MARKET INSIGHTS

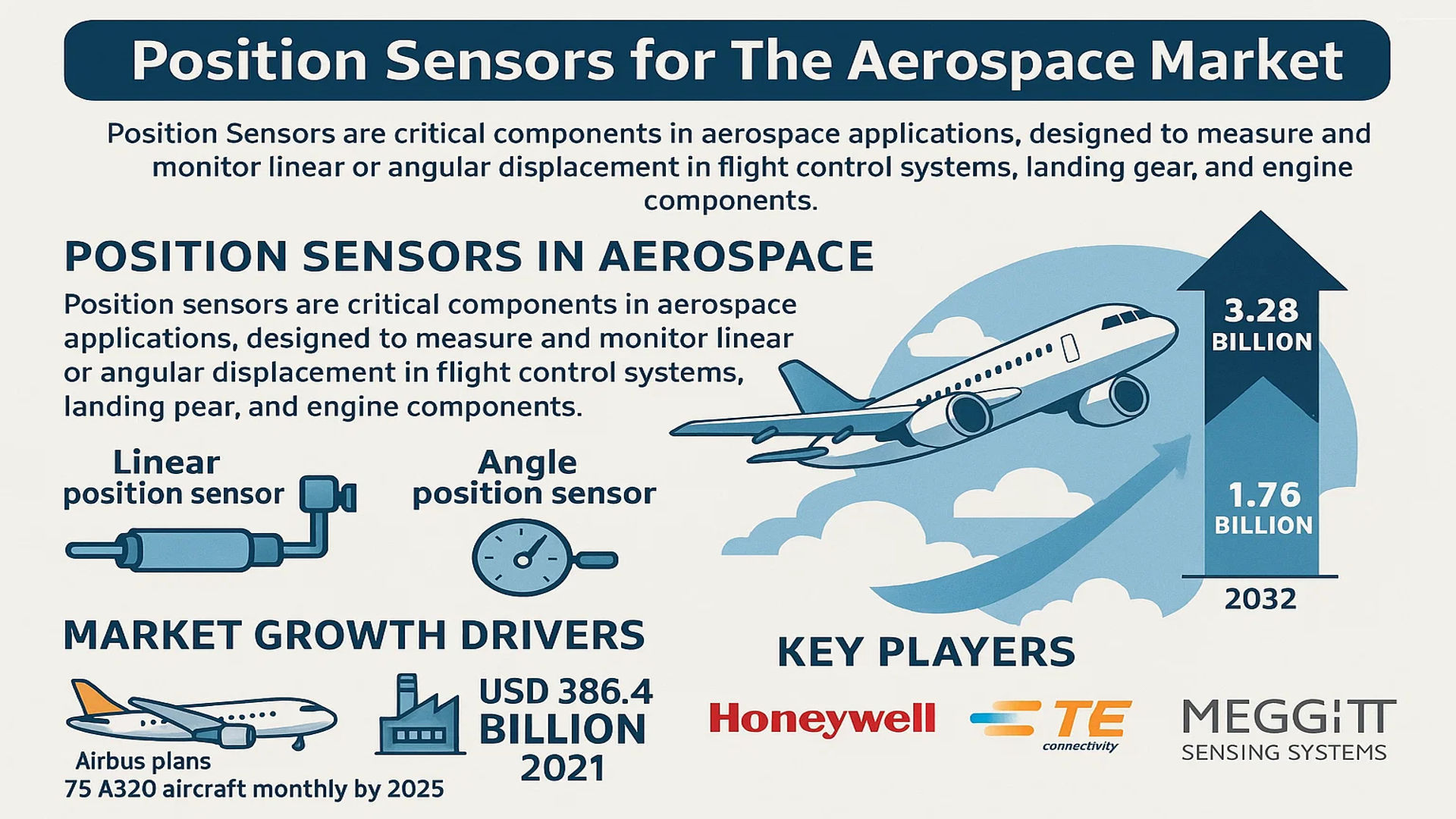

The global Position Sensors for The Aerospace Market size was valued at US$ 1.76 billion in 2024 and is projected to reach US$ 3.28 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032.

Position sensors are critical components in aerospace applications, designed to measure and monitor linear or angular displacement in flight control systems, landing gear, and engine components. These sensors include linear position sensors and angle position sensors, which provide real-time data for navigation, autopilot systems, and structural health monitoring.

The market growth is driven by increasing aircraft production rates, with Airbus planning to manufacture 75 A320 aircraft monthly by 2025. Meanwhile, the global aerospace industry revenue reached USD 386.4 billion in 2021, creating significant demand for precision sensing technologies. Key players like Honeywell, TE Connectivity, and Meggitt Sensing Systems are expanding their portfolios through R&D investments in next-generation sensor technologies for both commercial and military aircraft applications.

MARKET DYNAMICS

MARKET DRIVERS

Rebounding Aircraft Production Rates to Accelerate Demand for Position Sensors

The aerospace industry is witnessing a strong recovery post-pandemic, with major manufacturers aggressively ramping up production. Airbus has projected increasing A320 family production to 75 units monthly by 2025, up from 60 pre-pandemic levels. This manufacturing surge directly correlates with heightened demand for precision position sensors critical for flight control systems, landing gear monitoring, and engine component positioning. With commercial aviation orders backlogged through 2030 in some cases, sustained sensor demand appears inevitable.

Military Modernization Programs Fueling Advanced Sensor Adoption

Global defense spending continues its upward trajectory, exceeding $2 trillion annually, with significant allocations toward next-generation aircraft. Modern fighter jets now incorporate over 300 position sensors per aircraft – three times more than previous generations. The need for real-time flight data collection and autonomous systems operation makes high-accuracy position sensing indispensable. Recent geopolitical tensions have further accelerated military aircraft procurement, particularly in Asia-Pacific and Middle Eastern markets.

Emerging applications in unmanned systems present additional growth avenues. Military drones now utilize miniaturized position sensors for precise actuator control and navigation, with some models containing over 50 discrete sensing points. This expansion of sensing requirements across both manned and unmanned platforms creates sustained market momentum.

MARKET RESTRAINTS

Stringent Certification Requirements Increase Development Costs

Aerospace position sensors face rigorous qualification standards like DO-160 and DO-178C, extending development cycles by 18-24 months compared to industrial counterparts. Certification costs often exceed $500,000 per sensor variant, creating significant barriers for new entrants. These requirements stem from aviation’s zero-failure tolerance, necessitating extensive environmental, EMI, and lifecycle testing. While ensuring reliability, such protocols compress profit margins and delay time-to-market for innovative solutions.

Supply chain disruptions further exacerbate cost pressures. Aerospace-grade materials and specialized components often face 12-18 month lead times, requiring manufacturers to maintain large safety stocks. This capital-intensive environment makes the market particularly vulnerable to inflationary pressures and raw material shortages.

MARKET CHALLENGES

Miniaturization Demands Strain Sensor Performance Parameters

Modern aircraft designs prioritize weight reduction, pushing position sensor packages below 50g while maintaining micron-level accuracy. Achieving this performance in constrained footprints requires advanced materials and manufacturing techniques that currently have limited production scalability. Thermal stability becomes particularly challenging in compact designs, as small form factors struggle to dissipate heat from electronics while preventing measurement drift.

Power consumption presents another critical challenge. Next-gen aircraft systems increasingly demand sensors operating below 100mW without sacrificing refresh rates or resolution. Meeting these parameters requires innovative low-power ASIC designs and energy harvesting solutions that are still in developmental phases for most manufacturers.

MARKET OPPORTUNITIES

Electric Aircraft Development Opens New Sensor Frontiers

The emerging electric vertical takeoff and landing (eVTOL) market represents a $35 billion opportunity by 2035, with each vehicle requiring specialized position sensing for distributed electric propulsion systems. Unlike conventional aircraft, eVTOL designs incorporate dozens of electric motors needing continuous position feedback for flight control algorithms. This creates demand for lightweight, high-speed sensors capable of operating in high-EMI environments near power electronics.

Space commercialization provides another high-growth avenue. With over 1,300 satellites launched annually, demand persists for radiation-hardened position sensors capable of surviving 15+ years in orbit. New deep space exploration initiatives will further drive requirements for extreme environment sensors with operational ranges exceeding -150°C to +200°C.

Advancements in contactless sensing technology show particular promise. Emerging optical and magnetic field-based position sensors eliminate mechanical wear points while offering improved reliability and lifespan. Several major aerospace contractors have begun integrating these technologies into next-generation airframe designs expected to enter service post-2028.

POSITION SENSORS FOR THE AEROSPACE MARKET TRENDS

Increasing Aircraft Production Rates to Boost Demand for Position Sensors

The aerospace industry is witnessing a strong recovery post-pandemic, with commercial aircraft manufacturers ramping up production to meet surging demand. Airbus and Boeing, two of the largest aerospace companies, have announced ambitious production rate increases for their most popular models. Linear and angular position sensors play a critical role in flight control systems, landing gear monitoring, and engine control – all areas that see heightened demand with increased aircraft output. As aerospace OEMs work through record order backlogs, sensor manufacturers are scaling their production to meet the needs of both new aircraft builds and aftermarket replacements. This production surge isn’t limited to commercial aviation; defense spending increases in multiple nations are similarly driving军用飞机 sensor demand.

Other Trends

Miniaturization and Weight Reduction Initiatives

The aerospace sector’s relentless focus on weight reduction and space optimization continues to shape position sensor development. Modern aircraft designs incorporate smaller, lighter sensor packages with improved accuracy to support fuel efficiency goals while meeting stringent safety requirements. This trend aligns with the industry’s broader move toward more electric aircraft architectures, where precise position sensing becomes even more critical for systems like electromechanical actuators replacing traditional hydraulics.

Advancements in Space Exploration Fueling Specialized Sensor Demand

Global investment in space programs has reached unprecedented levels, with both government agencies and private companies pursuing ambitious satellite constellations and deep space exploration missions. Position sensors serve vital functions in spacecraft attitude control, solar array positioning, and robotic arm operations. The growing small satellite market, projected to launch thousands of units annually, particularly benefits from compact, radiation-hardened position sensing solutions. Current space sensor designs increasingly incorporate redundancy and fault-tolerant features to meet the reliability demands of extended missions beyond Earth’s orbit.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Competition in Aerospace Position Sensors

The global aerospace position sensors market is characterized by a mix of established multinational corporations and specialized technology providers. Honeywell remains a dominant player, leveraging its extensive avionics expertise and strong relationships with aircraft manufacturers like Airbus and Boeing. The company’s position sensor solutions are widely adopted in commercial and military aviation, with a market share exceeding 18% in 2024.

Meggitt Sensing Systems and TE Connectivity have emerged as key competitors, particularly in the defense sector. Both companies benefited from increased military spending, which reached $2.2 trillion globally in 2023 according to SIPRI data. Their growth is further fueled by technological advancements in MEMS-based sensors and ruggedized designs for extreme aerospace environments.

The market also sees active participation from mid-sized specialists like Netzer Precision Position Sensors and Micro-Epsilon, who compete through niche innovations. These companies focus on high-accuracy solutions for flight control systems and landing gear positioning, where precision tolerances below 0.1° are often required.

Recent developments highlight the competitive dynamics, with TT Electronics acquiring Stemmer Imaging in 2023 to bolster its sensor capabilities. Meanwhile, Novanta expanded its aerospace portfolio through strategic partnerships with tier-1 avionics suppliers, reflecting the industry’s preference for integrated solutions.

List of Key Aerospace Position Sensor Companies

- Honeywell International Inc. (U.S.)

- Woodward, Inc. (U.S.)

- Meggitt Sensing Systems (U.K.)

- Crane Aerospace & Electronics (U.S.)

- Kavlico Corporation (U.S.)

- Althen Sensors & Controls (Netherlands)

- Circor Aerospace & Defense (U.S.)

- Novanta Inc. (U.S.)

- Netzer Precision Position Sensors (Israel)

- Novotechnik U.S., Inc. (U.S.)

- Smith Systems, Inc. (U.S.)

- Micro-Epsilon (Germany)

- TE Connectivity (Switzerland)

Segment Analysis:

By Type

Linear Position Sensors Dominate Due to Critical Role in Flight Control Systems

The market is segmented based on type into:

- Linear Position Sensors

- Subtypes: Potentiometric, Magnetostrictive, LVDT, and others

- Angle Position Sensors

- Subtypes: Optical encoders, Resolvers, Capacitive sensors, and others

- Rotary Position Sensors

- Multi-Axis Position Sensors

By Application

Military Aircraft Segment Leads Due to Increased Defense Spending Worldwide

The market is segmented based on application into:

- Military Aircraft

- Subtypes: Fighters, Transport aircraft, Helicopters

- Civil Aircraft

- Subtypes: Commercial airliners, Business jets, General aviation

- Spacecraft

- Unmanned Aerial Vehicles

By Technology

Non-Contact Sensors Gain Traction Owing to Higher Reliability and Durability

The market is segmented based on technology into:

- Contact Sensors

- Non-Contact Sensors

- Subtypes: Optical, Magnetic, Inductive, and others

- Hybrid Sensors

Regional Analysis: Position Sensors for The Aerospace Market

North America

The North American aerospace position sensors market is driven by strong defense budgets, commercial aircraft production recovery, and technological innovation. The U.S. dominates with a 78% regional market share, supported by major OEMs like Boeing and defense contractors requiring high-precision sensors for next-generation aircraft. With Airbus increasing A320 production to 65 monthly units and Boeing ramping up 737 MAX output, demand for reliable position sensing solutions is escalating. Regulatory standards like FAA AC 43.13-1B mandate strict sensor performance criteria, pushing suppliers toward advanced non-contact technologies. However, supply chain disruptions and semiconductor shortages remain key challenges for manufacturers.

Europe

Europe maintains a 22% global market share in aerospace position sensors, anchored by Airbus’s production hubs and stringent EASA certification requirements. The EU’s €1.2 billion Aerospace & Defense Fund is accelerating R&D in smart sensor technologies for applications like fly-by-wire systems. Countries like Germany and France lead in adopting magnetostrictive and optical encoders, particularly for military platforms like the Eurofighter. Despite strong demand, Brexit-related trade complexities and reliance on imported raw materials create operational hurdles. The region’s focus on sustainable aviation is also driving sensor miniaturization to reduce aircraft weight.

Asia-Pacific

APAC is the fastest-growing market, projected to achieve an 8.3% CAGR through 2032. China accounts for 41% of regional demand, fueled by COMAC’s expanding C919 program and 2,000+ domestic aircraft orders. India’s UDAN regional connectivity scheme and Japan’s focus on eVTOL sensors contribute to growth. While cost-competitive LVDT sensors dominate, there’s increasing adoption of advanced Hall-effect sensors for space applications. The lack of indigenous precision manufacturing capabilities and IP protection concerns remain barriers, though partnerships with global players like Honeywell are bridging technology gaps.

South America

The region shows moderate growth, with Brazil’s Embraer driving 68% of position sensor demand for executive jets and military trainers. A $3.7 billion investment in modernizing F-5M fighter avionics has created opportunities for angular position sensors. Chile and Colombia’s growing satellite programs also contribute to niche demand. Economic instability and currency fluctuations discourage long-term supplier commitments, leading to reliance on imported sensors from North America. The absence of local certification bodies further complicates market entry for foreign manufacturers.

Middle East & Africa

MEA’s market is bifurcated between Gulf States’ luxury aviation sectors and Africa’s maintenance-driven demand. The UAE leads with 32% regional share, thanks to MRO hubs like Dubai World Central requiring sensor retrofit solutions. Saudi Arabia’s Vision 2030 is catalyzing investments in localized aerospace manufacturing, though sensor technologies remain import-dependent. South Africa’s Denel Aviation provides consistent military demand, while Ethiopian Airlines’ expansion supports commercial fleet sensor needs. Political instability in North Africa and underdeveloped supply networks limit growth potential outside key markets.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Position Sensors for the Aerospace markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Linear Position Sensor, Angle Position Sensor), application (Military Aircraft, Civil Aircraft), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of 25+ leading market participants including Honeywell, Woodward Inc., and Meggitt Sensing System, covering product portfolios and strategic developments.

- Technology Trends: Assessment of emerging sensor technologies, miniaturization trends, and integration with avionics systems.

- Market Drivers & Restraints: Analysis of factors including increasing aircraft production rates (Airbus targeting 75 A320s/month by 2025) and stringent aviation safety regulations.

- Stakeholder Analysis: Strategic insights for aerospace OEMs, sensor manufacturers, and technology providers in this USD billion market.

The research methodology combines primary interviews with aerospace experts and analysis of verified industry data from regulatory bodies and corporate disclosures.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Position Sensors for Aerospace Market?

-> Position Sensors for The Aerospace Market size was valued at US$ 1.76 billion in 2024 and is projected to reach US$ 3.28 billion by 2032, at a CAGR of 9.3% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Major players include Honeywell, Woodward Inc., Meggitt Sensing Systems, Crane Aerospace & Electronics, and TT Electronics, holding over 45% combined market share.

What are the key growth drivers?

-> Primary drivers include increasing aircraft production (Airbus/Ramprate increases), modernization of military fleets, and advancements in sensor precision technologies.

Which region dominates the market?

-> North America leads with 38% market share (2024), while Asia-Pacific shows fastest growth at 7.2% CAGR due to expanding aviation sectors in China and India.

What are the emerging technology trends?

-> Emerging trends include fiber-optic position sensors, contactless magnetic sensing, and integration with aircraft health monitoring systems for predictive maintenance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...