MARKET INSIGHTS

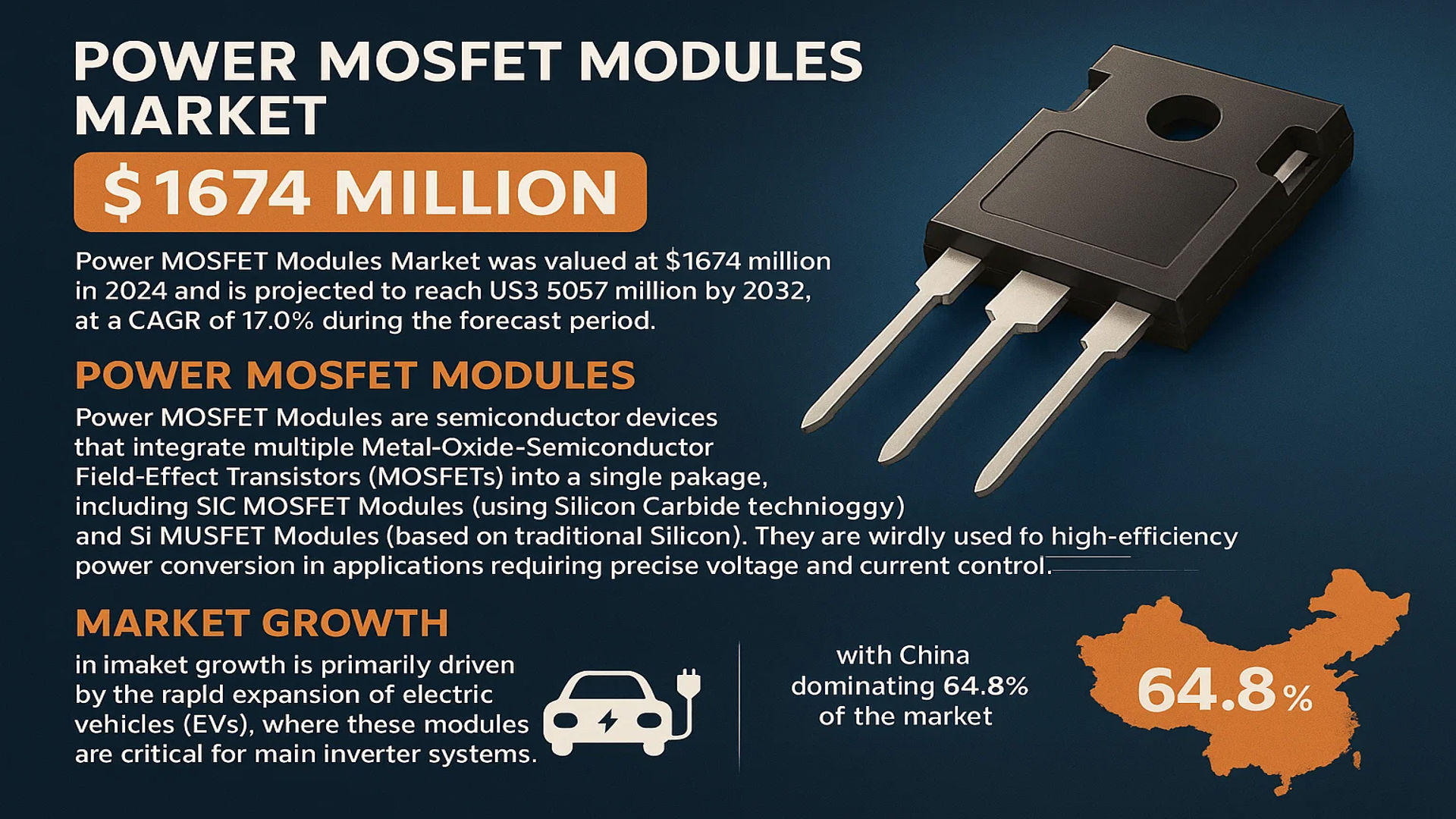

The global Power MOSFET Modules Market was valued at 1674 million in 2024 and is projected to reach US$ 5057 million by 2032, at a CAGR of 17.0% during the forecast period.

Power MOSFET Modules are semiconductor devices that integrate multiple Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs) into a single package, offering enhanced power handling capabilities. These modules include SiC MOSFET Modules (using Silicon Carbide technology) and Si MOSFET Modules (based on traditional Silicon). They are widely used for high-efficiency power conversion in applications requiring precise voltage and current control.

The market growth is primarily driven by the rapid expansion of electric vehicles (EVs), where these modules are critical for main inverter systems. In 2023, global EV sales surged to 14.65 million units, with China dominating 64.8% of the market. Additionally, industrial automation and renewable energy sectors are adopting Power MOSFET Modules for their superior thermal performance and energy efficiency. Key players like STMicroelectronics, Infineon, and Wolfspeed collectively hold over 70% market share, leveraging advanced semiconductor technologies to meet rising demand.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Demand for Electric Vehicles Drives Adoption of Power MOSFET Modules

The global transition toward electric mobility is fundamentally reshaping the automotive power electronics landscape. With new energy vehicle sales reaching 14.65 million units globally in 2023, the demand for efficient power conversion solutions like MOSFET modules has intensified. These modules, particularly Silicon Carbide (SiC) variants, are critical components in EV traction inverters where they enable higher switching frequencies and superior thermal performance. The accelerating EV adoption across China (64.8% global market share), Europe (48% growth), and North America (18.3% growth) creates a compounding demand effect for power semiconductor solutions.

Industrial Automation Boom Spurs Module Deployments

Industrial 4.0 initiatives worldwide are driving unprecedented demand for precision motor control and power management systems. Power MOSFET modules are finding increasing application in servo drives, robotics, and smart manufacturing equipment where they offer superior power density and thermal characteristics compared to discrete solutions. The global industrial automation market is projected to maintain a 9% CAGR through 2030, creating sustained demand for power modules across motor control and energy conversion applications.

Renewable Energy Integration Creates New Application Horizons

The rapid expansion of solar PV installations and energy storage systems presents significant opportunities for power module manufacturers. MOSFET modules enable more efficient DC/AC conversion in solar inverters and battery management systems, with SiC-based solutions showing particular promise in high-power applications. With global renewable capacity additions increasing consistently every year, the need for reliable power conversion technologies continues to accelerate across both utility-scale and distributed generation applications.

MARKET RESTRAINTS

Material Shortages Challenge Supply Chain Stability

The power semiconductor industry continues grappling with supply chain disruptions affecting critical raw materials like silicon wafers and specialty substrates. The market concentration of SiC substrate production among few suppliers creates vulnerabilities, while geopolitical factors affecting semiconductor-grade materials imports present ongoing challenges. These constraints impact both production volumes and pricing stability across the power module value chain.

High Development Costs Impede Technology Adoption

While advanced SiC MOSFET modules demonstrate clear performance advantages, their adoption faces barriers from substantially higher manufacturing and development costs compared to silicon-based solutions. The specialized fabrication processes and quality control requirements for power modules contribute to significant capital expenditure demands. These economic factors slow technology migration in cost-sensitive applications despite the long-term efficiency benefits.

Thermal Management Complexities Present Design Challenges

Power module integration in high-current applications generates substantial thermal dissipation requirements that challenge system designers. Maintaining optimal junction temperatures while minimizing size and weight necessitates sophisticated cooling solutions that impact overall system cost and complexity. These thermal constraints influence module selection criteria across automotive, industrial, and energy applications.

MARKET CHALLENGES

Intellectual Property Protection in Competitive Landscape

The concentrated nature of the power module market, where the top three players control over 70% market share, creates intense competition around proprietary technologies. Companies face mounting challenges in protecting advanced packaging designs and semiconductor innovations while meeting expanding market demands. This competitive pressure impacts R&D investment decisions and product development timelines across the industry.

Standardization Gaps Hinder Application Engineering

The absence of universally adopted standards for power module form factors and interfaces creates interoperability challenges for OEMs. Design teams frequently encounter difficulties when evaluating alternative module solutions due to variations in mechanical dimensions, pin configurations, and performance specifications. These inconsistencies increase development effort and limit the flexibility of power system architectures.

Lifecycle Management in Rapid Technology Evolution

The accelerating pace of semiconductor technology advancement presents unique longevity challenges for power module applications with extended product life requirements. Industrial and transportation applications in particular demand stable supply chains spanning decades, creating tension with the rapid improvement cycles of power semiconductor technologies. Manufacturers must balance innovation with long-term availability commitments.

MARKET OPPORTUNITIES

Emerging Wide Bandgap Semiconductor Applications

The expansion of SiC and GaN power semiconductor technologies creates new opportunities for module innovation. Emerging applications in aerospace, defense, and high-performance computing require the unique combination of high-temperature operation and power density enabled by advanced module packaging of these materials. Early adopters in these specialized sectors help drive technology maturation for broader commercialization.

Smart Module Integration Enhances Value Proposition

Incorporating intelligent features like built-in diagnostics, condition monitoring, and predictive maintenance capabilities represents a significant value-add opportunity. These smart module configurations address growing OEM demands for system-level reliability improvements and maintenance cost reductions across industrial and transportation applications.

Geographic Market Expansion in Developing Economies

The accelerating industrialization of emerging markets presents substantial growth potential for power module suppliers. Regions with developing manufacturing bases and expanding energy infrastructure require robust power conversion solutions tailored to local operating conditions and technical capabilities. Customized module solutions addressing these regional requirements can unlock new market segments.

POWER MOSFET MODULES MARKET TRENDS

Rising Demand for Silicon Carbide (SiC) MOSFET Modules in Automotive and Industrial Sectors

The Power MOSFET Modules market is experiencing significant growth due to the increasing adoption of Silicon Carbide (SiC) technology, particularly in the automotive and industrial sectors. SiC MOSFET modules offer superior efficiency, higher switching frequencies, and better thermal performance compared to traditional silicon-based modules. This has led to their widespread use in electric vehicle (EV) inverters, industrial motor drives, and renewable energy systems. The global automotive sector, specifically the EV market, is a major driver, with over 14.65 million new energy vehicles sold in 2023, representing a 35.4% year-on-year increase. China alone accounted for 64.8% of these sales, reinforcing its dominance in the market.

Other Trends

Technological Innovations in Power Electronics

Advancements in semiconductor manufacturing, including higher power density and reduced energy loss, are shaping the Power MOSFET Modules market. Leading manufacturers such as Infineon, STMicroelectronics, and Wolfspeed are investing heavily in R&D to develop SiC and Si MOSFET modules that meet the growing demand for compact, high-efficiency solutions. These innovations are particularly crucial for applications such as main inverters in electric vehicles and energy storage systems, where efficiency improvements can significantly impact performance and cost-effectiveness.

Impact of Global Semiconductor Supply Chain Dynamics

The Power MOSFET Modules market is also influenced by evolving supply chain dynamics, including semiconductor shortages and regional manufacturing shifts. While demand continues to surge, especially in Asia-Pacific regions like China and Japan, supply chain disruptions have occasionally led to price fluctuations and extended lead times. However, strategic collaborations among key industry players and government-backed initiatives for semiconductor self-sufficiency (such as those in the U.S. and Europe) are expected to stabilize the market in the medium to long term.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Innovations and Strategic Alliances to Dominate the Market

The global Power MOSFET Modules market is characterized by a mix of dominant semiconductor players, emerging manufacturers, and specialized suppliers, with the top three companies—STMicroelectronics, Infineon, and Wolfspeed—holding over 70% of the market share in 2024. The competitive environment is highly dynamic, with companies aggressively expanding their silicon carbide (SiC) and silicon (Si) MOSFET technologies to meet escalating demand from electric vehicle (EV) manufacturers, industrial automation, and renewable energy sectors.

Infineon Technologies and STMicroelectronics maintain leadership due to their extensive R&D investments, global production capabilities, and strong relationships with automotive OEMs. These players are accelerating the adoption of SiC MOSFET modules, particularly for high-voltage applications in EVs, where efficiency and thermal performance are critical. Meanwhile, Wolfspeed distinguishes itself with vertically integrated SiC production, from wafer fabrication to module assembly, ensuring supply chain resilience.

Asian players like BYD Semiconductor and Rohm are rapidly gaining ground, supported by China’s dominance in the EV market—accounting for 64.8% of global NEV sales in 2023. These companies benefit from regional government incentives and partnerships with domestic automakers. Mitsubishi Electric and Fuji Electric remain key contenders in industrial and railway applications, leveraging decades of expertise in high-power modules.

Smaller firms such as SemiQ and BASiC Semiconductor are carving niches in cost-optimized solutions, while startups like InventChip Technology focus on disruptive designs for emerging markets. Strategic acquisitions—such as onsemi’s purchase of GT Advanced Technologies—highlight the race to secure SiC supply chains. As competition intensifies, collaboration with OEMs and tier-1 suppliers will be pivotal for sustaining growth.

List of Key Power MOSFET Modules Companies Profiled

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- Wolfspeed (U.S.)

- Rohm Semiconductor (Japan)

- onsemi (U.S.)

- BYD Semiconductor (China)

- Microchip (Microsemi) (U.S.)

- Mitsubishi Electric (Vincotech) (Japan)

- Semikron Danfoss (Germany)

- Fuji Electric (Japan)

Segment Analysis:

By Type

SiC MOSFET Segment Leads Due to Superior Efficiency in High-Temperature Applications

The market is segmented based on type into:

- SiC MOSFET

- Si MOSFET

By Application

Main Inverter (Electric Traction) Segment Dominates with Growing Adoption in Electric Vehicles

The market is segmented based on application into:

- Main Inverter (Electric Traction)

- Industrial Drives

- UPS

- Trains & Traction

- PV & Energy

- Others

By End User

Automotive Sector Remains Key Consumer with Rapid EV Market Expansion

The market is segmented based on end user into:

- Automotive

- Industrial

- Energy & Power

- Railway

- Others

Regional Analysis: Power MOSFET Modules Market

Asia-Pacific

The Asia-Pacific region dominates the global Power MOSFET Modules market, driven primarily by China’s explosive growth in electric vehicle production and industrial automation. China accounts for nearly 65% of global new energy vehicle sales, with 9.495 million units sold in 2023, creating massive demand for silicon carbide (SiC) MOSFET modules in traction inverters. Japan and South Korea maintain strong positions in high-efficiency power electronics, with companies like Rohm, Toshiba, and Mitsubishi Electric leading SiC innovation. The region benefits from concentrated semiconductor manufacturing ecosystems, aggressive government support for electrification, and rapid adoption of renewable energy systems requiring advanced power conversion technology. However, price competition remains fierce, particularly in the silicon MOSFET segment.

North America

North America represents the second-largest market for Power MOSFET Modules, fueled by the U.S. automotive industry’s transition to electrification and substantial investments in renewable energy infrastructure. With 2.94 million new energy vehicles sold in 2023 (18.3% year-on-year growth), demand for high-voltage SiC modules in main inverters continues rising. Major players like Wolfspeed and onsemi are expanding SiC production capacity in response to the growing market, supported by government initiatives such as the CHIPS Act. The region sees strong adoption in industrial motor drives, datacenter power supplies, and military/aerospace applications requiring ruggedized power electronics solutions. Technological leadership and high R&D expenditure position North America as an innovation hub, though supply chain localization remains a challenge.

Europe

Europe’s Power MOSFET Modules market is characterized by stringent efficiency regulations and accelerating EV adoption, with 1.46 million new energy vehicle sales in 2023 (48% growth). German automotive manufacturers and tier-1 suppliers drive demand for premium SiC solutions, while industrial automation upgrades across Northern Europe sustain silicon MOSFET demand. The region benefits from strong semiconductor players like Infineon, STMicroelectronics, and Semikron Danfoss, coupled with EU policies promoting energy-efficient power electronics. Challenges include higher production costs compared to Asian competitors and fragmented standards for power module packaging technologies. The green energy transition, particularly in wind and solar power conversion, presents significant growth opportunities for advanced MOSFET modules.

South America

South America represents an emerging market for Power MOSFET Modules, with Brazil and Argentina showing gradual uptake in industrial automation and renewable energy applications. The automotive sector remains limited but shows potential with regional EV incentives and infrastructure development. Market growth is constrained by economic volatility, import dependency for semiconductor components, and slower technology adoption curves compared to other regions. Local assembly of power electronics remains scarce, with most modules imported from Asia or North America. However, increasing investments in solar power generation and mining electrification could drive future demand for modules suited to harsh operating environments.

Middle East & Africa

The Middle East & Africa region exhibits nascent but growing demand for Power MOSFET Modules, primarily in oil & gas electrification projects and renewable energy installations. Gulf Cooperation Council countries lead in adopting high-power modules for solar inverters and grid infrastructure, leveraging sovereign wealth fund investments. Africa shows potential in off-grid power solutions and industrial applications, though market development is hindered by limited local technical expertise and competing priorities in power infrastructure buildout. The lack of domestic semiconductor manufacturing means nearly all modules are imported, creating supply chain vulnerabilities. Strategic partnerships with global power electronics suppliers are beginning to establish localized support networks for critical energy projects.

Report Scope

This market research report provides a comprehensive analysis of the global Power MOSFET Modules market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Power MOSFET Modules market was valued at USD 1,674 million in 2024 and is projected to reach USD 5,057 million by 2032, growing at a CAGR of 17.0% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (SiC MOSFET Modules and Si MOSFET Modules), application (Main Inverter, Industrial Drives, UPS, Trains & Traction, PV & Energy), and end-user industries to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. Asia-Pacific dominates the market due to rapid growth in electric vehicle adoption, with China accounting for 64.8% of global new energy vehicle sales in 2023.

- Competitive Landscape: Profiles of leading market participants such as STMicroelectronics, Infineon, Wolfspeed, Rohm, and onsemi, including their product offerings, R&D focus, manufacturing capacity, and recent developments. The top three players hold over 70% market share in 2024.

- Technology Trends & Innovation: Assessment of emerging technologies in semiconductor design, including the transition to wide-bandgap materials like silicon carbide (SiC) for higher efficiency applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as electric vehicle adoption (global sales reached 14.65 million units in 2023), along with challenges like supply chain constraints and raw material costs.

- Stakeholder Analysis: Insights for component suppliers, automotive OEMs, power electronics manufacturers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Power MOSFET Modules Market?

->Power MOSFET Modules Market was valued at 1674 million in 2024 and is projected to reach US$ 5057 million by 2032, at a CAGR of 17.0% during the forecast period.

Which key companies operate in Global Power MOSFET Modules Market?

-> Key players include STMicroelectronics, Infineon, Wolfspeed, Rohm, onsemi, BYD Semiconductor, and Mitsubishi Electric, among others. The top three players hold over 70% market share.

What are the key growth drivers?

-> Key growth drivers include rapid adoption of electric vehicles (global sales reached 14.65 million in 2023), industrial automation trends, and renewable energy integration requiring efficient power conversion.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by China’s dominance in electric vehicle production (9.495 million units sold in 2023). Europe and North America show strong growth potential with 48.0% and 18.3% year-on-year increases in EV sales respectively.

What are the emerging trends?

-> Emerging trends include adoption of SiC MOSFET technology for higher efficiency, integration with AI-driven power management systems, and development of compact, high-power density modules for automotive and industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...