MARKET INSIGHTS

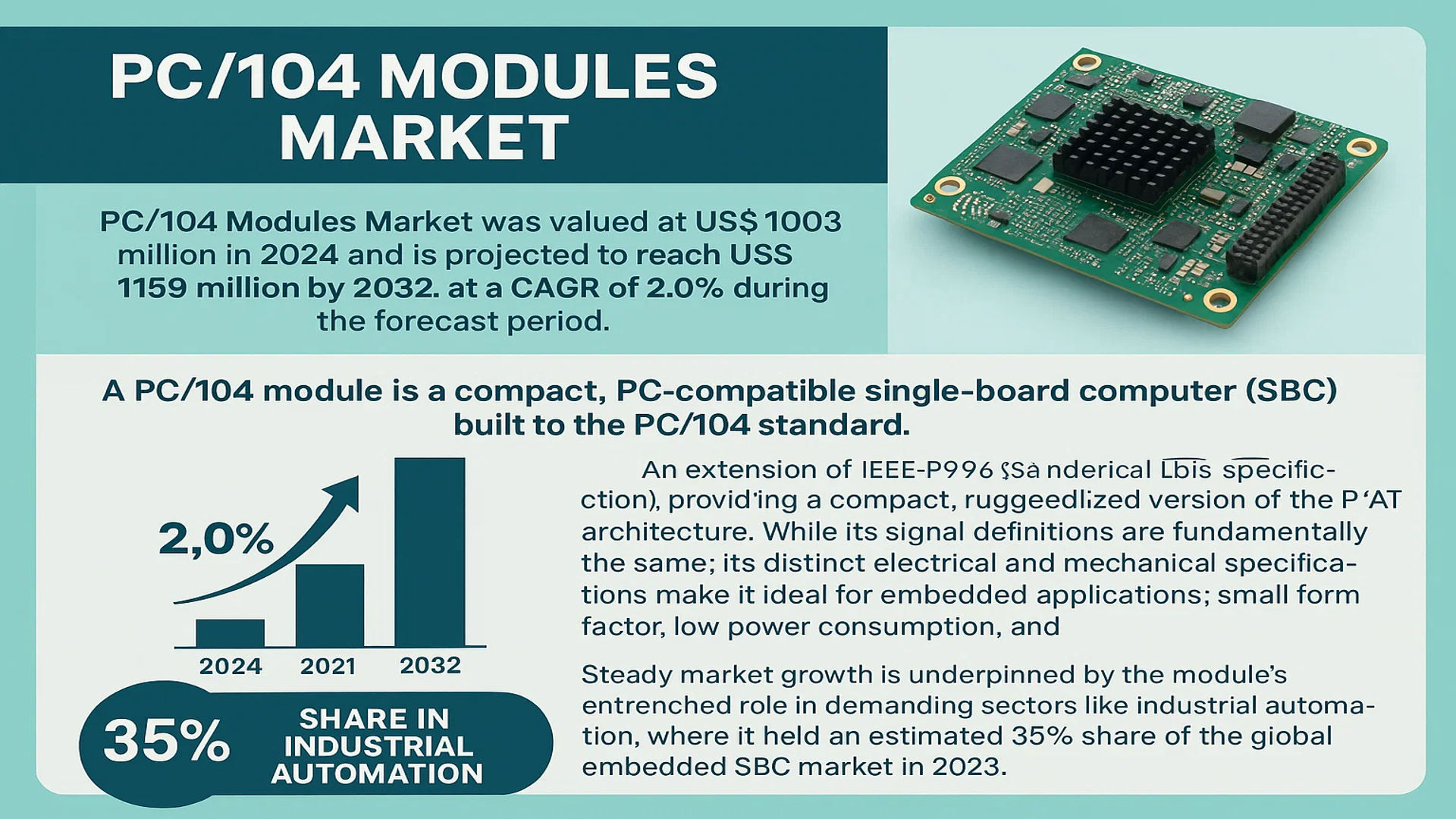

The global PC/104 Modules Market was valued at 1003 million in 2024 and is projected to reach US$ 1159 million by 2032, at a CAGR of 2.0% during the forecast period.

A PC/104 module is a compact, PC-compatible single-board computer (SBC) built to the PC/104 standard. This standard is an extension of the IEEE-P996 (ISA industrial bus specification), essentially providing a compact, ruggedized version of the PC/AT architecture. While its signal definitions are fundamentally the same, its distinct electrical and mechanical specifications make it ideal for embedded applications where small form factor, low power consumption, and high reliability are paramount.

Steady market growth is underpinned by the module’s entrenched role in demanding sectors like industrial automation, where it held an estimated 35% share of the global embedded SBC market in 2023. Furthermore, its adoption is accelerating in the Internet of Things (IoT) for building robust edge nodes, driven by the need for reliable connectivity in harsh environments. The military and aerospace sector remains a key consumer, leveraging the standard’s proven performance for applications in radar and communications systems. Recent technological integrations, such as support for 5G connectivity and AI co-processors for edge computing, are expanding its utility into new fields like telemedicine and smart city infrastructure, ensuring its continued relevance.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation and IoT Integration to Accelerate Market Growth

The global industrial automation sector is experiencing robust growth, with investments exceeding $200 billion annually, driving substantial demand for embedded computing solutions like PC/104 modules. These modules provide critical computing power in space-constrained environments where traditional computing systems are impractical. Their modular architecture enables flexible configuration for specific industrial applications, from robotic control systems to programmable logic controllers. The proliferation of Industry 4.0 initiatives worldwide has accelerated adoption rates, particularly in manufacturing sectors seeking to enhance operational efficiency through smart factory implementations. PC/104 modules serve as the computational backbone for numerous industrial IoT applications, processing sensor data and enabling real-time decision-making at the edge.

Military and Aerospace Sector Modernization Drives Specialized Demand

Defense modernization programs across major economies are creating sustained demand for ruggedized computing solutions. PC/104 modules meet stringent military specifications (MIL-STD-810) for shock, vibration, and temperature extremes, making them ideal for defense applications. The global defense electronics market, valued at approximately $150 billion, increasingly incorporates these modules in radar systems, unmanned vehicles, and communications equipment. Recent geopolitical developments have accelerated military spending, with NATO countries committing to minimum 2% GDP defense expenditures. This has directly translated into increased procurement of embedded computing systems, particularly in surveillance, reconnaissance, and command-and-control applications where reliability under extreme conditions is paramount.

Advancements in Medical Technology Create New Application Verticals

The medical equipment sector represents a growing market segment for PC/104 modules, particularly in portable diagnostic devices and laboratory instrumentation. The global medical devices market, projected to reach $600 billion by 2025, increasingly incorporates embedded computing solutions for data acquisition, processing, and connectivity functions. PC/104 modules enable medical device manufacturers to develop compact, power-efficient systems that meet regulatory requirements while providing computational capabilities necessary for modern healthcare applications. The COVID-19 pandemic accelerated adoption of portable medical devices and point-of-care testing equipment, many of which utilize PC/104 architecture for their computing needs. Regulatory approvals for new medical devices incorporating embedded computing have increased by approximately 15% annually, reflecting the growing integration of computational capabilities in healthcare technology.

MARKET CHALLENGES

Increasing Competition from Alternative Embedded Computing Architectures

The PC/104 market faces significant pressure from emerging embedded computing standards that offer higher performance and newer interfaces. COM Express, Qseven, and SMARC modules provide more modern processor interfaces and higher-speed connectivity options, attracting design wins in new applications. While PC/104 maintains advantages in legacy system compatibility and ruggedization, many new designs are opting for these alternative architectures. The embedded computing market has seen approximately 20% annual growth in alternative form factors, compared to 2-3% for traditional PC/104 designs. This competitive pressure requires existing PC/104 manufacturers to continuously innovate while maintaining backward compatibility, creating engineering challenges and increased development costs.

Other Challenges

Supply Chain Constraints and Component Availability

The global semiconductor shortage has particularly impacted legacy component availability, affecting PC/104 module production. Many PC/104 designs utilize older interface chips and components that are becoming increasingly difficult to source. Lead times for certain industrial-grade components have extended from typical 8-12 weeks to 40-52 weeks, causing production delays and increased costs. Manufacturers face difficult decisions between redesigning products with newer components—potentially compromising compatibility—or maintaining existing designs with limited component availability.

Technological Obsolescence Concerns

The relatively slow evolution of the PC/104 standard compared to modern computing interfaces creates long-term viability concerns. While the market maintains demand for legacy compatibility, new applications increasingly require interfaces like PCI Express 4.0, USB4, and 10GbE that are not native to traditional PC/104 architecture. This technological gap forces system integrators to implement additional bridging solutions, adding complexity and cost to end products.

MARKET RESTRAINTS

High Development Costs and Extended Product Lifecycles Limit Market Expansion

The development and certification processes for PC/104 modules, particularly for military and medical applications, involve substantial investment and extended timelines. Certification requirements such as DO-254 for aerospace and IEC 60601 for medical devices can add 18-24 months to product development cycles and increase development costs by 40-60%. These extended timelines conflict with rapidly evolving technological requirements, creating a mismatch between product availability and market needs. Additionally, the long product lifecycles typical in industrial and defense applications (often 10-15 years) limit opportunities for frequent design updates and technology refresh cycles.

Limited Processing Power Constrains High-Performance Applications

While PC/104 modules provide adequate computing performance for many embedded applications, they face limitations in processing-intensive applications such as artificial intelligence, machine learning, and advanced signal processing. The form factor constraints and power limitations restrict the integration of high-performance processors and accelerators required for these applications. This performance gap becomes increasingly significant as edge computing applications demand more computational capability closer to data sources. Applications requiring real-time video analytics, complex pattern recognition, or sophisticated control algorithms often exceed the capabilities of standard PC/104 modules, forcing designers to alternative solutions.

Transition to Wireless Technologies Creates Interface Compatibility Issues

The industry-wide transition to wireless connectivity presents integration challenges for PC/104 systems. While newer modules incorporate wireless capabilities, many legacy systems lack native support for modern wireless standards, requiring additional interface modules and creating integration complexity. The proliferation of 5G, Wi-Fi 6, and Bluetooth Low Energy technologies in industrial applications demands computing platforms with integrated wireless capabilities, which traditional PC/104 architecture was not originally designed to support. This architectural limitation requires system designers to implement additional components, increasing system complexity, power consumption, and potential points of failure.

MARKET OPPORTUNITIES

Modernization of Legacy Systems Creates Sustained Replacement Demand

The extensive installed base of PC/104 systems across industrial, military, and aerospace applications represents a significant opportunity for module manufacturers. Many systems installed 10-15 years ago are reaching end-of-life and require replacement with modern equivalents that maintain mechanical and electrical compatibility. This replacement market represents approximately 30% of annual PC/104 module sales, providing stable demand even as new design activity shifts toward alternative architectures. Manufacturers that can provide backward-compatible solutions with improved performance, reduced power consumption, and enhanced connectivity are positioned to capture this sustained replacement business.

Edge Computing Expansion Drives Demand for Ruggedized Computing Solutions

The rapid growth of edge computing applications across industrial, transportation, and energy sectors creates new opportunities for PC/104 modules. While many edge applications utilize commercial computing hardware, environments with extreme temperatures, vibration, or space constraints require the ruggedized characteristics of PC/104 architecture. The edge computing market is projected to grow at approximately 20% CAGR, with industrial applications representing the largest segment. PC/104 modules are particularly well-suited for transportation systems, remote monitoring equipment, and energy infrastructure where environmental conditions preclude standard computing solutions.

Integration with Modern Interfaces Through Hybrid Solutions

Manufacturers are developing hybrid solutions that combine PC/104 mechanical compatibility with modern computing interfaces, creating opportunities to bridge legacy and contemporary requirements. These solutions allow system integrators to maintain existing mechanical designs while incorporating current-generation processors and interfaces. The development of carrier boards and interface modules that translate between PC/104 and modern standards enables continued use of the form factor while addressing interface limitations. This approach particularly benefits military and aerospace applications where mechanical compatibility is often mandated while computational requirements continue to evolve.

PC/104 MODULES MARKET TRENDS

Integration of Advanced Computing Capabilities to Emerge as a Trend in the Market

The relentless progression of semiconductor technology is fundamentally reshaping the PC/104 modules landscape, enabling a significant leap in integration and processing power. While the standard has historically been valued for its ruggedness and compact form factor, it is now increasingly being equipped with capabilities once reserved for larger systems. This evolution is critical for applications at the edge, where artificial intelligence (AI) processing and real-time data analytics are becoming mandatory. The integration of powerful System-on-Chip (SoC) designs allows these modules to perform complex computational tasks locally, reducing latency and bandwidth requirements. Furthermore, the adoption of advanced communication interfaces like 5G and Wi-Fi 6 is enhancing data transmission speeds and connection reliability, making PC/104 modules indispensable for modern IoT infrastructures and smart city deployments. This technological convergence ensures the platform remains highly competitive against newer form factors by offering a unique blend of proven reliability and cutting-edge performance.

Other Trends

Proliferation in Industrial Automation and IoT

The expansion of Industrial Internet of Things (IIoT) and Industry 4.0 initiatives is a primary catalyst for market growth. PC/104 modules are exceptionally well-suited for the harsh environments typical of industrial settings, offering high reliability in extreme temperatures and under significant vibration. Their small footprint allows for seamless integration into space-constrained machinery, programmable logic controllers (PLCs), and human-machine interfaces (HMIs). This demand is reflected in the industrial automation segment, which consistently accounts for a substantial portion of the market’s application share. The need for distributed control and real-time monitoring is driving the deployment of these modules in smart manufacturing lines, where they facilitate predictive maintenance and optimize operational efficiency. Because these applications require robust and long-lifecycle components, the proven track record of the PC/104 standard provides a significant advantage over less mature technologies.

Sustained Demand from Defense and Aerospace Sectors

The defense, aerospace, and transportation sectors continue to be cornerstone consumers of PC/104 modules, driven by an uncompromising need for reliability and performance in critical systems. These modules are integral to a wide array of applications, including avionics, radar systems, unmanned vehicles, and satellite communications equipment. Their ability to withstand extreme environmental conditions—such as wide temperature fluctuations, high shock, and vibration—makes them a preferred choice. This segment’s growth is further bolstered by global increases in defense spending and the modernization of existing military hardware. The long product life cycles and stringent certification requirements in these industries align perfectly with the stable, standardized nature of the PC/104 architecture, ensuring a consistent and high-value demand stream that is less susceptible to economic fluctuations than consumer markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global PC/104 Modules market exhibits a fragmented competitive structure, characterized by a mix of established multinational corporations and specialized niche players. While the market is highly competitive, it remains dynamic due to continuous technological innovation and the diverse application requirements across industrial, military, and medical sectors. Advantech and Kontron (a S&T AG company) are widely recognized as dominant forces, leveraging their extensive R&D capabilities and global distribution networks to maintain significant market share. Their leadership is further solidified by comprehensive product portfolios that cater to both legacy systems and modern applications requiring enhanced processing power and connectivity, such as IoT edge nodes and ruggedized military computing.

Eurotech Group and Moxa Inc. also command considerable influence, particularly within the industrial automation and transportation segments. Their growth is largely driven by a strategic focus on developing high-reliability modules capable of operating in harsh environments, which is a critical requirement for many end-users. These companies have successfully expanded their market presence through targeted acquisitions and by forming strategic partnerships with sensor manufacturers and software providers, creating integrated solutions that offer greater value to customers.

p>Furthermore, the competitive intensity is heightened by the active participation of numerous specialized manufacturers, such as VersaLogic Corporation and WinSystems, Inc., who compete effectively by offering highly customized and application-specific solutions. Their agility allows them to respond quickly to emerging trends, such as the integration of AI co-processors and support for real-time operating systems. These players often focus on cultivating deep relationships within vertical markets like defense and aerospace, where product longevity and reliability are paramount.

Meanwhile, other key participants like Aaeon Technology Inc. and ADLINK Technology Inc. are strengthening their positions through significant investments in developing modules with advanced features, including support for 5G connectivity and enhanced graphics capabilities. Their strategy often involves pursuing certifications for military and medical applications, which allows them to access high-value contracts and ensures continued growth amidst fierce competition. The overall landscape is therefore defined by a constant push for innovation, portfolio expansion, and strategic market positioning to capture opportunities in a steadily growing global market.

List of Key PC/104 Modules Companies Profiled

- Advantech Co., Ltd. (Taiwan)

- Kontron S&T AG (Germany)

- Eurotech Group (Italy)

- Moxa Inc. (Taiwan)

- VersaLogic Corporation (U.S.)

- WinSystems, Inc. (U.S.)

- Aaeon Technology Inc. (Taiwan)

- ADLINK Technology Inc. (Taiwan)

- Connect Tech Inc. (Canada)

- Sealevel Systems, Inc. (U.S.)

- Data Device Corporation (U.S.)

- Texas Instruments Incorporated (U.S.)

Segment Analysis:

By Type

16-bit Bus Segment Dominates the Market Due to Superior Processing Capabilities and Broader Compatibility

The market is segmented based on type into:

- 8-bit Bus

- 16-bit Bus

By Application

Automated Industry Segment Leads Due to High Demand for Rugged and Reliable Embedded Computing Solutions

The market is segmented based on application into:

- Automated Industry

- Communication Device

- Medical Equipment

- Other

By End User

Industrial Automation End User Segment Holds Significant Share Owing to Extensive Use in Manufacturing and Process Control

The market is segmented based on end user into:

- Industrial Automation

- Defense and Aerospace

- Healthcare

- Telecommunications

- Transportation

By Operating System Compatibility

Linux-Compatible Segment Gains Traction Due to its Open-Source Nature and Customization Flexibility

The market is segmented based on operating system compatibility into:

- Linux-Compatible

- Windows-Compatible

- Real-Time Operating Systems (RTOS)

- Others

Regional Analysis: PC/104 Modules Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global PC/104 Modules market, accounting for the largest share of both volume consumption and manufacturing output. This leadership is primarily driven by China, which functions as a global electronics manufacturing hub, and Japan, a longstanding leader in industrial automation and precision engineering. The region’s massive manufacturing base, particularly in consumer electronics, automotive, and industrial equipment, creates sustained demand for embedded computing solutions like PC/104 modules. Government initiatives promoting Industry 4.0 and smart manufacturing, such as China’s “Made in China 2025” policy, further accelerate the adoption of these modules in automated production lines and robotics. While cost-competitive, legacy 8-bit bus modules remain popular for high-volume applications, there is a clear and accelerating trend toward more sophisticated 16-bit bus modules that support advanced functionalities like edge computing and AI processing. The extensive and growing Internet of Things (IoT) ecosystem across the region, from smart city projects in Singapore to agricultural automation in India, provides a significant and expanding market for compact, reliable embedded computing platforms.

North America

North America represents a highly advanced and innovation-driven market for PC/104 Modules, characterized by demanding applications that require high reliability and cutting-edge performance. The United States is the core of this region, with significant demand stemming from its robust military, aerospace, and defense sectors. PC/104 modules are extensively used in mission-critical systems, including avionics, unmanned vehicles, and ground support equipment, where their ruggedized design and proven reliability under extreme conditions are paramount. Beyond defense, the region’s strong medical device industry, supported by a stringent FDA regulatory framework, utilizes these modules in portable diagnostic equipment and laboratory analyzers. The market is also propelled by investments in modernizing industrial infrastructure and the development of sophisticated IoT solutions. While the volume may be lower than Asia-Pacific, the average selling price and technological sophistication of modules deployed in North America are typically higher, focusing on high-performance computing, enhanced security features, and long-lifecycle support.

Europe

The European market for PC/104 Modules is mature and is strongly influenced by a regulatory environment that emphasizes quality, environmental sustainability, and standardization. The region boasts a strong industrial automation sector, particularly in Germany (Industry 4.0) and Italy, where PC/104 modules are integrated into precision machinery and control systems. Strict EU directives, such as those concerning energy efficiency (ErP) and the restriction of hazardous substances (RoHS), drive the development and adoption of modules that are not only high-performing but also compliant with these environmental standards. There is a notable focus on research and development, leading to innovations in low-power designs and modules suitable for green technology applications. The aerospace sector, with major players like Airbus, also contributes to demand for modules that meet rigorous certification standards. The market is characterized by a preference for high-quality, reliable components from established suppliers, with a steady shift towards more integrated and connected solutions for smart manufacturing and infrastructure projects.

South America

The PC/104 Modules market in South America is emerging and presents a landscape of gradual growth amidst economic challenges. Countries like Brazil and Argentina are the primary markets, where these modules find applications in industrial automation, transportation systems, and natural resource extraction equipment. The adoption rate is often tempered by economic volatility, which can constrain capital expenditure on new industrial technology and lead to a higher reliance on cost-effective, often older-generation, modules. While there is recognition of the benefits of advanced embedded computing for improving operational efficiency, widespread adoption is hindered by limited local manufacturing and a complex import environment for electronic components. However, ongoing infrastructure development projects and the modernization of certain industrial sectors offer potential growth opportunities for suppliers who can navigate the regional economic landscape and provide robust, value-oriented solutions.

Middle East & Africa

The market for PC/104 Modules in the Middle East & Africa is nascent but holds long-term potential, primarily driven by infrastructure development and industrialization efforts in key Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE. Applications are often found in the oil & gas sector for process control and monitoring equipment, as well as in telecommunications infrastructure. The region’s harsh environmental conditions create a need for the ruggedness and reliability that PC/104 modules can provide. However, market growth is constrained by a relatively underdeveloped local industrial electronics ecosystem and a focus on larger turnkey projects rather than component-level sourcing. Investment in smart city initiatives and economic diversification plans away from oil dependence are expected to slowly generate increased demand for advanced embedded computing solutions in the coming years, though the market will likely remain a niche segment within the global landscape for the foreseeable future.

Report Scope

This market research report provides a comprehensive analysis of the global and regional PC/104 Modules market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global PC/104 Modules Market?

-> PC/104 Modules Market was valued at 1003 million in 2024 and is projected to reach US$ 1159 million by 2032, at a CAGR of 2.0% during the forecast period.

Which key companies operate in Global PC/104 Modules Market?

-> Key players include Advantech, AAEON Electronics, Inc., Moxa Inc., VersaLogic Corporation, and Eurotech Group, among others.

What are the key growth drivers?

-> Key growth drivers include technological advancements in integration and interfaces, rising demand in industrial control and IoT applications, and increasing adoption in military, aerospace, and medical equipment sectors.

Which region dominates the market?

-> North America holds a significant market share, while Asia-Pacific is the fastest-growing region, driven by industrial automation and IoT expansion.

What are the emerging trends?

-> Emerging trends include integration of edge computing and AI capabilities, adoption of advanced communication interfaces like 5G and WiFi, and development of multifunctional, low-power consumption modules for diverse applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...