MARKET INSIGHTS

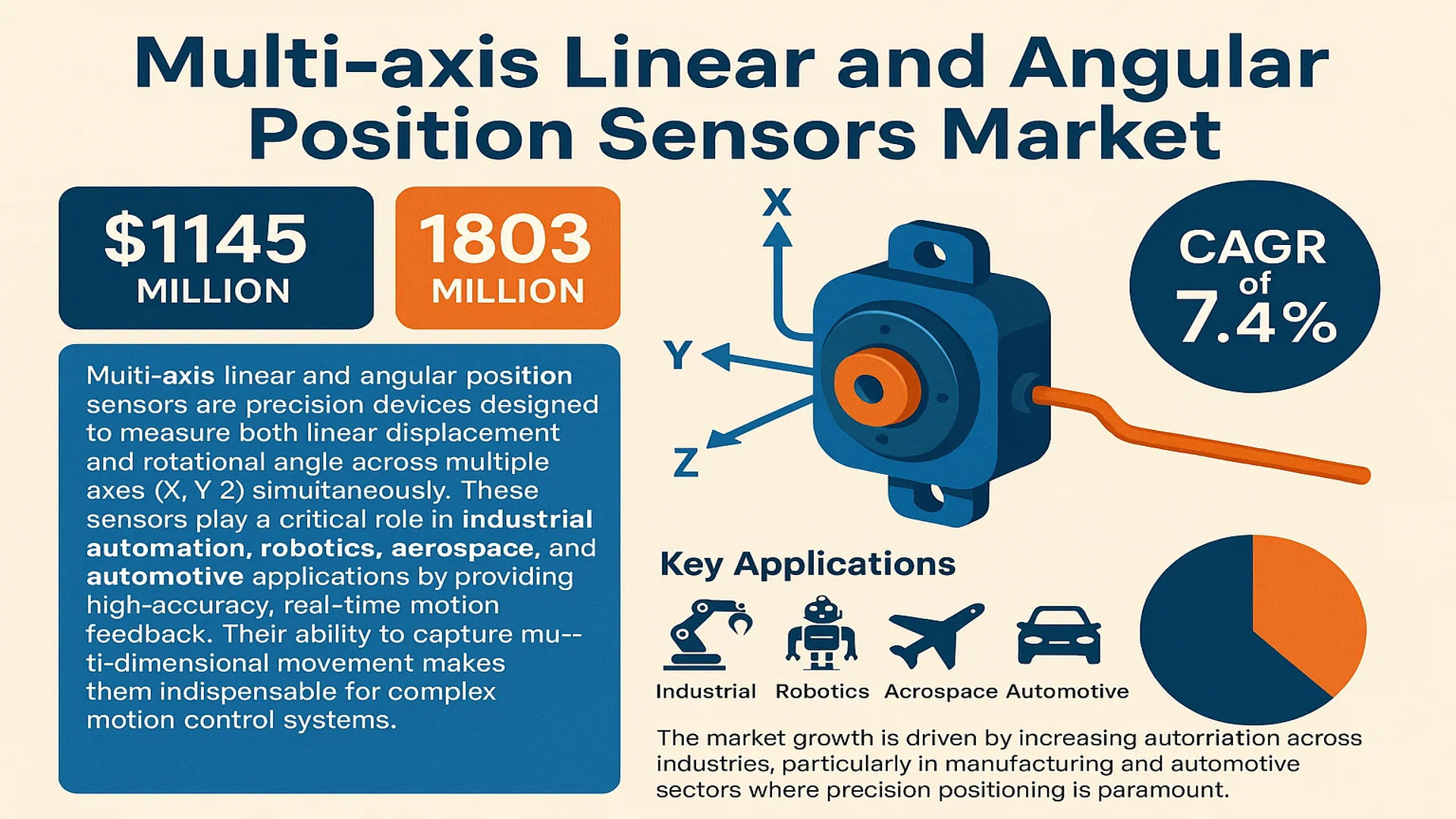

The global Multi-axis Linear and Angular Position Sensors Market was valued at 1145 million in 2024 and is projected to reach US$ 1803 million by 2032, at a CAGR of 7.4% during the forecast period.

Multi-axis linear and angular position sensors are precision devices designed to measure both linear displacement and rotational angle across multiple axes (X, Y, Z) simultaneously. These sensors play a critical role in industrial automation, robotics, aerospace, and automotive applications by providing high-accuracy, real-time motion feedback. Their ability to capture multi-dimensional movement makes them indispensable for complex motion control systems.

The market growth is driven by increasing automation across industries, particularly in manufacturing and automotive sectors where precision positioning is paramount. Furthermore, advancements in sensor technologies, such as improved resolution and reduced form factors, are expanding application possibilities. Key players like Honeywell, Infineon, and TE Connectivity are investing in R&D to develop more compact and energy-efficient sensors, fueling market expansion. The U.S. currently holds the largest market share, while China is emerging as the fastest-growing region due to rapid industrialization.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Industrial Automation Adoption Accelerates Demand for Precision Sensors

The global push toward Industry 4.0 and smart manufacturing is driving unprecedented demand for multi-axis position sensors. These components are becoming indispensable in automated production lines where millimeter-level precision in robotic arm positioning directly impacts product quality. Recent data indicates over 70% of automotive assembly plants now integrate these sensors into their robotic welding stations to maintain sub-millimeter accuracy. The semiconductor manufacturing sector, which requires nanometer-level alignment precision, has seen sensor adoption rates grow by 22% annually since 2021.

Expanding Aerospace and Defense Applications Fuel Market Expansion

Aerospace applications account for nearly 30% of the high-end multi-axis sensor market, driven by strict flight control system requirements. Modern aircraft incorporate over 200 position sensors per unit for functions ranging from flap positioning to landing gear monitoring. The defense sector’s increasing investment in unmanned systems creates additional demand, with military drones requiring compact, shock-resistant sensor solutions. Emerging satellite constellation projects by private space companies are projected to deploy approximately 35,000 multi-axis sensors annually by 2026 for attitude control systems.

Furthermore, the transition to electric vehicles creates new sensor requirements in automotive applications where traditional single-axis solutions prove inadequate for monitoring complex battery management systems. This sector alone is anticipated to generate $280 million in sensor revenue by 2025.

MARKET RESTRAINTS

High Development Costs Limit Entry for Small and Medium Enterprises

The sophisticated nature of multi-axis sensor technology creates significant barriers to market entry. Developing a single multi-axis platform with industry-standard ±0.01° angular accuracy typically requires R&D investments exceeding $2 million. Calibration equipment alone can cost upwards of $500,000, while maintaining sub-micron measurement capabilities demands continuous investment in cleanroom facilities. These financial hurdles concentrate approximately 85% of the market share among ten major players, limiting competition and innovation from smaller firms.

Supply Chain Vulnerabilities Impact Production Consistency

Critical materials for sensor manufacturing, particularly rare-earth magnets and specialized ceramics, remain concentrated in geopolitically sensitive regions. Recent trade policies have caused lead times for neodymium-based components to extend beyond 12 months in some cases. This instability creates production bottlenecks, with Tier 1 manufacturers reporting an average of 18% order fulfillment delays. The medical sector faces particular challenges, where surgical robotics manufacturers require guaranteed six-sigma quality levels that are difficult to maintain with inconsistent material supplies.

MARKET OPPORTUNITIES

Emerging Miniaturization Technologies Open New Application Verticals

Breakthroughs in MEMS (Micro-Electro-Mechanical Systems) fabrication enable sensor packages smaller than 3mm³ while maintaining 16-bit resolution. This allows integration into previously inaccessible applications such as minimally invasive surgical tools and wearable motion capture systems. The medical robotics segment alone presents a $120 million addressable market for these miniaturized solutions. Similarly, consumer electronics manufacturers are evaluating ultra-compact designs for next-generation augmented reality devices requiring precise head tracking.

Advancing Wireless and Energy Harvesting Capabilities Reduce System Complexity

Recent developments in low-power wireless protocols and kinetic energy harvesting eliminate traditional wiring constraints in industrial installations. Wireless multi-axis sensor networks can now operate for years on single power sources while transmitting data at 1kHz sampling rates. This innovation is particularly valuable in hazardous environments like oil refineries, where wired installations pose explosion risks. Early adopters report 40% reductions in installation costs and 60% faster deployment times compared to traditional wired solutions.

MARKET CHALLENGES

Competing Standards Create Integration Complexities

The absence of universal communication protocols forces manufacturers to maintain multiple product variants. Industrial IoT deployments frequently encounter compatibility issues between sensors using IO-Link, Profinet, Ethernet/IP, and other standards. A single automotive plant may require seven different interface configurations, increasing inventory costs by approximately 15%. This fragmentation also complicates predictive maintenance implementations where uniform data formats are essential for machine learning algorithms.

Environmental Tolerance Requirements Escalate Production Costs

Meeting industry demands for extreme environment operation (-40°C to 125°C) while maintaining accuracy specifications requires expensive material adaptations. Aerospace-grade sensors often incorporate platinum components and hermetically sealed enclosures that can triple unit costs compared to commercial equivalents. The renewable energy sector presents similar challenges, where offshore wind turbines require sensors that resist saltwater corrosion while withstanding constant vibration. These specialized applications account for nearly 25% of total R&D expenditures across the industry.

MULTI-AXIS LINEAR AND ANGULAR POSITION SENSORS MARKET TRENDS

Emergence of Smart Manufacturing and Industry 4.0 Drives Demand

The rapid adoption of Industry 4.0 and smart manufacturing technologies is significantly boosting the demand for multi-axis linear and angular position sensors. These sensors play a critical role in enabling precise motion control and real-time feedback in automated systems, which are foundational to modern manufacturing. The shift toward automated production lines, driven by the need for higher efficiency and reduced human intervention, has led to a CAGR of 7.4% in the market, which is projected to grow from $1,145 million in 2024 to $1,803 million by 2032. Robotics and CNC machining applications, in particular, rely on these sensors for accurate multi-dimensional positioning, ensuring seamless operation in high-precision environments. Manufacturers are increasingly integrating advanced sensor technologies to enhance predictive maintenance and reduce operational downtime.

Other Trends

Expansion in Automotive Electrification

The automotive sector’s push toward electrification and autonomous driving has accelerated the adoption of multi-axis position sensors. These sensors are crucial for applications such as throttle control, steering angle detection, and autonomous vehicle positioning. With electric vehicle (EV) production projected to grow exponentially, sensor manufacturers are developing solutions tailored for harsh automotive environments, including high-temperature and vibration-resistant models. Leading automotive OEMs are collaborating with sensor providers to integrate next-generation positioning systems that improve safety and performance.

High-Precision Medical Devices and Robotics Applications

Medical robotics and surgical instruments increasingly rely on multi-axis position sensors for minimally invasive procedures and diagnostic imaging equipment. The growing demand for high-precision medical devices, coupled with advancements in robotic-assisted surgery, has opened new opportunities for sensor manufacturers. For instance, haptic feedback systems in surgical robots leverage these sensors to provide real-time adjustments, improving procedural accuracy. Additionally, diagnostic equipment such as MRI and CT scanners benefits from high-resolution position sensing for precise patient alignment, further driving growth in the segment.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Technological Innovation to Capture Market Share

The global multi-axis linear and angular position sensors market features a moderately competitive landscape with both established multinational corporations and emerging regional players vying for dominance. The market is currently dominated by sensor specialists and diversified industrial conglomerates, with the top five players collectively accounting for approximately 35-40% of the 2024 market revenue. While the competitive intensity remains high, barriers to entry in terms of technological expertise and manufacturing capabilities create a partially protected environment for incumbent players.

Texas Instruments (TI) and Honeywell emerge as market leaders, leveraging their strong positions in semiconductor manufacturing and industrial automation respectively. These companies benefit from vertical integration capabilities and extensive R&D budgets, allowing them to introduce high-precision sensor solutions for mission-critical applications. Honeywell’s recent launch of its HR Series multi-axis sensors demonstrates this technological edge, combining magnetic sensing with advanced signal processing for aerospace applications.

Meanwhile, Infineon Technologies and ams-OSRAM AG are making significant inroads through innovative MEMS-based solutions, particularly in the automotive sector. Their focus on miniaturization and low-power consumption addresses key industry demands for compact sensor arrays in electric vehicles and advanced driver-assistance systems (ADAS). The acquisition of Micronas by TDK Corporation in recent years has further intensified competition in the automotive sensor segment.

Chinese manufacturers like Shanghai Orient-Chip Technology are rapidly gaining traction by offering cost-competitive alternatives, particularly in industrial automation applications. However, these regional players still face challenges in matching the reliability and accuracy specifications required for aerospace and medical applications, where TE Connectivity and Celera Motion maintain strong positions.

List of Key Multi-axis Position Sensor Manufacturers

- Texas Instruments (TI) (U.S.)

- Honeywell International Inc. (U.S.)

- Shanghai Orient-Chip Technology Co., Ltd. (China)

- Infineon Technologies AG (Germany)

- ams-OSRAM AG (Austria)

- Allegro MicroSystems (U.S.)

- Celera Motion (U.K.)

- TE Connectivity (Switzerland)

- Melexis NV (Belgium)

- Sensel Measurement (U.S.)

Segment Analysis:

By Type

Analog Signal Sensor Segment Dominates Due to its Wide Industrial Compatibility

The market is segmented based on type into:

- Analog Signal Sensor

- Digital Signal Sensor

By Application

Industrial Automation Leads the Market Owing to Increasing Smart Manufacturing Adoption

The market is segmented based on application into:

- Industrial Automation

- Aerospace

- Automotive

- Medical

- Architectural

By Technology

Magnetic Technology Segment Shows Strong Growth Potential in High-Precision Applications

The market is segmented based on technology into:

- Optical

- Magnetic

- Capacitive

- Inductive

By End User

Manufacturing Sector Accounts for Significant Adoption Due to Robotics and CNC Machinery Demand

The market is segmented based on end user into:

- Manufacturing

- Energy & Power

- Transportation

- Healthcare

- Defense

Regional Analysis: Multi-axis Linear and Angular Position Sensors Market

Asia-Pacific

Asia-Pacific dominates the global multi-axis linear and angular position sensors market, accounting for the largest revenue share in 2024. This leadership position is driven by China’s booming industrial automation sector and Japan’s advanced robotics industry. The region benefits from concentrated electronics manufacturing hubs, particularly in China, South Korea, and Taiwan, where sensor integration in production lines continues to expand. With major automotive OEMs and contract manufacturers scaling up smart factory initiatives, demand for high-precision positional feedback systems remains robust. Several indigenous manufacturers like Shanghai Orient-Chip Technology Co. are gaining market share by offering cost-effective solutions tailored for regional applications.

North America

The North American market is characterized by technological sophistication and early adoption of Industry 4.0 solutions. The United States leads in aerospace and defense applications, where multi-axis sensors are critical for flight control systems and military robotics. Stringent quality standards from organizations like the FAA and DoD drive demand for high-reliability components from suppliers such as Honeywell and TE Connectivity. Meanwhile, Canada’s growing medical device sector presents opportunities for miniaturized angular position sensors in surgical robotics. Though facing price competition from Asian manufacturers, North American players maintain competitiveness through superior after-sales support and customization capabilities.

Europe

Europe’s market shows steady growth, propelled by Germany’s Industry 4.0 initiatives and widespread automation in automotive manufacturing. The region benefits from strong R&D ecosystems, with firms like Infineon and ams-OSRAM AG developing advanced Hall-effect and magnetoresistive sensor technologies. Strict EU regulations on industrial equipment safety and energy efficiency continue to drive sensor upgrades across factory automation systems. However, the higher cost structure of European manufacturers compared to Asian counterparts has led to increased imports, particularly for standard sensor models used in consumer electronics and general industrial applications.

South America

The South American market remains in a developing phase, with Brazil accounting for the majority of regional demand. Growth is primarily driven by mining equipment modernization and gradual automation in food processing industries. Limited local manufacturing capability results in heavy reliance on imports, with price sensitivity favoring Chinese suppliers. Political and economic instability in key markets like Argentina continues to dampen investment in advanced industrial automation, causing many manufacturers to prioritize basic single-axis sensors over more sophisticated multi-axis solutions.

Middle East & Africa

This region exhibits the lowest market penetration but shows promising growth potential, particularly in oil & gas applications across GCC countries. UAE’s industrial diversification strategy is creating new demand for automation in manufacturing, while South Africa’s mining sector continues to invest in sensor-equipped heavy machinery. The lack of local production facilities and technical expertise results in complete dependence on imports, with European and American brands dominating high-end applications due to their reliability in harsh operating environments.

Report Scope

This market research report provides a comprehensive analysis of the global Multi-axis Linear and Angular Position Sensors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,145 million in 2024 and is projected to reach USD 1,803 million by 2032, growing at a CAGR of 7.4%.

- Segmentation Analysis: Detailed breakdown by product type (Analog Signal Sensor, Digital Signal Sensor), application (Industrial Automation, Aerospace, Automotive, Medical, Architectural), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K.), Asia-Pacific (China, Japan, South Korea), and other key regions.

- Competitive Landscape: Profiles of leading market participants including TI, Honeywell, Infineon, Allegro, and ams-OSRAM AG, covering their product portfolios, market share, and strategic developments.

- Technology Trends: Analysis of emerging innovations in multi-axis sensing technologies, integration with IoT systems, and advancements in precision measurement.

- Market Drivers & Restraints: Evaluation of factors such as increasing automation in manufacturing, growing demand in aerospace applications, alongside challenges like high development costs.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-axis Linear and Angular Position Sensors Market?

->Multi-axis Linear and Angular Position Sensors Market was valued at 1145 million in 2024 and is projected to reach US$ 1803 million by 2032, at a CAGR of 7.4% during the forecast period.

Which key companies operate in this market?

-> Major players include TI, Honeywell, Infineon, Allegro, ams-OSRAM AG, Shanghai Orient-Chip Technology, and Sensel Measurement.

What are the key growth drivers?

-> Growth is driven by increasing industrial automation, demand in aerospace applications, and advancements in robotics.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America currently holds significant market share.

What are the emerging trends?

-> Key trends include integration with Industry 4.0 systems, development of miniaturized sensors, and increased adoption in medical robotics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...