MARKET INSIGHTS

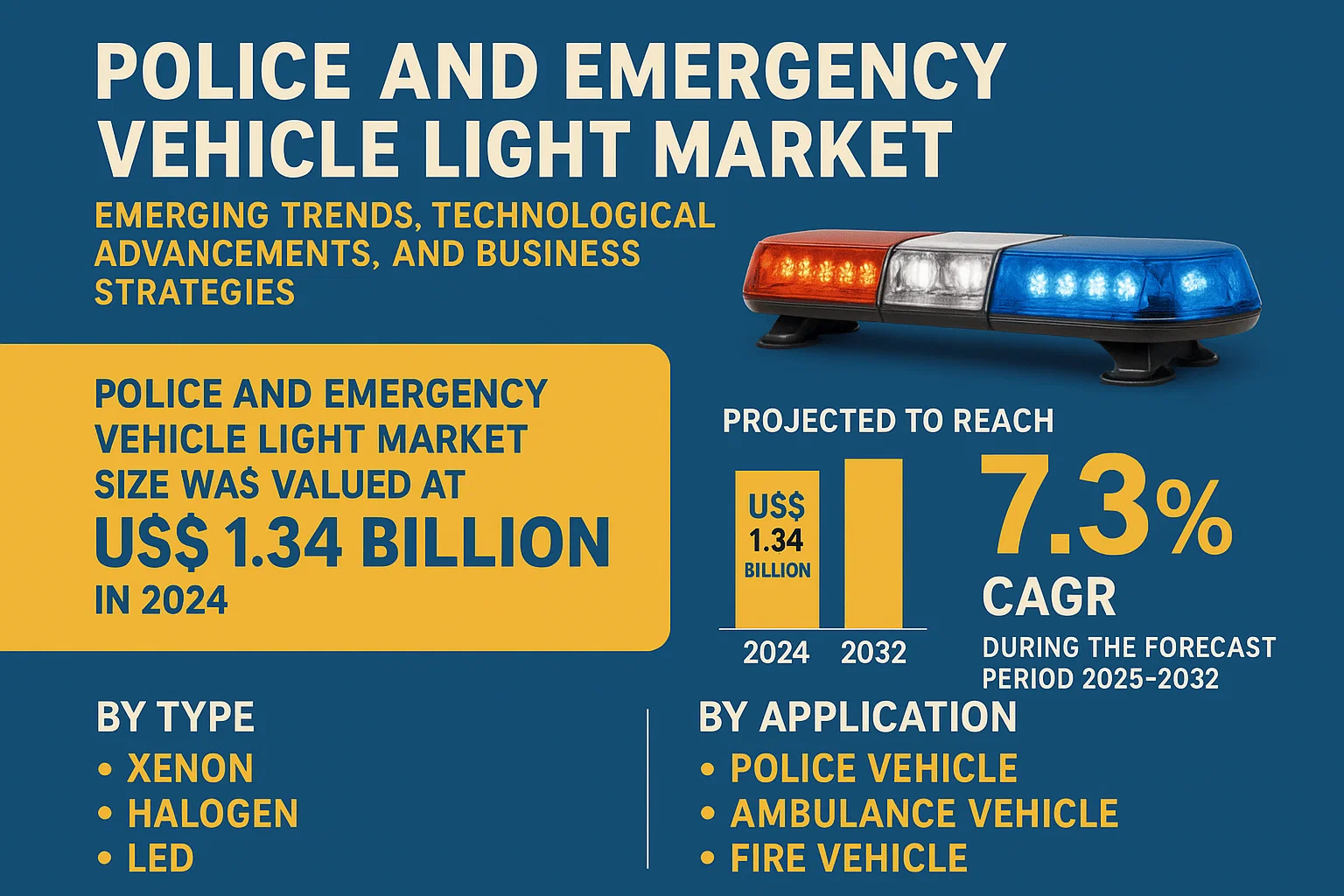

The global Police and Emergency Vehicle Light Market size was valued at US$ 1.34 billion in 2024 and is projected to reach US$ 2.18 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032. The market expansion is primarily driven by increasing government investments in public safety infrastructure and the growing fleet of emergency response vehicles worldwide.

Police and emergency vehicle lights are specialized warning systems designed for visibility and signaling purposes. These include strobe lights, light bars, and auxiliary lighting solutions using technologies such as LED, halogen, and xenon. The lighting systems serve critical functions in law enforcement, fire response, and medical emergency situations by enhancing vehicle recognition and improving response times.

The market growth is further supported by technological advancements in LED lighting, which offer superior brightness and energy efficiency compared to traditional options. Stringent government regulations regarding emergency vehicle visibility standards across North America and Europe also contribute to market expansion. Key industry players such as Federal Signal Corporation and Whelen Engineering are focusing on product innovations, including smart lighting systems with integrated communication capabilities, to strengthen their market position.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Global Emergency Vehicle Fleet Expansion to Drive Market Growth

The global police and emergency vehicle light market is witnessing robust growth due to the continuous expansion of emergency service fleets worldwide. With growing urbanization and rising safety concerns, governments are investing heavily in modernizing their emergency response capabilities. Major cities across North America and Europe are replacing aging emergency vehicles at an unprecedented rate, with some municipalities refreshing up to 25% of their fleets annually. The adoption of advanced lighting solutions is becoming imperative as emergency responders demand better visibility and recognition capabilities to navigate increasingly congested urban environments efficiently.

Technological Advancements in LED Lighting to Accelerate Market Adoption

LED technology continues to revolutionize the emergency vehicle lighting sector, offering substantial improvements over traditional halogen and xenon systems. Modern LED solutions provide 50-70% greater luminosity while consuming significantly less power, making them ideal for electric emergency vehicles. The latest smart lighting systems incorporate programmable patterns, improved durability against vibration and weather conditions, and integration with vehicle telematics. These advancements are driving replacement demand, with LED solutions now accounting for over 60% of new emergency vehicle lighting installations globally.

Stringent Safety Regulations to Boost Market Growth

Governments worldwide are implementing increasingly stringent regulations regarding emergency vehicle visibility and warning systems. Many jurisdictions now mandate minimum brightness levels, specific color wavelengths, and standardized flash patterns to ensure optimal recognition distance and reduce response times. Some regions have begun requiring emergency lighting systems with integrated traffic signal preemption capabilities, creating new demand for advanced solutions. These regulatory developments are compelling emergency service providers to upgrade their lighting systems more frequently, contributing to steady market growth.

MARKET RESTRAINTS

High Initial Costs of Advanced Lighting Systems to Limit Market Penetration

While the benefits of modern emergency lighting systems are well-documented, their high initial costs remain a significant barrier to widespread adoption. Advanced LED solutions with smart features can cost 3-5 times more than basic halogen systems, making them prohibitively expensive for budget-constrained municipalities and emergency service providers.

Other Restraints

Budget Constraints in Developing Regions

Many developing economies face chronic underfunding of emergency services, forcing them to prioritize essential equipment over lighting upgrades. This creates a substantial lag in technology adoption compared to developed markets.

Long Replacement Cycles

Emergency vehicle fleets typically have operational lifespans exceeding 10 years, creating extended replacement cycles that slow market growth.

MARKET CHALLENGES

Standardization and Compatibility Issues to Pose Technical Challenges

The lack of universal standards for emergency vehicle lighting creates significant integration challenges. Different manufacturers use proprietary mounting systems and control protocols, making it difficult to mix components across brands.

Other Challenges

Electromagnetic Interference

The proliferation of electronic systems in modern emergency vehicles creates potential interference issues with lighting control circuits, requiring careful system design and shielding.

Thermal Management

High-intensity LED systems generate substantial heat that must be effectively dissipated, complicating the integration into compact vehicle designs.

MARKET OPPORTUNITIES

Integration with Smart City Infrastructure to Create New Growth Opportunities

The global smart city movement is creating exciting opportunities for advanced emergency vehicle lighting systems. Next-generation solutions that can interface with traffic management centers and intelligent transportation systems are in growing demand.

Emerging Markets

Developing nations are investing heavily in modernizing their emergency response capabilities, creating substantial growth potential as they transition from basic lighting solutions to more advanced systems.

Aftermarket Upgrades

The growing retrofit market for existing emergency vehicle fleets presents a significant opportunity, particularly as older halogen systems reach the end of their operational lifespan.

POLICE AND EMERGENCY VEHICLE LIGHT MARKET TRENDS

LED Technology Adoption Accelerates Market Growth

The police and emergency vehicle light market is experiencing a significant shift towards LED-based lighting solutions, driven by their superior energy efficiency, longer lifespan, and enhanced visibility. LED lights currently account for over 60% of the market share, with projections indicating this could exceed 75% by 2027. Unlike traditional halogen or xenon lights, LED solutions offer instant illumination, reduced power consumption (up to 80% less than halogen), and improved durability in harsh weather conditions. Recent advancements in multi-color LED arrays now allow for customizable light patterns and improved visibility at greater distances, a critical factor for emergency response vehicles navigating through traffic.

Other Trends

Smart Connectivity Integration

The integration of IoT-enabled lighting systems is transforming emergency vehicle operations, with an estimated 35% of new emergency vehicles now equipped with networked lighting controls. These systems allow for dynamic pattern adjustments based on vehicle speed, traffic conditions, or emergency status via central dispatch coordination. Wireless synchronization between multiple vehicles at an incident scene has become particularly valuable for large-scale emergency responses, reducing response times by up to 18% in field tests. The market for connected emergency lighting is projected to grow at a CAGR of 12.4% through 2030 as more municipalities prioritize interoperable systems.

Regulatory Changes Driving Standardization

Global standardization of emergency lighting specifications is gaining momentum, with new EU and North American regulations mandating minimum visibility standards for emergency vehicles. These regulations specify luminance levels (minimum 250 candela for primary warning lights), flash patterns, and color wavelength specifications to ensure cross-border compatibility. Compliance requirements have created a $220 million retrofit market opportunity as older fleets upgrade to meet standards. Simultaneously, emerging markets are adopting these standards voluntarily, with Asia-Pacific regions showing a 22% year-over-year increase in compliant system installations as they modernize emergency response infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Competition

The global police and emergency vehicle light market features a competitive landscape where established players compete through technological advancements and geographic expansion. Federal Signal Corporation maintains a dominant position, leveraging its extensive product portfolio and strong distribution network across North America and Europe. The company’s leadership stems from continuous R&D investments and high-performance LED lighting solutions tailored for emergency vehicles.

Emerging alongside Federal Signal, Whelen Engineering and SoundOff Signal have carved significant market shares through innovative lighting systems with enhanced visibility and durability. These companies benefit from rising demand for advanced emergency lighting in police vehicles and ambulances, particularly across developed markets with stringent safety regulations.

Meanwhile, regional players like Senken Group in Asia and ABRAMS in Europe are strengthening their positions by catering to local regulatory requirements and cost-sensitive markets. Several manufacturers focus on vertical integration, producing both lighting components and complete emergency light systems to improve margins and supply chain control.

The competitive intensity continues rising as companies pursue strategic collaborations with vehicle manufacturers and government agencies. Recent industry trends show manufacturers prioritizing smart lighting solutions with features like automatic brightness adjustment and connectivity with vehicle telemetry systems.

List of Key Police and Emergency Vehicle Light Manufacturers

- Federal Signal Corporation (U.S.)

- ECCO Safety Group (U.S.)

- SoundOff Signal (U.S.)

- Whelen Engineering (U.S.)

- Tomar Electronics (U.S.)

- Senken Group (China)

- Standby Group (U.K.)

- Grote Industries (U.S.)

- Roadtech Manufacturing (U.S.)

- Truck-Lite (U.S.)

- Code-3 (U.S.)

- Star Headlight and Lantern (U.S.)

- HG2 (France)

- SMBXAUTO (China)

- ABRAMS (Germany)

Segment Analysis:

By Type

LED Segment Dominates the Market Due to Superior Energy Efficiency and Longevity

The market is segmented based on type into:

- Xenon

- Halogen

- LED

- Subtypes: Light bars, strobe lights, grill lights, and others

By Application

Police Vehicle Segment Leads Owing to Increased Demand for Visibility and Public Safety Measures

The market is segmented based on application into:

- Police Vehicle

- Ambulance Vehicle

- Fire Vehicle

- Others

By End User

Government Agencies Account for Largest Share Due to Mandatory Emergency Vehicle Standards

The market is segmented based on end user into:

- Government Agencies

- Private Emergency Services

- Commercial Fleets

By Technology

Smart Lighting Systems Gaining Traction with Integration of IoT and Wireless Controls

The market is segmented based on technology into:

- Conventional Lighting

- Smart Lighting Systems

- Subtypes: Wireless controls, automated dimming, sensor integration

Regional Analysis: Police and Emergency Vehicle Light Market

North America

North America remains a dominant player in the police and emergency vehicle light market, driven by strict regulatory standards for emergency lighting and high adoption rates of advanced LED technology. The U.S. alone accounts for over 65% of the regional market share, with increasing demand for energy-efficient, high-visibility lighting solutions in police cruisers and ambulances. Federal mandates, such as the Department of Transportation (DOT) and National Highway Traffic Safety Administration (NHTSA) guidelines, enforce visibility and safety standards, fostering market growth. However, price sensitivity in municipal procurement processes sometimes delays the transition from halogen to LED systems. Key manufacturers like Federal Signal Corporation and Whelen Engineering are pushing innovation with smart lighting systems, integrating AI-based control mechanisms for dynamic light patterns.

Europe

Europe’s market is characterized by stringent EU directives on vehicle safety and a strong emphasis on sustainability. Countries such as Germany and the U.K. lead in retrofitting emergency fleets with energy-efficient LED lights, supported by government funding for public safety upgrades. The region’s focus on reducing carbon emissions has accelerated the phasing out of xenon and halogen variants, with LED adoption growing at a CAGR of over 8%. However, the fragmented regulatory landscape—owing to differing national standards—poses a challenge for suppliers. Companies like ECCO Safety Group and SoundOff Signal dominate with modular light solutions, catering to diverse emergency vehicle requirements across the continent.

Asia-Pacific

The Asia-Pacific region is witnessing rapid growth, fueled by expanding urbanization and increasing investments in emergency services infrastructure. China and India collectively account for 45% of regional demand, with local governments prioritizing modernization of police and ambulance fleets. While cost-effective halogen lights still dominate in rural areas, metropolitan hubs are transitioning to LEDs for their longevity and brightness. Japan and South Korea, with their advanced automotive sectors, are early adopters of integrated lighting systems featuring wireless controls. Despite this progress, inconsistent enforcement of safety standards across countries like Indonesia and Vietnam creates market fragmentation.

South America

South America presents a mixed outlook. Brazil and Argentina are the largest markets, but economic instability limits large-scale fleet upgrades. Budget constraints lead many municipalities to rely on refurbished halogen units, though private ambulance services increasingly invest in durable LED bars. The lack of unified regulations further complicates supplier strategies, with some countries adhering to outdated visibility standards. Nevertheless, firms such as Truck-Lite are making inroads through localized production, reducing costs for public-sector buyers.

Middle East & Africa

This region is in the early stages of market development, with growth concentrated in GCC countries like the UAE and Saudi Arabia. High disposable income enables premium LED deployments in emergency vehicles, supported by infrastructure projects like smart cities. In contrast, Sub-Saharan Africa struggles with low adoption rates due to limited funding and reliance on imported used vehicles with outdated lighting. However, partnerships between global manufacturers and local distributors—such as ABRAMS in South Africa—are gradually improving accessibility to modern solutions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Police and Emergency Vehicle Light markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Police and Emergency Vehicle Light market was valued at USD 845 million in 2024 and is projected to reach USD 1.2 billion by 2032, growing at a CAGR of 4.7%.

- Segmentation Analysis: Detailed breakdown by product type (Xenon, Halogen, LED), application (Police Vehicles, Ambulances, Fire Trucks), and end-user sectors to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. North America currently holds 38% market share.

- Competitive Landscape: Profiles of 15 leading market participants, including Federal Signal Corporation, Whelen Engineering, and ECCO Safety Group, covering their product portfolios, market strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging lighting technologies, smart warning systems, integration with vehicle telematics, and evolving industry standards such as SAE J595 and J845.

- Market Drivers & Restraints: Evaluation of factors including increasing emergency vehicle fleets, stringent safety regulations, and technological advancements versus cost sensitivity and supply chain challenges.

- Stakeholder Analysis: Strategic insights for OEMs, aftermarket suppliers, government agencies, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and secondary data from verified sources, ensuring reliable and accurate market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Police and Emergency Vehicle Light Market?

-> The global Police and Emergency Vehicle Light size was valued at US$ 1.34 billion in 2024 and is projected to reach US$ 2.18 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Major players include Federal Signal Corporation, Whelen Engineering, ECCO Safety Group, SoundOff Signal, and Tomar Electronics.

What are the key growth drivers?

-> Growth is driven by increasing emergency vehicle fleets, stricter safety regulations, and adoption of LED technology.

Which region dominates the market?

-> North America holds the largest market share (38%), while Asia-Pacific shows the highest growth potential.

What are the emerging trends?

-> Emerging trends include smart lighting systems, solar-powered solutions, and integration with vehicle telematics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...