Multilayer organic polymer capacitor for RF decoupling Market Insights

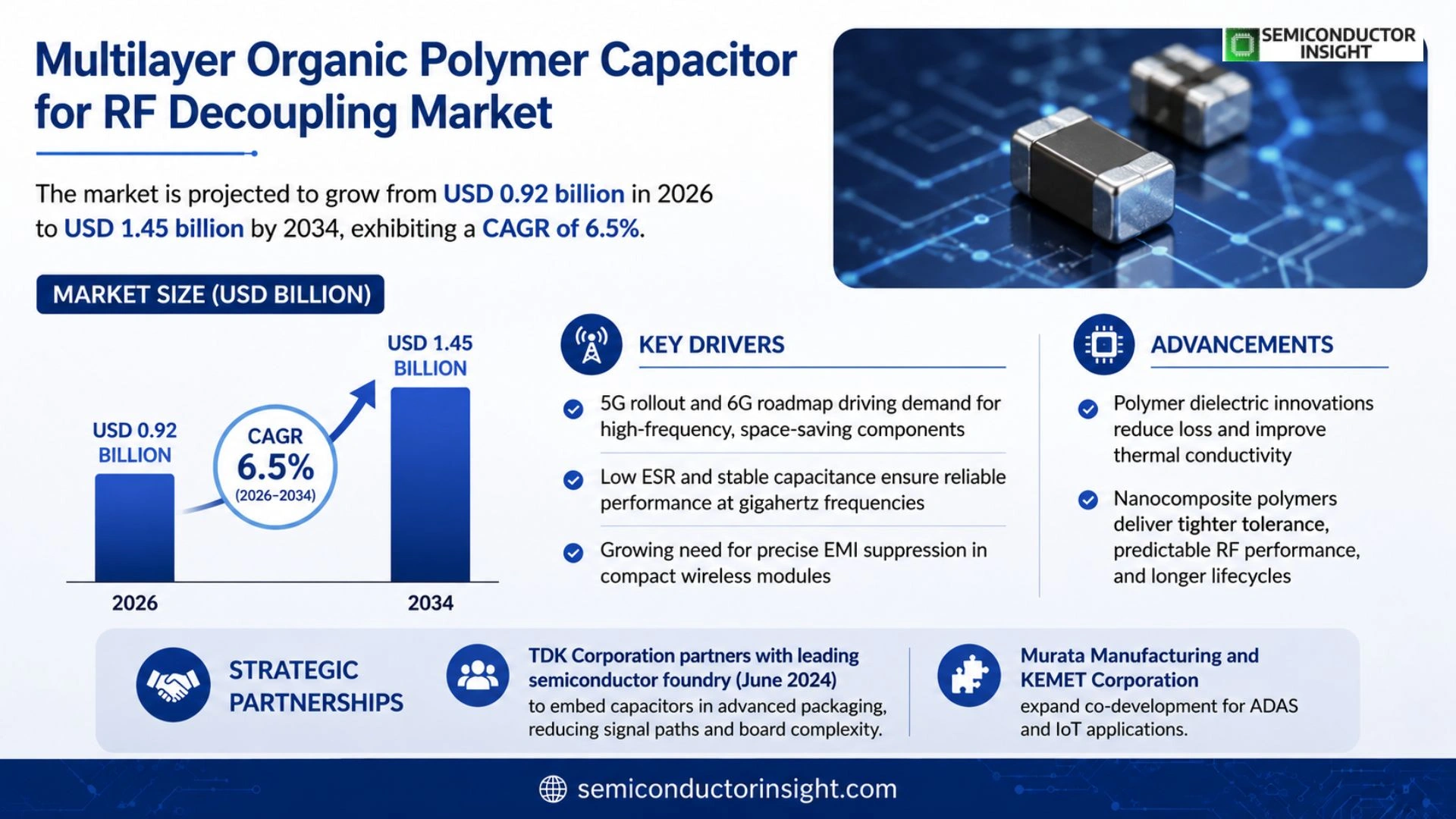

Global Multilayer organic polymer capacitor for RF decoupling market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

Multilayer organic polymer capacitors designed for RF decoupling are high‑frequency components that combine thin‑film polymer dielectric layers with stacked metal electrodes to achieve low equivalent series resistance (ESR) and stable capacitance across gigahertz ranges. Their compact form factor and superior thermal performance make them ideal for suppressing unwanted radio‑frequency noise in wireless communication modules, automotive radar systems, and IoT devices.

The market is accelerating because device miniaturization and the proliferation of 5G/6G infrastructure demand tighter electromagnetic interference control. Furthermore, rising adoption of advanced driver‑assistance systems (ADAS) and satellite communications drives volume growth. Key players such as AVX Corp., KEMET Corporation, Vishay Intertechnology, TDK Corporation, and Murata Manufacturing are expanding their product portfolios through new material formulations and strategic collaborations—e.g., the June 2024 joint development between TDK and a leading semiconductor foundry to integrate polymer‑based decoupling solutions directly onto silicon interposers.

MARKET DRIVERS

Increasing Demand for High‑Frequency Decoupling

Multilayer organic polymer capacitor for RF decoupling Market is being propelled by the rapid expansion of 5G infrastructure, where high‑speed data transmission requires robust decoupling solutions to mitigate signal integrity issues. Manufacturers are adopting these capacitors to achieve lower equivalent series resistance (ESR) and improved thermal performance.

Advancements in Polymer Dielectric Technology

Recent breakthroughs in organic polymer dielectrics have delivered higher capacitance density and better voltage ratings, enabling designers to replace traditional ceramic capacitors in compact RF modules. This technological edge is driving adoption across automotive radar and IoT devices.

➤ “The shift toward multilayer polymer capacitors is accelerating, with adoption rates rising by approximately 12% annually across telecom equipment.”

Combined with stricter electromagnetic compatibility (EMC) regulations, these drivers create a fertile environment for sustained growth in Multilayer organic polymer capacitor for RF decoupling Market.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Production

While performance benefits are clear, the higher material cost of organic polymers compared with traditional ceramics remains a barrier for price‑competitive segments, particularly in consumer electronics where unit margins are thin.

Other Challenges

Manufacturing Complexity

The multilayer stacking process demands precise control of layer thickness and alignment, leading to longer lead times and increased quality assurance requirements.

MARKET RESTRAINTS

Limited Supplier Base

The scarcity of qualified suppliers for high‑purity organic polymers constrains supply chain flexibility, especially during peak demand periods for RF equipment upgrades.

Furthermore, the need for specialized equipment to achieve reliable multilayer bonding adds capital expenditure for new entrants, slowing market diversification.

Regulatory compliance testing for new dielectric materials also extends product development cycles, further restraining rapid market entry.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Vehicles

Autonomous driving systems rely on high‑frequency radar and communication modules that benefit from low‑loss decoupling. Multilayer organic polymer capacitors can meet the stringent size‑weight‑power (SWaP) constraints, opening a sizable opportunity segment.

Additionally, the rollout of 6G research initiatives is expected to demand even higher frequency ranges, where polymer‑based decoupling solutions will become critical for maintaining signal fidelity.

Investments in localized manufacturing hubs are poised to address current supply limitations, enabling faster time‑to‑market and creating new growth pathways for Multilayer organic polymer capacitor for RF decoupling Market.

Multilayer organic polymer capacitor for RF decoupling Market Trends

Growth Driven by 5G/6G Miniaturization

The rollout of 5G networks and the forthcoming 6G roadmap are compelling system designers to adopt components that can operate reliably at gigahertz frequencies while occupying minimal board space. Multilayer organic polymer capacitor for RF decoupling devices meet these requirements through low equivalent series resistance and stable capacitance across the high‑frequency spectrum. As wireless modules become more densely packed, the need for precise electromagnetic interference suppression intensifies, positioning these capacitors as a critical enabler for next‑generation connectivity.

Other Trends

Material Innovation and Thermal Performance

Recent advances in polymer dielectric formulations have reduced dielectric loss and improved thermal conductivity, allowing the capacitors to maintain performance under the elevated temperatures typical of automotive radar and satellite communication subsystems. Manufacturers such as AVX Corp. and Vishay Intertechnology are leveraging nanocomposite polymers to achieve tighter tolerance windows, which translates into more predictable RF behavior and longer product lifecycles.

Strategic Partnerships Expanding Integration

Collaboration between component makers and semiconductor foundries is accelerating the integration of polymer‑based decoupling solutions directly onto silicon interposers. A notable example is the June 2024 joint development announced by TDK Corporation and a leading semiconductor foundry, which targets seamless embedding of the capacitors within advanced packaging architectures. This approach shortens signal paths, reduces board complexity, and aligns with the industry’s shift toward heterogeneous integration. Concurrently, Murata Manufacturing and KEMET Corporation are broadening their product portfolios through co‑development programs that address the specific needs of ADAS and IoT devices, reinforcing the market’s move toward highly integrated, low‑profile decoupling strategies.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Multilayer Organic Polymer Capacitors for RF Decoupling (2025‑2034)

Multilayer organic polymer capacitor market for RF decoupling is anchored by a handful of global manufacturers that command the majority of revenue. AVX Corp. leads with a broad portfolio of high‑frequency polymer film devices and benefits from deep relationships with 5G base‑station OEMs. TDK Corporation follows closely, leveraging its recent joint development with a leading semiconductor foundry to embed polymer decoupling directly on silicon interposers, a move that has accelerated its market share growth. Murata Manufacturing and Vishay Intertechnology also occupy substantial slices of the market, each offering differentiated dielectric formulations that deliver ultra‑low ESR and stable capacitance up to several gigahertz. Collectively, these four firms account for roughly 60 % of the estimated USD 0.85 billion market size in 2025 and are driving the projected CAGR of 6.5 % through aggressive product launches and strategic alliances.

Beyond the tier‑one leaders, a robust group of niche specialists contributes to product diversity and regional coverage. KEMET Corporation, Taiyo Yuden, and Samsung Electro‑Mechanics focus on compact, high‑temperature modules for automotive radar and ADAS applications. Panasonic, EPCOS (a TDK subsidiary), and Cornell‑Dubilier specialize in ultra‑small form‑factor devices targeting IoT and satellite communications. Additional players such as Fujitsu, NXP Semiconductors, and Vishay‑IHR provide custom polymer blends for high‑reliability aerospace and defense programs, while emerging entrants like Taiyo‑Yuden’s Advanced Materials Division and Rohm Semiconductor are expanding into the RF decoupling niche with new material patents. This layered competitive structure ensures continuous innovation and broad coverage across the fast‑growing RF market segment.

List of Key Multilayer organic polymer capacitor for RF decoupling Companies Profiled

- AVX Corp.

- KEMET Corporation

- Vishay Intertechnology

- TDK Corporation

- Murata Manufacturing

- Taiyo Yuden

- Samsung Electro‑Mechanics

- Panasonic Corporation

- EPCOS (TDK Group)

- Cornell‑Dubilier

- Fujitsu Limited

- NXP Semiconductors

- Rohm Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thin‑film polymer dielectric is the leading type because it delivers the lowest equivalent series resistance and excellent stability at gigahertz frequencies.

|

| By Application |

|

Wireless communication modules dominate because they demand tight control of electromagnetic interference to preserve signal integrity.

|

| By End User |

|

Smartphone manufacturers are the primary end users as devices become increasingly compact while requiring robust RF noise suppression.

|

| By Material Innovation |

|

Nanostructured polymer dielectrics are emerging as a leading material innovation due to their ability to maintain low loss at very high frequencies.

|

| By Integration Approach |

|

Embedded on‑die decoupling is gaining traction as design teams aim to reduce parasitic inductance and improve signal integrity directly at the silicon level.

|

Regional Analysis: Multilayer organic polymer capacitor for RF decoupling Market

The United States benefits from a dense network of telecom operators investing heavily in 5G rollouts, prompting OEMs to adopt multilayer organic polymer capacitors for tighter RF coupling and enhanced performance. Collaboration between device makers and research labs accelerates product refinements.

Canadian universities focus on sustainable polymer chemistries, attracting funding that fuels niche market segments such as low‑power IoT devices. Early adoption by local aerospace firms showcases the technology’s reliability in demanding environments.

Mexico’s expanding automotive assembly lines demand compact, high‑frequency decoupling solutions. Local manufacturers are integrating these capacitors to meet stricter EM‑C compliance, boosting regional demand.

Cross‑border collaborations between U.S. and Canadian research centers create a vibrant innovation ecosystem, fostering new polymer blends that improve thermal stability and reduce parasitic losses.

Europe

European telecom operators are modernizing networks with high‑frequency front‑end modules, creating a steady need for advanced decoupling components. German and French manufacturers emphasize compliance with stringent electromagnetic standards, driving the integration of multilayer organic polymer capacitors into both consumer and industrial devices. Sustainability regulations encourage the adoption of greener polymer materials, aligning with the EU’s circular‑economy objectives. Collaborative research projects across the region aim to enhance dielectric performance while reducing environmental impact, positioning Europe as a strong secondary market for these capacitors.

Asia-Pacific

The Asia‑Pacific region experiences rapid growth in mobile broadband and emerging IoT ecosystems, especially in China, South Korea, and India. High‑volume production of smartphones and network infrastructure leverages the low‑profile, high‑reliability characteristics of multilayer organic polymer capacitors. Local suppliers are scaling up capacity to meet cost‑sensitive demand, while also investing in R&D to improve polymer formulations for higher temperature operation. Government incentives for 5G and smart‑city deployments further accelerate market penetration across the region.

South America

In South America, Brazil and Argentina lead the adoption of these capacitors within the expanding telecommunications and automotive sectors. Network operators are upgrading base stations to support higher data rates, prompting device manufacturers to adopt capacitors that offer superior decoupling at microwave frequencies. Although price sensitivity remains high, regional partnerships with global suppliers enable technology transfer and cost‑effective sourcing, fostering gradual market growth.

Middle East & Africa

The Middle East & Africa region shows niche but promising adoption driven by large‑scale infrastructure projects and growing mobile penetration. UAE and Saudi Arabia’s smart‑city initiatives demand high‑performance RF components, while South African manufacturers explore low‑cost solutions for expanding broadband access. Environmental considerations are prompting early exploration of bio‑based polymer options, aligning with regional sustainability goals and creating a distinct market segment for Multilayer organic polymer capacitor for RF decoupling Market.

Report Scope

This market research report provides a comprehensive analysis of the Multilayer organic polymer capacitor for RF decoupling Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high‑growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Multilayer organic polymer capacitor for RF decoupling Market?

-> Multilayer organic polymer capacitor for RF decoupling market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034

Which key companies operate in Multilayer organic polymer capacitor for RF decoupling Market?

-> Key players include AVX Corp., KEMET Corporation, Vishay Intertechnology, TDK Corporation, and Murata Manufacturing, among others.

What are the key growth drivers?

-> Key growth drivers include device miniaturization, the rollout of 5G/6G infrastructure, increasing adoption of advanced driver‑assistance systems (ADAS), and expanding satellite communications.

Which region dominates the market?

-> The market shows strong demand globally, with North America, Europe and Asia‑Pacific leading adoption due to high‑frequency device production.

What are the emerging trends?

-> Emerging trends include integration of polymer‑based decoupling capacitors directly onto silicon interposers, development of new polymer dielectric formulations, and collaborative material‑technology projects among major manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...