Optical Lenses for Lithography Market Insights

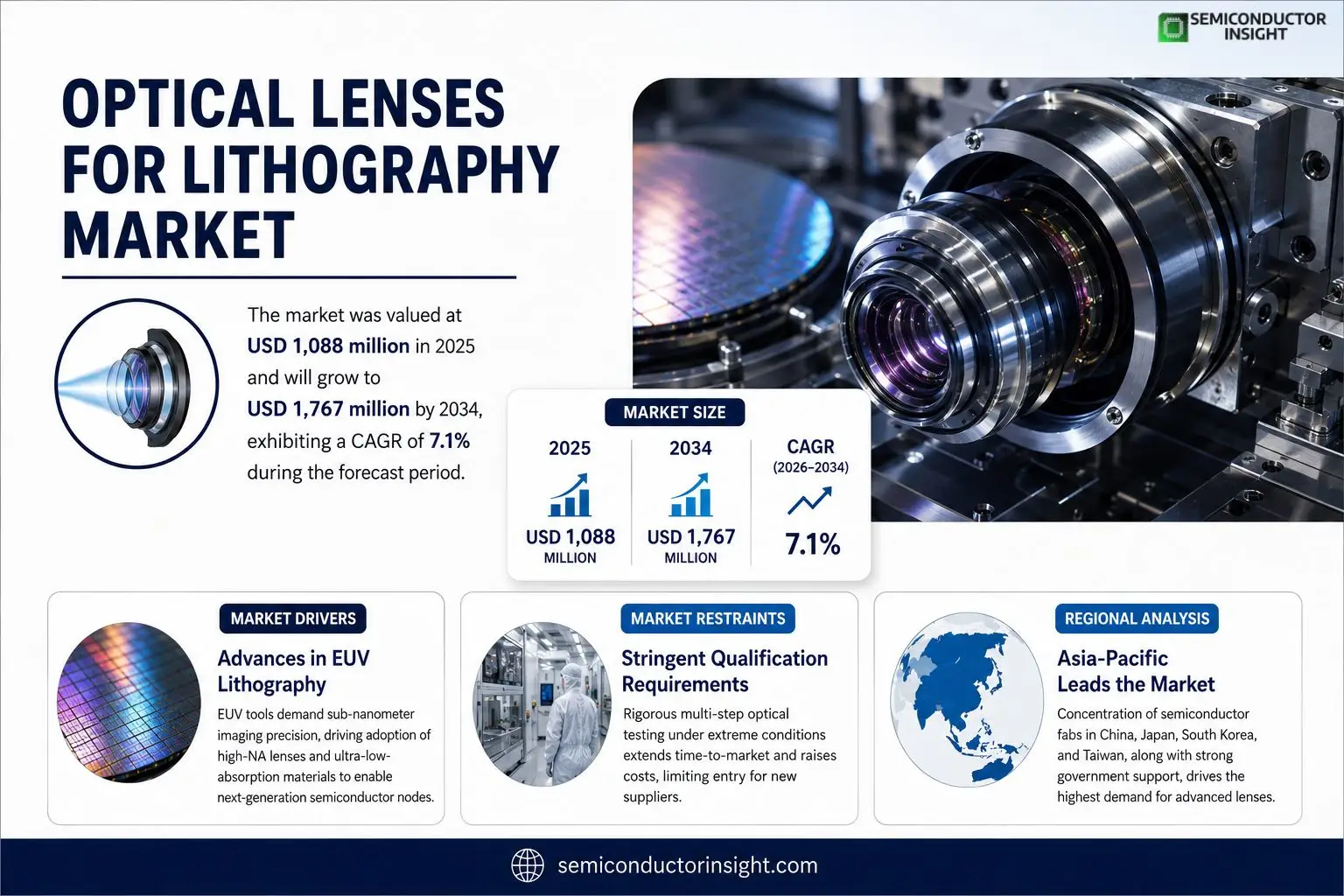

Optical Lenses for Lithography market was valued at USD 1,088 million in 2025 and will grow to USD 1,767 million by 2034, exhibiting a CAGR of 7.1% during forecast period.

Optical lenses for lithography are ultra‑high‑precision components that form core of lithographic projection systems used to transfer circuit patterns from a photomask onto silicon wafers coated with photoresist. By exploiting curvature differences, se lenses refract light and achieve exact magnification and focus through fine adjustments of distance, position and tilt among lens elements. Surface figure accuracy typically falls below one nanometer, while refractive‑index homogeneity and advanced anti‑reflective coatings are essential to limit wavefront error and light loss. portfolio comprises deep‑ultraviolet (DUV) lenses operating at 193 nm or 248 nm and extreme‑ultraviolet (EUV) reflective optics centered on 13.5 nm wavelength. market expands because semiconductor manufacturers pursue sub‑5 nm nodes and higher wafer yields, which raises demand for lenses that can sustain tighter critical‑dimension tolerances. In modern lithography tools optical subsystem represents roughly eighty percent of total equipment value; consequently any improvement in lens performance directly influences overall system cost efficiency. Recent activity includes ASML’s launch of a high‑NA EUV lens module in June 2024 and Zeiss’s introduction of a new DUV lens line featuring sub‑nanometer surface figure control. Major suppliers such as Corning (optical glass), Heraeus (syntic fused silica), Bond Optics and MLOPTIC provide upstream materials, while downstream demand is anchored by OEMs like ASML, Nikon and Canon.

MARKET DRIVERS

Advances in Extreme Ultraviolet (EUV) Lithography

Optical Lenses for Lithography Market is being reshaped by deployment of EUV tools that demand sub‑nanometer imaging precision. Chipmakers are replacing older immersion systems with EUV scanners, which in turn require lenses fabricated from ultra‑low‑absorption materials. This shift elevates premium tier of lens suppliers and creates a cascade of downstream equipment upgrades.

Demand for Higher Numerical Aperture (NA) Lenses

Production nodes now target 3 nm and below, a regime where higher NA lenses become indispensable for pattern fidelity. Manufacturers are investing in aspheric designs that mitigate diffraction artifacts, reby justifying higher capital outlays. trend forces vendors to accelerate R&D cycles, especially in coating technologies that preserve throughput under intense EUV flux.

➤ Strategic partnerships between lens producers and photomask firms are emerging as a direct response to NA challenge, enabling co‑development of inspection workflows that reduce yield loss.

Beyond equipment, emergence of heterogeneous integration in semiconductor packaging is prompting a secondary wave of lens demand. As foundries embed optical alignment modules directly onto wafer‑handling robots, market sees a diversification of end‑users beyond traditional fabs, expanding revenue base for specialized lens manufacturers.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Manufacturing

While performance premium of advanced lenses is clear, fabs operating at scale confront tight cost constraints. price differential between conventional and EUV‑qualified lenses can exceed 30 %, pressuring procurement teams to negotiate longer supply contracts and to justify expense through demonstrable yield improvements.

Or Challenges

Supply‑Chain Vulnerability

Intricate supply chain for high‑purity fused silica and specialty glass faces periodic disruptions, especially when geopolitical factors affect raw‑material exports. Firms that lack diversified sourcing strategies risk production bottlenecks that can cascade into wafer‑run delays.

MARKET RESTRAINTS

Stringent Qualification Requirements

qualification regime for lenses used in EUV lithography is exceptionally rigorous, involving multi‑step optical testing under vacuum and high‑intensity illumination. time‑consuming nature of qualification extends time‑to‑market for new designs, deterring niche players from entering space.

MARKET OPPORTUNITIES

Customization for Emerging 2‑D Materials

Researchers are exploring graphene, transition‑metal dichalcogenides, and or 2‑D substrates for next‑generation devices. se materials impose distinct optical requirements, such as reduced focal depth and altered wavelength tolerances. Lens manufacturers that develop bespoke solutions for se niche applications stand to capture early‑adopter revenue streams.

Optical Lenses for Lithography Market Trends

Precision Demands Driven by Sub‑5nm Node Advancement

shift toward sub‑5nm semiconductor nodes places unprecedented pressure on projection optics. Lens manufacturers must deliver surface‑figure tolerances well below a nanometer while maintaining homogenous refractive indices across large apertures. Even a marginal wave‑front error translates into critical‑dimension variation that can compromise yield on dense patterns. Consequently, design cycles have become more iterative, relying on advanced metrology that can resolve picometer‑scale deviations. premium placed on optical performance is reflected in fact that projection optics now represent roughly 80 % of a lithography system’s bill of materials, a proportion that has risen steadily as wavelength regimes moved from I‑line to deep‑ultraviolet (DUV) and extreme‑ultraviolet (EUV). Customers are refore willing to absorb higher unit costs to secure pattern fidelity required for next‑generation chips, prompting OEMs such as ASML and Nikon to prioritize lens‑module reliability in ir product roadmaps.

Or Trends

Supply‑Chain Tightening for High‑Purity Glass

Upstream, pool of suppliers capable of producing ultra‑low‑inclusion fused silica has narrowed to a handful of specialized firms. ir production lines operate at capacity limits, and any deviation in melt‑batch composition can cascade into costly re‑grinding steps downstream. result is a modest but persistent upward pressure on raw‑material pricing, which compresses gross margins for lens makers that depend on volume‑driven cost structures. To mitigate exposure, many manufacturers are establishing long‑term agreements with glass producers and investing in in‑house melt‑control facilities. Parallel efforts focus on diversifying coating‑material sources, as anti‑reflective multilayers now require rare‑earth compounds whose availability is subject to geopolitical fluctuations.

Margin Pressures from Coating Complexity

Anti‑reflective and protective coatings have evolved from single‑layer solutions to multilayer stacks engineered for specific wavelengths and numerical apertures. Each additional layer introduces process steps, inspection requirements, and defect‑control challenges that erode profitability. Companies are responding by automating coating deposition and by deploying AI‑assisted inspection to detect sub‑nanometer particles that would orwise cause yield loss. However, capital outlay for such systems is substantial, and return horizon extends beyond a single product cycle. As a strategic implication, firms that can harmonize coating R&D with downstream wafer‑fab feedback are better positioned to command premium pricing, while those that rely on legacy processes may see ir margin share shrink in competitive bids.

COMPETITIVE LANDSCAPE

Key Industry Players

Optical Lenses for Lithography: Competitive Overview

Sector is dominated by a handful of integrated‑optics powerhouses that combine deep R&D spend with exclusive access to ultra‑pure fused silica and proprietary coating chemistries. Carl Zeiss AG and Nikon Corporation hold largest market shares, largely because y supply high‑NA DUV and early‑generation EUV lens modules that form backbone of most leading‑edge scanners. ir vertical value‑chain controlfrom glass supplier contracts with Heraeus and Corning to in‑house metrologycreates a significant barrier for newcomers. Canon Inc., while traditionally stronger in i‑line and 248 nm platforms, has leveraged its semiconductor lithography legacy to capture a growing slice of EUV‑reflective‑optics market, especially in collaborative projects with ASML. se incumbents benefit from long‑term OEM agreements with major scanner manufacturers, ensuring stable demand that aligns with semiconductor industry’s node‑shrink cadence.Beyond tier‑one group, a constellation of specialized firms adds depth and regional nuance to competitive picture. Bond Optics and MLOPTIC Corp (Maolai Optics) have carved niches in custom DUV lens blanks, offering rapid prototyping services that appeal to fab‑level equipment integrators. Beijing Guowang Optics and Changchun Guoke Precision serve rapidly expanding Chinese foundry ecosystem, often partnering with domestic lithography OEMs to meet government‑backed capacity targets. European niche players such as SCHOTT and Hoya Corporation excel in high‑purity glass production, feeding both premium and mid‑tier lens segments. LightPath Technologies and Fuji Photo specialize in anti‑reflective coating solutions, a critical differentiator for EUV reflectors where every photon counts. presence of se firms creates a multi‑layered supply chain where large OEMs outsource specific sub‑assemblies, fostering a competitive environment that rewards technical agility and cost‑effective scale.

List of Key Optical Lenses for Lithography Companies Profiled

- Carl Zeiss AG

- Nikon Corporation

- Canon Inc.

- ASML Holding NV

- Heraeus Holding GmbH

- Corning Inc.

- SCHOTT AG

- Bond Optics

- MLOPTIC Corp (Maolai Optics)

- Beijing Guowang Optics

- Changchun Guoke Precision

- Hoya Corporation

- LightPath Technologies

- Fuji Photo Film Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

EUV Lenses are emerging as pivotal technology for sub‑5 nm nodes, driven by need for extreme resolution and depth‑of‑focus.

|

| By Application |

|

Projection Printing dominates market because it directly determines critical dimension uniformity and throughput.

|

| By End User |

|

Semiconductor manufacturers shape demand landscape by pushing process nodes to ever smaller dimensions.

|

| By Numerical Aperture |

|

Hyper NA Lenses are becoming focal point of advanced lithography roadmaps.

|

| By Wavelength |

|

EUV (13.5 nm) lenses represent strategic horizon of market.

|

Regional Analysis: Optical Lenses for Lithography Market

Aggressive node scaling, aggressive cost‑per‑wafer targets, and push for high‑NA (numerical aperture) systems converge to heighten demand for precision optical lenses. Manufacturers respond by investing in ultra‑low‑dispersion glass formulations that sustain image fidelity at extreme exposure energies.

A handful of legacy optics specialists dominate market, yet new entrants leveraging photonic‑integrated‑circuit platforms are gaining traction. Competitive pressure fosters collaborative R&D consortia that pool expertise across lithography equipment makers and lens fabricators.

transition to EUV (extreme ultraviolet) lithography has forced lens manufacturers to revisit coating technologies, emphasizing durability under high photon flux while preserving transmission efficiency.

Recent geopolitical shifts have prompted diversification of raw‑material sources, prompting firms to secure alternative glass vendors and to adopt modular production lines that can quickly re‑route capacity.

North America

In North America, market derives strength from a dense network of equipment OEMs and university research programs that pioneer novel lens geometries. region’s emphasis on intellectual property protection encourages firms to commercialize patented designs rar than license existing solutions, fostering a culture of differentiation. However, higher cost base and stricter environmental regulations mean that manufacturers must justify premium pricing through demonstrable performance gains, often by targeting niche high‑volume fabs that prioritize yield over cost. Strategic partnerships with chipmakers in United States are increasingly focused on co‑development of next‑generation immersion lenses, positioning region as a crucible for breakthrough optics despite its comparatively lower production volume.

Europe

European players leverage a heritage of precision optics engineering, translating heritage expertise in glass polishing into advanced lithography lenses. continent’s regulatory framework drives adherence to sustainability standards, prompting manufacturers to explore recyclable substrate materials and low‑temperature coating processes. Collaboration between German and Dutch firms and leading wafer fabs has yielded custom‑tailored lenses that address specific process windows, allowing European suppliers to maintain relevance through high‑value, low‑volume contracts. While market size lags behind Asia‑Pacific, focus on quality and compliance creates a niche where premium pricing is defensible.

South America

South America remains a peripheral market for optical lenses, yet recent investments in semiconductor assembly and testing facilities have sparked modest demand. Local distributors are beginning to act as aggregators for niche OEMs, offering value‑added services such as on‑site calibration. region’s growth is constrained by limited domestic fab capacity, but emergence of government‑driven initiatives to attract semiconductor back‑sourcing could modestly expand customer base over next decade.

Middle East & Africa

Middle East & Africa region currently occupies a supporting role, primarily as a consumer of imported high‑precision lenses for emerging photonics applications. Investment in data‑center infrastructure and nascent semiconductor design houses is gradually creating awareness of strategic importance of advanced lithography optics. Partnerships with European lens producers are facilitating technology transfer, laying groundwork for a modest but steady increase in local demand as regional players seek to move up value chain.

Report Scope

This market research report provides a comprehensive analysis of Optical Lenses for Lithography Market , covering forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping industry.

Key focus areas of report include:

- Market Overview: Report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including ir product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability of insights presented.

FREQUENTLY ASKED QUESTIONS:

What is current market size of Optical Lenses for Lithography Market?

-> Optical Lenses for Lithography Market was valued at USD 1088 million in 2025 and is expected to reach USD 1767 million by 2034, at a CAGR of 7.1% during forecast period.

Which key companies operate in Optical Lenses for Lithography Market?

-> Key players include Carl Zeiss AG, Nikon Corporation, Canon Inc., Bond Optics, MLOPTIC Corp (Maolai Optics), Beijing Guowang Optics, and Changchun Guoke Precision, among ors.

What are key growth drivers?

-> Key growth drivers include semiconductor industry’s relentless pursuit of sub‑5nm nodes, increasing wafer yields, need for ultra‑high‑precision lenses with sub‑nanometer surface figure accuracy, and fact that optical systems now account for roughly 80% of total lithography equipment value.

Which region dominates market?

-> Asia‑Pacific leads market due to concentration of semiconductor fabs and lithography equipment manufacturers in China, Japan, and South Korea.

What are emerging trends?

-> Emerging trends include shift toward EUV lithography lenses (especially high‑NA and hyper‑NA designs), increased adoption of reflective optics for 13.5 nm wavelengths, and continued innovation in anti‑reflective coating technologies to minimize light loss.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...