Optical Transceiver Market Insights

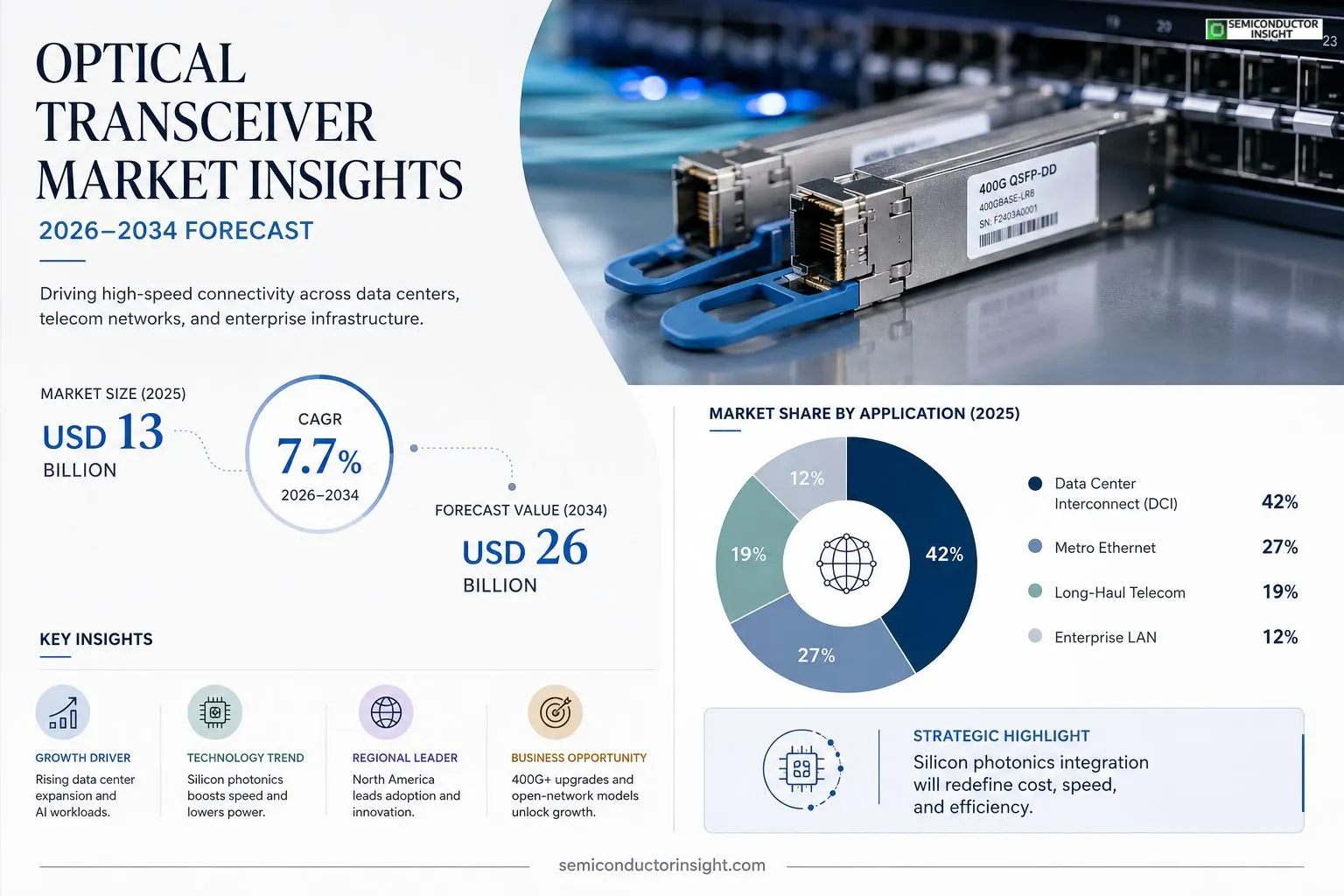

Global optical transceiver market size was valued at USD 13 billion in 2025. The market is projected to grow from USD 13 billion in 2025 to USD 26 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period.

Optical transceivers are compact electro‑optical modules that convert electrical signals into light and vice‑versa for high‑speed fiber‑optic communication links.They enable data transmission rates ranging from 10 Gbps up to 400 Gbps across telecom networks, data centers, and enterprise environments.Key form factors include SFP+, QSFP‑DD and CFP modules, each designed for specific bandwidth and distance requirements.The market is accelerating because exponential growth in internet traffic, cloud services and AI workloads drives demand for higher‑capacity links.Furthermore, the rollout of 400G Ethernet in backbone networks and the migration toward silicon photonics reduce power consumption while boosting speed.Major players such as Cisco, Finisar (II‑VI), Lumentum, Broadcom and Cienab are expanding their portfolios through new module introductions and strategic partnerships.For example, in March 2024 Broadcom launched a QSFP‑DD family supporting up to 400 Gbps per lane,while Intel’s silicon‑photonic transceivers were integrated into its latest Xeon processors later that year.These initiatives together fuel robust growth across Optical Transceiver Market.

MARKET DRIVERS

Growing Data Center Demand

The rapid expansion of hyperscale data centers is accelerating the need for high‑speed optical links. Operators are upgrading to 400 Gbps and beyond, creating a robust demand pipeline for Optical Transceiver Market.

5G and Edge Computing Adoption

Deployment of 5G networks and edge‑computing nodes requires low‑latency, high‑bandwidth connectivity, positioning optical transceivers as a critical component in the expanding telecom infrastructure.

➤ Integration of AI‑driven traffic management is expected to boost transceiver utilization rates by up to 15 % in the next three years.

In parallel, enterprise migration to cloud‑native architectures is driving procurement of modular, hot‑swappable transceiver modules, further energizing market growth.

MARKET CHALLENGES

High Capital Expenditure

Deploying advanced optical solutions involves significant upfront investment, which can deter mid‑size service providers from rapid adoption.

Other Challenges

Supply Chain Volatility

Component shortages and geopolitical tensions have introduced lead‑time extensions, compelling manufacturers to reassess inventory strategies.

MARKET RESTRAINTS

Cost Sensitivity in Emerging Regions

Price‑sensitive markets in Asia‑Pacific and Latin America often prioritize lower‑cost copper alternatives, limiting the penetration of premium optical transceiver solutions.Regulatory compliance requirements, such as stringent safety certifications, add additional layers of complexity and expense for manufacturers seeking market entry.Moreover, legacy infrastructure in several telecom operators slows the replacement cycle, restraining overall market acceleration.

MARKET OPPORTUNITIES

Emergence of Silicon Photonics

Silicon photonics promises lower production costs and higher integration density, presenting a compelling growth avenue for innovative players in Optical Transceiver Market.Additionally, the rise of open‑access network models encourages multi‑vendor ecosystems, fostering demand for interoperable transceiver modules.Finally, increasing investments in submarine cable projects across the Atlantic and Pacific corridors open long‑term revenue streams for manufacturers focused on high‑reliability designs.

Optical Transceiver Market Trends

Shift to Higher‑Speed 400G and Beyond

Optical Transceiver Market is being reshaped by the rapid deployment of 400 Gbps Ethernet across backbone and data‑center networks. Operators are replacing legacy 10 Gbps and 100 Gbps links with modules that support multiple 100 Gbps lanes, delivering the bandwidth needed for cloud services, AI workloads, and the escalating volume of internet traffic. This transition is also prompting a migration toward compact form factors such as QSFP‑DD, which provide higher port density while maintaining power efficiency. Vendors are focusing on low‑latency designs and flexible optics that can adapt to both short‑reach and long‑haul requirements, allowing network architects to future‑proof infrastructure without extensive hardware overhauls.

Other Trends

Silicon Photonics Integration

Silicon photonics is emerging as a cornerstone technology within Optical Transceiver Market, offering a path to lower power consumption and reduced form‑factor footprints. By leveraging CMOS‑compatible processes, manufacturers can integrate optical components directly onto silicon chips, thereby simplifying assembly and enabling higher production volumes. Recent product introductions demonstrate transceivers that combine silicon‑photonic engines with traditional polymer waveguides, delivering speeds up to 400 Gbps per lane while maintaining thermal stability. This approach also supports the trend toward programmable optics, where firmware updates can adjust wavelength allocation and modulation formats, providing operators with greater flexibility to respond to evolving traffic patterns.

Strategic Portfolio Expansion by Key Players

Leading suppliers such as Cisco, Broadcom, Lumentum, and Finisar are broadening their product portfolios through new module launches and strategic alliances. For instance, a recent QSFP‑DD family introduced by Broadcom offers 400 Gbps per lane capability, targeting high‑performance computing clusters and hyperscale data centers. Simultaneously, Intel’s silicon‑photonic transceivers have been integrated into its latest Xeon processors, embedding optical functionality directly into server CPUs. These moves illustrate a concerted effort to align optical transceiver offerings with the accelerating demand for bandwidth‑intensive applications, reinforcing the market’s growth trajectory while delivering cost‑effective, power‑efficient solutions.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Dynamics in the Global Optical Transceiver Market

Optical Transceiver Market is dominated by a handful of large semiconductor and networking firms that control both the design of high‑speed electro‑optical modules and the supply chain for key components such as lasers, photodiodes, and driver ASICs. Cisco Systems leads the ecosystem through its extensive portfolio of QSFP‑DD and SFP+ transceivers tightly integrated with its data‑center switches, leveraging scale to capture premium pricing. Broadcom and Intel complement this structure by offering silicon‑photonic transceiver silicon that integrates directly into server and processor silicon, accelerating adoption of 400 Gbps and beyond. Lumentum and II‑VI (Finisar) specialize in the optoelectronic sub‑assemblies, providing the laser engines that power the modules. Ciena and Huawei round out the top tier by bundling transceiver modules with carrier‑grade transport solutions, creating bundled value propositions for telecom operators. This concentration of capabilities across hardware, silicon, and system integration yields a market structure where strategic partnerships and co‑development agreements are essential for sustaining growth.Beyond the marquee names, a diverse group of niche innovators contributes significant specialty technology and regional market reach. NeoPhotonics focuses on coherent optics for long‑haul and metro networks, while Acacia Communications (now part of Marvell) supplies high‑performance coherent transceiver chips that enable flexible, software‑defined optics. Fujitsu and Nokia maintain strong positions in the European and Asian carrier segments through localized manufacturing and compliance with regional standards. Sumitomo Electric and Molex provide reliable passive and active interconnect solutions, ensuring mechanical robustness and thermal management for high‑density data‑center deployments. Smaller pure‑play silicon‑photonic firms such as Inphi (also part of Marvell) and emerging startups are accelerating innovation cycles, particularly in low‑power, high‑bandwidth designs that address the explosive demand from AI‑driven workloads and cloud hyperscalers. Collectively, these players enrich the competitive landscape with differentiated technologies and addressable markets that support the forecasted CAGR of 7.7 % through 2034.

List of Key Optical Transceiver Market Companies Profiled

- Cisco Systems

- Broadcom Inc.

- Intel Corporation

- Lumentum Holdings

- II‑VI Incorporated (Finisar)

- Ciena Corporation

- Huawei Technologies

- Juniper Networks

- Fujitsu Limited

- Nokia Corporation

- Acacia Communications (Marvell)

- NeoPhotonics Corporation

- Sumitomo Electric Industries

- Molex LLC

- Inphi (Marvell)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Digital Coherent transceivers dominate due to their ability to support long‑haul links with high spectral efficiency.

|

| By Application |

|

Data Center Interconnect remains the leading application as hyperscale operators seek ever‑greater bandwidth.

|

| By End User |

|

Cloud Service Providers are the primary end‑user segment, driving continuous upgrades of backbone infrastructure.

|

| By Form Factor |

|

QSFP‑DD has become the preferred form factor for high‑density, high‑speed deployments.

|

| By Technology Trend |

|

Silicon Photonics is reshaping the market by delivering cost‑effective, high‑performance modules.

|

Regional Analysis: North America

United States

The burgeoning data center sector in the US is a primary driver for Optical Transceiver demand. The need for higher bandwidth and lower latency within data centers necessitates the deployment of advanced optical solutions.

The rollout of 5G networks across the US is creating substantial opportunities for Optical Transceivers. The increased data traffic associated with 5G requires robust optical infrastructure to support network capacity and performance.

The continued expansion of cloud computing services in the US is fueling demand for high-speed data transfer and connectivity, directly impacting Optical Transceiver Market.

The rise of edge computing is driving the need for compact and energy-efficient Optical Transceivers to support distributed computing environments.

Europe

The European Optical Transceiver Market exhibits a strong emphasis on energy efficiency and sustainable solutions. Driven by stringent environmental regulations and a growing focus on green technology, the region is witnessing increased adoption of energy-efficient optical solutions. Key applications include telecommunications infrastructure upgrades, data center expansions, and the development of smart city initiatives. Research and development efforts are concentrated on improving the energy performance of Optical Transceivers and reducing their carbon footprint. Business strategies in Europe prioritize compliance with EU regulations, offering sustainable products, and fostering partnerships with energy-conscious organizations. The demand for Optical Transceivers in Europe is closely linked to the growth of high-speed internet access and the digital transformation of industries across the continent.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for Optical Transceivers globally. Driven by rapid industrialization, increasing internet penetration, and massive investments in telecommunications infrastructure, the region presents significant opportunities for market players. China is the dominant force in the Asia-Pacific Optical Transceiver Market, with substantial investments in 5G network deployment and data center development. Other key markets in the region include India, Japan, and South Korea. The demand for Optical Transceivers in Asia-Pacific is fueled by the growth of e-commerce, cloud computing, and the Internet of Things (IoT). Business strategies in the region focus on offering cost-effective solutions, building strong local partnerships, and adapting to the unique regulatory landscape of each country.

South America

The South American Optical Transceiver Market is experiencing moderate growth, driven by increasing investments in telecommunications infrastructure and the expanding digital economy. The demand for high-speed internet access is particularly strong in Brazil and Argentina. Key applications include telecom network upgrades, data center expansions, and the development of smart city initiatives. Challenges in the region include infrastructure limitations and regulatory complexities. Business strategies focus on offering affordable solutions and building partnerships with local telecom operators and infrastructure providers.

Middle East & Africa

The Middle East & Africa Optical Transceiver Market is witnessing gradual growth, fueled by increasing investments in telecommunications infrastructure and the expanding digital economy. Governments in the region are prioritizing the development of high-speed internet access and the digitalization of various sectors. Key applications include telecom network upgrades, data center developments, and the growth of e-commerce. Challenges include infrastructure limitations and economic instability in some countries. Business strategies focus on offering cost-effective solutions and collaborating with local partners to navigate the regional market dynamics.

Report Scope

This market research report provides a comprehensive analysis of the Optical Transceiver Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical Transceiver Market?

-> Optical Transceiver Market was valued at USD 13 billion in 2025 and is expected to reach USD 26 billion by 2034, representing a CAGR of 7.7% over the forecast period.

Which key companies operate in Optical Transceiver Market?

-> Key players include Cisco, Finisar (II‑VI), Lumentum, Broadcom, and Ciena, among others.

What are the key growth drivers?

-> Key growth drivers include exponential growth in internet traffic, expanding cloud services, AI workload increases, rollout of 400G Ethernet, and migration toward silicon photonics.

Which region dominates the market?

-> The reference material does not specify a single dominant region for Optical Transceiver Market.

What are the emerging trends?

-> Emerging trends include deployment of 400G Ethernet, integration of silicon‑photonic transceivers, and development of high‑speed modules such as QSFP‑DD supporting up to 400 Gbps per lane.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...