MicroLED Optoelectronics Market Insights

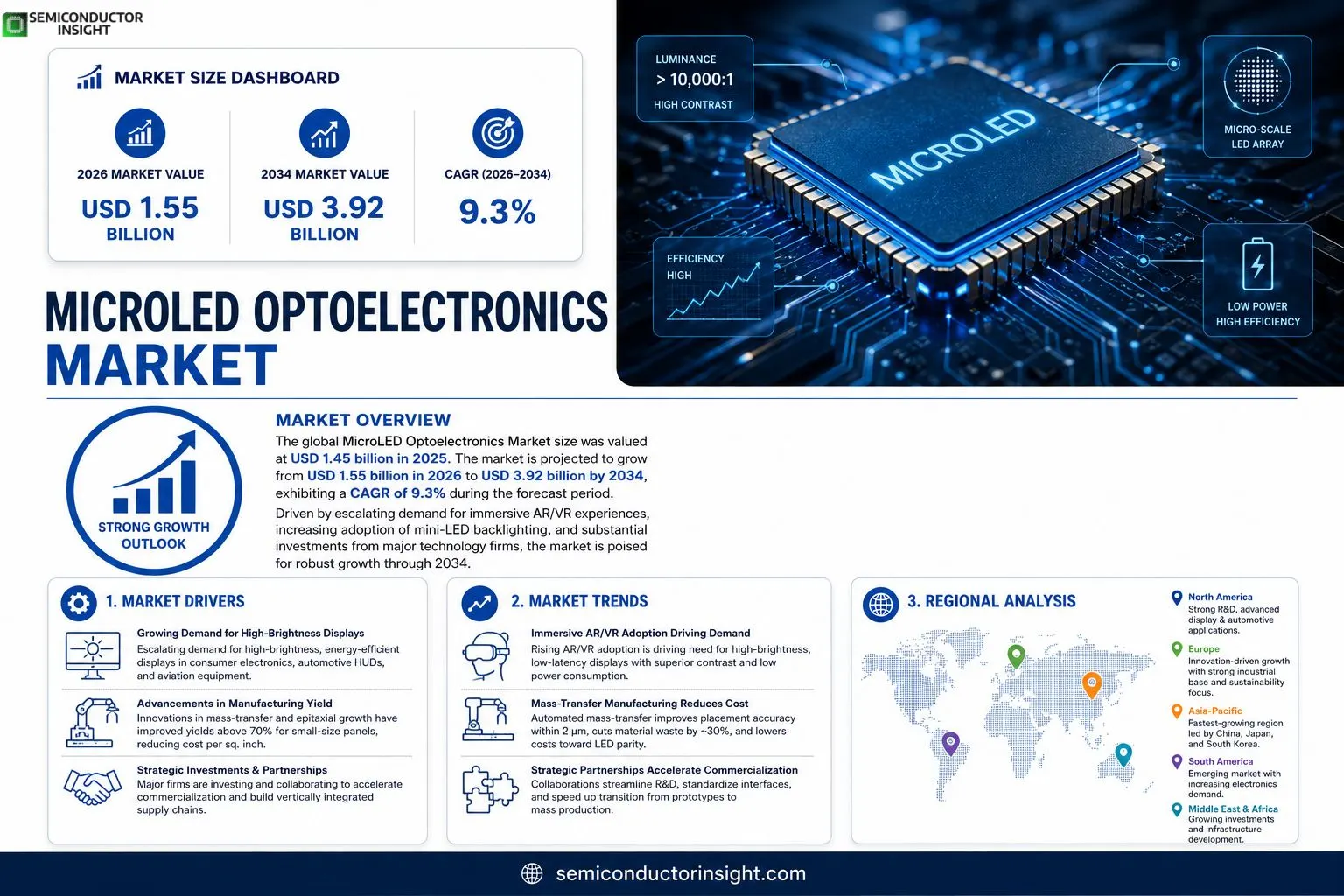

The global MicroLED Optoelectronics Market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.92 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

MicroLED optoelectronics encompass high‑brightness micro‑scale light‑emitting diodes integrated into display panels, illumination systems, and sensing devices. These components combine semiconductor physics with optical engineering to deliver superior contrast ratios, low power consumption, and extended lifespans compared with traditional LEDs or OLEDs.The market is experiencing rapid growth due to several factors, including escalating demand for immersive AR/VR experiences, increasing adoption of mini‑led backlighting in consumer electronics, and substantial investments from major technology firms seeking next‑generation display solutions. Furthermore, advancements in mass‑transfer manufacturing techniques are reducing production costs, while strategic partnerships,such as Samsung’s collaboration with SiTime on micro‑laser integration announced in March 2024 are accelerating commercialization pathways.

MARKET DRIVERS

Growing Demand for High‑Brightness Displays

MicroLED Optoelectronics Market is being propelled by an escalating demand for high‑brightness, energy‑efficient displays in consumer electronics, automotive heads‑up displays, and aviation equipment. Manufacturers are seeking pixel‑level control, which MicroLED technology uniquely delivers.

Advancements in Manufacturing Yield

Recent innovations in mass‑transfer equipment and epitaxial growth have lifted production yields from single‑digit percentages to above 70% for small‑size panels, reducing cost per square inch and making commercial rollout viable.

➤ Industry analysts forecast that MicroLED Optoelectronics Market could surpass $5 billion by 2030, driven largely by automotive and AR/VR adoption.

Additionally, strategic investments by leading semiconductor firms are creating vertically integrated supply chains, further accelerating market momentum and fostering ecosystem stability.

MARKET CHALLENGES

High Capital Expenditure for Production Facilities

Establishing a dedicated MicroLED fab requires multi‑hundred‑million‑dollar outlays for cleanroom infrastructure, substrate handling, and yield‑optimization tools, creating a financial barrier for new entrants.

Other Challenges

Yield Consistency at Large Volumes

Even with improved transfer techniques, maintaining uniformity across large‑area panels remains difficult, leading to higher reject rates and unpredictable pricing.

MARKET RESTRAINTS

Limited Supply of High‑Quality Substrates

The scarcity of defect‑free sapphire and silicon carbide substrates constrains scaling, as each wafer must meet stringent optical and thermal specifications for MicroLED devices.

Complex Integration with Existing Backplane Technologies

Integrating MicroLED arrays with CMOS backplanes demands precise alignment and sophisticated driver circuitry, increasing design complexity and time‑to‑market for OEMs.

MARKET OPPORTUNITIES

Expansion into Augmented Reality (AR) Headsets

AR headsets require lightweight, low‑power, high‑resolution displays; MicroLED’s superior luminance and contrast position it as a prime candidate, opening a multi‑billion‑dollar opportunity within MicroLED Optoelectronics Market.

Automotive HUD and Instrument Cluster Growth

Automakers are adopting MicroLED for heads‑up displays and digital instrument clusters to meet safety regulations and consumer expectations for vivid graphics, driving sustained demand.

MicroLED Optoelectronics Market Trends

Immersive AR/VR Adoption Driving Demand

The rapid expansion of augmented and virtual reality platforms has created a pressing need for displays that combine high brightness, low latency, and precise color rendering. In response, MicroLED Optoelectronics Market is witnessing a shift toward integrating micro‑scale LEDs directly into AR headset optics and VR panoramic panels. These components deliver contrast ratios that exceed 10,000:1 while consuming less power than conventional OLED stacks, thereby extending battery life in wearable devices. Leading manufacturers are re‑engineering driver ICs to match the fast switching speeds of micro‑LED arrays, enabling smoother motion tracking and reducing motion‑sickness complaints among end‑users. This trend is reinforced by strategic investments from consumer‑electronics giants seeking to differentiate premium head‑set offerings.

Other Trends

Mass‑Transfer Manufacturing Reduces Cost

Advances in mass‑transfer technology have emerged as a pivotal catalyst for cost containment in MicroLED Optoelectronics Market. Automated pick‑and‑place systems now achieve placement accuracies within 2 µm, allowing manufacturers to scale production volumes without compromising yield. The process leverages wafer‑level bonding and laser‑driven release mechanisms, which collectively cut material waste by roughly 30 percent compared with earlier manual techniques. As a result, price points for micro‑LED modules are approaching parity with traditional LED components, making the technology viable for mid‑range consumer products such as smartphones and automotive dashboards. Industry observers note that this manufacturing momentum is shortening the commercialization timeline for new display form factors.

Strategic Partnerships Accelerate Commercialization

Collaborative agreements between semiconductor firms and optical‑engine companies are reshaping the development pipeline for micro‑LED‑based solutions. Notable partnerships, such as the recent alliance that combines high‑precision laser integration with established micro‑LED foundries, are streamlining the transition from prototype to mass production. These joint ventures pool R&D resources and share intellectual property, reducing time‑to‑market for next‑generation lighting and sensing modules. Moreover, cross‑industry collaborations are fostering standardization of interface protocols, which simplifies integration into existing display architectures. This cooperative environment is expected to broaden the application scope of micro‑LED technology across sectors ranging from automotive illumination to medical imaging, thereby reinforcing the overall growth trajectory of the market.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Landscape of the Global MicroLED Optoelectronics Market

MicroLED Optoelectronics Market is currently dominated by a handful of vertically integrated technology groups that control both epitaxial wafer supply and advanced mass‑transfer assembly. Samsung Electronics leads the segment with its SiTime‑backed micro‑laser integration platform and substantial R&D spend on high‑resolution display modules for AR/VR headsets. Sony, leveraging its PictureWave technology, occupies a strong position in professional‑grade large‑format displays, while Taiwan‑based AU Optronics and TCL focus on mini‑LED backlighting solutions that serve as a stepping stone to full‑scale MicroLED adoption. These incumbents benefit from deep semiconductor manufacturing expertise, extensive IP portfolios, and supply‑chain relationships that enable rapid scaling of production capacities to meet the projected CAGR of 9.3%.Beyond the headline players, a vibrant ecosystem of niche innovators is accelerating differentiation across applications. LuxVue (now part of Rohm Semiconductor) supplies high‑efficiency micro‑LED chips for wearable optics, whereas Epistar and Himax specialize in epitaxial growth and driver IC integration for automotive lighting. Plessey (a Siemens spin‑off) and Leyard focus on micro‑LED module design for signage and immersive exhibition environments. Emerging entrants such as Foxconn’s Sharp subsidiary and AMS‑Osram are investing in hybrid silicon‑photonic approaches to reduce transfer yields, while smaller firms like Skyworks and Lumileds explore novel phosphor‑free illumination concepts. This layered competitive structure creates multiple pathways for market entrants to capture specialized segments while the larger players consolidate volume‑driven opportunities.

List of Key MicroLED Optoelectronics Companies Profiled

- Samsung Electronics

- Sony Corporation

- AU Optronics

- TCL Technology

- LuxVue (Rohm Semiconductor)

- Epistar Corporation

- Himax Technologies

- Plessey

- Leyard Technologies

- AMS‑Osram

- Foxconn (Sharp)

- Skyworks Solutions

- Lumileds

- Apple Inc. (through strategic MicroLED acquisitions)

- MicroLED Labs

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Active Matrix MicroLEDs drive the market with precise pixel‑level control, high refresh capabilities, and superior brightness uniformity. Their integration enables advanced visual experiences and supports innovative form factors across devices. Industry participants prioritize these solutions for scalability and the potential to reshape visual performance standards. |

| By Application |

|

Display Panels represent the core application, delivering unprecedented contrast and power efficiency for next‑generation screens. Their adoption fuels new product categories such as foldable and transparent displays. The technology also underpins immersive AR/VR experiences, while automotive lighting benefits from enhanced durability and design flexibility. |

| By End User |

|

Consumer Electronics lead adoption as manufacturers seek brighter, thinner screens with lower power draw. Devices ranging from smartphones to wearables benefit from the technology’s vivid color reproduction. Automotive stakeholders value the robustness and design versatility for interior ambiance lighting, while industrial users appreciate the long lifespan for critical instrumentation. |

| By Manufacturing Technology |

|

Mass Transfer Process emerges as the leading technology, offering efficient assembly of millions of micro‑LEDs onto substrates. Its scalability addresses volume production challenges, while maintaining high yield and performance consistency. Complementary approaches such as wafer‑level integration provide pathways for higher precision, and hybrid bonding introduces flexibility for heterogeneous device stacks. |

| By End‑Use Industry |

|

Smart Home Devices stand out as a rapid growth segment, where ultra‑compact, low‑power microLEDs enable vibrant displays for control panels and ambient lighting solutions. In healthcare, the technology improves imaging clarity and durability of diagnostic tools. Aerospace applications benefit from lightweight, high‑reliability lighting that withstands extreme environments. |

Regional Analysis: North America

United States

The US market is witnessing a shift towards MicroLED for superior display quality, energy efficiency, and design flexibility. This trend is particularly pronounced in the premium segment of televisions and high-end mobile devices. Continuous innovation in MicroLED fabrication techniques is further driving down costs and enhancing performance.

The automotive industry represents a significant growth area for MicroLED optoelectronics in North America. The demand for advanced in-vehicle displays, including instrument clusters, infotainment systems, and rear-seat displays, is escalating. MicroLED’s advantages in terms of brightness, contrast, and viewing angles make it well-suited for demanding automotive environments.

Significant investments in research and development are fueling the advancement of MicroLED optoelectronics in the US. Government initiatives and private sector funding are supporting innovation in materials science, device fabrication, and system integration. This strong R&D ecosystem is expected to accelerate the commercialization of MicroLED technologies.

The North American MicroLED optoelectronics market is characterized by a mix of established display manufacturers and emerging MicroLED specialists. Key players are focused on developing proprietary technologies and establishing strategic partnerships to gain a competitive edge in this rapidly evolving market.

Europe

The European market for MicroLED optoelectronics is gaining traction, driven by a strong emphasis on innovation and sustainability. Particularly in countries like Germany, France, and the UK, a growing demand for energy-efficient and high-quality displays is creating opportunities. The automotive sector in Europe is also actively exploring the potential of MicroLED for advanced in-vehicle applications. Government support for research and development, coupled with a robust industrial base, positions Europe as a significant emerging hub for MicroLED technology.

Asia-Pacific

Asia-Pacific, particularly China, Japan, and South Korea, represents a major and rapidly expanding market for MicroLED optoelectronics. China’s significant investments in display technology and consumer electronics manufacturing are driving substantial demand. South Korea remains a leader in display innovation and has a well-established ecosystem for MicroLED development. The region’s strong manufacturing capabilities and proximity to key supply chains are further facilitating the growth of the MicroLED market.

South America

MicroLED Optoelectronics Market in South America is in its nascent stages but holds potential for future growth. Increasing disposable incomes and a growing consumer electronics market are expected to drive demand for advanced displays. The automotive sector in Brazil and other South American countries could also represent a future opportunity for MicroLED adoption.

Middle East & Africa

The Middle East & Africa region presents a smaller but potentially growing market for MicroLED optoelectronics. Increasing investments in infrastructure and consumer electronics, along with rising disposable incomes in certain countries, are expected to drive demand. The automotive sector in the UAE and Saudi Arabia could offer future opportunities for MicroLED applications.

Report Scope

This market research report provides a comprehensive analysis of the MicroLED Optoelectronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MicroLED Optoelectronics Market?

-> MicroLED Optoelectronics Market was valued at USD 1.45 billion in 2025 and is expected to reach USD 3.92 billion by 2034.

Which key companies operate in MicroLED Optoelectronics Market?

-> Key players include Samsung, SiTime, and other leading semiconductor manufacturers, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for immersive AR/VR experiences, increasing adoption of mini‑LED backlighting, and substantial investments from major technology firms.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include advancements in mass‑transfer manufacturing techniques and strategic partnerships for micro‑laser integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...