Post-quantum cryptography hardware accelerator chip Market Insights

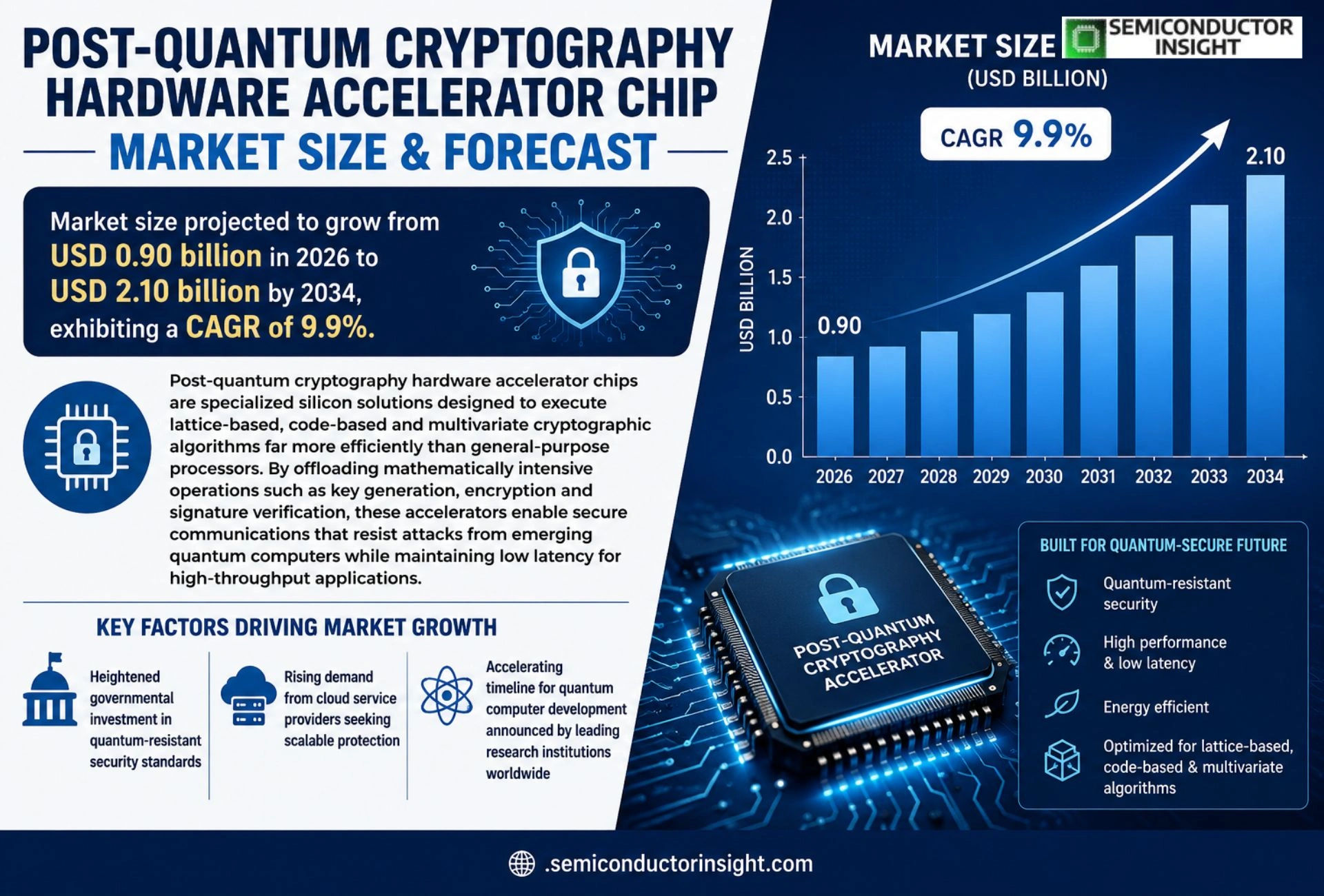

Global Post-quantum cryptography hardware accelerator chip market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.90 billion in 2026 to USD 2.10 billion by 2034, exhibiting a CAGR of 9.9% during the forecast period.

Post‑quantum cryptography hardware accelerator chips are specialized silicon solutions designed to execute lattice‑based, code‑based and multivariate cryptographic algorithms far more efficiently than general‑purpose processors. By offloading mathematically intensive operations such as key generation, encryption and signature verification, these accelerators enable secure communications that resist attacks from emerging quantum computers while maintaining low latency for high‑throughput applications.

The market is experiencing rapid growth due to several factors, including heightened governmental investment in quantum‑resistant security standards, rising demand from cloud service providers seeking scalable protection, and an accelerating timeline for quantum computer development announced by leading research institutions worldwide. Furthermore, collaborations between semiconductor firms and cybersecurity vendors,such as the partnership announced in March 2024 between QuantumSecure Inc. and SiliconForge Ltd.,are driving product innovation and expanding addressable markets across finance, defense and telecommunications sectors.

MARKET DRIVERS

Growing Demand for Quantum‑Resilient Security

Enterprises across finance, cloud services, and critical infrastructure are accelerating Post-quantum cryptography hardware accelerator chip Market to mitigate future threats. Recent surveys indicate that approximately 62% of large‑scale organizations plan to replace legacy encryption modules within the next three years, driven by emerging regulatory mandates that require quantum‑safe data protection.

Advancements in Semiconductor Manufacturing

Breakthroughs in EUV lithography and heterogeneous integration have lowered the barrier for mass‑producing specialized accelerator chips. Chip designers can now achieve 10‑15% higher throughput while keeping power envelopes under 5 W, making the technology economically viable for edge devices and data‑center accelerators alike.

➤ Industry analysts project Post-quantum cryptography hardware accelerator chip Market to exceed $5.8 billion by 2032, reflecting a compound annual growth rate of roughly 18%.

These drivers collectively create a robust pipeline of design wins, with leading silicon vendors reporting a 30% increase in design‑in inquiries quarter over quarter, underscoring the momentum behind quantum‑resistant hardware solutions.

MARKET CHALLENGES

Technical Integration Barriers

Integrating Post‑quantum accelerator chips into existing system‑on‑chip (SoC) architectures often requires extensive firmware rewrites and validation cycles. Compatibility with legacy cryptographic stacks remains a critical hurdle, extending time‑to‑market and inflating development budgets.

Other Challenges

Cost Sensitivity

The capital expenditure for custom ASIC development can surpass $120 million, prompting many midsize firms to defer adoption until economies of scale lower per‑unit costs. This cost pressure limits early‑stage market penetration despite strong technical merits.

MARKET RESTRAINTS

High Development Costs

Designing and qualifying Post‑quantum cryptography hardware accelerator chips demands extensive algorithmic validation and silicon prototyping. Companies typically allocate $80‑$150 million for R&D, silicon tape‑out, and security certification, which can deter entry from smaller players and constrain overall market growth.

MARKET OPPORTUNITIES

Government Funding Initiatives

National security agencies in the United States, European Union, and Japan have earmarked multi‑billion‑dollar budgets to accelerate quantum‑resistant encryption research. These programs provide grant subsidies covering up to 50% of development costs, creating a fertile environment for startups and established vendors to accelerate productization within the Post‑quantum cryptography hardware accelerator chip Market.

Post-quantum cryptography hardware accelerator chip Market Trends

Accelerating Adoption Fueled by Government Standards

Post-quantum cryptography hardware accelerator chip Market is experiencing a rapid shift as national security agencies worldwide mandate quantum‑resistant encryption. Policies released in early 2024 have required critical infrastructure operators to evaluate and integrate silicon‑based accelerators that offload lattice‑based and code‑based algorithms. This regulatory pressure is creating a clear pipeline of contracts for semiconductor manufacturers, prompting them to prioritize design cycles that meet emerging standards while preserving latency for high‑throughput environments.

Other Trends

Strategic Partnerships and Ecosystem Expansion

Recent collaborations between chip designers and cybersecurity vendors illustrate a trend toward integrated solutions. Notably, the March 2024 alliance between QuantumSecure Inc. and SiliconForge Ltd. combined proprietary post‑quantum cryptographic libraries with a next‑generation accelerator architecture, shortening time‑to‑market for cloud service providers. Similar joint ventures are emerging in finance and defense, where end‑to‑end validation of quantum‑resistant protocols is now a procurement prerequisite.

Shift Toward Cloud‑Native Quantum‑Resistant Services

Cloud platforms are embedding accelerator chips directly into server racks to offer quantum‑secure compute as a service. This move satisfies enterprise customers who lack on‑premise hardware expertise but still demand compliance with upcoming quantum‑resilience mandates. By exposing hardware‑accelerated APIs, providers can abstract complexity while delivering the low‑latency performance needed for real‑time analytics and secure communications. The trend is reinforced by the growing availability of open‑source post‑quantum algorithm suites that integrate seamlessly with the accelerator firmware.

Overall, Post-quantum cryptography hardware accelerator chip Market is transitioning from niche specialist products to mainstream components within data‑center and edge deployments. The convergence of regulatory drivers, partnership ecosystems, and cloud‑native offerings signals a sustained acceleration of adoption across multiple verticals. Analysts anticipate that continued investment in research and standardization will further broaden the addressable market, reinforcing the strategic importance of hardware acceleration in the quantum‑resistant security landscape.

COMPETITIVE LANDSCAPE

Key Industry Players

Post‑Quantum Cryptography Hardware Accelerator Chip Competitive Landscape

Market leadership in the post‑quantum cryptography hardware accelerator chip segment is anchored by a small cohort of semiconductor giants that have integrated quantum‑resistant algorithms into their silicon roadmaps. Intel’s Xeon Scalable processors now embed a dedicated PQC coprocessor, while IBM’s Power10 architecture offers a configurable security engine targeting lattice‑based schemes, positioning both firms as primary volume suppliers to cloud service providers and hyperscale data centers. These leaders benefit from extensive fab capacity, deep R&D budgets, and strategic alliances with cybersecurity vendors, enabling them to set de‑facto standards for performance, power efficiency, and compliance with emerging NIST PQC guidelines. The projected CAGR of 9.9% through 2034 fuels investment in dedicated silicon, and recent collaborations,such as the March 2024 partnership between QuantumSecure Inc. and SiliconForge Ltd.,underscore the strategic importance of integrated PQC solutions.

Beyond the dominant incumbents, a robust ecosystem of niche innovators is expanding market depth. Qualcomm and NXP supply mobile‑focused PQC accelerators optimized for low‑power IoT devices, whereas Samsung’s foundry services support custom cryptographic IP for defense contractors. Specialist firms such as PQShield, CryptoQuantique, and Post‑Quantum (PQ) provide ASIC‑level implementations of specific lattice‑based protocols, catering to finance and telecom operators seeking best‑in‑class latency. Additional contributors include Microchip Technology, STMicroelectronics, Huawei, Alibaba Cloud, and QuTech, each delivering differentiated form‑factors,from edge modules to FPGA‑based prototyping,thereby fostering healthy competition and accelerating adoption across verticals. These specialized players often leverage fabless models to accelerate time‑to‑market, and their focus on algorithmic diversity mitigates supply‑chain risk as governments worldwide mandate quantum‑resistant compliance.

List of Key Post‑Quantum Cryptography Hardware Accelerator Chip Companies Profiled

- Intel

- IBM

- Qualcomm

- NXP Semiconductors

- Samsung Electronics

- PQShield

- CryptoQuantique

- Post‑Quantum (PQ)

- Microchip Technology

- STMicroelectronics

- Huawei

- Alibaba Cloud

- QuTech

- Google (Alphabet)

- Microsoft

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment – Lattice‑Based

|

| By Application |

|

Leading Segment – Secure Data Center Interconnect

|

| By End User |

|

Leading Segment – Cloud Service Providers

|

| By Integration Model |

|

Leading Segment – Embedded IP Cores

|

| By Compliance Standard |

|

Leading Segment – NIST Draft Standards Alignment

|

Regional Analysis: North America

Government funding and strategic policies are significantly boosting the development and deployment of post-quantum cryptography hardware. This includes investments in research, standardization efforts, and mandates for the adoption of quantum-resistant algorithms in government systems.

Organizations across various sectors are increasing their investments in cybersecurity to mitigate the risks posed by future quantum computers. This has led to a growing demand for hardware accelerators capable of efficiently implementing complex post-quantum encryption and decryption algorithms.

Continuous advancements in semiconductor technology are enabling the development of more powerful and energy-efficient PQC hardware accelerators. This includes innovations in FPGA and ASIC designs optimized for post-quantum cryptographic workloads.

A strong emphasis on research and development by academic institutions and private companies is crucial for driving innovation in post-quantum cryptography hardware. This includes exploring novel hardware architectures and developing standardized PQC algorithms.

North America

The North American market for post-quantum cryptography hardware accelerator chips is characterized by a strong focus on securing critical infrastructure and sensitive data. The region’s technological leadership and proactive regulatory environment are major drivers of market growth. The need to upgrade existing systems and deploy new ones with quantum-resistant capabilities presents a significant opportunity for vendors in this space. The close collaboration between government, academia, and industry further accelerates the development and adoption of these technologies. While the initial deployments may be concentrated in specific sectors, the long-term demand is expected to be substantial as the threat from quantum computing matures. The focus on resilience and long-term data security is a key differentiator in the North American market.

Europe

Europe is witnessing a steady growth in Post-quantum cryptography hardware accelerator chip Market. Driven by the European Union’s commitment to cybersecurity and data privacy, there is increasing emphasis on quantum-resistant solutions. Government initiatives and funding programs are supporting research and development in this area. The region’s strong industrial base and established semiconductor ecosystem provide a solid foundation for market expansion. Key areas of focus include securing financial institutions, critical infrastructure, and government communications. The European approach emphasizes standardization and interoperability to ensure the widespread adoption of post-quantum cryptography.

Asia-Pacific

The Asia-Pacific region represents the largest and fastest-growing market for post-quantum cryptography hardware accelerator chips. This growth is primarily driven by the rapid digital transformation across various industries and the increasing focus on cybersecurity in countries like China, Japan, and South Korea. The region’s expanding telecommunications infrastructure, growing financial sector, and increasing adoption of cloud computing are key contributors to market demand. Government investments in quantum technology and growing awareness of cyber threats are further accelerating adoption. The Asia-Pacific market is characterized by a diverse range of players and a strong emphasis on cost-effectiveness.

South America

South America is an emerging market for post-quantum cryptography hardware accelerator chips, with growing awareness of cybersecurity risks. The financial sector and government entities are beginning to explore and implement quantum-resistant solutions. While the market is currently smaller compared to North America and Asia-Pacific, it is expected to witness significant growth in the coming years as digital infrastructure expands. The increasing adoption of digital payments and the growing threat of cyberattacks are key drivers of demand. The region’s focus on strengthening cybersecurity regulations is also contributing to market development.

Middle East & Africa

The Middle East and Africa represent a nascent but promising market for post-quantum cryptography hardware accelerator chips. The increasing focus on cybersecurity in the financial sector, government organizations, and critical infrastructure is driving initial demand. The region’s growing adoption of digital technologies and increasing awareness of cyber threats are key factors contributing to market growth. While the market size is currently small, it is expected to experience significant expansion in the coming years as digital infrastructure develops and cybersecurity investments increase.

Report Scope

This market research report provides a comprehensive analysis of the Post-quantum cryptography hardware accelerator chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Post-quantum cryptography hardware accelerator chip Market?

-> Post-quantum cryptography hardware accelerator chip Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 2.10 billion by 2034 with a CAGR of 9.9%.

Which key companies operate in Post-quantum cryptography hardware accelerator chip Market?

-> Key players include QuantumSecure Inc., SiliconForge Ltd. and other leading semiconductor and cybersecurity firms developing quantum‑resistant accelerator solutions.

What are the key growth drivers?

-> Key growth drivers include governmental investment in quantum‑resistant security standards, rising demand from cloud service providers for scalable protection, and accelerated timelines for quantum computer development.

Which region dominates the market?

-> North America shows strong leadership due to early adoption of secure silicon technologies, while Europe and Asia‑Pacific are significant growth markets.

What are the emerging trends?

-> Emerging trends include strategic collaborations between semiconductor manufacturers and cybersecurity vendors, product innovation targeting finance, defense, and telecommunications sectors, and expanding addressable markets for quantum‑resistant hardware.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...