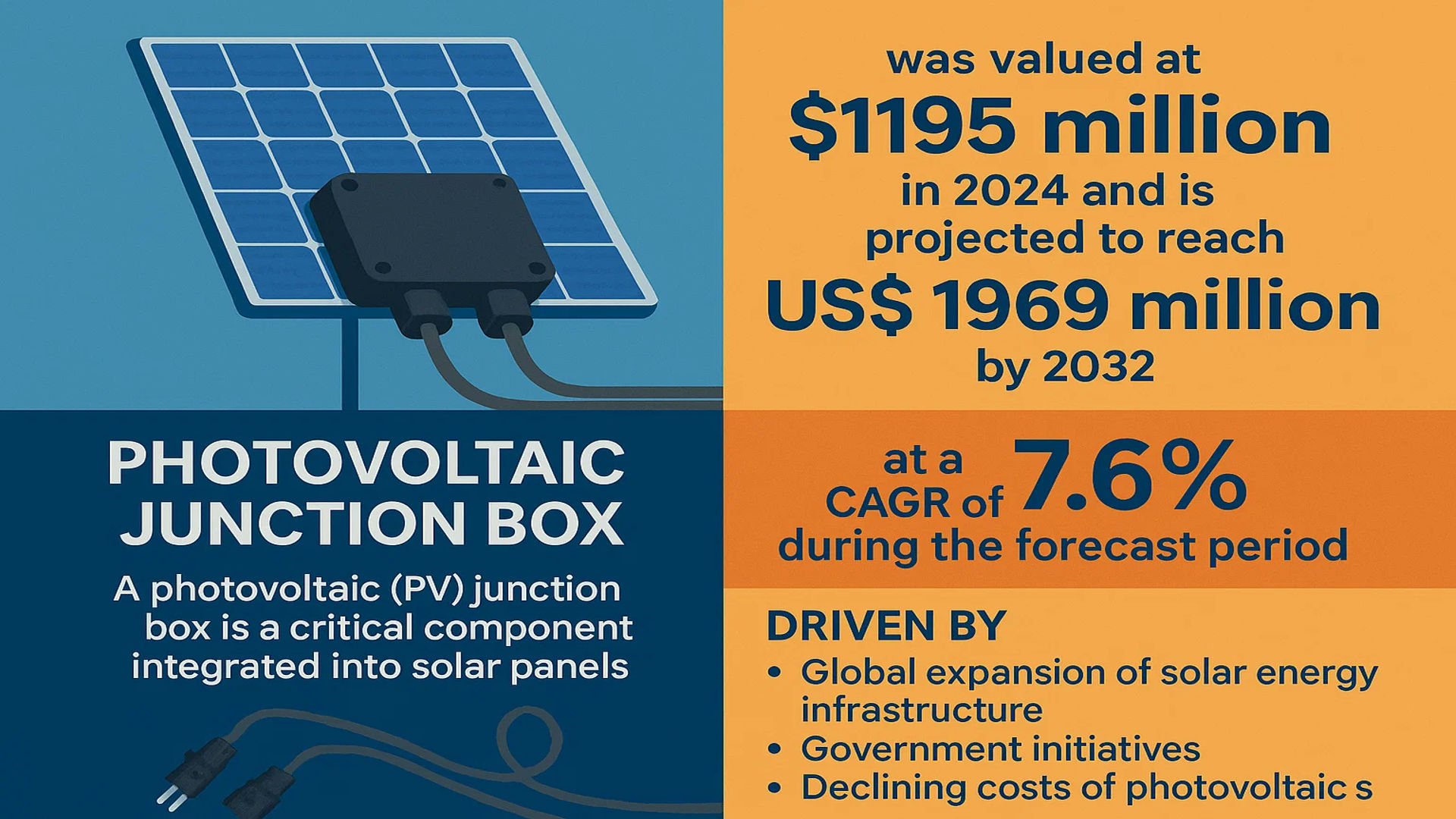

The global PV Junction Box Market was valued at 1195 million in 2024 and is projected to reach US$ 1969 million by 2032, at a CAGR of 7.6% during the forecast period.

A photovoltaic (PV) junction box is a critical component integrated into solar panels. This enclosure is mounted directly onto the back of a PV module and serves as the central hub where the photovoltaic strings are electrically interconnected. Its primary function is to act as the interface between the panel’s internal conductor ribbons and the external DC input and output cables, ensuring efficient power transmission and providing essential protection against environmental factors and electrical faults.

This robust growth is primarily driven by the global expansion of solar energy infrastructure, supported by government initiatives and declining costs of photovoltaic systems. However, the market faces challenges such as price volatility of raw materials and the need for continuous innovation to enhance durability and efficiency. Furthermore, technological advancements aimed at developing smart junction boxes with integrated monitoring capabilities are creating new opportunities for market players, including key manufacturers such as TE Connectivity, Amphenol, and Stäubli Electrical Connectors.

MARKET DYNAMICS

MARKET DRIVERS

Global Expansion of Solar Energy Infrastructure to Drive PV Junction Box Demand

The global solar energy market is experiencing unprecedented growth, with installed capacity projected to exceed 2.3 terawatts by 2025, creating substantial demand for photovoltaic components including junction boxes. This expansion is primarily driven by government initiatives promoting renewable energy adoption, with over 130 countries implementing solar energy support policies. The increasing focus on carbon neutrality targets has accelerated solar farm deployments worldwide, particularly in the utility-scale segment which accounts for approximately 60% of global solar installations. As solar panel production reaches record levels exceeding 300 gigawatts annually, the requirement for reliable electrical connection systems has become paramount, positioning PV junction boxes as critical components in the solar value chain.

Technological Advancements in Solar Panel Efficiency to Boost Market Growth

Continuous innovation in solar panel technology is significantly driving the PV junction box market. The transition towards higher efficiency modules, with premium panels now achieving conversion rates exceeding 22%, requires more sophisticated electrical management systems. Modern junction boxes incorporate advanced features such as integrated bypass diodes that reduce power loss from shading by up to 30%, smart monitoring capabilities enabling real-time performance tracking, and enhanced heat dissipation technologies that maintain optimal operating temperatures. The development of multi-contact junction boxes capable of handling increased current densities up to 20 amperes has become essential for next-generation high-output panels. These technological improvements directly correlate with improved system reliability and extended product lifespan, making them increasingly attractive to both manufacturers and end-users.

Furthermore, the integration of smart technologies within junction boxes enables predictive maintenance and fault detection, reducing operational costs and improving overall system efficiency. The adoption of these advanced features has become particularly crucial as solar installations expand into more demanding environments and applications.

➤ For instance, recent industry developments include the introduction of junction boxes with integrated wireless monitoring systems that can detect performance issues and potential failures before they impact system output, representing a significant advancement in solar technology.

Additionally, the standardization of safety features and compliance with international certification requirements has driven manufacturers to develop more robust and reliable junction box designs, further stimulating market growth across all solar application segments.

MARKET CHALLENGES

Intense Price Competition and Margin Pressure to Challenge Market Growth

The PV junction box market faces significant challenges from intense price competition, particularly from manufacturers in cost-competitive regions. With over 200 manufacturers operating globally and the top five players holding approximately 25% market share, pricing pressures have intensified as companies strive to maintain market position. Production costs have increased by approximately 15-20% over the past two years due to rising raw material prices, while end-product prices have remained relatively stable, squeezing manufacturer margins. This situation is particularly challenging for smaller manufacturers who lack the economies of scale enjoyed by market leaders, creating consolidation pressures within the industry.

Other Challenges

Supply Chain Vulnerabilities

Global supply chain disruptions have exposed vulnerabilities in the PV junction box manufacturing ecosystem. Critical raw materials including copper, silver, and specialized plastics have experienced price volatility exceeding 30% annually, while logistics costs have increased by approximately 25-40% compared to pre-pandemic levels. These fluctuations create significant challenges in production planning and inventory management, particularly for manufacturers operating with tight margins and just-in-time production models.

Technical Standardization Issues

The lack of global technical standards for junction box design and compatibility creates interoperability challenges across different solar panel manufacturers. With various connection systems, mounting configurations, and electrical specifications in use, manufacturers must maintain extensive product portfolios to meet diverse customer requirements, increasing production complexity and inventory costs. This fragmentation also complicates the replacement and maintenance processes for end-users, potentially affecting market adoption rates.

MARKET RESTRAINTS

Material Availability and Cost Fluctuations to Deter Market Growth

The PV junction box market faces significant restraints from material availability constraints and cost fluctuations. Copper, which constitutes approximately 40-50% of junction box material content, has experienced price increases exceeding 35% in recent years, while specialized engineering plastics have seen cost increases of 20-25%. These material cost pressures are compounded by increasing quality requirements for higher temperature resistance and longer product lifespans, necessitating more expensive material formulations. The industry’s reliance on specific rare earth elements for advanced conductivity features creates additional supply chain vulnerabilities, particularly given the concentrated geographic sources of these materials.

Additionally, the need for compliance with various international safety standards and certification requirements adds substantial testing and validation costs, particularly for manufacturers targeting multiple geographic markets. These factors collectively increase the entry barriers for new market participants and constrain profit margins for existing manufacturers, potentially limiting investment in innovation and capacity expansion.

MARKET OPPORTUNITIES

Emergence of Building-Integrated Photovoltaics to Provide Profitable Growth Opportunities

The rapidly growing building-integrated photovoltaics (BIPV) segment presents substantial opportunities for advanced PV junction box solutions. The global BIPV market is projected to grow at approximately 18% annually, requiring specialized junction boxes that offer enhanced aesthetic integration, improved safety features, and compatibility with building materials. These applications demand junction boxes with reduced profiles, custom color options, and advanced waterproofing capabilities exceeding IP68 standards. The integration of junction boxes with building management systems enables seamless energy monitoring and control, creating additional value propositions for architects and building owners.

Furthermore, the development of lightweight and flexible junction box solutions for emerging applications such as solar vehicles, portable solar systems, and aerospace applications opens new market segments. These specialized applications require junction boxes that can withstand extreme environmental conditions, including temperature ranges from -40°C to 120°C, high vibration environments, and exposure to various chemicals and fuels.

Additionally, the increasing adoption of microinverter and power optimizer technologies creates opportunities for integrated junction box solutions that combine traditional connection functions with power electronics. These integrated systems can improve overall system efficiency by 5-8% while reducing installation complexity and costs, representing a significant advancement in solar technology architecture.

PV JUNCTION BOX MARKET TRENDS

Shift Towards High-Efficiency and Smart Junction Boxes to Emerge as a Dominant Trend

The global PV junction box market is witnessing a significant paradigm shift from basic passive components to advanced, high-efficiency, and smart junction boxes. This evolution is primarily driven by the solar industry’s relentless pursuit of maximizing energy yield and improving the Levelized Cost of Energy (LCOE). Traditional junction boxes, which primarily served as connection and protection units, are being rapidly supplanted by smart junction boxes integrated with bypass diodes and Maximum Power Point Tracking (MPPT) capabilities at the module level. These smart devices can mitigate the impact of partial shading and soiling, which can cause power losses exceeding 20% in standard string inverter systems. Furthermore, the integration of monitoring and diagnostics features is gaining traction, allowing for real-time performance data and early fault detection. This trend is accelerating as module power ratings continue to climb, with many new utility-scale projects deploying panels exceeding 600W, necessitating junction boxes capable of handling higher currents up to 25A while maintaining superior heat dissipation to ensure long-term reliability and safety.

Other Trends

Material Innovation and Miniaturization

Concurrent with the push for smarter functionality is a strong trend towards material innovation and component miniaturization. Manufacturers are increasingly adopting advanced engineering plastics and composite materials that offer superior UV resistance, flame retardancy (achieving UL94 V-0 ratings), and higher Comparative Tracking Index (CTI) values above 600V to ensure long-term durability in harsh environmental conditions. The market is also seeing a pronounced move towards lead-free and halogen-free potting materials in response to stringent international environmental regulations and customer demand for greener products. This focus on material science is crucial because the junction box is a critical point of potential failure; for instance, moisture ingress can lead to rapid performance degradation. Alongside material advances, the physical design of junction boxes is becoming more compact and integrated, reducing their footprint on the panel to minimize shading and allow for more efficient cell layout, which is particularly important for the adoption of newer cell technologies like shingled and half-cut modules.

Expansion of Bifacial Module Deployment Driving Product Evolution

The rapid expansion of bifacial solar module deployment is acting as a powerful catalyst for specialized junction box design and innovation. Bifacial modules, which capture light from both sides, can increase energy generation by up to 30% compared to monofacial panels, but they present unique challenges for junction box placement and design. To avoid blocking rear-side irradiance, there is a growing demand for low-profile and corner-mounted junction boxes. This design shift requires re-engineering for mechanical stability, weatherproofing, and thermal management. Moreover, the electrical characteristics differ, as the current output can be higher and more variable. This necessitates junction boxes with robust diodes and connectors capable of handling these fluctuating parameters without compromising performance or safety. The proliferation of bifacial technology, which accounted for over 40% of new utility-scale project capacity in some regions last year, is therefore creating a distinct and fast-growing sub-segment within the broader junction box market, pushing manufacturers to develop products specifically tailored to this application.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Global Expansion to Secure Market Position

The global PV junction box market exhibits a fragmented yet dynamic competitive structure, characterized by a mix of established multinational corporations and numerous specialized regional manufacturers. While the top five players collectively hold approximately 25% of the market share, the remaining portion is distributed among a wide array of competitors, particularly from China, which dominates production with about 50% of the global output. This fragmentation drives intense competition on both price and technological features, with companies continuously innovating to enhance product reliability, weather resistance, and efficiency.

TE Connectivity stands as a prominent global player, leveraging its extensive expertise in electrical components and strong distribution networks across North America and Europe. The company’s market position is reinforced by its commitment to research and development, resulting in advanced junction box designs that offer superior durability and performance in diverse environmental conditions. Similarly, Amphenol maintains significant market influence through its robust product portfolio and strategic focus on high-reliability applications, particularly in the utility-scale solar segment which constitutes the largest application area.

Chinese manufacturers, including ZJRH, Tonglin, and GZX, collectively command substantial market presence due to their cost-competitive manufacturing capabilities and strong domestic supply chain integration. These companies have been progressively enhancing their product quality and international certification compliance to expand beyond the Asian market, where they already hold considerable sway. Their growth is further propelled by the massive domestic solar installation base and government support for renewable energy infrastructure.

Meanwhile, European specialists such as Stäubli Electrical Connectors and Kostal are strengthening their positions through technological differentiation and focus on high-value market segments. These companies invest significantly in developing proprietary connection technologies that reduce installation time and improve system safety, catering especially to the demanding requirements of commercial and utility projects in Europe and North America.

Additionally, several players are actively pursuing growth through strategic initiatives such as geographical expansion into emerging solar markets, new product launches featuring higher current ratings and smart monitoring capabilities, and strategic partnerships with major solar panel manufacturers. Because the junction box is a critical safety component, companies that can demonstrate superior product reliability, compliance with international standards, and strong technical support tend to gain preferential supplier status with large module producers, creating a competitive environment where quality and service are as important as price.

List of Key PV Junction Box Companies Profiled

- TE Connectivity (Switzerland)

- Amphenol (U.S.)

- ZJRH (China)

- Tonglin Technology Co., Ltd. (China)

- GZX (China)

- Jinko Solar (China)

- Stäubli Electrical Connectors (Switzerland)

- Kostal (Germany)

- Bizlink (U.S.)

- Shoals Technologies Group (U.S.)

- Linyang Energy (China)

- Yukita Electric Co., Ltd. (Japan)

- Hosiden Corporation (Japan)

- Sunter (China)

- Dongguan Zerun (China)

Segment Analysis:

By Type

Non-Potting PV Junction Box Segment Dominates the Market Due to Superior Heat Dissipation and Cost-Effectiveness

The market is segmented based on type into:

- Potting PV Junction Box

- Non-Potting PV Junction Box

By Application

Utility Segment Leads Due to Massive Scale Solar Farm Deployments Globally

The market is segmented based on application into:

- Residential

- Commercial

- Utility

By Diode Configuration

3 Diode Configuration Gains Traction for Enhanced Module Reliability and Mismatch Tolerance

The market is segmented based on diode configuration into:

- 2 Diode

- 3 Diode

- 4 Diode

- Others

By Material

PPO and PPS Materials Preferred for High Thermal Resistance and Long-Term Durability

The market is segmented based on material into:

- PPO (Polyphenylene Oxide)

- PPS (Polyphenylene Sulfide)

- Other Engineering Plastics

Regional Analysis: PV Junction Box Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the PV junction box market, accounting for approximately 50% of the total global market share, a dominance primarily driven by China. This leadership is anchored in the country’s position as the world’s largest manufacturer of solar panels, with massive domestic demand and export-oriented production. Government initiatives, such as China’s 14th Five-Year Plan which targets 1,200 GW of renewable capacity by 2030, create a powerful and sustained demand for all PV components, including junction boxes. While cost-competitive, non-potting junction boxes remain prevalent due to the scale of utility-scale projects, there is a notable and accelerating shift towards more advanced, high-efficiency, and reliable potting-type boxes. This trend is fueled by the need for enhanced durability in harsh environments and improving module performance standards. Other key markets in the region, including India, Japan, and Southeast Asian nations, are also experiencing robust growth, supported by ambitious national solar targets and increasing foreign investment in local manufacturing hubs.

North America

The North American market, holding roughly 15% of the global share, is characterized by a strong emphasis on quality, reliability, and compliance with stringent technical standards. Demand is heavily influenced by the U.S. Inflation Reduction Act, which has unleashed significant investment into domestic solar manufacturing and deployment. This policy environment prioritizes supply chain resilience and high-performance products, benefiting established international players and fostering local production. The market exhibits a higher penetration of advanced potting junction boxes, which are favored for their superior weather resistance and long-term performance guarantees, crucial for both large-scale utility projects and the growing residential solar sector. While the market is competitive, it is also innovation-driven, with a focus on developing smart junction boxes integrated with monitoring technologies to enhance system-level management and safety.

Europe

Europe also commands approximately 15% of the global PV junction box market, with growth propelled by the EU’s ambitious REPowerEU plan aiming to rapidly reduce reliance on fossil fuels. This has accelerated solar adoption across member states, creating a steady demand for high-quality components. The European market is particularly stringent regarding product certifications, safety standards (e.g., IEC 62790), and environmental regulations, which strongly favors established suppliers with proven track records of compliance and innovation. There is a pronounced demand for robust and durable junction boxes capable of withstanding diverse climatic conditions, from the Nordic cold to Mediterranean heat. Sustainability and the entire product lifecycle are key purchasing criteria, leading to innovations in recyclable materials and designs for easier end-of-life disassembly. Germany, Spain, and the Netherlands are among the most active national markets within the region.

South America

The South American market for PV junction boxes is in a growth phase, presenting significant long-term opportunities driven by the region’s abundant solar resources and increasing energy needs. Countries like Brazil and Chile are leading the charge with numerous large-scale solar auctions and projects coming online. However, the market is highly cost-sensitive, which often leads to a preference for standard, non-potting junction box solutions, especially in utility-scale applications. The development of a local manufacturing base is still nascent, leading to a heavy reliance on imports, primarily from Asia. Market growth can be intermittent, as it is often susceptible to local economic volatility and shifting political priorities. Nevertheless, the fundamental drivers of rising electricity demand and competitive solar energy costs ensure a positive outlook for future expansion.

Middle East & Africa

The Middle East and Africa region represents an emerging but high-potential market for PV junction boxes. The Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the UAE, are deploying gigawatt-scale solar projects as part of broader economic diversification plans, such as Saudi Vision 2030. These mega-projects require vast quantities of reliable junction boxes capable of performing in extreme desert heat and dust. In contrast, parts of Africa are seeing growth driven more by off-grid and mini-grid solutions aimed at increasing electricity access. Across the region, the market is challenged by a price-competitive landscape and a need for products that offer a balance between cost and extreme environmental durability. While the market is currently smaller in volume compared to other regions, its growth trajectory is among the steepest globally, attracting significant attention from international suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional PV Junction Box markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PV Junction Box Market?

-> PV Junction Box Market was valued at 1195 million in 2024 and is projected to reach US$ 1969 million by 2032, at a CAGR of 7.6% during the forecast period.

Which key companies operate in Global PV Junction Box Market?

-> Key players include ZJRH, Jinko, Tonglin, GZX, and TE Connectivity, among others.

What are the key growth drivers?

-> Key growth drivers include global expansion of solar energy infrastructure, supportive government policies for renewable energy, and increasing demand for efficient and reliable PV components.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China alone holding approximately 50% of the global market share.

What are the emerging trends?

-> Emerging trends include development of smart junction boxes with integrated monitoring capabilities, use of advanced materials for improved heat dissipation, and miniaturization of components for higher power density panels.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...