Photonic Integrated Circuits Market Insights

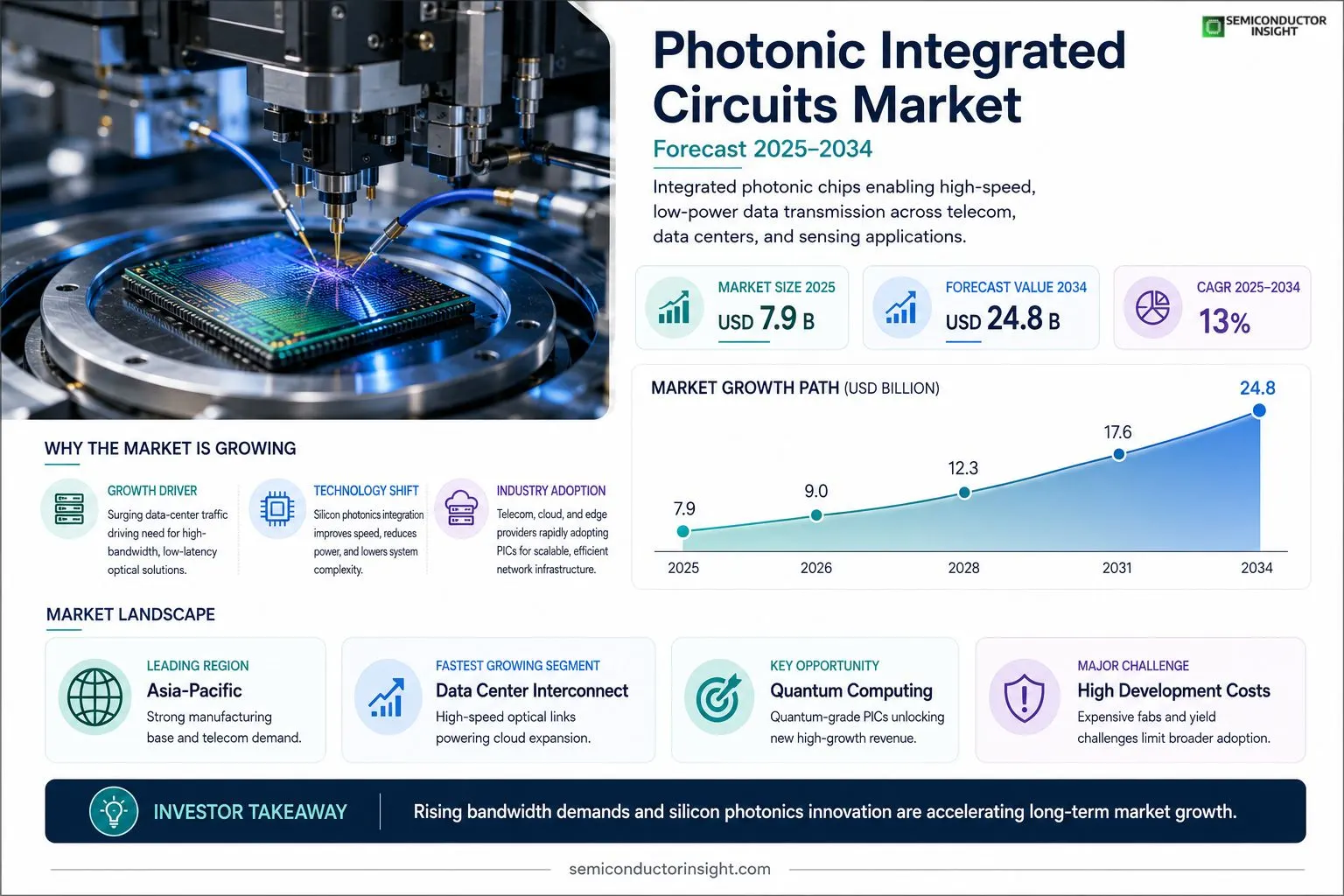

Global photonic integrated circuits market size was valued at USD 7.9 billion in 2025. The market is projected to grow from USD 8.0 billion in 2025 to USD 24.8 billion by 2034, exhibiting a CAGR of approximately 13% during the forecast period.

Photonic integrated circuits (PICs) are semiconductor devices that integrate multiple optical components,such as lasers, modulators, detectors, and waveguides,onto a single chip, enabling high‑speed data transmission and reduced power consumption for telecommunications, data centers, and sensing applications.The market is experiencing rapid growth because of escalating demand for bandwidth‑intensive services, increased investment in silicon photonics research, and the rollout of advanced optical networks worldwide. Furthermore, strategic collaborations,like Intel’s partnership with IBM on silicon‑photonic platforms announced in March 2024,and the expansion of product portfolios by leaders such as Lumentum Holdings Inc., II‑VI Incorporated, and NeoPhotonics are further fueling adoption across telecom operators and cloud service providers.

MARKET DRIVERS

Rising Data‑Center Bandwidth Demand

Photonic Integrated Circuits Market is being propelled by exponential growth in data‑center traffic, which is projected to exceed 120 EB per year by 2028. Operators adopt photonic chips to achieve low‑latency and energy‑efficient interconnects, reducing power consumption by up to 70 % compared with traditional copper solutions.

Expansion of 5G and Edge Computing

Deployment of 5G networks and edge‑computing nodes requires high‑speed optical transceivers that can be integrated onto a single chip. This trend is forecast to increase Photonic Integrated Circuits Market CAGR to roughly 15 % through 2032, as telecom operators seek compact, scalable solutions.

➤ Industry analysts estimate that photonic integration could capture more than 30 % of the total optical module market by 2027.

In addition, government initiatives promoting quantum information processing and Lidar for autonomous vehicles are creating new demand corridors, further fortifying the market outlook.

MARKET CHALLENGES

High Development Costs

Designing and qualifying photonic chips involves sophisticated fabrication facilities, often costing upwards of $150 million per fab. These capital expenditures limit participation to a handful of well‑funded players, slowing broader adoption.

Other Challenges

Manufacturing Yield Variability

Achieving consistent wafer‑level yields remains difficult due to intricate waveguide alignment and material heterogeneity, leading to price pressures and longer time‑to‑market.

MARKET RESTRAINTS

Limited Standardization

Without universally accepted standards for photonic packaging and interface specifications, system integrators face compatibility hurdles. This lack of harmonization restrains the speed at which Photonic Integrated Circuits Market can scale across diverse applications.

MARKET OPPORTUNITIES

Emerging Quantum Computing Platforms

Quantum processors rely on precise optical control, positioning photonic integrated circuits as essential enablers. Investment in quantum‑grade photonic foundries is expected to open a $5 billion revenue stream within the next five years, presenting a high‑growth opportunity for early entrants.

Photonic Integrated Circuits Market Trends

Escalating Bandwidth Demand Drives PIC Adoption

Photonic Integrated Circuits Market is responding to a surge in bandwidth‑intensive services such as 5G, hyperscale cloud workloads, and high‑resolution video streaming. By integrating lasers, modulators, detectors and waveguides on a single chip, photonic integrated circuits reduce power consumption while delivering terabit‑per‑second data rates. Telecom operators and data‑center providers are prioritizing solutions that minimize latency and energy costs, prompting a rapid shift from discrete optical components to highly integrated silicon‑photonic platforms. This transition supports the broader goal of expanding network capacity without proportionally increasing infrastructure footprints.

Other Trends

Strategic Partnerships and Silicon‑Photonic Research

Collaborations are accelerating market momentum. Intel’s partnership with IBM, announced in March 2024, focuses on co‑developing silicon‑photonic transceivers that target cloud service providers seeking scalable interconnects. Simultaneously, leaders such as Lumentum Holdings, II‑VI Incorporated and NeoPhotonics are expanding product portfolios to include next‑generation modulators and wavelength‑multiplexed transceivers. These alliances combine deep semiconductor expertise with advanced packaging capabilities, shortening time‑to‑market for high‑performance PICs. The resulting ecosystem fosters a virtuous cycle of investment, where research funding translates into commercially viable components that further stimulate demand across telecom and data‑center segments.

Emerging Applications in Data‑Center Networking and Sensing

Beyond traditional telecommunications, Photonic Integrated Circuits Market is witnessing growth in data‑center networking and sensing applications. Cloud operators are deploying PIC‑based optical switches to achieve higher port densities and lower energy per bit, directly impacting operational expenditures. In parallel, silicon‑photonic sensors are being integrated into environmental monitoring and biomedical devices, leveraging the same chip‑scale technology to detect minute optical signals with high precision. These cross‑industry deployments diversify revenue streams and encourage manufacturers to adopt flexible design architectures that can be repurposed for multiple end‑markets, reinforcing the market’s resilience and long‑term growth trajectory.

COMPETITIVE LANDSCAPEKey Industry Players

Photonic Integrated Circuits Market – Competitive Overview

Photonic Integrated Circuits (PIC) Market, valued at USD 7.9 billion in 2025, is dominated by a handful of vertically integrated firms that combine silicon‑photonic foundry capabilities with system‑level packaging. Intel leads the landscape, leveraging its silicon‑photonic platform and strategic partnership with IBM to accelerate data‑center deployments. This leadership is reinforced by substantial R&D spend and a broad IP portfolio that spans lasers, modulators, and detectors. The market structure reflects a semi‑consolidated model where large incumbents such as Intel, Lumentum Holdings, and II‑VI Incorporated command significant revenue share, while a growing ecosystem of specialized suppliers supports niche applications in telecom, aerospace, and sensing.Beyond the primary leaders, a vibrant set of niche and emerging players enhances the competitive dynamics. NeoPhotonics and Infinera focus on high‑performance coherent transceivers, while Acacia Communications (now part of Cisco) supplies advanced optical modules for carrier networks. Ciena and Nokia contribute extensive optical networking expertise, integrating PICs into their broader portfolio. STMicroelectronics, GlobalFoundries, and Sumitomo offer foundry services that enable custom silicon‑photonic designs, and NTT Electronics provides advanced packaging solutions. These firms, together with regional specialists such as Huawei and Fujitsu, drive innovation through collaborations, diversified product roadmaps, and targeted market penetration across data‑center, telecom, and emerging quantum‑photonic segments.

List of Key Photonic Integrated Circuits Companies Profiled

- Intel Corporation

- Lumentum Holdings Inc.

- II‑VI Incorporated

- NeoPhotonics Corp.

- Infinera Corporation

- Acacia Communications

- Ciena Corporation

- Nokia Corporation

- STMicroelectronics

- GlobalFoundries

- Sumitomo Electric Industries

- NTT Electronics

- Huawei Technologies Co., Ltd.

- Fujitsu Ltd.

- Broadcom Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon photonic PICs

|

| By Application |

|

Data center interconnect

|

| By End User |

|

Cloud service providers

|

| By Technology |

|

Passive waveguide integration

|

| By Market Driver |

|

Escalating bandwidth demand

|

Regional Analysis: North America

United States

The telecommunications sector is a primary driver for Photonic Integrated Circuits, with increasing demand for high-bandwidth communication networks. PICs enable greater efficiency and lower costs in optical transmission systems, supporting 5G and future network generations. Analysis reveals a continuous need for enhanced optical components within telecom infrastructure.

The rapid expansion of data centers and cloud computing facilities is creating substantial demand for PICs. These components are crucial for high-speed data transfer within data centers and for interconnecting them across geographical locations. The need for energy-efficient and scalable optical solutions is a key trend in this segment.

Beyond telecommunications and data centers, Photonic Integrated Circuits are finding increasing applications in industrial automation, environmental monitoring, and medical sensing. Their ability to provide precise and real-time data acquisition is driving adoption in these diverse fields. This expanding application scope presents significant growth opportunities.

The automotive and defense sectors are exploring the use of PICs for advanced sensor systems, LiDAR technology, and secure communication. The demand for compact, reliable, and high-performance optical components within these applications is expected to grow in the coming years.

Europe

Europe represents a significant market for Photonic Integrated Circuits, characterized by strong research capabilities, particularly in Germany, France, and the UK. The region’s focus on sustainable technologies and advanced manufacturing is fostering innovation in PIC design and manufacturing. The automotive industry in Europe also presents a growing opportunity for PIC applications. Regional research collaborations are enhancing the development of next-generation PICs.

Asia-Pacific

Asia-Pacific is emerging as a major growth hub for Photonic Integrated Circuits Market. Countries like China, Japan, and South Korea are investing heavily in semiconductor manufacturing and optical communication infrastructure. The burgeoning telecommunications sector in China and the increasing demand for data centers across the region are driving the adoption of PICs. The competitive landscape in Asia-Pacific is intense, with numerous domestic and international players vying for market share.

South America

Photonic Integrated Circuits Market in South America is relatively nascent but holds potential for growth. The expansion of telecommunications networks and increasing investments in data infrastructure are expected to drive demand. The region’s growing industrial sector also presents opportunities for PIC applications in sensing and automation. Government initiatives supporting digital infrastructure development will play a key role in fostering market growth.

Middle East & Africa

Photonic Integrated Circuits Market in the Middle East & Africa is characterized by increasing investments in telecommunications and infrastructure development. The growing demand for high-bandwidth communication and the expansion of data centers are key drivers. The region presents emerging opportunities for PIC adoption in various sectors, including oil and gas, defense, and healthcare. Government initiatives focused on digital transformation are expected to further stimulate market growth.

Report Scope

This market research report provides a comprehensive analysis of the Photonic Integrated Circuits Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Photonic Integrated Circuits Market?

-> Photonic Integrated Circuits Market was valued at USD 7.9 billion in 2025 and is expected to reach USD 24.8 billion by 2034.

Which key companies operate in Photonic Integrated Circuits Market?

-> Key players include Lumentum Holdings Inc., II‑VI Incorporated, NeoPhotonics, Intel, IBM, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for bandwidth‑intensive services, increased investment in silicon photonics research, and the global rollout of advanced optical networks.

Which region dominates the market?

-> Asia‑Pacific shows rapid adoption, while North America and Europe remain major markets.

What are the emerging trends?

-> Emerging trends include silicon‑photonic platform collaborations, integration of AI/IoT into photonic designs, and expanding data‑center interconnect solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...