MARKET INSIGHTS

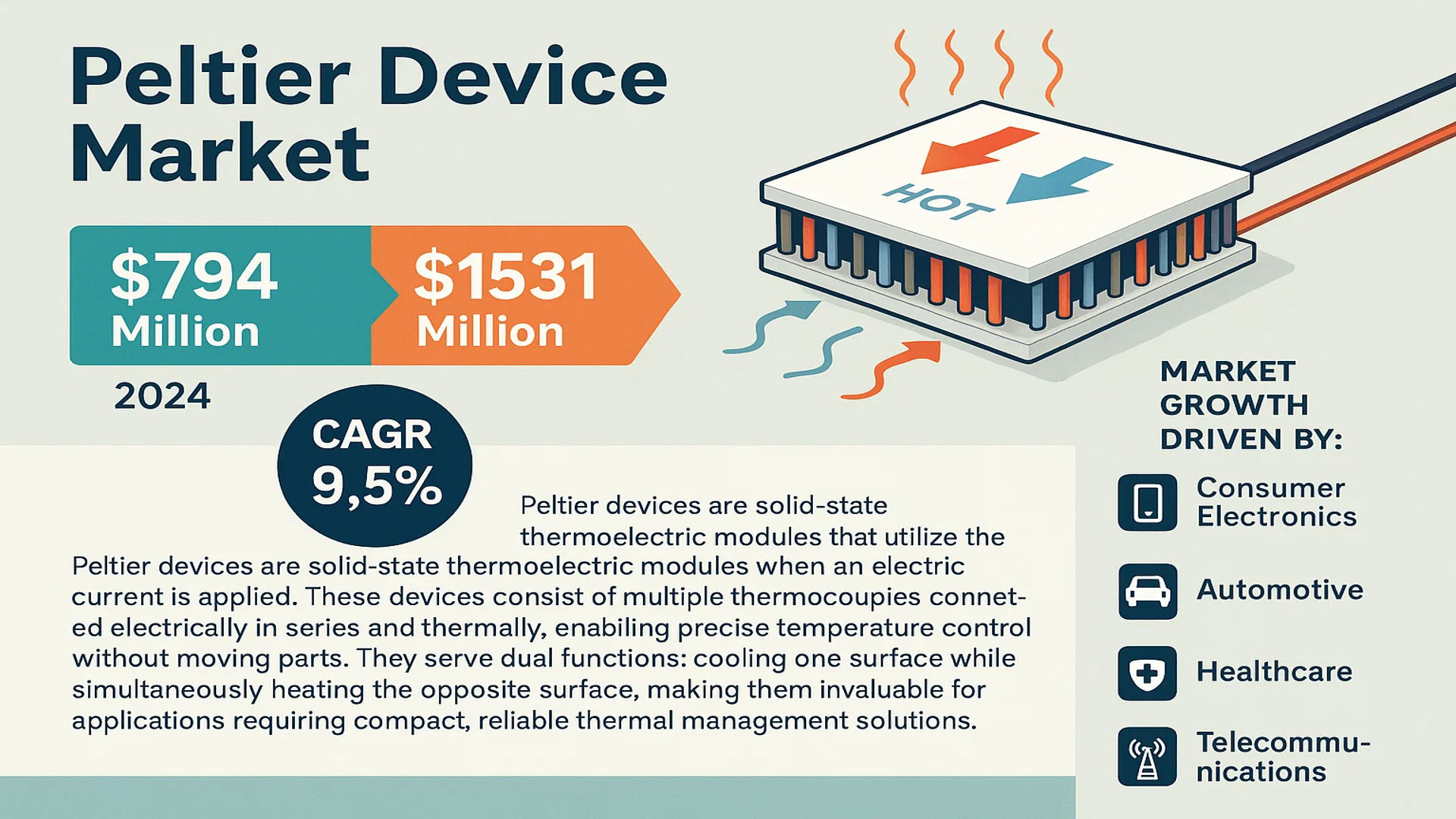

The global Peltier Device Market was valued at 794 million in 2024 and is projected to reach US$ 1531 million by 2032, at a CAGR of 9.5% during the forecast period.

Peltier devices are solid-state thermoelectric modules that utilize the Peltier effect to transfer heat between two surfaces when an electric current is applied. These devices consist of multiple thermocouples connected electrically in series and thermally in parallel, enabling precise temperature control without moving parts. They serve dual functions: cooling one surface while simultaneously heating the opposite surface, making them invaluable for applications requiring compact, reliable thermal management solutions.

The market growth is driven by increasing demand across industries such as consumer electronics, automotive, healthcare, and telecommunications. The rise of 5G infrastructure, electric vehicles, and advanced medical equipment has particularly accelerated adoption. Furthermore, technological advancements in semiconductor materials and manufacturing processes are enhancing device efficiency, broadening their application scope. Key players like Ferrotec, Laird Thermal Systems, and TE Technology continue to innovate, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for Compact Thermal Management Solutions to Propel Market Growth

The increasing miniaturization of electronic devices across consumer electronics, medical equipment, and automotive applications is driving substantial demand for Peltier devices. These solid-state heat transfer solutions provide precise temperature control without moving parts, making them ideal for space-constrained applications. The global consumer electronics market, valued at approximately $1 trillion in 2024, continues to demand more efficient cooling solutions as device power densities increase. In medical applications, Peltier devices enable precise temperature stabilization for analytical instruments and portable medical devices, with the medical equipment market projected to exceed $800 billion by 2026.

Rise of 5G Infrastructure and Electric Vehicles to Accelerate Adoption

The global rollout of 5G networks and rapid growth in electric vehicle (EV) production present significant opportunities for Peltier device integration. 5G base stations require efficient thermal management systems to maintain optimal operating temperatures for sensitive components, with annual deployments expected to surpass 7 million units worldwide by 2027. In the automotive sector, EV battery management systems and onboard electronics increasingly utilize Peltier devices for temperature regulation, particularly as EV production is forecast to grow at a CAGR of 22% between 2024-2032.

Advancements in Thermoelectric Materials to Enhance Efficiency

Recent breakthroughs in thermoelectric materials have significantly improved the coefficient of performance (COP) of Peltier devices, making them more energy-efficient for various applications. Developments in nanostructured bismuth telluride alloys and other advanced semiconductor materials have enabled temperature differentials exceeding 70°C in some commercial modules. These material innovations, coupled with improved manufacturing techniques, have reduced unit costs while improving reliability, making Peltier technology more accessible across multiple industries.

MARKET RESTRAINTS

Energy Efficiency Concerns to Limit Widespread Adoption

Despite technological advancements, Peltier devices still face limitations in energy efficiency compared to traditional refrigeration systems. Typical commercial modules operate at 5-10% of Carnot efficiency, significantly lower than compressor-based systems. This performance gap makes them less competitive for applications requiring large cooling capacities, restricting their use primarily to small-scale temperature control scenarios. Energy consumption concerns are particularly problematic in battery-powered applications where power efficiency is paramount.

High-Performance Semiconductor Material Costs to Impact Affordability

The specialized semiconductor materials required for high-performance Peltier devices, particularly bismuth telluride, remain expensive due to limited global supply and complex manufacturing processes. Material costs account for approximately 40-60% of total module production expenses, keeping end-user prices relatively high compared to alternative cooling solutions. This cost factor makes price-sensitive markets hesitant to adopt Peltier technology for mass-market applications, despite its technical advantages.

MARKET CHALLENGES

Thermal Cycling and Reliability Issues to Pose Usage Barriers

Peltier devices experience significant thermal stress during operation, particularly when subjected to frequent power cycling or extreme temperature differentials. This can lead to mechanical failure at solder joints and electrical contacts, reducing operational lifespan. Manufacturers report average failure rates of 5-15% within the first five years of operation for standard modules, though high-reliability versions for medical and military applications demonstrate better performance with failure rates below 3%.

Integration Complexities to Hinder Implementation

The effective implementation of Peltier devices requires careful system design, including proper heat sinking, power regulation, and thermal interface management. Many end-users lack the expertise to properly integrate these components, leading to suboptimal performance and premature failures. The industry has observed that approximately 30% of field returns are attributed to improper installation rather than inherent product defects, creating a significant barrier to broader adoption.

MARKET OPPORTUNITIES

Expansion in Quantum Computing and AI Hardware to Create New Applications

The emerging markets for quantum computing and artificial intelligence hardware present promising opportunities for high-precision Peltier devices. Quantum computers require ultra-stable thermal environments with temperature control precision down to ±0.01°C, driving demand for advanced thermoelectric solutions. The global quantum computing market, projected to exceed $5 billion by 2030, could significantly boost adoption of specialized Peltier modules for quantum processor cooling applications.

Growing Industrial Automation to Drive Demand for Reliable Cooling Solutions

Industrial automation systems increasingly incorporate sensors, controllers, and communication modules that require precise thermal management. Peltier devices offer maintenance-free operation well-suited for industrial environments, with the global industrial automation market expected to grow at 8.9% CAGR through 2032. Manufacturers are developing ruggedized thermoelectric modules specifically designed for harsh industrial conditions, opening new market segments beyond traditional electronics cooling.

PELTIER DEVICE MARKET TRENDS

Growing Demand for Energy-Efficient Cooling Solutions Drives Peltier Device Adoption

The global Peltier device market is witnessing significant growth due to the rising demand for energy-efficient and compact cooling solutions across various industries. With an expanding consumer electronics sector, Peltier devices are increasingly being used in applications such as refrigerators, coolers, and wearable health monitors. Their solid-state design eliminates the need for refrigerants, making them environmentally friendly compared to traditional compressor-based cooling systems. The market is also benefiting from advancements in material science, leading to improved thermoelectric efficiency. For instance, developments in nanostructured semiconductor materials have enhanced heat absorption and dissipation capabilities, boosting the performance of Peltier devices in high-power applications.

Other Trends

Medical and Healthcare Applications

The medical sector is emerging as a key driver for Peltier device adoption, particularly in portable medical devices and laboratory equipment. Thermal regulation is critical in devices like PCR machines, blood analyzers, and cryogenic storage units. Peltier technology enables precise temperature control, ensuring stable conditions for sensitive biological samples. Additionally, wearable cooling patches integrated with Peltier elements are being explored for therapeutic applications, such as pain relief and localized cooling for burn injuries. The increasing focus on point-of-care diagnostics and portable healthcare solutions further amplifies demand, particularly in regions with limited access to advanced medical infrastructure.

Automotive Sector Embracing Peltier-Based Thermal Management

The automotive industry represents a rapidly growing segment for Peltier devices, particularly in electric and hybrid vehicles. As automakers seek innovative solutions to manage battery temperatures, Peltier modules are being integrated into battery thermal management systems (BTMS) to enhance efficiency and longevity. These devices help maintain optimal operating temperatures for lithium-ion batteries, improving performance and safety. Beyond EVs, Peltier technology is being adopted in climate-controlled seating, contributing to improved passenger comfort and luxury vehicle differentiation. The trend toward autonomous and connected vehicles will likely create additional opportunities, given the need to regulate temperature-sensitive electronic components in ADAS (Advanced Driver-Assistance Systems) and infotainment systems.

Industrial Automation and Consumer Electronics Innovation

Industrial applications are increasingly leveraging Peltier devices for precise temperature control in manufacturing processes, particularly in semiconductor fabrication and laser cooling. The ability to achieve sub-zero temperatures without mechanical components makes them ideal for sensitive industrial environments. Meanwhile, consumer electronics giants continue to integrate Peltier coolers in gaming consoles, high-end smartphones, and data center cooling solutions. The demand for smaller, quieter, and more power-efficient cooling mechanisms aligns perfectly with Peltier technology, ensuring sustained growth in this segment.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansions and Technological Innovation Drive Market Competition

The global Peltier Device Market is moderately fragmented, with a mix of multinational corporations, regional players, and emerging manufacturers vying for market share. Leading companies are focusing on R&D investments, strategic acquisitions, and geographic expansion to solidify their positions in this rapidly growing sector.

Ferrotec Corporation has emerged as a dominant player, capturing an estimated 18% revenue share in 2024. The company’s success stems from its vertically integrated manufacturing capabilities and extensive product portfolio spanning multiple industries. While Ferrotec maintains strongholds in consumer electronics and automotive applications, competitors are quickly closing the gap through targeted innovations.

North American leaders Laird Thermal Systems and TE Technology have fortified their market positions through technological advancements in high-efficiency modules. Meanwhile, Asian manufacturers like Guangdong Fuxin Technology and KYOCERA are gaining traction by offering cost-competitive solutions for mass-market applications. The European market sees strong representation from Kryotherm Industries, which specializes in custom thermoelectric solutions for industrial applications.

Recent market developments highlight intensifying competition: Coherent Corp (formerly II-VI Incorporated) acquired a smaller thermoelectrics specialist in Q1 2024 to expand its industrial cooling solutions, while Phononic secured $50 million in funding to accelerate development of next-generation solid-state cooling devices. These moves indicate the growing strategic importance of Peltier technology across multiple sectors.

The competitive landscape is further shaped by emerging players from China, such as Zhejiang Wangu Semiconductor and P&N Technology, which are rapidly capturing market share through aggressive pricing strategies and government-backed semiconductor initiatives. However, established players maintain advantages in reliability certifications and intellectual property portfolios.

List of Key Peltier Device Manufacturers Profiled

- Ferrotec Corporation (Japan)

- KELK Ltd. (Komatsu) (Japan)

- Coherent Corp (U.S.)

- Laird Thermal Systems (U.K.)

- Z-MAX (Japan)

- KJLP (South Korea)

- Thermion Company (U.S.)

- Phononic (U.S.)

- Guangdong Fuxin Technology (China)

- KYOCERA (Japan)

- Thermonamic Electronics (China)

- TE Technology (U.S.)

- Same Sky (formerly CUI Devices) (U.S.)

- Kryotherm Industries (Russia)

- Crystal Ltd (Russia)

Market competition is expected to intensify as manufacturers develop solutions for emerging applications in 5G infrastructure, electric vehicle battery management, and precision medical devices. Companies that successfully balance performance improvements with cost reductions will likely gain significant advantages in this evolving landscape.

Segment Analysis:

By Type

Single-Stage Peltier Devices Dominate Due to Widespread Adoption in Consumer Electronics and Automotive Applications

The market is segmented based on type into:

- Single-Stage

- Standard models

- Multi-Stage

- Cascade configurations

By Application

Consumer Electronics Leads Market Demand Owing to Growing Need for Compact Cooling Solutions

The market is segmented based on application into:

- Consumer electronics

- Automobile

- Healthcare

- Industrial

- Military

- Others

By Temperature Range

Standard Temperature Modules Maintain Market Dominance for Commercial Applications

The market is segmented based on temperature range into:

- Standard temperature range (-40°C to 85°C)

- Extended temperature range (below -40°C or above 85°C)

By End User

Electronics Manufacturers Represent Largest End-User Segment Due to High Volume Requirements

The market is segmented based on end user into:

- Electronics manufacturers

- Automotive OEMs

- Medical equipment producers

- Industrial equipment manufacturers

- Research institutions

Regional Analysis: Peltier Device Market

Asia-Pacific

The Asia-Pacific region dominates the global Peltier device market, driven by rapid industrialization and expanding electronics manufacturing. Countries like China, Japan, and South Korea lead in demand due to thriving consumer electronics, automotive, and telecommunications sectors. China alone accounts for over 40% of regional market share, supported by government initiatives like Made in China 2025 which prioritizes semiconductor and cooling technology advancements. The increasing adoption of 5G infrastructure and electric vehicles further accelerates Peltier device applications. However, market fragmentation and price competition among local manufacturers such as Guangdong Fuxin Technology and Zhejiang Wangu Semiconductor present challenges for premium product penetration.

North America

North America’s market growth stems from robust R&D investments and high-performance application requirements in medical devices, aerospace, and defense sectors. The U.S. constitutes nearly 80% of regional revenue, with companies like Laird Thermal Systems and Phononic leading innovation in miniature and multi-stage Peltier modules. Strict FDA regulations for medical equipment cooling solutions and DOE standards for energy-efficient devices shape product development trends. Though labor and production costs remain high, partnerships between academic institutions and manufacturers continue to drive Next-gen thermoelectric material research, particularly in solid-state refrigeration.

Europe

Europe maintains a strong focus on sustainable Peltier solutions, aligning with EU Green Deal objectives to reduce carbon emissions. Germany and France spearhead adoption in industrial automation and renewable energy systems, where precise thermal management is critical. Automotive applications are growing through collaborations between module suppliers like Ferrotec and electric vehicle manufacturers to optimize battery thermal regulation. While stringent RoHS and WEEE compliance increases production costs, it has incentivized development of lead-free and recyclable thermoelectric materials. The market faces moderate growth due to economic uncertainties but benefits from well-established supply chains across Eastern European manufacturing hubs.

South America

South America represents an emerging market where Brazil and Argentina show gradual uptake of Peltier devices, primarily in healthcare and food preservation applications. Limited local manufacturing capabilities create import dependency, though government tax incentives for electronics production are encouraging domestic players like Termoelectricos Brasil to expand operations. Economic volatility and currency fluctuations hinder large-scale investments, causing price sensitivity that favors cheaper single-stage modules over advanced multi-stage units. Infrastructure development in temperature-controlled logistics presents new opportunities, particularly for cold chain pharmaceutical distribution networks.

Middle East & Africa

The MEA region exhibits nascent demand concentrated in GCC countries and South Africa, where extreme climates drive cooling applications in telecom base stations and military equipment. UAE’s Smart City initiatives and Saudi Arabia’s Vision 2030 are fostering adoption in building automation systems. While the lack of localized component production necessitates imports from Asian suppliers, partnerships with distributors like Z-MAX are improving market access. Low awareness about energy-efficient thermal solutions and inadequate technical expertise remain significant barriers to widespread Peltier device implementation across the region’s industrial sectors.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Peltier Device markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Peltier Device market was valued at USD 794 million in 2024 and is projected to reach USD 1531 million by 2032, growing at a CAGR of 9.5%.

- Segmentation Analysis: Detailed breakdown by product type (single-stage vs. multi-stage), application (automotive, consumer electronics, healthcare, industrial, etc.), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets like China, US, Germany, Japan, and South Korea.

- Competitive Landscape: Profiles of 25+ leading market participants including Ferrotec, Laird Thermal Systems, KYOCERA, and TE Technology, covering their product portfolios, manufacturing capabilities, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging thermoelectric materials, integration with IoT systems, miniaturization trends, and efficiency improvements in Peltier module design.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for precision temperature control in electronics and medical devices versus challenges like energy efficiency limitations.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding supply chain dynamics and growth opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory bodies, company reports, and trade associations to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Peltier Device Market?

-> Peltier Device Market was valued at 794 million in 2024 and is projected to reach US$ 1531 million by 2032, at a CAGR of 9.5% during the forecast period.

Which key companies operate in Global Peltier Device Market?

-> Key players include Ferrotec, Laird Thermal Systems, Coherent Corp, KYOCERA, TE Technology, Guangdong Fuxin Technology, and Phononic, among others.

What are the key growth drivers?

-> Primary growth drivers include rising demand in consumer electronics cooling, medical device applications, and automotive temperature control systems, along with advancements in thermoelectric materials.

Which region dominates the market?

-> Asia-Pacific is both the largest and fastest-growing market, accounting for over 45% of global demand, driven by electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of high-efficiency thermoelectric materials, integration with IoT for smart cooling systems, and miniaturization for portable medical devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...