MARKET INSIGHTS

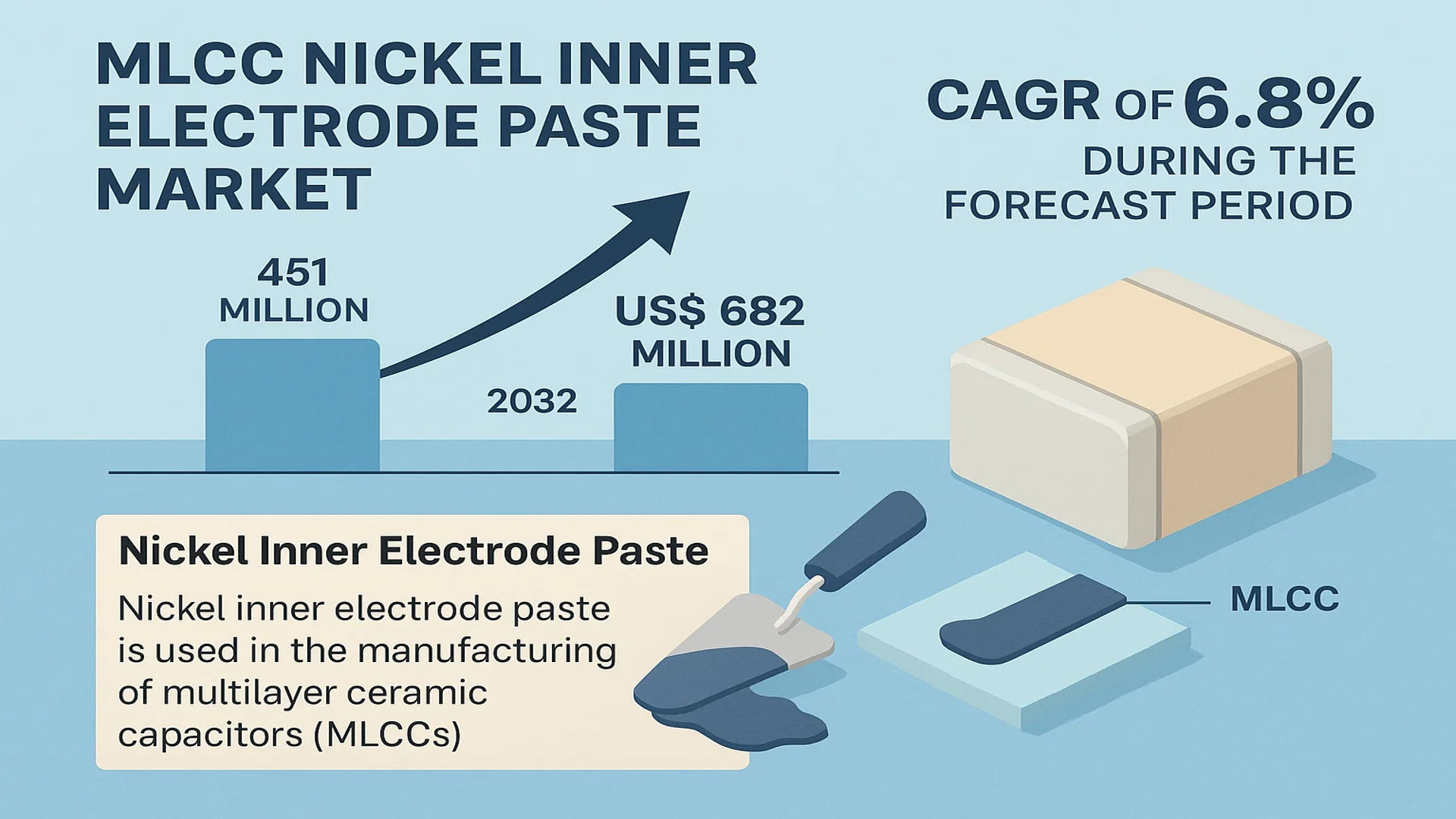

The global MLCC Nickel Inner Electrode Paste Market was valued at 451 million in 2024 and is projected to reach US$ 682 million by 2032, at a CAGR of 6.8% during the forecast period.

Nickel inner electrode paste is a critical raw material used in the manufacturing of Multilayer Ceramic Capacitors (MLCCs). This conductive paste is screen-printed onto ceramic dielectric layers to form the internal electrodes of the capacitor. The shift from precious metal-based pastes (using silver and palladium) to nickel-based formulations has been a significant industry trend because nickel offers a substantial cost advantage, being only about 5% the cost of a conventional Pd30-Ag70 electrode, while also providing superior electrochemical stability, higher mechanical strength, and better conductivity.

The market is experiencing steady growth, primarily driven by the relentless miniaturization and performance demands of the global electronics industry. The expansion is further fueled by the rapid adoption of new energy vehicles, which require a higher volume of advanced, high-capacity MLCCs, and the ongoing rollout of 5G infrastructure. The Chinese market exemplifies this growth, reaching a size of USD 196 million (1.42 billion yuan) in 2024. While consumer electronics remains the largest application segment, accounting for approximately 40% of demand, the automotive sector is poised to be the fastest-growing segment. Key global players shaping the market include Murata, Dowton Electronic Materials, and Daiken Chemical, among others.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Consumer Electronics and 5G Infrastructure to Accelerate Market Growth

The global consumer electronics sector continues to demonstrate robust growth, with smartphone shipments exceeding 1.4 billion units annually and the 5G smartphone penetration rate surpassing 60% in key markets. MLCCs serve as critical components in these devices, with a single 5G smartphone containing approximately 1,200-1,500 MLCC units compared to 800-900 units in 4G devices. This represents a 40-50% increase in MLCC content per device, directly driving demand for nickel inner electrode paste. The transition to 5G networks requires higher frequency operations and improved signal integrity, which nickel-based MLCCs provide through their superior electrical properties and reliability. The ongoing miniaturization trend in electronics further necessitates advanced MLCC formulations, positioning nickel electrode paste as an essential material for next-generation electronic devices.

Electric Vehicle Revolution Creating Substantial Demand for High-Performance MLCCs

The automotive industry’s rapid shift toward electrification represents a significant growth driver for the MLCC nickel inner electrode paste market. Electric vehicles typically incorporate 8,000-10,000 MLCC units per vehicle, compared to 3,000-4,000 units in conventional internal combustion engine vehicles. This represents a 150-200% increase in MLCC content, primarily driven by advanced driver assistance systems, battery management systems, and power electronics. The global electric vehicle market is projected to grow at a compound annual growth rate of 25-30%, with annual sales expected to reach 40 million units by 2030. Nickel electrode MLCCs are particularly favored in automotive applications due to their excellent thermal stability, reliability under harsh conditions, and cost-effectiveness compared to precious metal alternatives. Automotive-grade MLCCs require stringent performance standards, and nickel-based formulations consistently meet these requirements while providing significant cost savings.

Cost Efficiency and Performance Advantages Over Precious Metal Alternatives

The economic benefits of nickel inner electrode paste continue to drive widespread adoption across the electronics manufacturing sector. Nickel-based electrodes cost approximately 5% of conventional palladium-silver electrodes, representing potential savings of 20-30% on overall MLCC production costs. This cost advantage becomes particularly significant given that MLCCs account for 20-25% of total electronic component costs in many devices. Beyond cost considerations, nickel electrodes demonstrate superior technical performance including 30-40% higher mechanical strength, improved resistance to electromigration, and enhanced thermal stability up to 125°C operating temperatures. These performance characteristics enable manufacturers to produce more reliable components while maintaining competitive pricing. The ongoing volatility in precious metal markets, where palladium prices have experienced fluctuations of 40-60% annually, further strengthens the case for nickel-based alternatives as a more stable and predictable material choice.

MARKET RESTRAINTS

Technical Complexities in Manufacturing and Quality Consistency Challenges

The production of high-quality nickel inner electrode paste involves sophisticated manufacturing processes that present significant technical challenges. Achieving consistent particle size distribution in the 200-400 nanometer range requires precise control of milling and classification processes, with even minor variations potentially affecting final MLCC performance. The paste formulation must maintain optimal viscosity, solid content, and rheological properties throughout the manufacturing process, which becomes increasingly challenging as particle sizes decrease. Manufacturers face difficulties in achieving batch-to-batch consistency, with quality control parameters requiring deviations of less than 3% for critical characteristics. These technical requirements necessitate substantial investment in advanced manufacturing equipment and rigorous quality control systems, creating barriers for new market entrants and limiting production scalability for existing manufacturers.

Raw Material Price Volatility and Supply Chain Constraints

The nickel inner electrode paste market faces significant pressure from raw material price fluctuations and supply chain vulnerabilities. Nickel prices have experienced volatility of 25-40% annually due to factors including mining output variations, geopolitical tensions, and changing demand patterns from other industries. This volatility creates pricing uncertainty for paste manufacturers and their customers, complicating long-term planning and contract negotiations. Additionally, the supply chain for high-purity nickel powders faces constraints, with limited global production capacity meeting stringent electronic-grade specifications. The concentration of nickel mining and processing in specific geographic regions creates potential supply risks, particularly when considering that over 60% of global nickel production originates from countries experiencing political or economic instability. These factors combine to create a challenging environment for cost management and supply security.

Stringent Technical Specifications and Performance Requirements

End-user industries continue to demand increasingly stringent performance specifications for MLCC components, creating challenges for nickel inner electrode paste manufacturers. Automotive applications require components capable of operating at temperatures up to 150°C with failure rates below 0.1 parts per million, while aerospace and defense applications demand even higher reliability standards. Meeting these requirements necessitates continuous improvement in paste formulations, particularly regarding thermal stability, aging characteristics, and mechanical strength. The transition to smaller form factors and higher capacitance values requires pastes with improved printing characteristics and finer feature resolution. These technical challenges require substantial research and development investment, with leading manufacturers allocating 5-8% of annual revenue to R&D activities. The pace of technological change in end-use applications means that paste formulations must continuously evolve, creating ongoing pressure on manufacturers to innovate while maintaining production efficiency and cost competitiveness.

MARKET CHALLENGES

Intense Global Competition and Price Pressure from Established Manufacturers

The MLCC nickel inner electrode paste market faces intense competitive pressure from established global players with significant manufacturing scale and technological expertise. The top five manufacturers control over 70% of global market share, creating challenges for smaller participants seeking to gain market position. These leading companies benefit from economies of scale, established customer relationships, and extensive intellectual property portfolios covering key manufacturing processes and formulations. Price competition remains fierce, with manufacturers facing pressure to reduce costs while maintaining quality standards. The industry has experienced average selling price declines of 3-5% annually despite increasing technical requirements and raw material cost pressures. This competitive environment creates challenges for profitability and investment in future innovation, particularly for companies without significant scale or technological differentiation.

Other Challenges

Technological Obsolescence Risk

Rapid advancements in electronic component technology create constant pressure for paste manufacturers to innovate and adapt. Emerging alternative technologies, including conductive polymer formulations and advanced ceramic compositions, potentially threaten the position of traditional nickel-based pastes. The development of new MLCC architectures and manufacturing processes may require fundamentally different paste formulations, necessitating continuous research and development investment. Manufacturers must balance the need for innovation with the requirement to maintain compatibility with existing production infrastructure and customer requirements.

Environmental Regulations and Sustainability Requirements

Increasing environmental regulations and customer sustainability requirements present growing challenges for paste manufacturers. Regulations governing nickel usage, waste disposal, and manufacturing emissions continue to evolve, requiring ongoing compliance efforts and potential process modifications. Customers increasingly demand environmentally responsible manufacturing practices and materials, with some implementing strict sustainability criteria for supplier selection. Meeting these requirements often involves additional costs for pollution control equipment, waste treatment systems, and certification processes, creating pressure on profitability while requiring specialized expertise in environmental compliance.

MARKET OPPORTUNITIES

Expansion into Emerging Applications and Next-Generation Electronic Devices

The ongoing development of advanced electronic systems creates significant growth opportunities for nickel inner electrode paste manufacturers. Emerging applications in 6G communication systems, advanced automotive electronics, and industrial Internet of Things devices require MLCCs with enhanced performance characteristics that nickel-based formulations can effectively provide. The transition to higher frequency communications above 100 GHz necessitates components with improved high-frequency performance, an area where nickel electrodes demonstrate particular advantages. Additionally, the growing adoption of wide-bandgap semiconductors in power electronics creates demand for MLCCs capable of operating at higher temperatures and voltages, presenting opportunities for advanced nickel paste formulations. These emerging applications typically command premium pricing and provide opportunities for manufacturers to differentiate through technical innovation and specialized product development.

Geographical Market Expansion and Supply Chain Diversification

Significant opportunities exist for expansion into developing regional markets and diversification of global supply chains. The electronics manufacturing industry continues to expand beyond traditional centers in East Asia, with growing production capacity in Southeast Asia, Eastern Europe, and Latin America. This geographical diversification creates opportunities for paste manufacturers to establish local production facilities and develop relationships with new customer bases. Additionally, ongoing efforts to diversify supply chains and reduce geographical concentration risks provide opportunities for manufacturers with multiple production locations or those establishing new facilities in underserved regions. The increasing emphasis on supply chain resilience and regional self-sufficiency in critical electronic components further supports these expansion opportunities, particularly for companies able to demonstrate reliable supply and technical capability across multiple geographical markets.

Advanced Material Development and Performance Enhancement Initiatives

Research and development efforts focused on advanced material formulations present substantial opportunities for market growth and differentiation. Developments in nanoparticle technology, surface treatment methods, and additive formulations enable creation of nickel pastes with enhanced electrical properties, improved processing characteristics, and reduced environmental impact. Opportunities exist for manufacturers developing pastes with lower sintering temperatures, improved adhesion properties, or enhanced reliability under extreme operating conditions. Additionally, the integration of digital manufacturing technologies, including advanced process control systems and real-time quality monitoring, enables production of more consistent and higher-performance pastes. These technological advancements provide opportunities for manufacturers to capture premium market segments, develop proprietary formulations, and establish stronger competitive positions through technical differentiation and performance advantages.

MLCC NICKEL INNER ELECTRODE PASTE MARKET TRENDS

Advancements in Automotive Electronics to Emerge as a Trend in the Market

The rapid electrification of vehicles is fundamentally reshaping the demand landscape for MLCCs and, consequently, for nickel inner electrode paste. While consumer electronics historically dominated consumption, accounting for approximately 40% of the market in 2024, the automotive sector is now the primary growth engine. This shift is driven by the increasing electronic content per vehicle, particularly in New Energy Vehicles (NEVs) which require an estimated 8,000 to 10,000 MLCCs per unit, compared to just 3,000 in conventional internal combustion engine vehicles. This surge necessitates high-reliability, high-capacitance MLCCs that can withstand harsh operating conditions, a niche perfectly served by nickel electrode technology due to its superior thermal stability and electrochemical performance. The transition towards Advanced Driver-Assistance Systems (ADAS), in-vehicle infotainment, and comprehensive vehicle electrification is creating sustained, long-term demand for these specialized pastes, pushing manufacturers to innovate in particle size uniformity and sintering behavior to meet stringent automotive-grade qualifications.

Other Trends

Miniaturization and High-Capacitance Demands

The relentless drive towards smaller, more powerful electronic devices is compelling the MLCC industry to pack higher capacitance into increasingly diminutive form factors. This trend directly influences the nickel inner electrode paste market, as achieving this requires ultra-fine, highly uniform nickel powders. Pastes utilizing nickel particles at 200nm and below are seeing accelerated adoption to facilitate the production of MLCCs with more layers and thinner dielectric coatings. This technological arms race is evident in the rising R&D investments focused on improving the dispersibility and stability of these nanoscale pastes to prevent agglomeration during the tape-casting process. The ability to consistently produce pastes that enable the fabrication of over 1,000 layers in a single capacitor is becoming a key differentiator for suppliers, as this capability is critical for next-generation 5G infrastructure, high-performance computing, and premium consumer electronics.

Supply Chain Localization and Regional Production

Geopolitical tensions and a heightened focus on supply chain resilience are accelerating the trend of regional production and localization, particularly outside of traditional manufacturing hubs. This is most pronounced in China, where the domestic market for nickel electrode paste reached an estimated 1.42 billion yuan in 2024, supported by strong governmental policies aimed at self-sufficiency in key electronic components. Major Chinese manufacturers, including Zhaorong and Sinoceramic Materials, have significantly expanded their production capacities to capture this growing domestic demand and reduce reliance on imports. This regionalization is not without its challenges; it requires substantial capital investment and the transfer of sophisticated metallurgical and ceramic processing know-how. However, it also fosters intense competition and innovation, leading to improvements in cost efficiency and product performance as companies vie for market share in a industry where the top five players controlled over 73% of the global market in 2024.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Expansion to Secure Market Position

The global MLCC Nickel Inner Electrode Paste market exhibits a semi-consolidated structure, characterized by the presence of established multinational corporations, specialized medium-sized enterprises, and emerging regional players. Murata Manufacturing Co., Ltd. stands as a dominant force, leveraging its vertically integrated business model and extensive R&D capabilities. The company’s leadership is reinforced by its significant market share in both MLCC production and the advanced materials required for their manufacture, including nickel electrode paste. Its global manufacturing footprint and longstanding relationships with major electronics OEMs provide a formidable competitive advantage.

Shoei Chemical Inc. and Daiken Chemical Co., Ltd. are also pivotal players, holding substantial market shares. Their growth is largely driven by their specialization in high-purity metal pastes and deep-rooted presence within the Asian electronics supply chain. These companies have consistently invested in developing pastes with finer nickel particle sizes, such as 200nm and 300nm variants, which are critical for manufacturing next-generation, miniaturized MLCCs. Their expertise in powder metallurgy and paste formulation is a key differentiator.

Furthermore, strategic initiatives such as capacity expansions, technological partnerships with MLCC manufacturers, and new product launches aimed at enhancing conductivity and sintering properties are expected to be primary growth drivers for these leading firms over the forecast period.

Meanwhile, Chinese manufacturers like Shandong Sinocera Functional Material Co., Ltd. and Fenghua Advanced Technology Holding Co., Ltd. are aggressively strengthening their positions. This is achieved through significant capital investments in domestic production facilities, aimed at reducing reliance on imports and catering to the booming local electronics and electric vehicle industries. Their competitive strategy often revolves around cost-efficiency and rapid responsiveness to domestic market demands, posing an increasing challenge to established international suppliers.

List of Key MLCC Nickel Inner Electrode Paste Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- Shoei Chemical Inc. (Japan)

- Daiken Chemical Co., Ltd. (Japan)

- Dowton Electronic Materials Co., Ltd. (China)

- Shandong Sinocera Functional Material Co., Ltd. (China)

- Fenghua Advanced Technology Holding Co., Ltd. (China)

- Dalian Overseas Huasheng Electronic Materials Co., Ltd. (China)

- FM Co., Ltd. (South Korea)

- ChangDi New Material Co., Ltd. (China)

- Hunan Zhongrui Xincai Co., Ltd. (China)

Segment Analysis:

By Type

200nm Particle Size Segment Dominates Due to Superior Performance in High-Frequency Applications

The market is segmented based on particle size into:

- 200nm

- 300nm

- 400nm

- Others

By Application

Consumer Electronics Segment Leads Due to Pervasive Use in Smartphones and Portable Devices

The market is segmented based on application into:

- Consumer Electronics

- Automotive

- Industrial Machinery

- Defense

- Other

By End User

MLCC Manufacturers Segment is the Core End User Driving Market Dynamics

The market is segmented based on end user into:

- MLCC Manufacturers

- Electronic Component Distributors

- Research and Development Institutions

Regional Analysis: MLCC Nickel Inner Electrode Paste Market

Asia-Pacific

The Asia-Pacific region dominates the global MLCC Nickel Inner Electrode Paste market, accounting for over 85% of global production and consumption in 2024. This dominance is primarily driven by China, which alone represents approximately 65% of the regional market with a value of $293 million in 2024. The region’s leadership stems from its position as the global electronics manufacturing hub, with major MLCC producers like Murata, Samsung Electro-Mechanics, and TDK maintaining significant production facilities across China, Japan, and South Korea. The rapid expansion of 5G infrastructure, coupled with robust consumer electronics demand and the accelerating adoption of electric vehicles, particularly in China and India, continues to drive market growth. However, the region faces challenges including raw material price volatility and increasing environmental regulations that are pushing manufacturers toward more sustainable production processes.

North America

North America represents a technologically advanced but smaller segment of the MLCC Nickel Inner Electrode Paste market, valued at approximately $38 million in 2024. The region’s market is characterized by high-value, specialized applications in aerospace, defense, and automotive electronics, particularly in the United States. Strict quality standards and certification requirements govern the market, with manufacturers focusing on high-reliability pastes for critical applications. The recent CHIPS Act and infrastructure investments are stimulating domestic electronics manufacturing, potentially creating new opportunities for local paste suppliers. However, the region’s higher production costs and limited manufacturing base compared to Asia present ongoing challenges for market expansion.

Europe

Europe’s MLCC Nickel Inner Electrode Paste market, valued at around $32 million in 2024, is driven by stringent environmental regulations and high-performance automotive applications. The EU’s End-of-Life Vehicles Directive and REACH regulations have pushed manufacturers toward developing more environmentally friendly paste formulations with reduced VOC emissions. Germany remains the regional leader, supported by its strong automotive electronics sector and presence of major automotive manufacturers requiring high-reliability MLCCs. The region’s focus on electric vehicle development and industrial automation continues to drive demand for specialized nickel electrode pastes, though competition from Asian imports and high production costs remain significant market constraints.

South America

South America represents an emerging market for MLCC Nickel Inner Electrode Paste, with Brazil accounting for the majority of regional demand. The market remains relatively underdeveloped, valued at approximately $8 million in 2024, primarily serving consumer electronics and industrial applications. Economic volatility and limited local electronics manufacturing capacity have constrained market growth, with most paste requirements being met through imports. However, gradual industrialization and increasing smartphone penetration rates are creating slow but steady demand growth. The region faces challenges including infrastructure limitations and currency fluctuations affecting import-dependent supply chains.

Middle East & Africa

The Middle East & Africa region presents the smallest market segment for MLCC Nickel Inner Electrode Paste, estimated at $5 million in 2024. Market development is primarily concentrated in countries with growing electronics manufacturing sectors, such as Israel, Turkey, and South Africa. The region’s market is characterized by import dependency and limited local production capabilities. While growing mobile phone penetration and gradual industrial development are creating baseline demand, the market faces significant challenges including limited technical expertise, infrastructure constraints, and political instability in certain areas. Long-term growth potential exists as digital transformation initiatives gain momentum across the region.

Report Scope

This market research report provides a comprehensive analysis of the global MLCC Nickel Inner Electrode Paste market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global MLCC Nickel Inner Electrode Paste Market?

-> MLCC Nickel Inner Electrode Paste Market was valued at 451 million in 2024 and is projected to reach US$ 682 million by 2032, at a CAGR of 6.8% during the forecast period.

Which key companies operate in Global MLCC Nickel Inner Electrode Paste Market?

-> Key players include Daiken Chemical, Dowton Electronic Materials, FM Co., Ltd., Shandong Sinocera, Fenghua Advanced, Dalian Overseas Huasheng, ChangDi New Material, Hunan Zhongrui Xincai, Murata, and Shoei Chemical, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of 5G infrastructure, rising demand for electric vehicles, growth in consumer electronics, and cost advantages of nickel over precious metal electrodes.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China accounting for the largest share of both production and consumption globally.

What are the emerging trends?

-> Emerging trends include development of finer particle pastes (below 200nm), increased automation in manufacturing processes, and growing adoption in automotive safety systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...