MARKET INSIGHTS

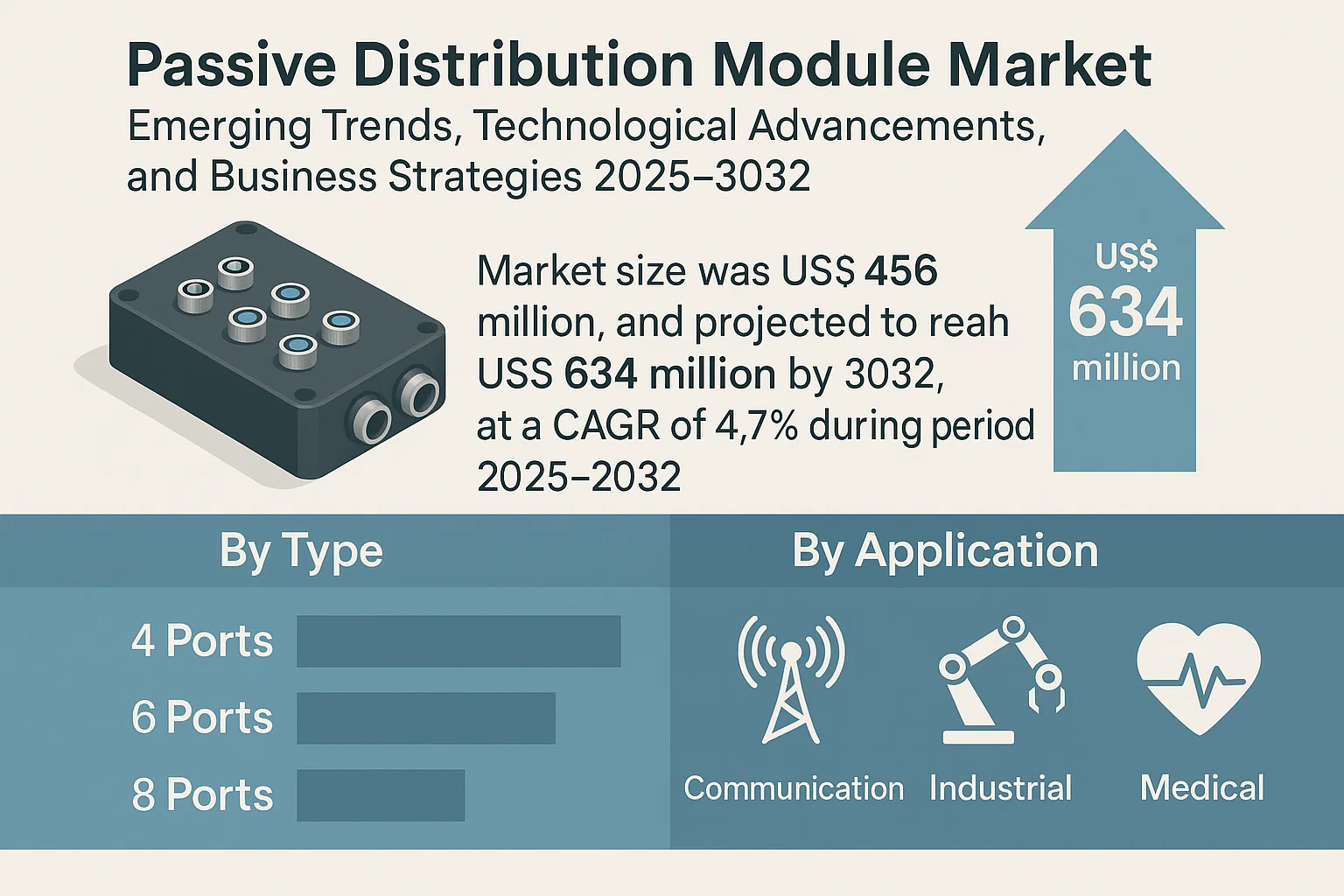

The global Passive Distribution Module Market size was valued at US$ 456 million in 2024 and is projected to reach US$ 634 million by 2032, at a CAGR of 4.7% during the forecast period 2025-2032. While North America currently holds the largest market share at 35%, the Asia-Pacific region is expected to witness the fastest growth due to increasing industrialization.

Passive Distribution Modules are critical components in industrial automation systems, designed to isolate, filter, and distribute 4-20mA signals from two-wire transmitters without requiring external power. These modules automatically draw power from the output circuit, making them energy-efficient solutions for signal conditioning applications. Major configurations include 4-port, 6-port, and 8-port variants, with the 4-port segment accounting for approximately 40% of total market revenue.

The market growth is driven by expanding industrial automation across manufacturing sectors, particularly in oil & gas and chemical processing industries where signal integrity is paramount. Recent technological advancements in module design have improved noise immunity and signal accuracy, further boosting adoption. Key players like Belden, Phoenix Contact, and Schneider Electric are investing in product innovation to capture larger market shares, with the top five companies collectively holding about 55% of the global market.

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation Boom Accelerating Demand for Passive Distribution Modules

The rapid adoption of Industry 4.0 technologies across manufacturing sectors is creating unprecedented demand for passive distribution modules (PDMs). These components play a critical role in signal conditioning and distribution within automated systems, enabling seamless integration of sensors and control units. With the global industrial automation market projected to surpass $400 billion by 2030, PDMs have become indispensable for ensuring signal integrity in complex automation networks. Recent advancements in predictive maintenance and IoT-enabled devices further amplify this demand, as these applications require reliable signal processing components for continuous data transmission.

Expansion of Smart Building Infrastructure Fuels Market Growth

The proliferation of smart building technologies represents another significant driver for passive distribution modules. Modern building automation systems rely on PDMs to distribute and condition control signals for HVAC, lighting, and security systems efficiently. The global smart building market, growing at a CAGR of over 12%, necessitates robust signal distribution solutions that can operate without external power sources. Passive distribution modules perfectly meet this requirement with their self-powered operation capability, making them ideal for energy-efficient building designs. Municipal initiatives for green building certifications are further accelerating adoption across commercial and residential construction sectors.

Additionally, advancements in communication infrastructure are creating new opportunities for PDMs. The rollout of 5G networks and industrial IoT applications requires precise signal conditioning solutions to maintain network reliability. Leading manufacturers have responded by introducing PDMs with enhanced filtering capabilities to minimize signal interference in dense electronic environments.

MARKET RESTRAINTS

Supply Chain Disruptions Pose Significant Challenges to Market Stability

The passive distribution module market faces persistent challenges from global supply chain volatility. Recent semiconductor shortages have created ripple effects across electronic component manufacturing, causing delays in PDM production and delivery cycles. Lead times for essential raw materials have extended significantly, forcing manufacturers to maintain larger inventories and absorb higher operational costs. This situation particularly impacts price-sensitive market segments where cost optimization is critical for adoption.

Additional Constraints

Technical Complexity in Custom Designs

While standard PDM solutions are widely available, customized configurations for specialized applications often require extensive engineering resources. The development cycle for application-specific passive distribution modules can extend beyond typical project timelines, creating bottlenecks in system integration processes. This challenge is most apparent in medical and aerospace applications where stringent reliability requirements demand rigorous testing protocols.

Competition from Alternative Solutions

Emerging digital signal distribution technologies present competitive pressure on traditional passive modules. Some system designers opt for active distribution alternatives that offer additional functionality, despite their higher power requirements. This trend threatens to constrain market growth in segments where compact design and power efficiency remain secondary to feature-rich solutions.

MARKET OPPORTUNITIES

Medical Equipment Modernization Creates New Application Frontiers

The healthcare sector presents significant growth opportunities for passive distribution module manufacturers as medical facilities worldwide upgrade their diagnostic and monitoring equipment. The increasing digitization of healthcare infrastructure requires reliable signal distribution solutions that meet strict medical safety standards. PDMs are particularly valuable in patient monitoring systems where electrical isolation is critical for patient safety. With the medical electronics market growing at approximately 7% annually, specialized passive distribution solutions tailored for healthcare applications are expected to gain substantial traction.

Renewable Energy Integration Drives Innovation in Power Distribution

The global transition to renewable energy systems opens new avenues for passive distribution module applications. Solar and wind power installations increasingly incorporate PDMs for condition monitoring and control signal distribution. These applications demand components that can withstand harsh environmental conditions while maintaining signal integrity. Manufacturers are responding by developing ruggedized PDM variants with enhanced protection against moisture, temperature extremes, and electromagnetic interference. As renewable energy capacity continues its rapid expansion, these specialized solutions are positioned for significant market growth.

Furthermore, the automotive sector’s shift toward electric vehicles presents complementary opportunities. EV charging infrastructure requires sophisticated power distribution solutions where passive modules can play an important role in signal conditioning and system monitoring applications.

MARKET CHALLENGES

Miniaturization Demands Test Engineering Capabilities

The passive distribution module market faces mounting pressure to deliver increasingly compact solutions without compromising performance. Modern industrial and consumer applications demand smaller form factors to accommodate space-constrained designs, requiring manufacturers to overcome significant engineering hurdles. Achieving comparable signal integrity in reduced footprints poses challenges in thermal management and electromagnetic compatibility that can increase development costs and time-to-market for new products.

Additional Industry Challenges

Rapid Technological Obsolescence

The fast pace of technological advancement in end-use industries creates challenges for PDM manufacturers to maintain product relevance. Design standards and interface protocols evolve frequently, necessitating continuous research and development investments. This dynamic environment makes product lifecycle management increasingly complex, particularly for manufacturers serving multiple industry verticals.

Global Competition Intensifies

The passive distribution module market has seen growing competition from international manufacturers, particularly in price-sensitive segments. Regional suppliers with lower operating costs have gained market share by offering basic PDM solutions at aggressive price points. This competition pressures established manufacturers to optimize production efficiency while maintaining quality standards, creating significant operational challenges.

PASSIVE DISTRIBUTION MODULE MARKET TRENDS

Industrial Automation Surge Drives Passive Distribution Module Demand

The global Passive Distribution Module market, valued at millions in 2024, is witnessing significant growth due to accelerating industrial automation across manufacturing and process industries. These modules play a critical role in signal conditioning for 4-20mA instruments, eliminating the need for external power by drawing energy directly from output circuits. With factory automation investments projected to grow at 8-10% annually through 2030, the demand for efficient signal distribution solutions like passive modules continues to intensify. Recent technological upgrades in Module versions now support higher port densities and improved signal isolation, making them indispensable in complex control systems. The U.S. remains the largest regional market, accounting for approximately 30% of global revenue, while China’s rapid industrial expansion pushes its share upwards of 20% in 2024.

Other Trends

Smart Factory Integration

The transition towards Industry 4.0 standards is reshaping passive module requirements, with growing emphasis on network interoperability and real-time monitoring capabilities. Modern passive distribution modules now incorporate advanced filtering algorithms to prevent signal degradation in electrically noisy industrial environments. Leading manufacturers have introduced 12-port variants that reduce control cabinet footprint by 40% compared to traditional solutions. The medical equipment sector represents an emerging application area, where signal isolation modules help maintain precision in diagnostic instruments and patient monitoring systems.

Technical Innovation Reshapes Competitive Landscape

The passive distribution module sector is experiencing a wave of product innovations as manufacturers address evolving industrial needs. 4-port solutions currently dominate with over 35% market share, but demand is shifting toward higher density configurations as factories optimize control panel space. Major players like Phoenix Contact and Murrelektronik have launched modules with integrated diagnostics LEDs and tamper-proof housings for harsh environments. Meanwhile, Belden’s recent patent for a self-calibrating passive module promises to reduce maintenance downtime in continuous process industries. With energy efficiency becoming paramount, new module designs demonstrate 97%+ power conversion efficiency from loop-powered operation.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Alliances and Innovation Drive Market Competition

The global Passive Distribution Module market exhibits a moderately consolidated structure, with established industrial automation solution providers dominating the revenue share. Belden Inc. emerges as a market leader, holding approximately 18% of the 2024 market share, owing to its comprehensive signal transmission solutions and strong foothold in North American industrial sectors.

European manufacturers Phoenix Contact and Murrelektronik GmbH collectively account for nearly 25% of the market, leveraging their expertise in industrial connectivity solutions. Their growth stems from increasing automation adoption across German and French manufacturing sectors, which witnessed 7.2% year-over-year growth in industrial IoT deployment in 2023.

The market sees intensified competition through technological differentiators – Eaton Corporation recently launched its next-generation PDM series with enhanced EMI shielding, capturing significant demand from the energy sector. Meanwhile, Schneider Electric strengthened its position through strategic acquisitions in Asian markets, where industrial automation spending is projected to grow at 9.1% CAGR through 2030.

Smaller players like KLOTZ AIS and Turck are gaining traction through specialized solutions for harsh environments, particularly in oil & gas applications. Their modular designs address the growing need for explosion-proof signal distribution systems, comprising 12.4% of 2024 application-specific sales.

List of Key Passive Distribution Module Manufacturers

- Belden Inc. (U.S.)

- EUCHNER GmbH (Germany)

- Schmersal Group (Germany)

- Murrelektronik GmbH (Germany)

- Eaton Corporation (Ireland)

- Parker Hannifin (U.S.)

- Snap One LLC (U.S.)

- KLOTZ AIS GmbH (Germany)

- Leviton Manufacturing (U.S.)

- Phoenix Contact (Germany)

- Schneider Electric SE (France)

- Huber+Suhner AG (Switzerland)

- Turck GmbH (Germany)

- Molex LLC (U.S.)

- CommScope (U.S.)

Segment Analysis:

By Type

4 Ports Segment Dominates Due to Widespread Use in Industrial Automation Applications

The market is segmented based on type into:

- 4 Ports

- 6 Ports

- 8 Ports

- 10 Ports

- 12 Ports

- Others

By Application

Industrial Segment Leads Market Share Owing to Automation and Control System Demands

The market is segmented based on application into:

- Communication

- Industrial

- Medical

- Others

By Region

Asia Pacific Emerges as Fastest Growing Market for Passive Distribution Modules

The market is segmented based on region into:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

By Technology

Signal Conditioning Modules Gain Traction for Improved Signal Integrity

The market is segmented based on technology into:

- Basic Passive Distribution

- Signal Conditioning

- Isolation Modules

- Others

Regional Analysis: Passive Distribution Module Market

North America

The North American market for Passive Distribution Modules (PDMs) is characterized by high technological adoption and robust industrial automation. The U.S., in particular, dominates the region due to its advanced manufacturing and communications infrastructure. Key demand drivers include rising automation in industries such as oil & gas, automotive, and pharmaceuticals, where PDMs ensure reliable signal distribution without requiring external power. Additionally, stringent safety and efficiency standards in these sectors necessitate high-performance PDMs. Canada follows closely, with increasing investments in smart factories and Industry 4.0 initiatives. However, market saturation and competition from integrated solutions pose challenges to rapid growth.

Europe

Europe remains a mature yet steadily growing market for PDMs, with Germany, France, and the U.K. leading in adoption. The region’s focus on energy efficiency and stringent industrial regulations (e.g., IEC and EN standards) supports the demand for high-quality PDMs. The automotive and renewable energy sectors are significant contributors, especially in Germany, where automation and signal processing play a critical role. Furthermore, the push for smart grid technologies and industrial IoT integration creates opportunities for PDM manufacturers. Eastern Europe is gradually catching up, though adoption is slower due to cost sensitivity and a less developed industrial base.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for PDMs, driven by rapid industrialization in China, India, and Southeast Asia. China, in particular, leads due to its vast manufacturing base and increasing investments in factory automation. The region benefits from cost-competitive production and high demand across consumer electronics, automotive, and telecom sectors. While affordability drives demand for basic PDM models, there’s a growing shift toward advanced modules with higher port configurations (e.g., 8-12 ports) to support complex automation systems. However, market fragmentation and the dominance of local manufacturers create pricing pressures for global players.

South America

South America presents a developing market for PDMs, with Brazil and Argentina as the primary demand centers. The region’s oil & gas and mining industries drive the need for reliable signal distribution solutions. However, economic instability and inconsistent industrial policies have slowed significant growth. Local manufacturing is limited, leading to reliance on imports, particularly from North American and European suppliers. Despite these challenges, gradual progress in automation and infrastructural investments suggests long-term potential, especially in energy and industrial automation sectors.

Middle East & Africa

The Middle East & Africa exhibit moderate but steady growth in PDM adoption, primarily propelled by oil & gas, petrochemical industries, and telecom expansions. The UAE and Saudi Arabia lead the region due to their focus on industrial modernization and smart city projects. Africa’s market remains nascent, constrained by infrastructure limitations and lower industrial automation penetration. While multinational companies dominate the supply chain, local partnerships are emerging to cater to region-specific requirements. The lack of stringent regulatory frameworks compared to Western markets slows the adoption of high-end PDMs, but increasing industrial activities signal future opportunities.

Report Scope

This market research report provides a comprehensive analysis of the Global Passive Distribution Module Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD million in 2024 and is projected to reach USD million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (4 Ports, 6 Ports, 8 Ports, 10 Ports, 12 Ports, Others) and application (Communication, Industrial, Medical, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with the U.S. and China as key growth markets.

- Competitive Landscape: Profiles of leading players including Belden, Eaton, Phoenix Contact, Schneider Electric, and Murrelektronik GmbH, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of signal processing advancements, power efficiency improvements, and integration with industrial automation systems.

- Market Drivers & Restraints: Evaluation of factors including industrial automation growth, IIoT adoption, and supply chain challenges affecting component availability.

- Stakeholder Analysis: Insights for manufacturers, system integrators, and end-users regarding technology adoption and market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Passive Distribution Module Market?

-> Passive Distribution Module Market size was valued at US$ 456 million in 2024 and is projected to reach US$ 634 million by 2032, at a CAGR of 4.7% .

Which key companies operate in this market?

-> Major players include Belden, Eaton, Phoenix Contact, Schneider Electric, Murrelektronik GmbH, and Parker Hannifin, with the top five accounting for approximately % market share in 2024.

What are the key growth drivers?

-> Key drivers include increasing industrial automation, growth in IIoT applications, and demand for energy-efficient signal distribution solutions.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of modules, integration with smart factory systems, and development of high-density distribution solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...