MARKET INSIGHTS

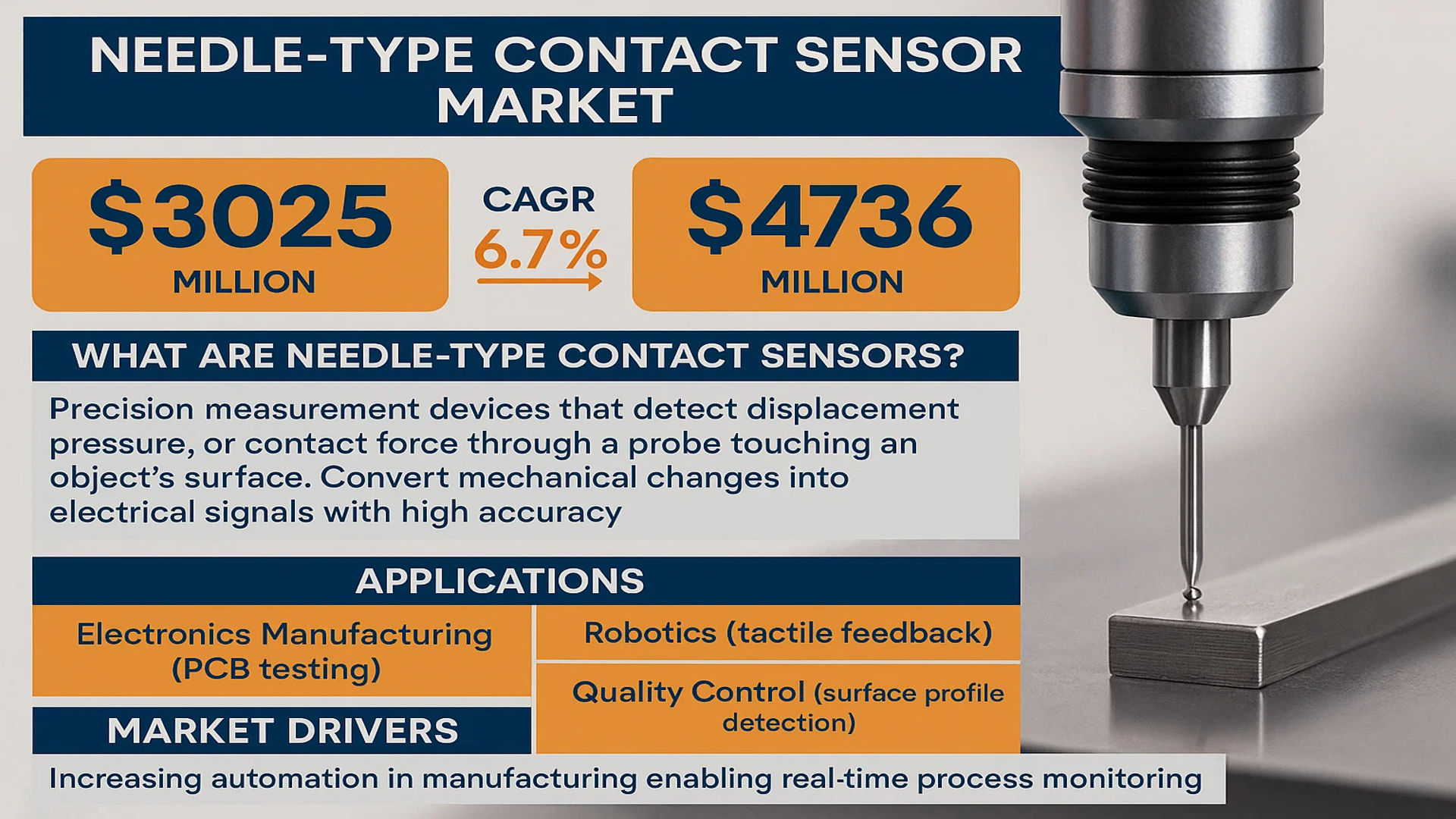

The global Needle-Type Contact Sensor Market was valued at 3025 million in 2024 and is projected to reach US$ 4736 million by 2032, at a CAGR of 6.7% during the forecast period.

Needle-type contact sensors are precision measurement devices that detect displacement, pressure, or contact force through a probe touching an object’s surface. These sensors convert minute mechanical changes into electrical signals with high accuracy, making them indispensable in applications requiring sub-micron precision. The technology finds widespread use across industries including electronics manufacturing (for PCB testing), robotics (tactile feedback), and quality control (surface profile detection).

Market growth is being driven by increasing automation in manufacturing, where these sensors enable real-time process monitoring. The electronics manufacturing segment accounted for 32% of total applications in 2024, as sensor miniaturization aligns with demand for smaller, more precise components. Recent innovations include multi-axis needle sensors capable of 3D surface mapping, with Keyence and Panasonic introducing models featuring 0.1μm resolution. While North America leads in industrial adoption (35% market share), Asia-Pacific shows the fastest growth (8.2% CAGR) due to expanding electronics production in China and Japan.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Precision Manufacturing to Fuel Needle-Type Contact Sensor Demand

The global shift towards Industry 4.0 and smart manufacturing is creating significant growth opportunities for needle-type contact sensors. These sensors play a critical role in quality control applications across automotive, aerospace, and electronics industries where micron-level precision is required. With manufacturers increasingly adopting automated inspection systems, the demand for high-accuracy contact sensors has grown by approximately 18% annually over the past three years. The automotive sector alone accounts for nearly 35% of total needle sensor deployments, driven by stringent quality requirements in powertrain component manufacturing.

Robotics Boom Accelerates Sensor Adoption

The rapid growth of industrial robotics, projected to maintain a compound annual growth rate of over 12% through 2030, is creating robust demand for tactile sensing solutions. Needle-type contact sensors provide essential feedback for robotic systems performing delicate assembly or inspection tasks. Collaborative robots (cobots) increasingly incorporate these sensors for force-limited applications where human-robot interaction occurs. Asia-Pacific leads this adoption curve, representing over 45% of global robotic sensor deployments, with China’s electronics manufacturing sector being particularly active in implementing these technologies.

Miniaturization Trend in Electronics Manufacturing

As electronic components continue shrinking, with semiconductor feature sizes now below 5nm, manufacturers require increasingly precise measurement tools. Needle-type sensors capable of resolving features below 10 microns have seen adoption rates triple in semiconductor backend processes since 2020. The proliferation of wearable devices and compact medical electronics has further driven demand for miniature contact probes that can verify component placement and surface profiles without damaging delicate substrates.

MARKET RESTRAINTS

High Costs Limit Adoption Among SMEs

While needle-type contact sensors deliver unparalleled precision, their sophisticated manufacturing processes and calibration requirements result in premium pricing that challenges budget-conscious buyers. A single high-end contact probe system can exceed $15,000, putting it out of reach for many small and medium manufacturers. This cost barrier restricts market penetration in developing economies where price sensitivity remains high, with some regions showing adoption rates 40% below global averages for comparable industrial applications.

Durability Concerns in Harsh Environments

Sensor longevity becomes a significant constraint in applications involving abrasive materials or corrosive conditions. Frequent probe tip replacement drives up total cost of ownership, with some automotive stamping operations reporting replacement cycles as short as three months. While advanced materials like tungsten carbide and synthetic ruby extend service life, they often increase initial costs by 25-30%. These durability challenges have slowed adoption in heavy industries despite the technology’s measurement capabilities.

MARKET OPPORTUNITIES

Emerging Applications in Medical Device Manufacturing

The medical technology sector presents significant growth potential for needle-type sensors, particularly in quality assurance for minimally invasive surgical tools and implantable devices. Precision measurement requirements for items like stents and orthopedic implants now demand sub-micron resolution that contact probes can reliably provide. The global market for medical device testing equipment incorporating such sensors is forecast to grow at nearly 9% annually through 2030, outpacing broader industrial measurement segments.

Integration with AI-Powered Inspection Systems

Advanced machine vision systems increasingly incorporate contact probe data to enhance defect detection algorithms. This convergence of tactile and visual measurement creates opportunities for sensor manufacturers to develop hybrid solutions. Early adopters in automotive electronics have achieved defect rate reductions exceeding 30% by combining these technologies, driving interest across multiple industries. The market for intelligent measurement systems utilizing both technologies is projected to exceed $2.5 billion by 2027.

MARKET CHALLENGES

Skilled Labor Shortage Impacts Implementation

The precision measurement field faces a critical shortage of technicians qualified to operate and maintain advanced contact measurement systems. Industry surveys indicate nearly 60% of manufacturers report difficulties finding personnel with the required metrology expertise. This skills gap becomes particularly acute when implementing complex multi-probe systems, often requiring extensive training programs that can delay production ramp-ups by several months.

Standardization Hurdles in Emerging Markets

Divergent measurement standards across regions complicate global deployments of contact sensing technologies. While ISO and ANSI standards dominate in North America and Europe, many Asian markets maintain separate certification requirements. These regulatory differences force manufacturers to maintain multiple product versions, increasing inventory costs by an estimated 15-20% for companies operating internationally.

NEEDLE-TYPE CONTACT SENSOR MARKET TRENDS

Integration of Miniaturized Sensors Boosts Demand in Precision Industries

The global needle-type contact sensor market is witnessing significant growth, driven by the rising demand for high-precision measurement tools in industries such as electronics manufacturing, robotics, and automated testing. Miniaturization of sensors has emerged as a key trend, with manufacturers developing ultra-sensitive probes capable of detecting micron-level deformations. The increasing complexity of electronic components, particularly in semiconductor fabrication, necessitates sensors with exceptionally high resolution. For instance, modern needle-type sensors now offer resolutions as fine as 0.1 µm in displacement measurement applications, making them indispensable in quality control processes. Further innovations in materials science, such as the adoption of diamond-coated probes, have extended their lifespan while maintaining measurement accuracy under repeated use.

Other Trends

Automation in Manufacturing Accelerates Adoption

As industries increasingly embrace Industry 4.0 and smart automation, the deployment of needle-type contact sensors has surged in robotic assembly and inspection systems. These sensors enable real-time monitoring of surface profiles, ensuring consistency in high-volume production lines. The automotive sector, for example, relies on them for in-line inspection of engine components and circuit boards, minimizing defects. Recent advancements in wireless data transmission have further enhanced their utility, allowing seamless integration into IoT-enabled industrial ecosystems. Additionally, the growing adoption of collaborative robots (cobots) in manufacturing has created new opportunities for tactile sensing solutions, where needle-type sensors provide crucial force feedback.

Expansion in Medical and Research Applications

Beyond traditional industrial uses, needle-type contact sensors are gaining traction in medical device manufacturing and biomedical research. Their ability to measure micro-scale forces and displacements has proven valuable in applications such as surgical robotics and tissue engineering. For instance, sensors with biocompatible tips are being utilized to assess the mechanical properties of artificial tissues. Meanwhile, academic and corporate R&D labs employ these sensors in material science studies, analyzing surface textures and elasticity at nano-level precision. This diversification into high-value niches is expected to contribute significantly to the market’s projected CAGR of 6.7%, positioning it to reach $4.7 billion by 2032.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Market Leadership in Needle-Type Contact Sensor Space

The global needle-type contact sensor market features a dynamic competitive environment where established players leverage their technological expertise to maintain dominance while emerging companies focus on niche applications. Keyence Corporation leads the market with its wide-ranging portfolio of high-precision contact sensors, particularly favored in automated manufacturing environments. The company’s strong presence across Asia and North America, coupled with its continuous R&D investments, positions it as the technology frontrunner.

Panasonic and Amphenol follow closely, capturing significant market share through their industrial sensor solutions. These players benefit from established distribution networks and long-term contracts with major electronics manufacturers. Their growth stems from both technological leadership and the ability to provide customized solutions for specialized applications in robotics and microelectronics.

Meanwhile, the market sees increasing competition from specialized firms such as Sugawara Laboratories and CCP Contact Probes, who focus on ultra-high precision measurement tools for semiconductor and medical device manufacturing. These companies compete through superior product differentiation rather than scale, offering specialized sensors with micron-level accuracy that larger players typically do not provide.

The competitive landscape continues to evolve as companies adopt various strategies – from Acmeto Technology Group’s recent expansion into European markets to Metrol’s strategic partnerships with robotic arm manufacturers. These moves demonstrate how vendors are positioning themselves to capitalize on the growing automation trend across multiple industries.

List of Key Needle-Type Contact Sensor Companies Profiled

- Keyence Corporation (Japan)

- Panasonic Corporation (Japan)

- Amphenol Corporation (U.S.)

- Sugawara Laboratories Inc. (Japan)

- CCP Contact Probes (U.S.)

- Acmeto Technology Group (China)

- Unipulse Corporation (Japan)

- Janpos Precision Instruments (Japan)

- Metrol Co., Ltd. (Japan)

- Sugiden Instruments (Japan)

Segment Analysis:

By Type

NPN Normally Open Type Leads Due to Its Wide Adoption in Automation and Robotics

The market is segmented based on type into:

- NPN Normally Open Type

- NPN Normally Closed Type

By Application

Precision Measurement Segment Holds Key Share Due to Rising Demand for Micro-Level Accuracy

The market is segmented based on application into:

- Precision Measurement

- Electronic Manufacturing

- Automated Testing

- Robotics

- Surface Profile Detection

By End User

Industrial Sector Dominates Owing to Increasing Automation in Manufacturing

The market is segmented based on end user into:

- Industrial

- Electronics

- Automotive

- Aerospace & Defense

- Medical Devices

Regional Analysis: Needle-Type Contact Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the Needle-Type Contact Sensor market due to rapid industrialization and widespread adoption of automation in manufacturing sectors. Countries like China, Japan, and South Korea lead in production and application, with China alone contributing approximately 40% of the global demand. Strong government support for smart manufacturing initiatives and the presence of key electronics manufacturers drive consistent growth. While cost-competitive NPN Normally Open Type sensors remain popular for basic applications, high-performance variants are gaining traction in semiconductor and robotics industries. The region benefits from local supply chains and technological expertise, though intellectual property concerns occasionally surface with regional competitors.

North America

North America represents the second-largest market, characterized by high-value precision applications in aerospace, medical devices, and advanced robotics. The U.S. accounts for over 65% of regional demand, with stringent quality standards pushing manufacturers toward closed-loop sensor systems with micron-level accuracy. Notable growth comes from reshoring initiatives in electronics manufacturing and increasing R&D investments in tactile robotics. However, higher production costs compared to Asian counterparts create pricing pressure. Leading players like Amphenol and CCP Contact Probes focus on customization and IP-protected designs to maintain market share against imported alternatives.

Europe

European demand centers on high-reliability industrial applications, particularly in German and Italian automotive/machinery sectors. Strict EU regulations on electromagnetic compatibility (EMC) and workplace safety standards favor suppliers offering certified products with robust documentation. While growth remains steady, market consolidation is occurring as mid-sized manufacturers struggle with energy costs and component shortages. Interestingly, the Nordic region shows above-average adoption in marine and renewable energy applications due to harsh environment requirements. European companies lead in miniaturized sensor solutions for medical and scientific instruments, though Asian competition in standard products intensifies yearly.

South America

Market development in South America faces infrastructure limitations, with Brazil and Argentina accounting for 80% of regional sensor usage. Primary demand comes from automotive assembly and basic industrial automation, favoring economical NPN-type sensors. Political-economic instability periodically disrupts supply chains, causing manufacturers to maintain higher inventories. Nonetheless, growing foreign investment in Mexican manufacturing presents opportunities, particularly for suppliers serving cross-border industries. The lack of localized technical support and calibration services remains a significant adoption barrier compared to more mature markets.

Middle East & Africa

This emerging market shows potential in oil/gas and construction equipment applications, though adoption rates lag behind global averages. The UAE and Saudi Arabia lead in high-end installations, often specifying corrosion-resistant variants for desert climates. Limited local technical expertise creates reliance on European and Asian suppliers for after-sales support. While overall market size remains small, projected infrastructure investments and gradual industrial automation suggest long-term growth potential, particularly if regional distributors strengthen service capabilities. Many projects currently use imported sensors due to unestablished local manufacturing bases.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Needle-Type Contact Sensor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Needle-Type Contact Sensor market was valued at USD 3,025 million in 2024 and is projected to reach USD 4,736 million by 2032, growing at a CAGR of 6.7% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (NPN Normally Open Type, NPN Normally Closed Type), application (Precision Measurement, Electronic Manufacturing, Automated Testing, Robotics, Surface Profile Detection), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market size is estimated at USD million in 2024, while China is forecast to reach USD million.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Acmeto Technology Group, Panasonics, Keyence, Sugawara Laboratories, Unipulse, Janpos, Metrol, Sugiden, CCP Contact Probes, and Amphenol.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in sensor applications, advancements in precision measurement techniques, and evolving industry standards for contact sensors.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing automation, demand for precision measurement) along with challenges (supply chain constraints, technical limitations in extreme environments).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the contact sensor market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Needle-Type Contact Sensor Market?

-> Needle-Type Contact Sensor Market was valued at 3025 million in 2024 and is projected to reach US$ 4736 million by 2032, at a CAGR of 6.7% during the forecast period..

Which key companies operate in Global Needle-Type Contact Sensor Market?

-> Key players include Acmeto Technology Group, Panasonics, Keyence, Sugawara Laboratories, Unipulse, Janpos, Metrol, Sugiden, CCP Contact Probes, and Amphenol, among others.

What are the key growth drivers?

-> Key growth drivers include increasing automation in manufacturing, rising demand for precision measurement in electronics, and expanding applications in robotics and surface profile detection.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by electronics manufacturing expansion, while North America remains a significant market due to advanced automation adoption.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with IoT systems, development of more durable probe materials, and increasing use in quality control applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...