Optical Sensors Market Insights

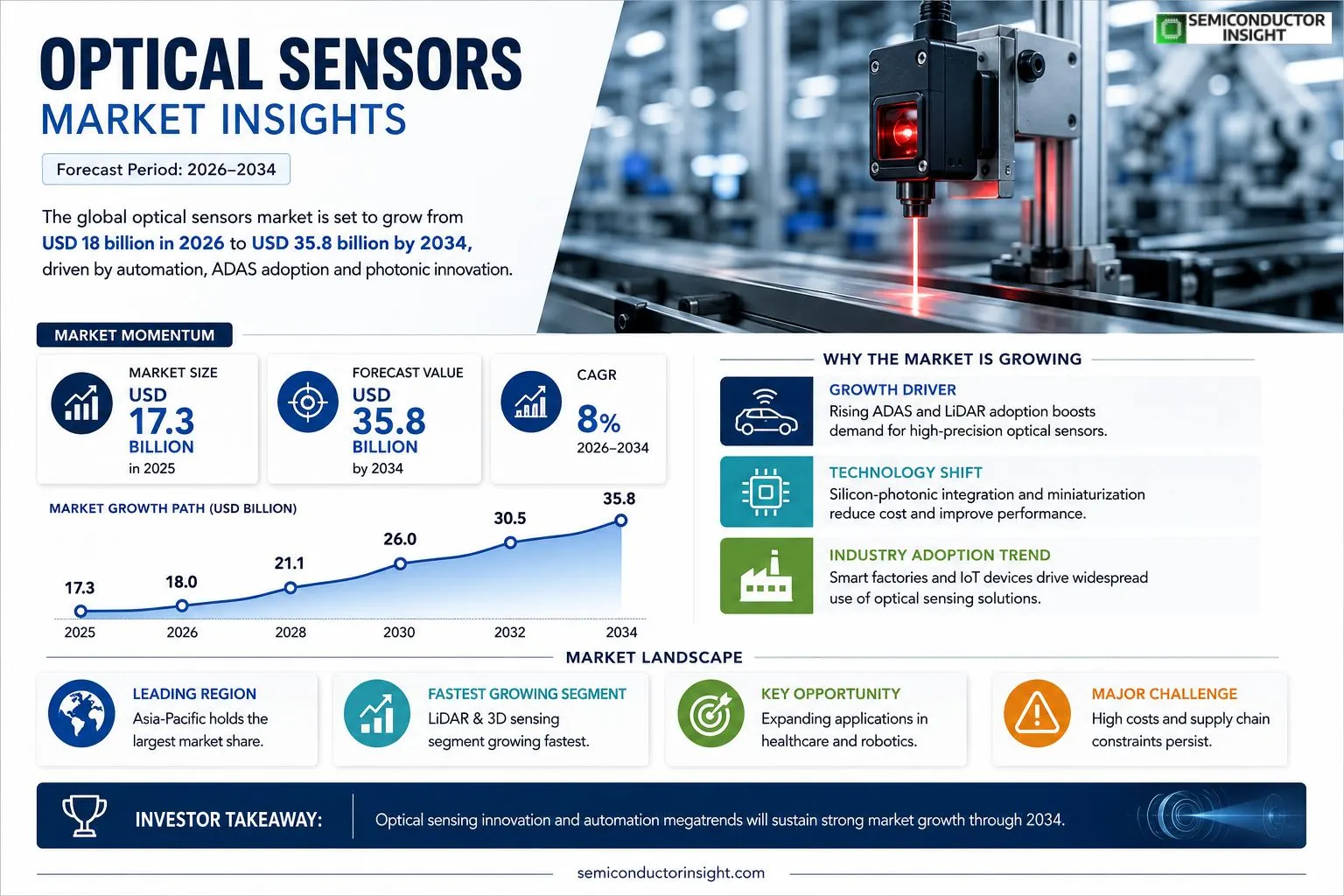

Optical Sensors Market size was valued at USD 17.3 billion in 2025.The market is projected to grow from USD 18 billion in 2026 to USD 35.8 billion by 2034, exhibiting a CAGR of 8% during the forecast period.Optical sensors are devices that convert light rays into electronic signals for precise measurement of distance, position, speed or environmental conditions.They encompass photodiodes, phototransistors, infrared (IR) receivers, LIDAR modules and fiber‑optic sensing systems, enabling applications ranging from industrial automation and automotive safety to consumer electronics and medical diagnostics.

The market is accelerating because manufacturers are investing heavily in miniaturization and integration of photonic components, while demand surges for advanced driver‑assistance systems (ADAS), smart factories and wearable health monitors.

Furthermore, breakthroughs such as silicon‑photonic integration announced by major foundries in early 2024 are reducing cost per unit.

Key players,including Texas Instruments, STMicroelectronics, Honeywell International and Bosch Sensortec,are expanding their portfolios through strategic acquisitions and collaborations aimed at enhancing sensor accuracy and power efficiency.

MARKET DRIVERS

Increasing Adoption in Automotive Safety Systems

Optical Sensors Market is being propelled by automakers embedding LiDAR and laser‑based sensors into advanced driver‑assistance systems (ADAS). These sensors enable real‑time object detection, which boosts vehicle safety ratings and fuels a steady demand for higher‑resolution optical components.

Growth of Industrial Automation

Factories are upgrading to smart production lines where optical sensors monitor material flow, positioning, and quality control. The push toward Industry 4.0 creates a robust pipeline of orders for compact, high‑speed photonic devices.

➤ “By 2028, optical sensor integration is expected to account for over 30% of new automation projects worldwide.”

Overall, the convergence of vehicle electrification, robotics, and IoT connectivity supplies a sustained growth engine for the sector.

MARKET CHALLENGES

Supply Chain Constraints for High‑Purity Materials

Manufacturers rely on specialty glass and semiconductor wafers that are sourced from a limited number of suppliers. Recent geopolitical tensions have amplified lead times, driving up component costs and slowing project roll‑outs.

Other Challenges

Regulatory Compliance

Stringent automotive safety standards and medical device regulations require rigorous testing, which can extend product development cycles and increase certification expenses.

MARKET RESTRAINTS

High Initial Capital Expenditure

Establishing clean‑room facilities and precision lithography lines demands multi‑million‑dollar investments, deterring entry of smaller players and concentrating market power among a few incumbents.

Limited Awareness in Emerging Economies

Potential adopters in regions such as Sub‑Saharan Africa and parts of Southeast Asia lack exposure to the benefits of optical sensing, resulting in slower market penetration despite growing industrialization.

These factors collectively cap the upside potential until infrastructure upgrades and education initiatives mature.

MARKET OPPORTUNITIES

Emerging Applications in Wearable Health Devices

Miniaturized optical sensors are now integral to pulse‑oximeters, glucose monitors, and continuous vital‑sign trackers. The rapid adoption of remote health monitoring creates a sizable niche for low‑power, high‑accuracy photonic modules.

Integration with AI‑Driven Analytics

Combining real‑time optical data with machine‑learning algorithms enables predictive maintenance and adaptive control systems. Companies that bundle sensing hardware with analytics platforms can command premium pricing and differentiate from commodity suppliers.Overall, these growth avenues position Optical Sensors Market for a dynamic expansion over the next decade.

Optical Sensors Market Trends

Accelerated Miniaturization and Integration

Optical Sensors Market is being reshaped by a concerted push toward smaller, more integrated photonic components. Manufacturers are leveraging silicon‑photonic processes to combine light detection and signal processing on a single chip, which reduces bill of materials and improves reliability. This technical evolution aligns with surging demand in Advanced Driver‑Assistance Systems (ADAS), where precise distance and speed measurement are critical for safety functions, and in smart‑factory environments that require high‑resolution, low‑latency feedback for robotic control. Wearable health monitors also benefit from compact, low‑power optical sensors that enable continuous monitoring of vital signs without compromising user comfort. As integration levels rise, power consumption drops, enabling battery‑operated devices to achieve longer runtimes while maintaining measurement accuracy. The combined effect of cost efficiencies and performance gains is driving broader adoption across automotive, industrial, consumer, and medical segments, establishing a robust growth trajectory for Optical Sensors Market.

Other Trends

Strategic Acquisitions and Partnerships

Leading suppliers such as Texas Instruments, STMicroelectronics, Honeywell International and Bosch Sensortec are actively reshaping their portfolios through targeted acquisitions and collaborative alliances. These strategic moves are designed to secure advanced intellectual property in photonic design, expand manufacturing capacity, and accelerate time‑to‑market for next‑generation sensor solutions. Partnerships with semiconductor foundries enable co‑development of customized process nodes that optimize optical throughput and thermal performance. In parallel, joint ventures with automotive OEMs and equipment manufacturers ensure that sensor specifications are tightly aligned with emerging system requirements, particularly for high‑definition LIDAR and vision‑based safety suites. By consolidating expertise and resources, these entities are strengthening the competitive landscape and fostering innovation pipelines that keep Optical Sensors Market at the forefront of emerging technology trends.

Emergence of Silicon‑Photonic Integration

Recent breakthroughs in silicon‑photonic integration have transitioned from research prototypes to commercially viable solutions, delivering higher bandwidth and dramatically lower energy consumption compared with traditional discrete optics. This shift enables the deployment of high‑resolution LIDAR modules in vehicles, where dense point clouds can be generated with reduced system size and power draw. Fiber‑optic sensing systems also benefit from integrated photonic circuits, allowing distributed temperature and strain monitoring across large infrastructures with enhanced signal fidelity. In medical diagnostics, silicon‑photonic platforms support compact imaging devices that provide clinicians with real‑time data while maintaining stringent sterility standards. The convergence of these capabilities creates a compelling value proposition for OEMs seeking to differentiate products through superior sensor performance, positioning silicon‑photonic integration as a cornerstone of future growth within Optical Sensors Market.

COMPETITIVE LANDSCAPEKey Industry Players

Optical Sensors Market Competitive Landscape Overview

Optical Sensors Market is currently led by a handful of large semiconductor manufacturers that command the majority of revenue and drive technology roadmaps. Texas Instruments leverages its extensive analog portfolio to integrate photodiode front‑ends with on‑chip signal processing, while STMicroelectronics combines silicon‑photonic integration with automotive‑grade reliability, positioning itself as a key supplier for ADAS and smart‑factory applications. Honeywell International, through its precision measurement heritage, focuses on rugged IR and LIDAR modules for aerospace and defense, and Bosch Sensortec supplies compact, low‑power optical motion and proximity sensors that underpin consumer wearable devices. These incumbents dominate the market structure by offering end‑to‑end sensor solutions, investing heavily in miniaturization, and securing strategic collaborations with foundries to reduce unit costs, thereby setting high entry barriers for new entrants.Beyond the core giants, a cohort of specialized firms enriches the competitive landscape with niche expertise and innovative form factors. OmniVision Technologies supplies camera‑centric optical arrays for mobile and IoT devices, while AMS AG excels in advanced CMOS image sensors and ambient light solutions. Sony Semiconductor contributes high‑performance photodiodes and time‑of‑flight sensors for automotive LIDAR, and Panasonic delivers fiber‑optic sensing modules for industrial automation. TE Connectivity and On Semiconductor offer rugged optical transceivers for harsh environments, and Broadcom provides integrated optical transceiver IP for data‑center interconnects. Melexis and Osram Opto Semiconductors target automotive safety applications with high‑precision IR receivers, whereas Lumentum and II‑VI Incorporated focus on high‑bandwidth photonic components for telecom and sensing markets. Collectively, these players foster a vibrant ecosystem that drives continuous innovation across multiple verticals.

List of Key Optical Sensors Companies Profiled

- Texas Instruments

- STMicroelectronics

- Honeywell International

- Bosch Sensortec

- OmniVision Technologies

- AMS AG

- Sony Semiconductor

- Panasonic

- TE Connectivity

- On Semiconductor

- Broadcom

- Melexis

- Osram Opto Semiconductors

- Lumentum

- II-VI Incorporated

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Photodiodes • Serve as the foundational element for high‑precision light detection across multiple environments. • Benefit from ongoing miniaturization, enabling tighter integration within compact electronic systems. • Drive innovation in low‑power applications, supporting battery‑operated devices and wearables. |

| By Application |

|

Industrial Automation • Enables precise distance and position monitoring, enhancing robotic accuracy. • Supports predictive maintenance by detecting subtle changes in machine conditions. • Integrates seamlessly with emerging Industry 4.0 platforms for real‑time data exchange. |

| By End User |

|

Automotive OEMs • Rely on optical sensors for advanced driver‑assistance features and occupant monitoring. • Prioritize sensor reliability under harsh temperature and vibration conditions. • Seek integrated solutions that combine multiple sensing modalities for richer perception. |

| By Integration Level |

|

Monolithic Photonic‑Electronic Chips • Represent the leading trend toward ultra‑compact modules that embed optics directly on silicon. • Reduce signal latency and power consumption, vital for edge‑AI applications. • Accelerate product cycles as manufacturers can co‑design optics and electronics in a single process. |

| By Industry |

|

Healthcare & Wearables • Leverage optical sensors for non‑invasive monitoring of vital signs, driving the move toward continuous health tracking. • Emphasize biocompatibility and low‑heat operation to suit skin‑contact devices. • Benefit from advances in miniaturization that enable discreet form factors without compromising accuracy. |

Regional Analysis: North America

United States

The automotive sector is a primary driver of growth for optical sensors in the United States. Applications include lane departure warning systems, adaptive cruise control, automatic emergency braking, and pedestrian detection. Stringent safety regulations and the increasing demand for autonomous vehicles are propelling the adoption of these sensors.

Optical sensors play a crucial role in medical diagnostics, imaging systems, and patient monitoring devices. Applications range from blood glucose monitoring and optical coherence tomography to endoscopic imaging and flow cytometry. The aging population and the increasing prevalence of chronic diseases are fueling the demand for these advanced sensing technologies within the healthcare sector.

In industrial settings, optical sensors are used for object detection, barcode scanning, laser measurement, and quality inspection. They enhance efficiency, accuracy, and safety in manufacturing processes. The growing adoption of Industry 4.0 initiatives and the need for real-time data analysis are boosting the demand for these sensors.

Optical sensors are increasingly integrated into consumer electronics such as smartphones, wearables, and smart home devices. They enable features like facial recognition, gesture control, and ambient light sensing. The proliferation of the Internet of Things (IoT) is further driving the demand for these sensors in various connected devices.

Europe

Europe presents a diverse and competitive landscape for Optical Sensors Market. Germany, France, the United Kingdom, and Italy are key contributors to the region’s overall demand. The automotive industry in Europe is a major driver, with a strong emphasis on advanced driver-assistance systems and electric vehicles, necessitating sophisticated optical sensing solutions. The healthcare sector in countries like Germany and Switzerland also exhibits significant growth potential, particularly in areas like medical imaging and diagnostics. Furthermore, the increasing focus on sustainable manufacturing practices is driving the adoption of optical sensors for process monitoring and quality control in various industrial applications. Government initiatives promoting technological innovation and research funding play a crucial role in fostering the growth of Optical Sensors Market across Europe. The integration of optical sensors with smart city initiatives and the expansion of the IoT sector are also expected to contribute to future market expansion. The region’s commitment to environmental regulations is also influencing the development of optical sensors for environmental monitoring and pollution control.

Asia-Pacific

Asia-Pacific is the fastest-growing region for Optical Sensors Market, driven by rapid industrialization, increasing automotive production, and significant investments in infrastructure development. China, Japan, South Korea, and India are the key markets within the region. China’s automotive industry is experiencing exponential growth, leading to a surge in demand for optical sensors used in ADAS and autonomous driving systems. The electronics manufacturing sector in countries like South Korea and Taiwan also contributes significantly to the market’s expansion. The healthcare industry in Japan and India is witnessing increasing adoption of optical sensors for medical diagnostics and treatment. Government initiatives promoting domestic manufacturing and technological innovation are further fueling the growth of Optical Sensors Market in Asia-Pacific. The expanding IoT ecosystem and the increasing adoption of smart manufacturing practices are also expected to drive future market growth in this dynamic region.

South America

The South American market for optical sensors is characterized by moderate growth potential, driven primarily by the automotive and industrial sectors. Brazil and Argentina are the leading markets in the region. The automotive industry in Brazil is a significant consumer of optical sensors for applications such as parking assistance, collision avoidance, and adaptive cruise control. The mining and energy sectors in the region also utilize optical sensors for process monitoring and quality control. Increasing investments in infrastructure development and the growing adoption of automation technologies are expected to contribute to future market growth. However, factors such as economic volatility and regulatory complexities can pose challenges to market expansion in South America. The demand from the agricultural sector for optical sensors used in precision agriculture is also emerging as a potential growth area.

Middle East & Africa

The Middle East and Africa represent an emerging market for optical sensors, with growth driven by investments in infrastructure, increasing automotive production, and expanding industrial activities. The United Arab Emirates, Saudi Arabia, and South Africa are key markets in the region. The automotive sector in the Middle East is witnessing increasing adoption of advanced driver-assistance systems, leading to a growing demand for optical sensors. The oil and gas industry in the region utilizes optical sensors for pipeline monitoring, leak detection, and flow measurement. Investments in smart city initiatives and the growth of the construction industry are also expected to drive future market growth. However, political instability and economic fluctuations in some parts of the region can pose challenges to market expansion. The increasing focus on renewable energy projects may also create opportunities for optical sensors used in solar energy monitoring and control systems.

Report Scope

This market research report provides a comprehensive analysis of the Optical Sensors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical Sensors Market?

-> Optical Sensors Market was valued at USD 17.3 billion in 2025 and is expected to reach USD 35.8 billion by 2034.

Which key companies operate in Optical Sensors Market?

-> Key players include Texas Instruments, STMicroelectronics, Honeywell International, and Bosch Sensortec, among others.

What are the key growth drivers?

-> Key growth drivers include miniaturization and integration of photonic components, rising demand for ADAS, smart factories, and wearable health monitors.

Which region dominates the market?

-> The provided data does not specify a dominant region; regional performance will be detailed in the full report.

What are the emerging trends?

-> Emerging trends include silicon‑photonic integration breakthroughs, increased adoption in automotive ADAS, and expansion of smart‑factory sensor networks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...