MARKET INSIGHTS

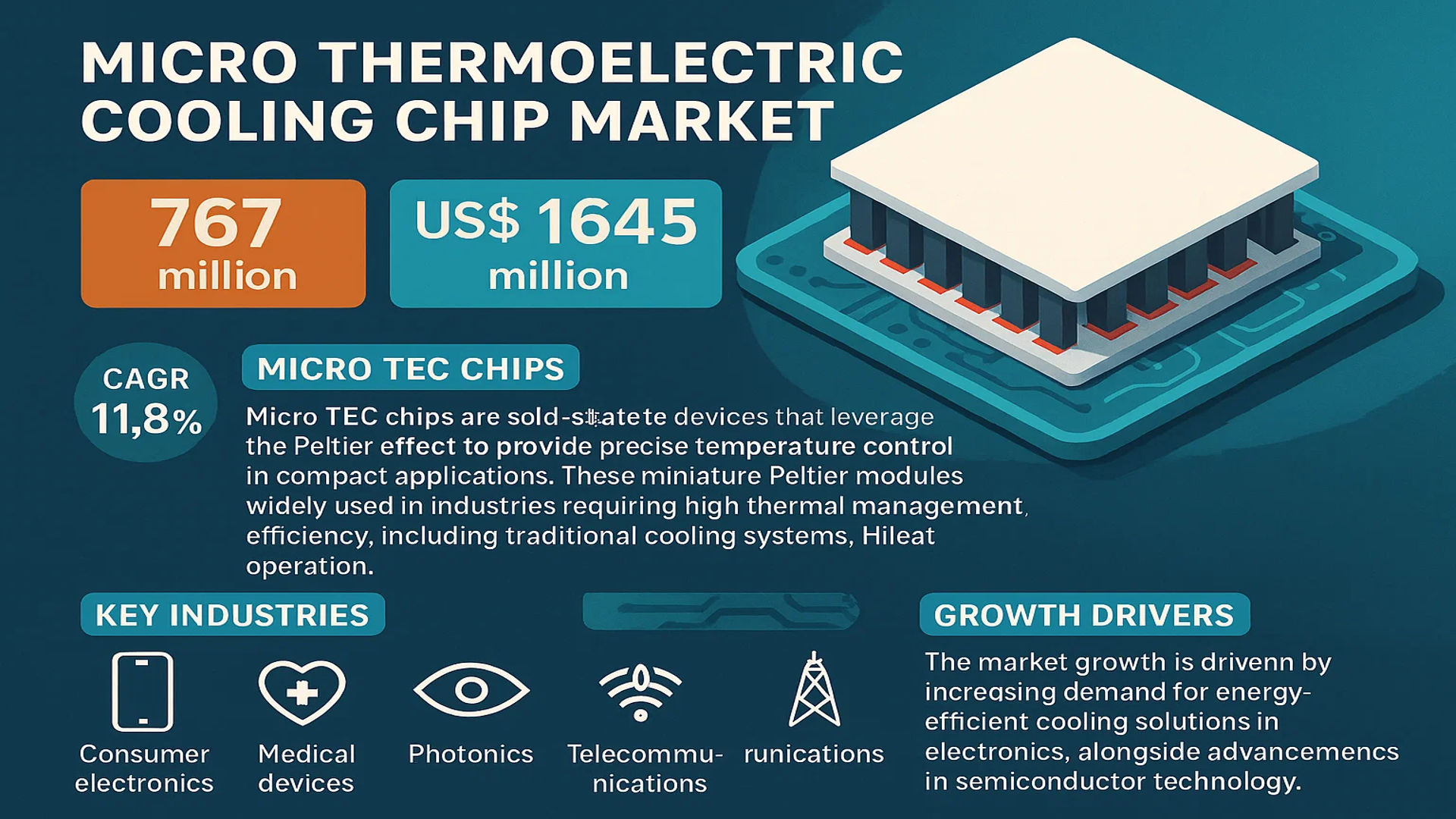

The global Micro Thermoelectric Cooling Chip Market was valued at 767 million in 2024 and is projected to reach US$ 1645 million by 2032, at a CAGR of 11.8% during the forecast period.

Micro Thermoelectric Cooling (Micro TEC) chips are solid-state devices that leverage the Peltier effect to provide precise temperature control in compact applications. These miniature Peltier modules are widely used in industries requiring high thermal management efficiency, including consumer electronics, medical devices, photonics, and telecommunications. Unlike traditional cooling systems, Micro TECs operate without moving parts, offering reliability and silent operation.

The market growth is driven by increasing demand for energy-efficient cooling solutions in electronics, alongside advancements in semiconductor technology. While North America currently leads in adoption due to strong R&D investments, Asia-Pacific is emerging as a high-growth region because of expanding electronics manufacturing. Key players such as Coherent Corp, Ferrotec, and Laird Thermal Systems are investing in product innovations to capture opportunities in sectors like 5G infrastructure and electric vehicles, where thermal management is critical.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Miniaturized Cooling Solutions in Electronics to Accelerate Market Growth

The global micro thermoelectric cooling chip market is experiencing significant growth, primarily driven by the electronics industry’s relentless push toward miniaturization. As electronic components become smaller and more powerful, conventional cooling methods often prove inadequate. Micro TECs offer precise temperature control in compact form factors, making them ideal for smartphones, wearables, and IoT devices. The consumer electronics sector alone is expected to account for over 35% of micro TEC applications by 2026.

Advancements in Medical Technology to Fuel Adoption

Medical applications represent one of the fastest-growing segments for micro thermoelectric cooling chips. These components are critical for maintaining precise temperatures in portable medical devices, diagnostic equipment, and laboratory instruments. The global medical device market, currently valued at over $500 billion, is increasingly incorporating micro TEC technology for applications ranging from DNA sequencing equipment to portable imaging systems. Their solid-state nature makes them particularly valuable for sensitive medical environments where reliability and precision are paramount.

Emerging applications in laser diode cooling and optical communication systems further contribute to market expansion. The telecommunications sector’s rapid growth, particularly with 5G deployment, creates substantial demand for temperature stabilization in photonic components.

MARKET RESTRAINTS

High Production Costs and Material Challenges Limit Market Penetration

Despite their advantages, micro thermoelectric cooling chips face significant adoption barriers. The manufacturing process requires specialized materials like bismuth telluride, with material costs accounting for approximately 60-70% of total production expenses. While performance continues to improve, achieving high coefficients of performance (COP) at miniature scales remains technically challenging. These cost factors make micro TECs less competitive compared to conventional cooling methods in price-sensitive applications.

Other Constraints

Temperature Differential Limitations

Current micro TEC designs typically achieve maximum temperature differentials of 60-70°C, restricting use in applications requiring more extreme cooling. While multi-stage designs can improve performance, they significantly increase complexity and cost.

Energy Efficiency Concerns

At smaller scales, energy efficiency becomes increasingly critical. Many micro TEC applications in portable devices face strict power budgets, requiring novel designs to maintain effectiveness while minimizing power consumption.

MARKET CHALLENGES

Technical Hurdles in Manufacturing Consistency

The micro TEC market faces persistent quality control challenges in mass production. Maintaining consistent performance across miniature thermoelectric modules requires extremely precise manufacturing tolerances. Current yield rates for high-performance micro TECs remain below 80% at many facilities, driving up costs. Additionally, thermal cycling stresses can lead to premature failure if bonding interfaces aren’t properly engineered.

The industry also grapples with materials science challenges. While bismuth telluride alloys remain standard, their relatively low melting points and mechanical fragility complicate thin-film deposition processes at micro scales.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicles to Unlock New Growth Potential

The automotive sector presents significant opportunities, particularly for battery thermal management in electric vehicles. As EV adoption accelerates globally, with projections exceeding 30 million annual sales by 2030, micro TECs offer precise temperature control solutions for battery cells and power electronics. Their compact size and solid-state reliability make them attractive alternatives to liquid cooling systems in certain applications.

Advancements in wearable technology and smart clothing represent another promising frontier. Several leading sportswear brands are actively developing next-generation wearable cooling systems incorporating micro TEC technology for athletic and medical applications. The global wearable technology market is expected to surpass $100 billion by the end of the decade, creating substantial demand for miniature thermal management solutions.

MICRO THERMOELECTRIC COOLING CHIP MARKET TRENDS

Miniaturization in Electronics Drives Demand for Micro TEC Solutions

The rapid advancement of compact and high-power-density electronics has significantly increased the need for precise thermal management solutions, positioning Micro Thermoelectric Cooling (Micro TEC) chips as a critical enabler in modern applications. With the global Micro TEC market projected to grow from $767 million in 2024 to $1.645 billion by 2032, expanding at a CAGR of 11.8%, industries are prioritizing these solid-state cooling devices for their reliability and space-saving advantages. Unlike traditional cooling methods, Micro TECs offer localized temperature control without moving parts, making them indispensable in consumer electronics, medical devices, and telecommunications equipment. Their adoption is further accelerated by the trend toward edge computing and IoT devices, where efficient heat dissipation in confined spaces is non-negotiable.

Other Trends

Electrification of Automotive and Aerospace Systems

The automotive and aerospace sectors are increasingly integrating Micro TEC chips to manage thermal loads in electric vehicle battery systems, LiDAR modules, and avionics. Automakers are leveraging these chips to enhance the efficiency of onboard electronics, with single-stage TEC modules alone expected to capture a significant share of the market. Additionally, the aerospace industry relies on Micro TECs for satellite thermal regulation, as their lightweight and vibration-resistant properties align with stringent performance requirements. The convergence of 5G infrastructure deployment and autonomous vehicle technologies is further amplifying demand, as these applications require fail-safe thermal management in extreme environments.

Healthcare Innovations Fuel Precision Cooling Needs

Medical applications, particularly in diagnostic imaging and portable medical devices, are driving specialized Micro TEC adoption. Devices such as PCR machines, blood analyzers, and infrared sensors rely on precise temperature stabilization to ensure accuracy, with multi-stage TECs emerging as the preferred solution for ultra-low-temperature requirements. The medical segment is projected to grow significantly, supported by advancements in point-of-care diagnostics and wearable health monitors. Meanwhile, partnerships between semiconductor manufacturers and healthcare providers are fostering customized solutions, such as implantable cooling systems for neurological therapies. As regulatory standards for medical equipment tighten globally, the demand for energy-efficient and contamination-free cooling will continue to rise.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation in Compact Cooling Solutions

The global micro thermoelectric cooling chip market features a dynamic mix of established manufacturers and emerging players, competing across diverse applications from consumer electronics to aerospace. Coherent Corp and Ferrotec Corporation currently dominate market share, leveraging their extensive R&D capabilities and vertically integrated manufacturing processes. Their dominance stems from proprietary semiconductor material formulations that enable higher energy efficiency in compact form factors – a critical requirement across end-use industries.

Meanwhile, Laird Thermal Systems has emerged as a key innovator, particularly in medical device cooling applications. The company’s recent partnership with a leading MRI equipment manufacturer demonstrates how specialized thermal management solutions are becoming integral to advanced healthcare technologies. Similarly, TE Technology has strengthened its position through strategic acquisitions, expanding its portfolio of miniature thermoelectric assemblies for 5G infrastructure.

Asia-based manufacturers like Guangdong Fuxin Technology and Zhejiang Advanced Thermoelectric Technology are rapidly gaining ground by offering cost-competitive alternatives without compromising performance benchmarks. Their growing influence reflects the increasing importance of localized supply chains, especially in consumer electronics manufacturing hubs across China and Southeast Asia.

List of Key Micro Thermoelectric Cooling Chip Manufacturers

- Coherent Corp (U.S.)

- Ferrotec Corporation (Japan)

- Laird Thermal Systems (U.K.)

- TEC Microsystems GmbH (Germany)

- Guangdong Fuxin Technology (China)

- TE Technology, Inc. (U.S.)

- Zhejiang Advanced Thermoelectric Technology (China)

- Z-MAX Co. Ltd. (Japan)

- Kryotherm (Russia)

- Thermonamic Electronics (China)

The competitive landscape continues evolving as manufacturers invest in next-generation materials like bismuth telluride composites and graphene-enhanced substrates. Such advancements are particularly crucial for applications requiring extreme temperature stability, such as aerospace sensors and electric vehicle battery management systems. Market leaders are also expanding production capacities in strategic regions to mitigate supply chain risks while meeting growing demand for localized thermal solutions.

Segment Analysis:

By Type

Single-Stage TEC Segment Leads Due to Cost-Effectiveness and Widespread Applications

The market is segmented based on type into:

- Single-Stage TEC

- Subtypes: Standard, Miniature, and High-Performance

- Multi-Stage TEC

- Subtypes: Cascade and Stacked Configurations

- Micro TEC Arrays

- Thin-Film Thermoelectric Modules

- Others

By Application

Consumer Electronics Segment Dominates Owing to Expanding Use in Smartphones and Wearables

The market is segmented based on application into:

- Consumer Electronics

- Medical Devices

- Automotive Electronics

- Aerospace & Defense Systems

- Industrial Equipment

- Others

By Cooling Capacity

Low-Capacity Cooling Solutions See High Demand for Portable Device Applications

The market is segmented based on cooling capacity into:

- Low-Capacity (Below 5W)

- Medium-Capacity (5W-50W)

- High-Capacity (Above 50W)

By Substrate Material

Ceramic Substrates Preferred for Their Thermal and Electrical Properties

The market is segmented based on substrate material into:

- Ceramic Substrates

- Metal Substrates

- Polymer Substrates

- Others

Regional Analysis: Micro Thermoelectric Cooling Chip Market

North America

North America leads the global Micro Thermoelectric Cooling Chip market, driven by advanced R&D investments, particularly in the U.S. semiconductor and medical device sectors. The region benefits from strong demand for precision cooling in data centers, 5G infrastructure, and electric vehicle battery management systems. Companies like Coherent Corp and Laird Thermal Systems capitalize on this growth, supported by government initiatives such as the CHIPS Act, which allocates $52 billion for semiconductor manufacturing. However, high production costs and competition from Asian manufacturers create pricing pressures. The U.S. accounts for over 60% of regional market revenue, with Canada emerging as a key adopter in aerospace applications.

Asia-Pacific

Asia-Pacific is the fastest-growing market, projected to dominate volume consumption by 2032 due to China’s electronics manufacturing boom and Japan’s leadership in photonics. China’s Guangdong Fuxin Technology and Zhejiang Advanced Thermoelectric Technology leverage cost advantages to supply 40% of global Micro TEC demand. India’s expanding telecom sector and Southeast Asia’s medical device production further propel growth. While price sensitivity favors single-stage TECs, premium applications in automotive ADAS systems and industrial automation are driving multi-stage chip adoption. The region faces challenges in standardization but benefits from vertically integrated supply chains.

Europe

Europe’s market thrives on stringent energy-efficiency regulations and automotive electrification trends, particularly in Germany and France. The EU’s Ecodesign Directive pushes for sustainable cooling solutions in consumer electronics, benefiting suppliers like TEC Microsystems GmbH. Medical applications, including portable diagnostic devices, account for 28% of regional demand. However, reliance on imported raw materials and slow adoption in Eastern Europe limit growth potential. Collaborative R&D initiatives between universities and manufacturers aim to improve material efficiency, addressing the region’s cost competitiveness gap.

South America

South America shows nascent but promising growth, with Brazil leading in industrial process cooling applications for food processing and mining equipment. Argentina’s renewable energy projects create opportunities for thermoelectric power generation modules. Market expansion faces hurdles from economic instability, import dependency, and fragmented distribution networks. Local players focus on retrofit solutions for existing machinery rather than high-end applications. The region’s growth trajectory depends on stabilization of semiconductor supply chains and increased foreign direct investment.

Middle East & Africa

The MEA market remains underdeveloped but presents long-term potential in oil & gas sensor cooling and telecommunications infrastructure. UAE and Saudi Arabia drive demand through smart city initiatives, while South Africa leads in medical equipment applications. Limited local manufacturing capacity results in 90% import dependency, primarily from European and Chinese suppliers. Growth is constrained by budgetary priorities favoring conventional cooling systems, though increasing data center investments signal future opportunities for Micro TEC adoption in harsh climatic conditions.

Report Scope

This market research report provides a comprehensive analysis of the Global Micro Thermoelectric Cooling Chip Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 767 million in 2024 and is projected to reach USD 1645 million by 2032, growing at a CAGR of 11.8%.

- Segmentation Analysis: Detailed breakdown by product type (Single-Stage TEC, Multi-Stage TEC), application (Consumer Electronics, Communications, Medical, Automobile, Industry, Aerospace and Defense), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including Coherent Corp, Ferrotec, Laird Thermal Systems, TEC Microsystems GmbH, and Guangdong Fuxin Technology, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor materials, miniaturization techniques, and integration with IoT/AI-driven thermal management systems.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for compact cooling solutions in electronics, alongside challenges like high production costs and material limitations.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs primary and secondary research methodologies, including expert interviews and analysis of verified market data, to deliver accurate and actionable insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Micro Thermoelectric Cooling Chip Market?

-> Micro Thermoelectric Cooling Chip Market was valued at 767 million in 2024 and is projected to reach US$ 1645 million by 2032, at a CAGR of 11.8% during the forecast period.

Which key companies operate in this market?

-> Key players include Coherent Corp, Ferrotec, Laird Thermal Systems, TEC Microsystems GmbH, and Guangdong Fuxin Technology, among others.

What are the key growth drivers?

-> Growth is driven by rising demand for compact thermal management in electronics, medical devices, and automotive applications, alongside advancements in semiconductor materials.

Which region dominates the market?

-> Asia-Pacific leads in market share due to robust electronics manufacturing, while North America shows significant growth in medical and defense applications.

What are the emerging trends?

-> Emerging trends include development of high-efficiency thermoelectric materials, integration with IoT for smart cooling, and miniaturization for wearable devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...