Printed Electronics Materials Market Insights

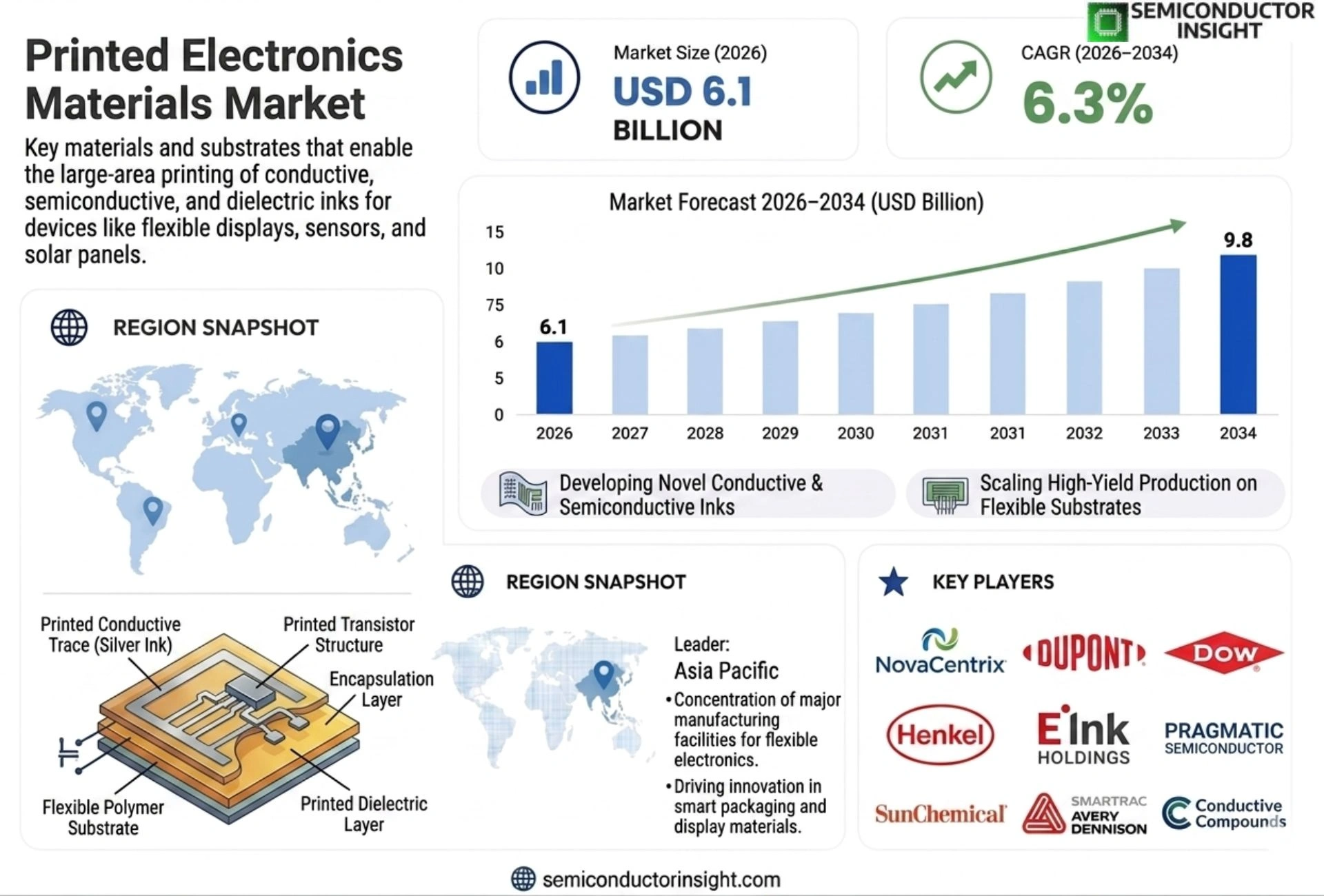

Global Printed Electronics Materials Market size was valued at USD 5.2 billion in 2025. The market is projected to grow from USD 6.1 billion in 2026 to USD 9.8 billion by 2034, exhibiting a CAGR of approximately 6.3% during the forecast period.

Printed electronics materials encompass conductive inks, dielectric polymers, substrates, and functional coatings that enable the fabrication of flexible circuits, sensors, displays, and RFID tags through additive manufacturing techniques such as inkjet, screen printing, and aerosol jet printing.

The market is experiencing rapid growth because demand for lightweight, low‑cost smart devices is rising across consumer electronics, automotive, and healthcare sectors. Furthermore, advancements in nanomaterial formulations improve conductivity and durability, while sustainability pressures drive adoption of recyclable substrates. Key players,including DuPont™, Merck KGaA, Fujifilm Holdings Corp., and Nano Dimension Ltd.,are expanding portfolios through strategic partnerships and R&D investments.

MARKET DRIVERS

Growing Demand for Lightweight Consumer Electronics

The surge in wearable devices, flexible displays, and IoT sensors is driving manufacturers to adopt printed electronics solutions that reduce weight and improve form‑factor flexibility. Printed Electronics Materials Market players are benefiting from this shift as end‑users prioritize thin, bendable components over traditional rigid circuits.

Advancements in Inkjet and Aerosol Printing Technologies

Recent breakthroughs in high‑resolution inkjet heads and low‑temperature aerosol deposition have expanded the printable substrate range to include plastics, paper, and textiles. These technological gains lower production costs and enable high‑volume manufacturing, further accelerating market growth.

➤ Integration of conductive polymers and nano‑metal inks is shortening product development cycles, allowing companies to launch new printed electronic solutions within 12‑18 months instead of the traditional 24‑36 month timeline.

Combined, these drivers are expected to push the global market revenue upward, with double‑digit compound annual growth rates projected for the next five years.

MARKET CHALLENGES

High Capital Expenditure for Production Lines

Establishing a dedicated printed electronics fabrication line requires significant investment in specialized printers, curing ovens, and quality‑control equipment. Smaller firms often face financing constraints, limiting their ability to scale operations quickly.

Other Challenges

Material Compatibility Issues

The need to match ink rheology with diverse substrates creates engineering complexity. Inconsistent adhesion or conductivity can lead to yield losses and increase quality assurance costs.

Regulatory compliance for environmentally hazardous solvents also adds to operational overhead, especially in regions with strict emissions standards.

MARKET RESTRAINTS

Limited Standardization Across Supply Chains

Without industry‑wide standards for ink formulations, substrate preparation, and printing parameters, interoperability remains fragmented. This lack of uniformity hampers large‑scale adoption, as manufacturers must develop bespoke processes for each new application.

The fragmented testing protocols also increase time‑to‑market, as products undergo multiple rounds of validation before they can be commercialized.

MARKET OPPORTUNITIES

Expansion into Automotive and Aerospace Sectors

Lightweight, low‑power printed circuitry offers compelling benefits for vehicle interior sensors, flexible wiring harnesses, and aircraft health‑monitoring systems. Printed Electronics Materials Market suppliers that can certify material reliability under extreme temperature and vibration conditions are poised to capture a sizable share of this emerging demand.

Additionally, the rise of smart packaging and biodegradable printed tags presents a near‑term growth avenue, leveraging sustainability trends while delivering functional performance.

Printed Electronics Materials Market Trends

Shift Toward Sustainable Substrates

Printed Electronics Materials Market is experiencing a pronounced shift toward recyclable and bio‑based substrates. Manufacturers are transitioning from conventional PET to cellulose‑derived films and polymer blends that retain flexibility while meeting circular‑economy criteria. This movement is driven by stricter waste‑management regulations in Europe and growing consumer preference for green electronics. Suppliers have introduced low‑temperature curing processes that reduce energy consumption, allowing roll‑to‑roll production on renewable feedstocks. Cost differentials have narrowed as scale improves, and the availability of locally sourced agricultural fibers mitigates reliance on petrochemical imports. This alignment of environmental policy and economic feasibility accelerates adoption across consumer and industrial segments.

Other Trends

Advancements in Conductive Ink Formulations

Recent innovations in nanomaterial dispersions have boosted the conductivity of inkjet‑compatible inks while enhancing shelf life. Silver nanowire and copper nanoparticle inks now achieve bulk‑metal resistivity at printing temperatures compatible with flexible polymers. At the same time, water‑based binders reduce volatile organic compound emissions, supporting stricter workplace safety standards. These technical gains enable finer line widths and higher component densities, expanding the design space for wearable sensors and IoT tags. Companies are leveraging proprietary surfactant systems to balance viscosity and droplet formation, resulting in more reliable large‑area printing runs and lower material waste.

Integration Across Automotive and Healthcare

Automotive manufacturers are embedding printed circuitry into interior panels and under‑hood components to lower weight and simplify assembly. The technology supports real‑time diagnostics and over‑the‑air updates without extensive wiring harnesses. In healthcare, printed biosensors on flexible substrates provide continuous monitoring of vital signs, offering a low‑cost alternative to traditional rigid devices. Both sectors benefit from the thin‑film form factor and the ability to integrate directly onto existing polymer parts. As supply chains mature and qualification processes streamline, adoption rates are expected to rise, reinforcing Printed Electronics Materials Market’s role as an enabling platform for next‑generation smart products.

COMPETITIVE LANDSCAPE

Key Industry Players

Printed Electronics Materials Market , Competitive Dynamics, Strategic Positioning, and Leading Manufacturer Profiles

Printed electronics materials market is characterized by the presence of a diversified mix of large multinational chemical and materials corporations alongside specialized technology-driven firms. DuPont de Nemours, Inc. remains one of the most prominent forces in this space, leveraging its extensive portfolio of conductive inks, functional pastes, and dielectric materials tailored for flexible electronics and RFID applications. Merck KGaA commands a strong position through its advanced functional materials division, supplying organic semiconductors and specialty coatings that serve display and sensor manufacturing segments. Fujifilm Holdings Corporation applies its deep expertise in precision chemical formulations to deliver high-performance inkjet-printable electronic inks, reinforcing its competitiveness across both consumer electronics and industrial printing platforms. The competitive intensity across the market is further elevated by continuous R&D investments, portfolio diversification strategies, and a growing emphasis on nanomaterial-based conductive formulations that offer superior conductivity and mechanical durability for next-generation printed circuit applications.

Beyond the tier-one incumbents, several niche yet strategically significant players are shaping the competitive contours of Printed Electronics Materials Market. Nano Dimension Ltd. has carved out a differentiated position through its focus on additive manufacturing systems and proprietary conductive and dielectric inks designed for multi-layer printed electronics. Henkel AG & Co. KGaA contributes robust competition through its LOCTITE range of electrically conductive adhesives and inks widely adopted in automotive and healthcare electronics. Sun Chemical Corporation, a subsidiary of DIC Corporation, offers an extensive line of functional printing materials including silver and carbon-based conductive inks. Agfa-Gevaert Group, Heraeus Holding GmbH, and Creative Materials Incorporated are also recognized contributors to substrate coatings, photovoltaic pastes, and specialty ink formulations. Meanwhile, Vorbeck Materials, Applied Ink Solutions, Novacentrix, and Intrinsiq Materials continue to advance graphene-based and copper nanoparticle ink technologies that address cost reduction and recyclability requirements increasingly demanded by sustainability-conscious manufacturers across global supply chains.

List of Key Printed Electronics Materials Companies Profiled

- DuPont de Nemours, Inc.

- Merck KGaA

- Fujifilm Holdings Corporation

- Nano Dimension Ltd.

- Henkel AG & Co. KGaA

- Sun Chemical Corporation

- Agfa-Gevaert Group

- Heraeus Holding GmbH

- Novacentrix

- Creative Materials Incorporated

- Vorbeck Materials Corp.

- Applied Ink Solutions

- Intrinsiq Materials Inc.

- Carestream Advanced Materials

- Inkron Oy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Conductive Inks are recognized as the primary driver because they enable low‑resistance pathways for flexible circuits.

|

| By Application |

|

Wearable Sensors dominate due to the surge in health‑monitoring and IoT wearables.

|

| By End User |

|

Consumer Electronics are the leading end‑user segment, reflecting the appetite for lightweight, thin and customizable devices.

|

| By Technology |

|

Inkjet Printing is identified as the most flexible technology, supporting high‑resolution patterns and multi‑material deposition.

|

| By Industry |

|

Smart Textiles are emerging as a high‑potential arena where printed electronics embed functionality directly into fabrics.

|

Regional Analysis: North America

The market for flexible circuits and RFID tags in the US is experiencing substantial growth, catering to the increasing demand for smart packaging, asset tracking, and wearable technologies.

The demand for conductive inks and pastes is being driven by the proliferation of printed electronics applications, particularly in flexible displays and solar cells.

The need for high-quality substrates and adhesives is crucial for the successful manufacturing of printed electronics devices.

The increasing adoption of polymer materials in printed electronics is being driven by their flexibility, lightweight properties, and cost-effectiveness.

Europe

Europe represents a significant market for Printed Electronics Materials, with a strong emphasis on innovation and sustainability. The region’s advanced manufacturing capabilities and supportive government policies are fostering growth in this sector. Key applications include smart textiles, wearable electronics, and flexible sensors. The European market is also witnessing increasing adoption of eco-friendly materials and processes, aligning with the region’s commitment to environmental responsibility. The consistent investment in R&D across European nations positions them as innovators in printing electronics materials.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing market for Printed Electronics Materials, driven by rapid industrialization and the expansion of electronics manufacturing in countries like China, Japan, and South Korea. The growing demand for flexible displays, wearable devices, and IoT devices is fueling the adoption of printed electronics in this region. China, in particular, is a major consumer and producer of printed electronics materials, benefiting from substantial government support and a thriving electronics industry. The cost-effectiveness of printed electronics manufacturing is also attracting significant investment in Asia-Pacific.

South America

Printed Electronics Materials Market in South America is showing steady growth, particularly in Brazil and Mexico. The increasing adoption of printed electronics in sectors such as agriculture, healthcare, and consumer goods is driving this growth. The region’s growing middle class and rising disposable incomes are also contributing to the demand for printed electronics applications. Limited local manufacturing capabilities mean reliance on imports, presenting both opportunities and challenges for regional players.

Middle East & Africa

The Middle East & Africa region presents a high-growth potential for Printed Electronics Materials Market. Increased investment in infrastructure, healthcare, and smart city initiatives is driving demand for printed electronics applications. The region’s expanding consumer electronics market and growing adoption of IoT devices are also contributing to market growth. While currently a smaller market compared to other regions, the potential for expansion is significant, particularly with continued economic development and technological advancements.

Report Scope

This market research report provides a comprehensive analysis of the Printed Electronics Materials Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Printed Electronics Materials Market?

-> Printed Electronics Materials Market was valued at USD 5.2 billion in 2025 and is expected to reach USD 9.8 billion by 2034.

Which key companies operate Printed Electronics Materials Market?

-> Key players include DuPont™, Merck KGaA, Fujifilm Holdings Corp., and Nano Dimension Ltd.

What are the key growth drivers?

-> Key growth drivers include demand for lightweight, low‑cost smart devices across consumer electronics, automotive, and healthcare sectors; advancements in nanomaterial formulations that improve conductivity and durability; and sustainability pressures driving the adoption of recyclable substrates.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include conductive inks, dielectric polymers, flexible substrates, and functional coatings that enable the fabrication of flexible circuits, sensors, displays, and RFID tags through additive manufacturing techniques such as inkjet, screen printing, and aerosol jet printing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...