MARKET INSIGHTS

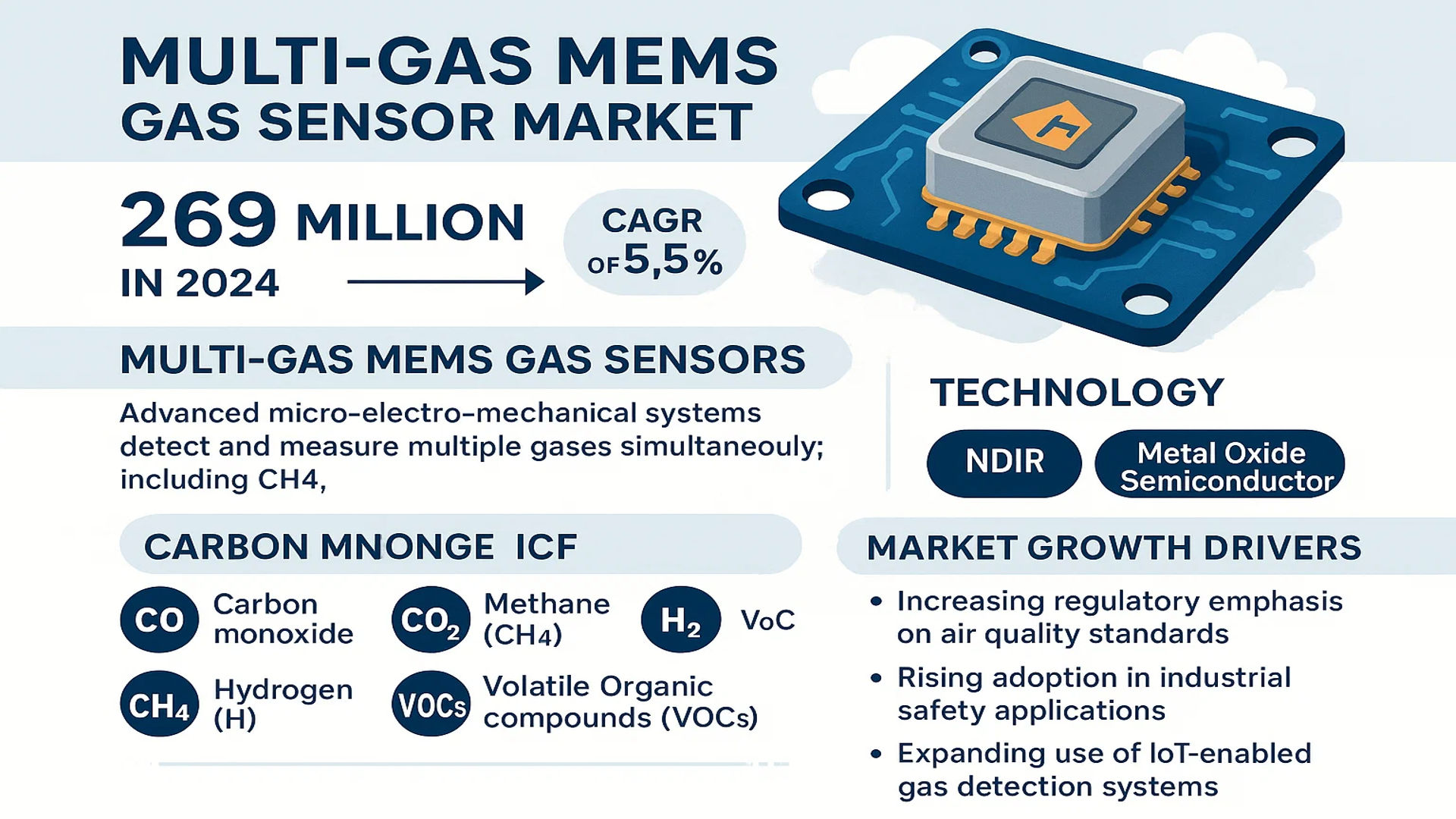

The global Multi-Gas MEMS Gas Sensor Market was valued at 269 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 5.5% during the forecast period.

Multi-Gas MEMS Gas Sensors are advanced micro-electro-mechanical systems designed to detect and measure multiple gases simultaneously, including carbon monoxide (CO), carbon dioxide (CO2), methane (CH4), hydrogen (H2), and volatile organic compounds (VOCs). These sensors integrate MEMS technology with sophisticated gas detection mechanisms such as NDIR (Non-Dispersive Infrared) and Metal Oxide Semiconductor principles, offering advantages like compact design, energy efficiency, and real-time monitoring capabilities.

The market growth is driven by increasing regulatory emphasis on air quality standards, rising adoption in industrial safety applications, and the expanding use of IoT-enabled gas detection systems. However, challenges such as cross-sensitivity issues and calibration complexities persist. Key players like Amphenol, Senseair, and Figaro are actively innovating to address these challenges, with recent developments focusing on enhanced selectivity and integration with wireless networks for smarter environmental monitoring solutions.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Environmental Regulations to Drive Adoption of Multi-Gas MEMS Sensors

Increasingly stringent environmental protection regulations worldwide are creating significant demand for advanced gas detection technologies. Governments globally are implementing tighter emissions standards, particularly for industrial facilities and automotive applications. Multi-Gas MEMS sensors play a crucial role in monitoring volatile organic compounds, greenhouse gases, and other pollutants with high accuracy. The European Union’s recent Industrial Emissions Directive (IED) requires continuous monitoring of multiple gas emissions, creating immediate demand for sophisticated detection solutions. Similar regulations in North America and Asia are following suit, establishing a robust regulatory-driven demand environment for these sensors.

Growing Smart City Initiatives Accelerate Deployment Across Urban Infrastructure

The rapid expansion of smart city projects globally represents a major growth driver for multi-gas MEMS sensors. Municipalities are increasingly integrating these sensors into urban air quality monitoring networks, smart building systems, and transportation infrastructure. With over 1000 smart city projects currently underway worldwide, the need for compact, low-power sensors capable of detecting multiple gases simultaneously has surged. These sensors enable real-time environmental monitoring that helps cities manage pollution levels, optimize energy consumption, and improve public health outcomes through data-driven decision making.

Industrial Safety Requirements Fuel Demand in Manufacturing Sectors

Industrial applications remain the largest end-use segment for multi-gas MEMS sensors, driven by mandatory workplace safety regulations. The oil & gas, chemical processing, and manufacturing sectors require continuous monitoring for hazardous gases like methane, hydrogen sulfide, and carbon monoxide. Recent advancements in sensor miniaturization and selectivity have enabled their integration into personal protective equipment, fixed monitoring systems, and autonomous inspection robots. The global industrial safety equipment market’s projected growth underscores the expanding opportunities for gas detection technologies in occupational health and safety applications.

MARKET RESTRAINTS

High Development Costs and Technical Complexity Limit Market Penetration

While demand for multi-gas MEMS sensors is growing, their widespread adoption faces significant technical and economic barriers. Developing sensors capable of accurately detecting multiple gases simultaneously requires substantial R&D investment, often running into millions per product development cycle. The need for specialized materials, precise calibration, and advanced signal processing algorithms result in higher unit costs compared to single-gas alternatives. This price sensitivity is particularly acute in cost-conscious markets, where buyers may opt for less sophisticated solutions despite performance trade-offs.

Cross-Sensitivity Issues Affect Measurement Accuracy

A key technical challenge facing multi-gas MEMS sensors involves cross-sensitivity between different gas species, which can compromise measurement accuracy. The presence of multiple gases in a sample can create interference patterns that complicate data interpretation. While advanced filtering algorithms have improved performance, these solutions often require frequent recalibration and sophisticated signal processing, adding to operational complexity. This limitation remains particularly problematic in industrial environments with complex gas mixtures, where false readings could have significant safety implications.

Limited Standardization Hampers Interoperability

The lack of universal standards for multi-gas MEMS sensor performance metrics creates adoption barriers across different industries and regions. Unlike other sensing technologies that benefit from well-established testing protocols, multi-gas MEMS devices often face inconsistent evaluation criteria from different regulatory bodies. This fragmentation increases compliance costs for manufacturers while creating uncertainty among end-users about product reliability and performance claims. Efforts to develop industry-wide standards are underway but have yet to achieve widespread recognition.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicle Battery Monitoring Present New Growth Frontiers

The rapid electrification of transportation is creating novel applications for multi-gas MEMS sensors in battery safety systems. Modern lithium-ion battery packs require continuous monitoring for thermal runaway precursors such as hydrogen, carbon monoxide, and volatile organic compounds. Automakers are increasingly incorporating these sensors into battery management systems as a critical safety feature. With electric vehicle production expected to grow substantially, this emerging application represents a significant expansion opportunity for sensor manufacturers to diversify beyond traditional markets.

Integration with IoT Platforms Expands Data Monetization Potential

The combination of multi-gas MEMS sensors with cloud-based IoT platforms unlocks valuable data analytics capabilities. Real-time gas concentration data, when combined with other environmental parameters, enables predictive maintenance models and process optimization algorithms. This creates recurring revenue opportunities for sensor manufacturers through value-added services, moving beyond hardware sales alone. Leading industrial companies are increasingly willing to pay premium prices for comprehensive monitoring solutions that deliver actionable insights rather than standalone sensor devices.

Miniaturization Breakthroughs Enable Wearable Health Monitoring

Recent advances in MEMS fabrication techniques have created opportunities in personal health monitoring applications. Compact multi-gas sensors capable of detecting biomarkers in human breath are being integrated into wearable devices for early disease detection. The potential to monitor multiple health indicators simultaneously – from metabolic byproducts to environmental exposures – represents a transformative application in preventative healthcare. While still in early stages, this segment could become significant as clinical validation progresses and regulatory approvals are secured.

MARKET CHALLENGES

Extended Product Development Cycles Delay Time-to-Market

The development timeline for advanced multi-gas MEMS sensors presents a significant challenge for market participants. From initial concept to commercial production, these sensors typically require extended development periods due to the complex interplay of chemical sensing, microelectronics, and data processing components. Testing and validation processes alone can take months as manufacturers must verify performance across diverse environmental conditions and gas mixtures. This elongated development cycle makes it difficult to quickly respond to shifting market demands or emerging application requirements.

Intense Competition from Alternative Sensing Technologies

While MEMS technology offers advantages in miniaturization and integration, it faces competition from alternative sensing approaches such as optical spectroscopy and electrochemical cells. These competing technologies often demonstrate superior performance in specific applications, particularly where extreme accuracy or long-term stability are paramount. The presence of these alternatives creates pricing pressure and forces MEMS sensor manufacturers to continually justify their value proposition through enhanced features or cost reductions.

Supply Chain Vulnerabilities Impact Production Consistency

The specialized materials and components required for multi-gas MEMS sensors create supply chain vulnerabilities that can disrupt production. Many sensors rely on rare-earth materials or proprietary semiconductor processes that have limited supplier bases. Geopolitical tensions and trade restrictions have exacerbated these vulnerabilities, leading to extended lead times and occasional production bottlenecks. Manufacturers must navigate these challenges while maintaining product quality and meeting increasing market demand.

MULTI-GAS MEMS GAS SENSOR MARKET TRENDS

Integration of IoT and Smart Technologies to Drive Market Growth

The global Multi-Gas MEMS Gas Sensor market is witnessing significant growth due to the increasing adoption of smart technologies and the Internet of Things (IoT). These sensors play a crucial role in real-time gas monitoring across industrial, residential, and commercial applications. The rapid expansion of smart city initiatives and the increasing demand for air quality monitoring solutions are further accelerating market growth. Projections indicate a market valuation of approximately $390 million by 2032, driven by the integration of MEMS gas sensors in IoT-based environmental monitoring systems. With advancements in wireless connectivity and low-power consumption designs, these sensors are becoming more efficient and capable of operating in diverse environments.

Other Trends

Shift Toward Low-GWP Refrigerants and Safety Compliance

With growing environmental concerns, industries are transitioning toward low Global Warming Potential (GWP) refrigerants, many of which are flammable or toxic. This shift has heightened the need for precise gas detection technologies, with Multi-Gas MEMS Sensors emerging as a critical solution due to their ability to detect multiple hazardous gases simultaneously. The demand for refrigerant leak detection, particularly in HVAC-R (Heating, Ventilation, Air Conditioning, and Refrigeration) systems, is expected to drive sensor adoption. Governments are also enforcing stricter safety regulations, further boosting the market for reliable gas detection solutions.

Advancements in Sensor Miniaturization and Energy Efficiency

Manufacturers are investing heavily in improving MEMS sensor miniaturization and power efficiency to enhance their application in portable and battery-operated devices. Nanotechnology and micro-fabrication techniques have enabled the development of ultra-compact multi-gas sensors with high sensitivity and low power consumption. These innovations are driving adoption in wearable devices, automotive air quality monitoring, and smart home applications. Furthermore, improvements in metal-oxide semiconductor (MOS) and non-dispersive infrared (NDIR) sensing technologies are enhancing the accuracy and response time of these sensors, making them indispensable for industrial safety and environmental monitoring.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Dynamics

The global Multi-Gas MEMS Gas Sensor market showcases a moderately fragmented competitive landscape, characterized by a mix of established players and emerging innovators competing for dominance across key regions, including North America, Europe, and Asia-Pacific. Amphenol Corporation leads the market with its diversified product portfolio and strong foothold in industrial and environmental gas sensing applications. Their strategic partnerships with automotive and HVAC manufacturers have reinforced their market position, contributing significantly to their revenue share, estimated at 18% in 2024.

Meanwhile, Senseair AB and Figaro Engineering Inc. have gained traction due to their advanced non-dispersive infrared (NDIR) sensors, which dominate the residential and commercial segments. These players have collectively captured nearly 25% of the market, driven by rising demand for energy-efficient and IoT-enabled gas detection solutions. Their R&D investments in miniaturized sensors and low-power consumption technologies have further enhanced their competitive edge.

Recent developments highlight a surge in collaborations aimed at expanding geographic reach. For instance, NISSHA Co., Ltd. acquired a European sensor manufacturer in early 2024 to bolster its presence in the region’s industrial safety sector. Similarly, Cubic Sensor and Instrument Co. announced a joint venture with a Chinese automotive supplier, reflecting the industry’s shift toward integrated solutions for electric vehicle battery monitoring.

Smaller players like smartGAS Mikrosensorik GmbH and Dynament Ltd. are carving niches by focusing on specialty gases and customized sensor modules. Their agility in addressing niche applications—such as refrigerant leak detection in green buildings—positions them for above-average growth despite intense competition from larger firms.

List of Key Multi-Gas MEMS Sensor Companies Profiled

- Amphenol Corporation (U.S.)

- Senseair AB (Sweden)

- smartGAS Mikrosensorik GmbH (Germany)

- Figaro Engineering Inc. (Japan)

- NISSHA Co., Ltd. (Japan)

- Veris Industries (U.S.)

- Dynament Ltd. (U.K.)

- Cubic Sensor and Instrument Co. (China)

Segment Analysis:

By Type

NDIR (Non-Dispersive Infrared) Sensors Dominate the Market Due to Their High Accuracy in Gas Detection

The market is segmented based on type into:

- NDIR (Non-Dispersive Infrared) Sensors

- Subtypes: Single-channel, Multi-channel, and others

- Metal Oxide Semiconductor Sensors

- Subtypes: Carbon-based, Tin oxide-based, and others

By Application

Industrial Segment Leads Due to Strict Safety Regulations and Demand for Continuous Monitoring

The market is segmented based on application into:

- Residence

- Business

- Industrial

By Detection Capability

Multi-Gas Detection Systems Gain Preference Over Single-Gas Detectors

The market is segmented based on detection capability into:

- Single-gas detectors

- Multi-gas detectors

- Subtypes: 2-gas, 4-gas, and 6-gas systems

By End-Use Industry

Oil & Gas Sector Remains Key Consumer of Multi-Gas MEMS Sensors

The market is segmented based on end-use industry into:

- Oil & Gas

- Chemicals

- Mining

- Environmental Monitoring

- Automotive

Regional Analysis: Multi-Gas MEMS Gas Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the global Multi-Gas MEMS Gas Sensor market, accounting for over 38% of total revenue in 2024. Rapid industrialization in China and India, coupled with strict workplace safety regulations, drives demand for gas detection across manufacturing, oil & gas, and chemical sectors. China’s 14th Five-Year Plan prioritizes industrial automation and environmental monitoring, accelerating adoption of MEMS-based sensors. Meanwhile, Japan and South Korea lead in technological advancements, with key players like Figaro Engineering investing in miniaturized NDIR sensors for consumer electronics and automotive applications. However, price sensitivity remains a challenge for widespread adoption in developing markets.

North America

Stringent safety standards from OSHA and the EPA, along with growing smart city initiatives, position North America as the second-largest market. The U.S. contributes 72% of regional demand, particularly for industrial leak detection and HVAC monitoring systems. Recent Biden administration policies, including the Inflation Reduction Act, allocate funds for air quality monitoring infrastructure, benefiting MEMS sensor manufacturers. Canada’s focus on methane emission reduction in oilfields further propels demand for multi-gas detection solutions. However, high product costs compared to conventional sensors restrain market penetration among small enterprises.

Europe

Europe’s market growth is propelled by the EU Industrial Emissions Directive and REACH regulations mandating toxic gas monitoring. Germany leads with 28% of regional revenue, driven by its robust automotive sector adopting MEMS sensors for battery safety in electric vehicles. The Nordic countries demonstrate strong adoption in smart buildings, leveraging the technology’s low-power advantages for wireless air quality networks. Brexit-induced supply chain disruptions have temporarily impacted UK market growth, though recovery is evident with renewed investments in industrial IoT applications.

Middle East & Africa

This emerging market shows promising growth, particularly in GCC countries implementing Vision 2030 diversification plans. Oil refineries and petrochemical plants in Saudi Arabia and the UAE are transitioning from fixed gas detectors to MEMS-based portable systems for worker safety. Israel’s thriving tech ecosystem fosters innovations in nanotechnology-enhanced sensors. However, political instability in some African nations and reliance on imported sensors hinder market expansion. The region’s growth potential lies in urban air quality monitoring projects funded by development banks.

South America

Brazil and Argentina drive regional demand, primarily for industrial safety applications in mining and agriculture. The Brazilian government’s NR-22 mining safety regulations mandate continuous gas monitoring, creating steady demand. Economic volatility and currency fluctuations, however, make technology upgrades challenging for local manufacturers. Recent discoveries of lithium reserves in Argentina present new opportunities for gas sensors in battery production facilities. The lack of local MEMS fabrication units results in dependence on North American and Asian imports.

Report Scope

This market research report provides a comprehensive analysis of the global Multi-Gas MEMS Gas Sensor market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Multi-Gas MEMS Gas Sensor market was valued at USD 269 million in 2024 and is projected to reach USD 390 million by 2032, growing at a CAGR of 5.5%.

- Segmentation Analysis: Detailed breakdown by product type (NDIR and Metal Oxide Semiconductor Sensors), application (Residential, Business, Industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets.

- Competitive Landscape: Profiles of leading market participants including Amphenol, Senseair, smartGAS, Figaro, and NISSHA, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of MEMS sensor advancements, IoT integration, miniaturization trends, and evolving industry standards for gas detection.

- Market Drivers & Restraints: Evaluation of factors including industrial safety regulations, environmental monitoring needs, and technological advancements versus challenges like high development costs.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, investors, and policymakers regarding market opportunities and challenges.

The report employs rigorous primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-Gas MEMS Gas Sensor Market?

-> Multi-Gas MEMS Gas Sensor Market was valued at 269 million in 2024 and is projected to reach US$ 390 million by 2032, at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Multi-Gas MEMS Gas Sensor Market?

-> Key players include Amphenol, Senseair, smartGAS, Figaro, NISSHA, Veris Industries, Dynament, and Cubic Sensor and Instrument.

What are the key growth drivers?

-> Key growth drivers include increasing industrial safety regulations, demand for environmental monitoring, smart city initiatives, and adoption in HVAC systems.

Which region dominates the market?

-> Asia-Pacific leads in market share due to rapid industrialization, while North America shows strong growth in smart home applications.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with IoT platforms, AI-powered analytics, and development of low-power consumption models.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...