MARKET INSIGHTS

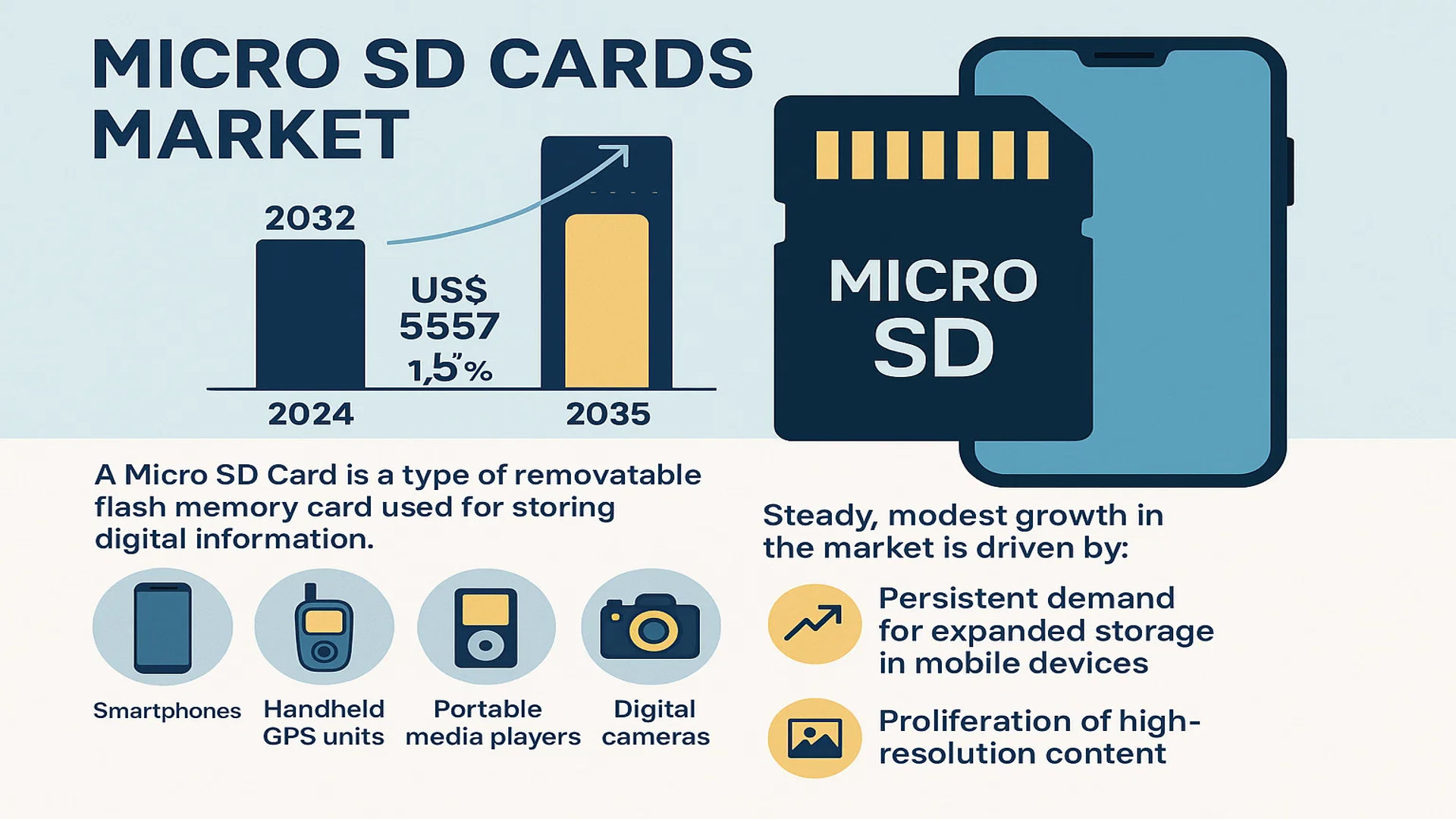

The global Micro SD Cards Market was valued at 5014 million in 2024 and is projected to reach US$ 5557 million by 2032, at a CAGR of 1.5% during the forecast period.

A Micro SD Card is a type of removable flash memory card used for storing digital information. SD is an abbreviation of Secure Digital, and these cards are a compact form factor essential for portable data storage. They are primarily utilized in smartphones, which account for the largest application segment. Furthermore, they are integral components in devices such as handheld GPS units, portable media players, digital cameras, gaming consoles, and expandable USB flash drives.

The market is experiencing steady, albeit modest, growth driven by the persistent demand for expanded storage in mobile devices and the proliferation of high-resolution content. However, this growth is tempered by the increasing integration of larger internal storage capacities in smartphones and the rising adoption of cloud-based solutions. In terms of product segmentation, the SDHC (2G-32G) category dominates, holding over 80% of the market share. Geographically, Taiwan is the largest manufacturing hub, representing over 30% of the market, followed by Japan and China, which each hold over a 20% share. Key players operating in this competitive landscape include SanDisk, Samsung Electronics, Kingston Technology, and Toshiba.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of High-Resolution Mobile Content Creation to Drive Market Growth

The exponential growth in smartphone adoption globally continues to fuel demand for expandable storage solutions. With over 6.8 billion smartphone users worldwide generating increasingly data-intensive content, the need for reliable, high-capacity storage has become paramount. Modern smartphones now routinely feature 4K video recording capabilities, high-resolution photography, and resource-intensive applications that quickly consume internal storage. This creates sustained demand for microSD cards as essential expansion tools. The average smartphone user now generates approximately 4.3 GB of data monthly, creating persistent storage pressure that drives replacement cycles and capacity upgrades. Furthermore, the gaming segment on mobile devices has evolved into a major storage consumer, with premium titles often requiring 2-5 GB of installation space plus additional data for updates and saved content.

Expansion of IoT and Edge Computing Devices to Accelerate Market Expansion

The rapid deployment of Internet of Things devices across industrial, commercial, and consumer segments represents a significant growth vector for microSD cards. These storage solutions provide critical local storage capabilities for edge computing devices that process data before cloud transmission. Surveillance systems, automotive infotainment units, industrial controllers, and smart home devices increasingly incorporate microSD slots for data logging, firmware storage, and operational redundancy. The industrial IoT sector alone is projected to maintain a compound annual growth rate exceeding 12%, directly driving demand for reliable, high-endurance storage solutions. These applications require cards with superior temperature tolerance, extended write cycles, and enhanced data integrity features that command premium pricing and contribute to market value growth despite volume fluctuations in consumer segments.

Advancements in Storage Technology and Capacity Scaling to Stimulate Demand

Technological innovations in 3D NAND flash memory and controller architectures continue to push storage capacities upward while reducing cost per gigabyte. The transition to higher capacity SDXC and SDUC formats enables cards that can store 1TB or more, making them viable alternatives to portable SSDs for certain applications. This capacity progression addresses the growing storage requirements of professional content creators, drone operators, and action camera enthusiasts who require reliable high-capacity storage in compact form factors. The photography and videography segments particularly benefit from these advancements, as 8K video recording and high-resolution burst photography modes generate files exceeding hundreds of megabytes per second of recording. These technical improvements maintain market relevance despite increasing internal storage options in some device categories.

MARKET RESTRAINTS

Increasing Integration of Non-Expandable Device Designs to Constrain Market Growth

The trend toward sealed, non-expandable device architectures presents a significant challenge to microSD card adoption. Major smartphone manufacturers have increasingly eliminated external storage slots in premium devices, citing design integrity, performance optimization, and security considerations. This design philosophy has trickled down to mid-range devices, reducing the addressable market for consumer storage expansion. Approximately 42% of smartphones shipped in the last year featured no expandable storage options, representing a substantial constraint on market growth. This shift is particularly pronounced in North American and European markets where carrier-subsidized device plans often prioritize integrated storage upgrades over expandable options. The resulting decline in socket availability directly impacts volume sales and requires market participants to pivot toward alternative applications and regions.

Performance Limitations Compared to Integrated Storage Solutions to Restrict Premium Applications

Inherent performance limitations of removable flash storage create adoption barriers in performance-sensitive applications. The interface constraints of microSD technology limit maximum sequential read speeds to approximately 300 MB/s under ideal conditions, while integrated UFS storage solutions routinely achieve speeds exceeding 800 MB/s. This performance gap becomes particularly relevant for applications requiring rapid data access, such as high-bitrate video recording, augmented reality applications, and resource-intensive mobile gaming. The latency introduced by removable storage interfaces can also impact application loading times and system responsiveness, leading device manufacturers to prioritize integrated solutions for premium segments. These technical limitations confine microSD cards primarily to secondary storage roles rather than primary performance storage applications.

Counterfeit Products and Quality Consistency Issues to Erode Consumer Confidence

The prevalence of counterfeit and substandard products in the market creates significant challenges for legitimate manufacturers and consumers alike. Fake cards often report inflated capacities while actually containing far less storage, leading to data loss and consumer frustration. Industry estimates suggest approximately 15-20% of cards sold through certain online marketplaces may be counterfeit or misrepresented. These products not only capture revenue that would otherwise go to legitimate manufacturers but also damage overall consumer confidence in the product category. The performance inconsistencies and reliability issues associated with counterfeit cards create hesitation among consumers considering storage expansions, particularly for valuable data storage applications. This problem is exacerbated by the difficulty consumers face in verifying authentic products and the technical sophistication required to identify performance discrepancies.

MARKET CHALLENGES

Intensifying Price Competition and Margin Compression to Challenge Manufacturer Viability

The microSD card market faces severe price competition that threatens manufacturer profitability and innovation investment. Flash memory represents a commoditized technology with numerous manufacturers capable of producing functionally similar products. This environment creates relentless downward pressure on prices, with average selling prices declining approximately 8-12% annually despite capacity increases. The manufacturing infrastructure required for competitive flash production requires billions in capital investment, creating significant barriers to entry but intense competition among established players. This combination of high fixed costs and declining prices squeezes profit margins, particularly for manufacturers lacking vertical integration or proprietary technology advantages. The situation is further complicated by cyclical flash memory pricing fluctuations that can abruptly transform profitable segments into loss-making operations.

Other Challenges

Technical Standardization and Compatibility Issues

The evolution of storage standards creates compatibility challenges across device generations. Newer UHS-III, Speed Class, and Application Performance Class ratings create consumer confusion and compatibility concerns with older devices. This standards fragmentation requires manufacturers to maintain extensive product SKUs to address different market segments and device requirements. The backward compatibility requirements also constrain innovation, as new features must not disrupt functionality in older host devices. These technical complexities increase manufacturing costs, complicate inventory management, and create consumer adoption barriers when purchasers cannot easily determine compatibility with their specific devices.

Data Security and Reliability Concerns

The removable nature of microSD cards introduces data security vulnerabilities that integrated solutions avoid. Cards can be easily removed, lost, or stolen, potentially exposing sensitive data. The physical interface also represents a potential entry point for malware or unauthorized data extraction. These security concerns limit adoption in enterprise and government applications where data protection is paramount. Additionally, the consumer perception of removable storage as less reliable than integrated solutions creates adoption resistance for critical data storage, despite technological advances that have significantly improved card reliability and endurance ratings.

MARKET OPPORTUNITIES

Emerging Applications in Automotive and Surveillance Systems to Create New Growth Vectors

The automotive industry’s rapid digitization creates substantial opportunities for high-reliability storage solutions. Modern vehicles increasingly incorporate multiple systems requiring local storage, including dashcams, event data recorders, infotainment systems, and autonomous driving data loggers. These applications require storage solutions capable of withstanding extreme temperatures, vibration, and extended write cycles without failure. The automotive segment typically commands premium pricing for qualified components, providing margin relief from commoditized consumer segments. Similarly, the surveillance market continues to expand globally, with both consumer and professional systems requiring reliable storage for continuous recording. These applications often utilize multiple cards in rotation or RAID-like configurations, increasing per-system storage requirements and creating opportunities for specialized high-endurance products.

Development of Specialized Performance Tiers and Application-Specific Solutions to Enable Premium Segmentation

Market participants increasingly differentiate products through application-specific optimizations that command price premiums. Gaming-optimized cards featuring faster load times, surveillance cards with enhanced write endurance, and photography cards with sustained write speeds for burst mode capture represent emerging specialized segments. This diversification allows manufacturers to escape the worst effects of commoditization by creating value-added products addressing specific use case requirements. The professional content creation segment particularly shows willingness to pay premium prices for guaranteed performance and reliability, with specialized cards often commanding 100-200% price premiums over standard offerings with similar capacities. This trend toward market segmentation creates opportunities for brand differentiation and margin protection despite overall market price erosion.

Expansion in Emerging Markets and Value Segment Devices to Sustain Volume Growth

While premium devices in developed markets often omit expandable storage, budget and mid-range devices in emerging markets continue to incorporate microSD support as a cost-effective storage expansion solution. Markets across Southeast Asia, Latin America, and Africa show strong demand for expandable storage options as consumers seek to maximize functionality from value-oriented devices. These regions frequently feature data-intensive usage patterns despite network constraints, making local storage expansion particularly valuable. The growing middle class in these regions represents a substantial volume opportunity, with smartphone penetration rates still below saturation levels. Manufacturers can leverage these markets to maintain production volumes and offset declining demand in mature markets where integrated storage predominates.

MICRO SD CARDS MARKET TRENDS

Rising Demand for High-Capacity Storage in Mobile Devices to Emerge as a Trend in the Market

The proliferation of high-resolution content, including 4K video recording, advanced mobile gaming, and extensive application libraries, is fundamentally driving the need for expanded storage in smartphones and other portable electronics. While many flagship devices offer substantial internal storage, the cost-effectiveness and flexibility of expandable memory remain highly attractive to a broad consumer base. This is particularly evident in emerging markets, where price sensitivity is a significant factor. The market has responded with a pronounced shift towards higher capacity cards, with the SDHC (2G-32G) segment historically dominating but now being rapidly supplemented by the SDXC (32G-400G) category. This evolution is critical as the average size of mobile applications and media files continues to grow exponentially, necessitating reliable and affordable external storage solutions that can keep pace with consumer demand.

Other Trends

Integration with IoT and Edge Computing Devices

Beyond traditional consumer electronics, the Micro SD card market is experiencing growth through its integration into a new generation of Internet of Things (IoT) devices and edge computing systems. These applications require robust, low-power, and removable storage for data logging, firmware updates, and temporary processing at the network’s edge. From smart security cameras and industrial sensors to in-car infotainment systems, Micro SD cards provide a standardized and reliable form factor for non-volatile memory. This diversification of application is creating new, stable revenue streams for manufacturers, moving beyond the volatile smartphone cycle and into more specialized industrial and commercial sectors that value durability and long-term data integrity.

Technological Advancements in Speed and Reliability

The relentless pursuit of faster data transfer speeds and enhanced reliability is a cornerstone of the market’s evolution. The adoption of newer bus interfaces, such as UHS-I, UHS-II, and UHS-III, alongside application performance class ratings like A1 and A2 (designed specifically for smoother app operation directly from the card), are direct responses to performance bottlenecks in modern devices. Furthermore, advancements in 3D NAND flash memory technology have been instrumental. This technology allows for higher storage densities within the same physical space, enabling the production of terabyte-level Micro SD cards that were once unimaginable. This technological arms race, focused on achieving higher read/write speeds and greater endurance, is a key differentiator among leading brands and a primary driver for consumers upgrading their storage media to match the capabilities of their new devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Prioritize Innovation and Capacity Expansion to Secure Market Position

The global Micro SD Cards market is characterized by a highly concentrated competitive environment, dominated by a handful of major flash memory manufacturers and technology conglomerates. These players compete intensely on factors such as storage capacity, data transfer speeds, product reliability, and price. The market’s concentration is largely due to the significant capital investment required for NAND flash fabrication facilities and the complex intellectual property surrounding memory controller technology.

SanDisk, a subsidiary of Western Digital Corporation, is a preeminent force in this space. Its leadership is anchored in its extensive patent portfolio, longstanding brand recognition, and widespread distribution network. The company has consistently pioneered higher capacity and speed classes, such as the SDXC and SDUC standards. Similarly, Samsung Electronics and Micron Technology (through its Crucial and Lexar brands) leverage their vertical integration, controlling the production of NAND flash chips, which provides a critical advantage in managing supply chains and cost structures, especially during periods of global semiconductor shortage.

These leading companies are aggressively pursuing growth through strategic capacity expansions and technological advancements. For instance, the industry-wide transition to more advanced 3D NAND stacking processes allows for higher storage densities at a lower cost per gigabyte. This technological race is crucial for meeting the escalating demand for high-capacity storage in 4K/8K video recording, advanced mobile gaming, and increasingly sophisticated smartphone applications.

Meanwhile, other significant players like Kingston Technology, Transcend Information, and ADATA Technologies are strengthening their market positions by focusing on specific consumer segments and value propositions. Kingston, for example, has built a strong reputation for reliability and customer support. These companies often compete effectively in the mid-range market by offering robust performance and competitive pricing, frequently sourcing NAND flash from the major manufacturers and differentiating themselves through their controller designs and firmware.

The competitive dynamics are further influenced by regional strengths. A substantial portion of the world’s memory card manufacturing and assembly is concentrated in Taiwan, China, and Japan, which together account for a significant majority of global production. This regional concentration impacts logistics, production costs, and the ability to respond swiftly to shifts in global demand.

List of Key Micro SD Cards Companies Profiled

- SanDisk (Western Digital Corporation) (U.S.)

- Samsung Electronics (South Korea)

- Micron Technology Inc. (U.S.)

- Kingston Technology Company, Inc. (U.S.)

- Transcend Information, Inc. (Taiwan)

- ADATA Technology Co., Ltd. (Taiwan)

- Panasonic Corporation (Japan)

- Sony Corporation (Japan)

- Toshiba Corporation (Japan)

- PNY Technologies, Inc. (U.S.)

- Lexar (A brand of Micron Technology) (U.S.)

Segment Analysis:

By Type

SDHC (2G-32G) Segment Dominates the Market Due to its Optimal Balance of Capacity, Cost, and Compatibility

The market is segmented based on type into:

- SD (8M-2G)

- SDHC (2G-32G)

- SDXC (32G-400G)

By Application

Smartphone Segment Leads Due to Pervasive Global Adoption and High Storage Demands for Multimedia Content

The market is segmented based on application into:

- Smartphone

- Tablet PC

- Digital Camera

- Gaming Consoles

- Others

By End User

Consumer Electronics Segment Leads Due to High Volume Sales in Mobile Devices and Portable Gadgets

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Industrial

- Others

By Sales Channel

Retail Segment Leads Due to Widespread Availability and Consumer Preference for In-Person Purchases

The market is segmented based on sales channel into:

- Retail

- Online

- OEM

Regional Analysis: Micro SD Cards Market

Asia-Pacific

The Asia-Pacific region dominates the global Micro SD Cards market, accounting for over 70% of both production and consumption volume. This leadership is anchored by Taiwan, which holds a market share exceeding 30%, largely due to its robust semiconductor and electronics manufacturing ecosystem. Key players like Transcend Information and ADATA Technologies are headquartered here, driving innovation and high-volume output. China and Japan follow closely, each commanding over 20% of the market. The region’s strength stems from its massive consumer electronics manufacturing base, particularly for smartphones, which is the largest application segment. While cost-competitive SDHC cards (2G-32G) remain the volume leader, there is a noticeable and accelerating shift towards higher-capacity SDXC cards (32G-400G) to meet the demands of 4K video recording, advanced mobile gaming, and burgeoning IoT device adoption. However, intense price competition and market saturation in entry-level segments present ongoing challenges for manufacturers.

North America

The North American market is characterized by a high demand for premium, high-performance Micro SD cards. Consumers and enterprises prioritize speed (UHS-I, UHS-II classes), reliability, and large capacities, driven by the use-case in high-resolution photography, professional videography, and next-generation gaming consoles like the PlayStation 5 and Xbox Series X/S. The United States is the largest national market within the region. Leading brands such as SanDisk (a Western Digital company) and Kingston Technology have a strong presence, leveraging their brand reputation for quality. The market is relatively mature, with growth primarily fueled by the replacement cycle of existing devices and the adoption of new technologies that require more robust storage solutions, such as action cameras and drones. While volume growth is modest, value growth is sustained by the steady uptake of higher-margin, high-capacity products.

Europe

Europe represents a stable and quality-conscious market for Micro SD cards. Stringent consumer protection laws and environmental regulations, such as the EU’s WEEE Directive, influence product standards and recycling programs, adding a layer of compliance for suppliers. Germany, the UK, and France are the key revenue contributors. The demand pattern mirrors North America’s in its preference for high-speed, high-reliability cards from established brands like Sony and Samsung Electronics. A significant application driving demand is the automotive sector, where Micro SD cards are increasingly used for in-car infotainment systems and navigation data storage. Furthermore, the region’s strong gaming culture supports consistent sales for Nintendo Switch and other portable gaming devices. The market is highly competitive, with a focus on brand trust, data security, and product longevity rather than just price.

South America

The South American market is emerging and is primarily driven by price sensitivity and growing smartphone penetration. Brazil and Argentina are the largest markets, but economic volatility often leads to fluctuating demand and a consumer preference for more affordable SDHC cards. The market is largely served by international brands and local distributors, with a significant volume of sales coming from the replacement and upgrade market for mobile phones. The adoption of higher-capacity cards is slower compared to more developed regions, hindered by lower disposable income and the higher cost of advanced storage media. Nonetheless, as mobile network infrastructure improves and data consumption rises, there is a clear, albeit gradual, trajectory towards the adoption of larger capacity cards to store more media content locally.

Middle East & Africa

The Middle East and Africa region presents a market with strong potential for long-term growth, though it is currently in a developing phase. The United Arab Emirates, Saudi Arabia, and South Africa are the most active markets. Demand is primarily fueled by rising smartphone ownership, increasing internet penetration, and a young, tech-savvy population. Similar to South America, the market is cost-driven, with a high volume of mid-range capacity cards. However, affluent consumer segments in Gulf Cooperation Council (GCC) countries demonstrate a growing appetite for premium products for use in high-end drones, cameras, and gaming. The main challenges include underdeveloped retail distribution channels in certain areas and economic disparities that limit widespread adoption of high-end storage solutions. Market growth is expected to correlate closely with broader economic development and digitalization initiatives across the region.

Report Scope

This market research report provides a comprehensive analysis of the global Micro SD Cards market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Micro SD Cards Market?

-> Micro SD Cards Market was valued at 5014 million in 2024 and is projected to reach US$ 5557 million by 2032, at a CAGR of 1.5% during the forecast period.

Which key companies operate in Global Micro SD Cards Market?

-> Key players include SanDisk, Transcend Information, ADATA Technologies, Panasonic, Kingston Technology, Micron Technology, Sony, Samsung Electronics, Toshiba, PNY Technologies, and Lexar, among others.

What are the key growth drivers?

-> Key growth drivers include rising smartphone penetration, increasing demand for high-capacity storage in consumer electronics, and growth in gaming consoles and IoT devices.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with Taiwan holding over 30% market share, followed by Japan and China, each with over 20% share.

What are the emerging trends?

-> Emerging trends include development of higher capacity SDXC cards, integration of advanced security features, and adoption of UHS (Ultra High Speed) interfaces for faster data transfer.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...