MARKET INSIGHTS

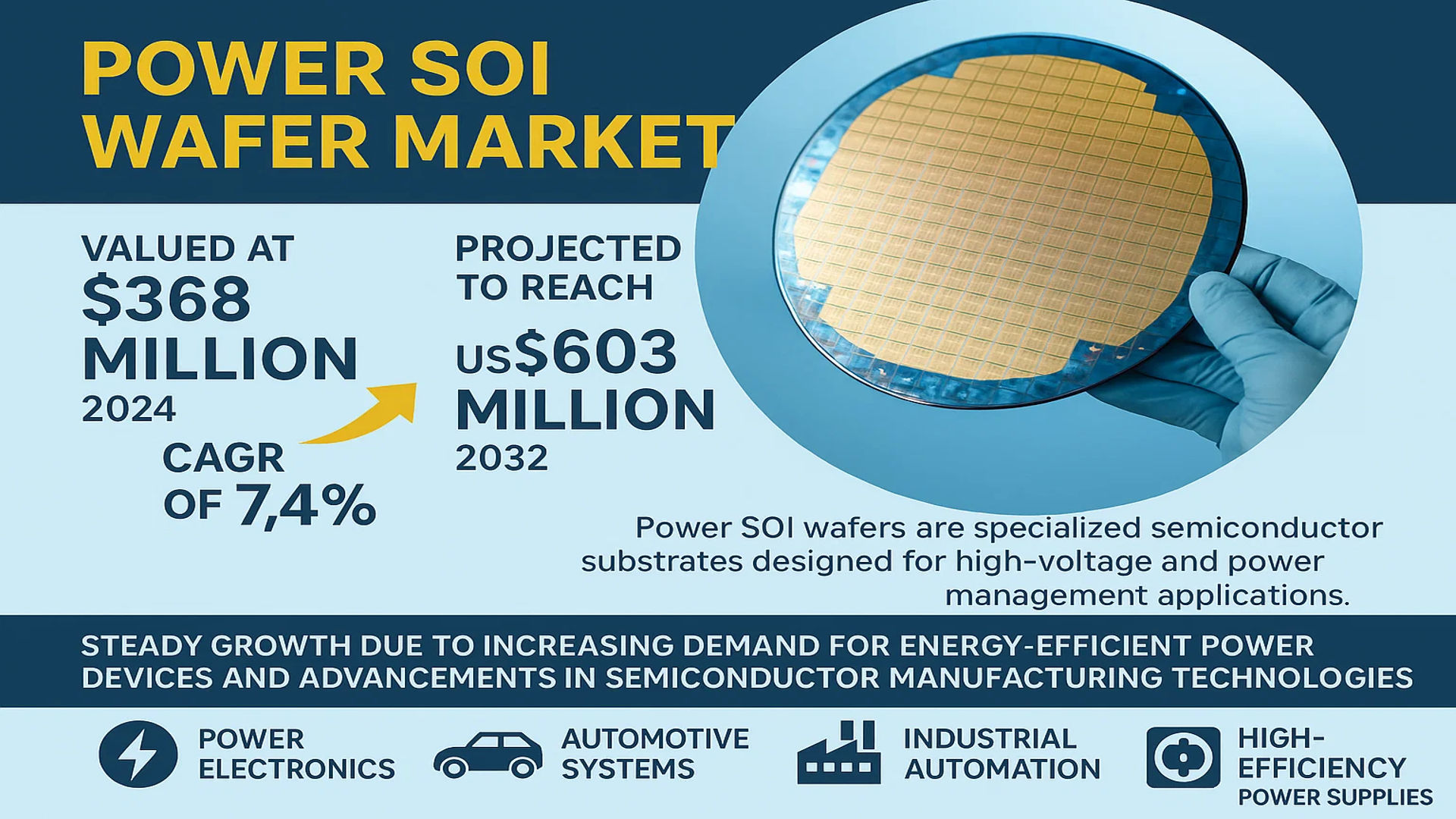

The global Power SOI wafer Market was valued at 368 million in 2024 and is projected to reach US$ 603 million by 2032, at a CAGR of 7.4% during the forecast period.

Power SOI wafers are specialized semiconductor substrates designed for high-voltage and power management applications. These wafers leverage silicon-on-insulator (SOI) technology to enhance energy efficiency, thermal performance, and electrical isolation, making them critical components in power electronics, automotive systems, industrial automation, and high-efficiency power supplies.

The market is experiencing steady growth due to increasing demand for energy-efficient power devices and advancements in semiconductor manufacturing technologies. The automotive sector, particularly electric vehicles (EVs), is a key driver, as Power SOI wafers enable higher power density and reliability in EV power modules. Furthermore, industrial automation and renewable energy applications are contributing to market expansion, with the 150mm and below segment expected to witness significant growth. Leading manufacturers such as Soitec, Shin-Etsu, and SUMCO dominate the market, leveraging their technological expertise to meet rising demand.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Energy-Efficient Semiconductor Solutions to Fuel Power SOI Wafer Adoption

The global push towards energy efficiency across industries is driving significant demand for Power Silicon-on-Insulator (SOI) wafers. These substrates offer superior electrical isolation and reduced power consumption compared to conventional silicon wafers, making them ideal for power management applications. The automotive sector’s electrification trend is particularly impactful, with Power SOI wafers enabling more efficient power conversion in hybrid and electric vehicles. As governments worldwide implement stricter energy efficiency regulations, semiconductor manufacturers are increasingly adopting SOI technology to meet these requirements while maintaining performance.

Expansion of 5G and IoT Infrastructure to Accelerate Market Growth

The rapid deployment of 5G networks and IoT devices creates substantial opportunities for Power SOI wafer manufacturers. These wafers are critical for radio frequency (RF) power amplifiers in 5G base stations, offering better thermal management and signal integrity. As telecom operators invest billions annually to expand 5G coverage, the demand for high-performance RF components built on Power SOI substrates continues to rise. Additionally, the proliferation of smart devices and industrial IoT applications drives need for energy-efficient power management ICs, many of which utilize SOI technology for its low leakage characteristics.

Automotive Industry Transformation to Drive Long-Term Demand

The automotive sector’s transition toward electrification and advanced driver-assistance systems (ADAS) presents a major growth opportunity for Power SOI wafers. These substrates enable higher voltage operation and better thermal performance in power electronics for electric vehicles, addressing key challenges in vehicle electrification. With the global electric vehicle market projected to maintain double-digit growth rates through 2030, automotive applications will remain a crucial driver for SOI wafer adoption. Furthermore, the increasing complexity of in-vehicle electronics and demand for reliable high-voltage components in autonomous driving systems further reinforces this growth trajectory.

MARKET RESTRAINTS

High Manufacturing Costs to Limit Market Penetration

Power SOI wafer production involves complex manufacturing processes that require specialized equipment and stringent quality control measures. The additional fabrication steps needed for creating buried oxide layers and handling thin silicon films lead to significantly higher costs compared to conventional silicon wafers. These elevated prices can deter adoption in price-sensitive applications and emerging markets, particularly when conventional alternatives provide adequate performance. While costs have decreased over time through process optimizations, the price premium remains a substantial barrier for many potential users.

Other Restraints

Supply Chain Vulnerabilities

The Power SOI wafer market faces constraints from concentrated supply chains, with few manufacturers capable of producing high-quality substrates at scale. This concentration creates vulnerabilities to disruptions, as seen during recent semiconductor shortages. Additionally, the specialized nature of SOI wafer production limits the ability to quickly ramp up capacity during demand surges.

Design Complexity

Migrating from conventional silicon to SOI technology requires significant redesign of semiconductor devices and manufacturing processes. This transition demands specialized expertise and additional design verification, increasing development costs and time-to-market for new products. The learning curve associated with SOI design can deter some manufacturers from adopting the technology.

MARKET CHALLENGES

Technical Hurdles in Large-Diameter Wafer Production to Constrain Market Expansion

While the industry continues transitioning toward larger wafer diameters for improved manufacturing efficiency, Power SOI wafer producers face significant technical challenges in scaling beyond 200mm. The process of creating defect-free buried oxide layers becomes increasingly difficult as wafer sizes grow, with yield and uniformity issues rising substantially at 300mm scales. These production challenges have limited the availability of large-diameter Power SOI wafers, constraining their adoption in high-volume manufacturing where 300mm substrates have become standard.

Other Challenges

Material Innovation Competition

Power SOI technology faces growing competition from alternative wide bandgap materials like silicon carbide (SiC) and gallium nitride (GaN) in high-power applications. While SOI maintains advantages in integration and cost for certain applications, these emerging materials offer superior performance in high-voltage, high-temperature environments, potentially limiting SOI market growth in specific segments.

Standardization Gaps

The lack of universal standards for Power SOI wafer specifications and characterization methods creates challenges for broad industry adoption. Variations in wafer properties between manufacturers can complicate device design and qualify processes, requiring additional customization and testing.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy to Create New Growth Avenues

The global transition toward renewable energy systems presents significant opportunities for Power SOI wafer adoption. These substrates are increasingly used in power conversion and management systems for solar inverters and wind turbines, where their high-voltage tolerance and efficiency advantages provide meaningful benefits. As renewable energy installations continue expanding globally, demand for advanced power semiconductor solutions will grow accordingly. Power SOI technology is particularly well-suited for next-generation smart grid applications, where it enables more efficient power distribution and conversion in increasingly complex electrical networks.

Advancements in SOI Fabrication Technology to Expand Addressable Market

Recent innovations in SOI manufacturing processes are creating opportunities to reduce costs and improve performance. Advances in wafer bonding techniques and implantation processes enable production of higher quality Power SOI wafers with better thickness uniformity and defect control. These improvements expand potential applications to include more demanding automotive and industrial uses where reliability is critical. Additionally, ongoing research into alternative substrate materials and engineered wafers with specialized properties may open new market segments for Power SOI technology in coming years.

Strategic Collaborations to Accelerate Market Development

The Power SOI wafer ecosystem is witnessing increased collaboration between substrate suppliers, foundries, and device manufacturers to develop optimized solutions. These partnerships aim to create end-to-end solutions that simplify adoption for system designers while improving performance and yield. Such collaborations are particularly valuable for addressing application-specific challenges in automotive and industrial power electronics, where complete solution offerings can significantly reduce customer development risks and time-to-market.

POWER SOI WAFER MARKET TRENDS

Rising Demand for Energy-Efficient Power Electronics Drives Market Growth

The global Power Silicon-on-Insulator (SOI) wafer market is experiencing robust growth, primarily driven by the rising demand for energy-efficient power electronics across industries. Power SOI wafers offer superior electrical isolation, reduced power loss, and enhanced thermal management compared to conventional bulk silicon wafers. These advantages make them indispensable in high-voltage applications, where efficiency and reliability are paramount. The automotive sector, particularly electric vehicles (EVs), represents a key growth driver, with demand increasing at a compound annual growth rate (CAGR) of over 8%.

Other Trends

Expansion in Industrial Automation and Smart Grid Technologies

Industrial automation and smart grid technologies are significantly boosting the adoption of Power SOI wafers. These wafers enhance the performance of power management ICs (PMICs), motor controllers, and converters used in industrial settings. The shift towards Industry 4.0 and IoT-enabled devices has further accelerated the need for advanced semiconductor substrates. As governments worldwide invest in smart energy grids to improve efficiency, the demand for high-performance Power SOI solutions is projected to grow substantially.

Technological Advancements and Miniaturization

Technological advancements in fabrication processes are enabling the production of thinner and more efficient Power SOI wafers, catering to the trend of semiconductor miniaturization. Leading manufacturers are investing in R&D to develop 300mm SOI wafers, which offer higher cost-efficiency and yield. Innovations in bonding techniques and substrate materials are also improving wafer performance, making them suitable for next-generation power devices. The increasing adoption of AI and 5G technologies necessitates high-speed, low-power semiconductor components, further fueling the market.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansions Drive Market Dominance

The global Power SOI wafer market displays a moderately consolidated structure, with established semiconductor leaders and specialized manufacturers competing aggressively for market share. Soitec emerges as a dominant force in this space, leveraging its proprietary SmartCut™ technology that delivers superior wafer quality while optimizing production efficiency. The company maintains strong partnerships with automotive and industrial customers, reinforcing its market position.

Japanese conglomerate Shin-Etsu commands significant influence through its vertically integrated operations, ranging from silicon crystal growth to finished wafer production. Similarly, SUMCO Corporation capitalizes on its manufacturing scale and technological expertise to serve high-voltage power applications. Both companies benefit from Asia’s thriving semiconductor ecosystem, though they face intensifying competition from Chinese manufacturers making rapid technological advancements.

Mid-sized players like GlobalWafers and NSIG (Okmetic) pursue differentiated strategies to carve out market niches. GlobalWafers has been expanding its 200mm SOI wafer production capacity to meet growing demand for industrial power modules, while NSIG focuses on customized wafer solutions for military and aerospace applications where performance requirements are exceptionally stringent.

The competitive dynamics continue evolving as emerging Chinese manufacturers such as Shanghai Advanced Silicon Technology and Zhonghuan Advanced aggressively expand their SOI wafer capabilities. Backed by government semiconductor initiatives and domestic procurement policies, these companies are gradually penetrating global supply chains, although quality consistency remains a work in progress compared to established players.

List of Key Power SOI Wafer Companies Profiled

- Soitec (France)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- SUMCO Corporation (Japan)

- GlobalWafers Co., Ltd. (Taiwan)

- NSIG (Okmetic) (Finland)

- IceMos Technology (UK)

- Wafer Works Corporation (Taiwan)

- Shenyang Silicon Technology (China)

- Zhonghuan Advanced (China)

- Shanghai Advanced Silicon Technology (China)

- WaferPro (U.S.)

- SEIREN KST (Japan)

- PlutoSemi (China)

Segment Analysis:

By Type

150mm and Below Segment Dominates the Market Due to Cost-Effectiveness and High Adoption in Consumer Electronics

The market is segmented based on type into:

- 150mm and Below

- 200 mm

- 300 mm

By Application

Automotive Segment Leads Due to Increasing Demand for Electric Vehicles and Advanced Driver-Assistance Systems

The market is segmented based on application into:

- Automotive

- Industrial Control

- Grid and Energy

- Others

By Region

Asia Pacific Holds Major Share Due to Expanding Semiconductor Manufacturing Ecosystem

The market is segmented based on region into:

- North America

- Europe

- Asia Pacific

- South America

- Middle East & Africa

By Material

Silicon-on-Insulator (SOI) Segment Dominates with Superior Performance Characteristics

The market is segmented based on material into:

- Silicon-on-Insulator (SOI)

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Others

Regional Analysis: Power SOI Wafer Market

Asia-Pacific

The Asia-Pacific region dominates the Power SOI wafer market, accounting for the largest revenue share due to robust semiconductor manufacturing ecosystems in China, Japan, and South Korea. China’s aggressive investments in electric vehicles and renewable energy infrastructure have significantly increased demand for high-performance power electronics. Japan remains a technology leader with companies like Shin-Etsu and SUMCO advancing wafer fabrication techniques. Meanwhile, South Korea’s focus on industrial automation and consumer electronics drives steady adoption. Despite price sensitivity favoring 150mm and below wafers, the shift toward 200mm and 300mm SOI solutions is accelerating for automotive and grid applications.

North America

North America is a key innovator in Power SOI technology, with the U.S. spearheading R&D through partnerships between semiconductor firms and national labs. The CHIPS Act’s $52 billion funding pool is bolstering domestic wafer production capabilities, particularly for automotive and aerospace applications. Silicon Valley startups and established players like GlobalWafers are pioneering energy-efficient wafer designs to meet stringent EPA and DOE efficiency standards. The region shows strong preference for 300mm wafers in premium applications, though supply chain realignments post-pandemic continue to pose challenges.

Europe

Europe maintains a strong position in specialized Power SOI applications, particularly for industrial automation and smart grid technologies. EU directives on energy efficiency and the push for semiconductor sovereignty under the European Chips Act are driving local production. Germany’s automotive sector and France’s aerospace industry are primary consumers, with companies like Soitec leading in FD-SOI development. Strict environmental regulations favor advanced wafer solutions with lower thermal losses, though higher costs limit adoption in price-sensitive segments.

South America

The South American market shows emerging potential for Power SOI wafers, primarily driven by Brazil’s growing automotive electronics sector and Argentina’s renewable energy projects. However, limited local manufacturing infrastructure and dependence on imports constrain market growth. Most demand comes from multinational corporations operating in the region, with 150mm wafers dominating due to cost advantages. Government initiatives to develop local semiconductor capabilities could unlock future opportunities.

Middle East & Africa

This region represents a nascent but promising market, with the UAE and Saudi Arabia making strategic investments in power electronics infrastructure. Smart city initiatives and oil/gas industry modernization are creating demand for robust wafer solutions. While currently reliant on imports, regional players are exploring joint ventures with Asian and European wafer manufacturers. The market shows preference for mid-range 200mm wafers balancing performance and cost, with growth potential tied to energy sector diversification plans.

Report Scope

This market research report provides a comprehensive analysis of the global Power SOI wafer market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Power SOI wafer market was valued at USD 368 million in 2024 and is projected to reach USD 603 million by 2032, growing at a CAGR of 7.4% during the forecast period.

- Segmentation Analysis: Detailed breakdown by wafer size (150mm and below, 200mm, 300mm) and application (automotive, industrial control, grid & energy, others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Soitec, Shin-Etsu, SUMCO, GlobalWafers, and NSIG (Okmetic), covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging fabrication techniques, advanced power management solutions, and evolving industry standards for SOI wafers.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for energy-efficient power electronics and electric vehicles, along with challenges like high manufacturing costs.

- Stakeholder Analysis: Insights for semiconductor manufacturers, foundries, equipment suppliers, and investors regarding strategic opportunities in the Power SOI wafer ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Power SOI Wafer Market?

-> Power SOI wafer Market was valued at 368 million in 2024 and is projected to reach US$ 603 million by 2032, at a CAGR of 7.4% during the forecast period.

Which key companies operate in Global Power SOI Wafer Market?

-> Key players include Soitec, Shin-Etsu, SUMCO, GlobalWafers, NSIG (Okmetic), IceMos Technology, Wafer Works Corporation, and Shenyang Silicon Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for electric vehicles, expansion of industrial automation, and increasing adoption of energy-efficient power management solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by semiconductor manufacturing expansion in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of 300mm Power SOI wafers, integration with advanced packaging technologies, and increasing use in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...