MARKET INSIGHTS

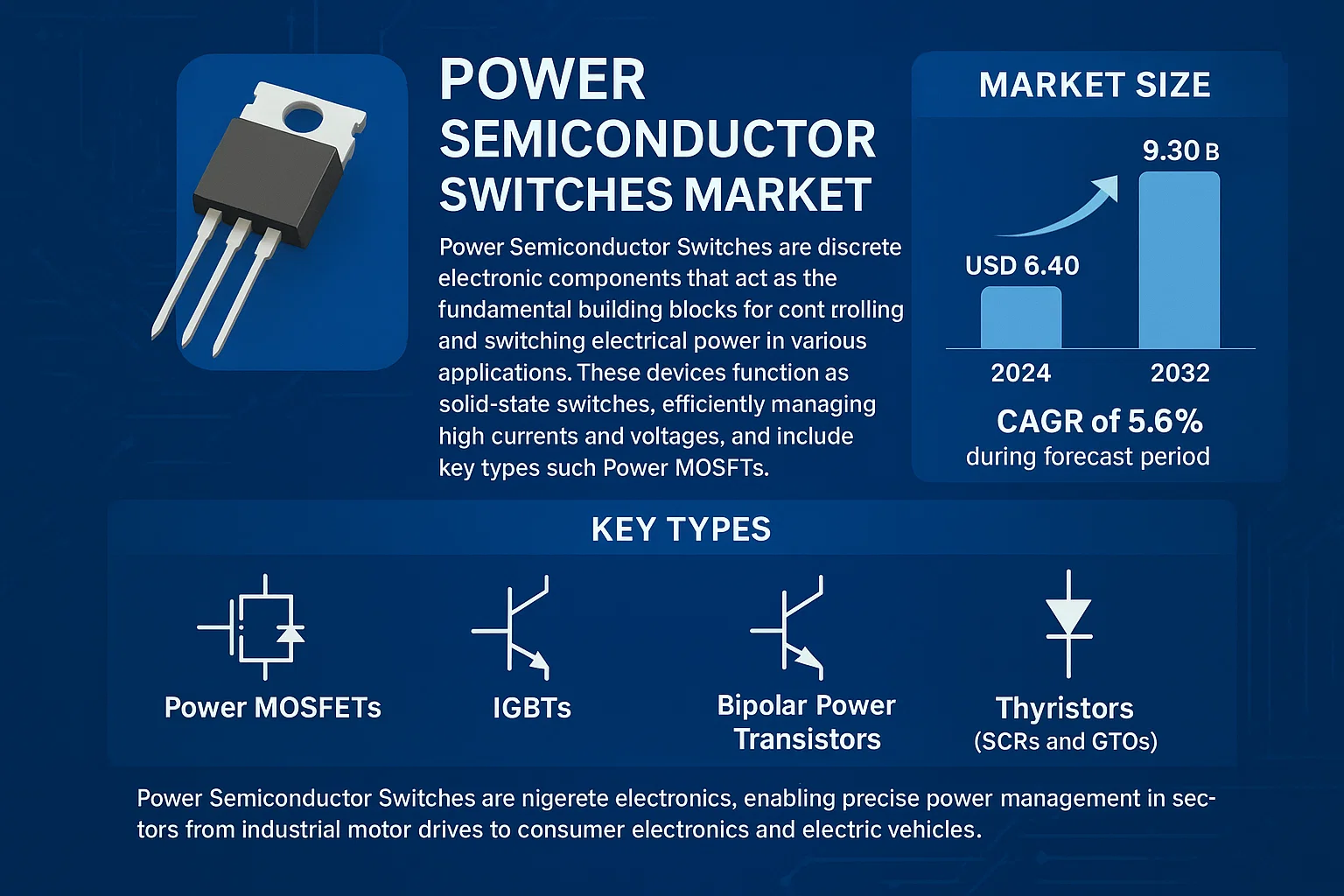

Global Power Semiconductor Switches Market size was valued at USD 6.40 billion in 2024 to USD 9.30 billion by 2032, exhibiting a CAGR of 5.6% during the forecast period.

Power Semiconductor Switches are discrete electronic components that act as the fundamental building blocks for controlling and switching electrical power in a vast array of applications. These devices function as solid-state switches, efficiently managing high currents and voltages, and include key types such as Power MOSFETs, IGBTs (Insulated-Gate Bipolar Transistors), Bipolar Power Transistors, and Thyristors (including SCRs and GTOs). They are indispensable in modern electronics, enabling precise power management in sectors from industrial motor drives to consumer electronics and electric vehicles.

The market’s steady growth is primarily driven by the global push towards electrification and energy efficiency. The rapid expansion of the electric vehicle (EV) industry, which relies heavily on these components for powertrains and charging infrastructure, is a major catalyst. Furthermore, the increasing automation in industrial processes and the relentless growth of renewable energy systems, which require sophisticated power conversion, are significant contributors. The market is highly concentrated, with the top four manufacturers—Infineon Technologies AG, ON Semiconductor, STMicroelectronics N.V., and Toshiba Corporation—collectively holding over 35% of the global market share. Geographically, China dominates as the largest consumer, accounting for nearly 50% of the global demand, fueled by its massive manufacturing base and strong government support for EVs and industrial automation.

MARKET DRIVERS

Rising Demand in Automotive and Industrial Sectors

The rapid electrification of vehicles and industrial automation systems has significantly increased the demand for efficient power management components. Power Semiconductor Switches are critical in controlling power flow in electric vehicles, industrial motors, and power supplies, driving market growth through increased adoption in these high-growth sectors.

Growth in Renewable Energy Infrastructure

Global investments in renewable energy infrastructure, particularly in solar and wind power generation, require sophisticated power conversion and control systems. Power Semiconductor Switches enable efficient energy conversion and grid stability, making them essential components in inverters, converters, and power conditioning units across renewable energy projects worldwide.

➤ The shift toward Industry 4.0 and smart manufacturing has accelerated the integration of power electronics in automated systems. This trend is particularly strong in emerging economies where industrial modernization programs are being implemented, further driving demand for advanced power semiconductor components.

Additionally, the increasing complexity of power management in data centers and telecommunications infrastructure has created new demand vectors for high-efficiency switches. The need for energy-efficient solutions in these sectors aligns with global sustainability goals, creating a virtuous cycle of demand and innovation in the power semiconductor space.

MARKET CHALLENGES

Supply Chain Constraints and Material Shortages

The global semiconductor industry has faced significant supply chain disruptions since 2020, affecting the availability of raw materials and components essential for power semiconductor manufacturing. These constraints have particularly affected specialty materials like silicon carbide and gallium nitride, which are crucial for advanced power switches, leading to extended lead times and increased costs across the supply chain.

Other Challenges

Technological Complexity and Miniaturization Pressure

As power semiconductor devices become more advanced, manufacturers face increasing challenges in balancing performance with miniaturization. The need to pack more functionality into smaller form factors while maintaining thermal performance and reliability requires significant R&D investment and advanced manufacturing techniques that not all market participants can readily access.

MARKET RESTRAINTS

Economic Uncertainty and Investment Constraints

Global economic uncertainties and inflationary pressures have led to reduced capital expenditure in some sectors, particularly affecting industrial equipment procurement. This has temporarily slowed some large-scale deployments that would normally drive demand for power semiconductor components, though the long-term outlook remains strong due to fundamental drivers in electrification and digitalization.

MARKET OPPORTUNITIES

Electric Vehicle Revolution and Charging Infrastructure

The rapid transition to electric vehicles represents the largest growth opportunity for power semiconductor components. With major markets mandating the phase-out of internal combustion engines, the demand for power electronics in EVs and their charging infrastructure is projected to grow exponentially. This includes not just the vehicles themselves but also the nationwide and eventually global network of fast-charging stations, all requiring advanced power management solutions.

Power Semiconductor Switches Market Trends Rising Demand for Energy-Efficient Power Electronics Drives Market Growth

The global power semiconductor switches market is experiencing significant growth, primarily driven by the increasing demand for energy-efficient power conversion across industries. With the global shift towards electrification in automotive, industrial automation, and renewable energy systems, power semiconductor switches have become critical components. The market is projected to grow from $6.39 billion in 2024 to $9.29 billion by 2032, representing a compound annual growth rate (CAGR) of 5.6%. This growth is fueled by several key technological and market trends shaping the industry landscape.

Other Trends

Advancements in Wide Bandgap Semiconductors

The adoption of silicon carbide (SiC) and gallium nitride (GaN) based power semiconductor switches is accelerating, particularly in electric vehicles, renewable energy systems, and industrial motor drives. These wide bandgap materials offer superior performance characteristics including higher switching frequencies, higher temperature operation, and reduced switching losses compared to traditional silicon-based devices. Major manufacturers are increasingly investing in SiC and GaN production capacity to meet the growing demand from automotive and industrial sectors.

Increasing Integration with Smart Grid Infrastructure

Power semiconductor switches are playing a crucial role in the modernization of electrical grids through smart grid applications. The integration of renewable energy sources, grid stabilization, and power quality management require advanced power electronics with sophisticated switching capabilities. This trend is particularly prominent in developed regions like North America and Europe, where grid modernization initiatives are driving demand for high-performance power semiconductor devices with enhanced reliability and efficiency.

The market continues to be dominated by Asia-Pacific, particularly China, which accounts for nearly 50% of global demand. This is driven by massive investments in electric vehicle production, industrial automation, and renewable energy infrastructure. North America and Europe follow with strong growth in electric vehicle adoption and industrial automation, while emerging markets in Southeast Asia and Latin America are showing increasing adoption rates as manufacturing capabilities expand in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Global Players Dominate Semiconductor Switch Market

The global Power Semiconductor Switches market is highly competitive with several key players dominating the landscape. Infineon Technologies AG leads the market with the largest market share, followed by ON Semiconductor and STMicroelectronics N.V. These companies have established strong global distribution networks and extensive product portfolios that cater to various industry verticals including automotive, industrial, and consumer electronics.

Other significant players include Toshiba Corporation, Vishay Intertechnology Inc, and Fuji Electric, which have strong regional presence particularly in the Asian markets. Renesas Electronics, ROHM Semiconductor, and Sanken Electric have been growing their market share through strategic partnerships and technological innovations. Companies like Nexperia, Mitsubishi Electric, and Microchip Technology focus on specialized high-performance segments, while IXYS and Semikron maintain strong positions in industrial power modules.

List of Key Power Semiconductor Switches Companies

- Infineon Technologies AG

- ON Semiconductor

- STMicroelectronics N.V.

- Toshiba Corporation

- Vishay Intertechnology Inc

- Fuji Electric

- Renesas Electronics

- ROHM Semiconductor

- Sanken Electric

- Nexperia

- Mitsubishi Electric Corporation

- Microchip Technology

- Semikron Inc

- IXYS Corporation

- ABB Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

The Insulated Gate Bipolar Transistors (IGBT) segment leads due to its widespread adoption in high-power industrial applications and motor drives, offering excellent switching characteristics and voltage handling capabilities that make them indispensable in heavy industries. |

| By Application |

|

Industrial Motor Drives dominate due to massive industrial automation adoption and the need for precise motor control in manufacturing, robotics, and heavy machinery where reliability and efficiency are paramount for continuous operation. |

| By End User |

|

The Original Equipment Manufacturers (OEMs) lead as they integrate these switches directly into their final products across industries, from electric vehicles to industrial machinery, creating sustained demand and driving innovation through direct implementation. |

| By Voltage Range |

|

The Medium Voltage Devices lead as they cover the broadest range of industrial applications from 600V to 6.5kV, offering the optimal balance between performance requirements and cost-effectiveness for majority of industrial and renewable energy applications. |

| By Switching Frequency |

|

The Medium Frequency Switches lead as they offer the optimal trade-off between switching losses and system performance, making them ideal for motor drives and power supplies where both efficiency and thermal management are critical considerations. |

Regional Analysis: Power Semiconductor Switches Market

Asia-Pacific’s rapid industrialization drives demand for motor drives, robotics, and factory automation systems requiring sophisticated power semiconductor switches. Countries like China, Japan, and South Korea lead in industrial automation equipment exports.

China dominates global electric vehicle production with over 50% market share, driving massive demand for power semiconductors in traction inverters, onboard chargers, and charging infrastructure. Regional governments provide strong subsidies and policy support.

Massive investments in solar and wind power across China, India, and Southeast Asia drive demand for power semiconductor switches in inverters, converters, and grid infrastructure. China leads global solar panel production with over 70% market share.

Asia-Pacific remains the world’s primary consumer electronics manufacturing hub, driving continuous demand for power management ICs and semiconductor switches. The region produces over 75% of global consumer electronics.

North America

North America holds the second largest market share for power semiconductor switches, driven by strong aerospace, defense, and automotive industries. The region benefits from advanced manufacturing capabilities and significant investments in electric vehicle infrastructure. Major semiconductor companies maintain strong R&D presence in Silicon Valley and other tech hubs. The U.S. Inflation Reduction Act provides incentives for clean energy and electric vehicle adoption, supporting power semiconductor demand. The region leads in wide-bandgap semiconductor adoption with Silicon Carbide and Gallium Nitride technologies seeing rapid growth in electric vehicle chargers and renewable energy applications.

Europe

Europe maintains a strong position in the high-performance segment of power semiconductor switches, particularly in automotive and industrial applications. German automotive suppliers lead in developing advanced power modules for electric vehicles. The region benefits from strong collaboration between automotive OEMs and semiconductor manufacturers. Strict emissions regulations accelerate adoption of efficient power electronics across industries. Europe leads in offshore wind power, driving demand for high-voltage power conversion systems. The region maintains technological leadership in precision industrial applications and high-performance automotive sectors.

Rest of World

Emerging markets in Latin America, Middle East, and Africa show accelerating growth in power semiconductor adoption, though from a smaller base. These regions benefit from increasing electrification and industrialization. Infrastructure development projects drive demand for power electronics in energy, transportation, and industrial sectors. Regional manufacturing capabilities continue to develop, supported by both local and international semiconductor companies. The regions show particular strength in renewable energy integration and power infrastructure modernization, with growing investments in smart grid technologies and industrial automation.

Report Scope

This report provides a comprehensive analysis of the Global Power Semiconductor Switches Market, covering the forecast period 2025-2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power Semiconductor Switches Market?

-> Power Semiconductor Switches Market size was valued at USD 6.40 billion in 2024 to USD 9.30 billion by 2032, exhibiting a CAGR of 5.6% during the forecast period.

Which key companies operate in Power Semiconductor Switches Market?

-> Key players include Infineon Technologies AG, ON Semiconductor, STMicroelectronics N.V., Toshiba Corporation, Vishay Intertechnology Inc, Fuji Electric, Renesas Electronics, ROHM Semiconductor, Sanken, Nexperia, Mitsubishi Electric Corporation, Microchip Technology, Semikron Inc, IXYS, and ABB Ltd. among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for energy-efficient systems, electrification of transportation, growth in renewable energy integration, and rising demand for industrial automation.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China alone accounting for nearly 50% of the global market share. North America and Europe also hold significant market shares due to advanced industrial infrastructure.

What are the emerging trends?

-> Emerging trends include development of wide-bandgap semiconductors (SiC and GaN), integration of smart grid technologies, and increasing adoption of electric vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...