MEMS Test Cell Market Insights

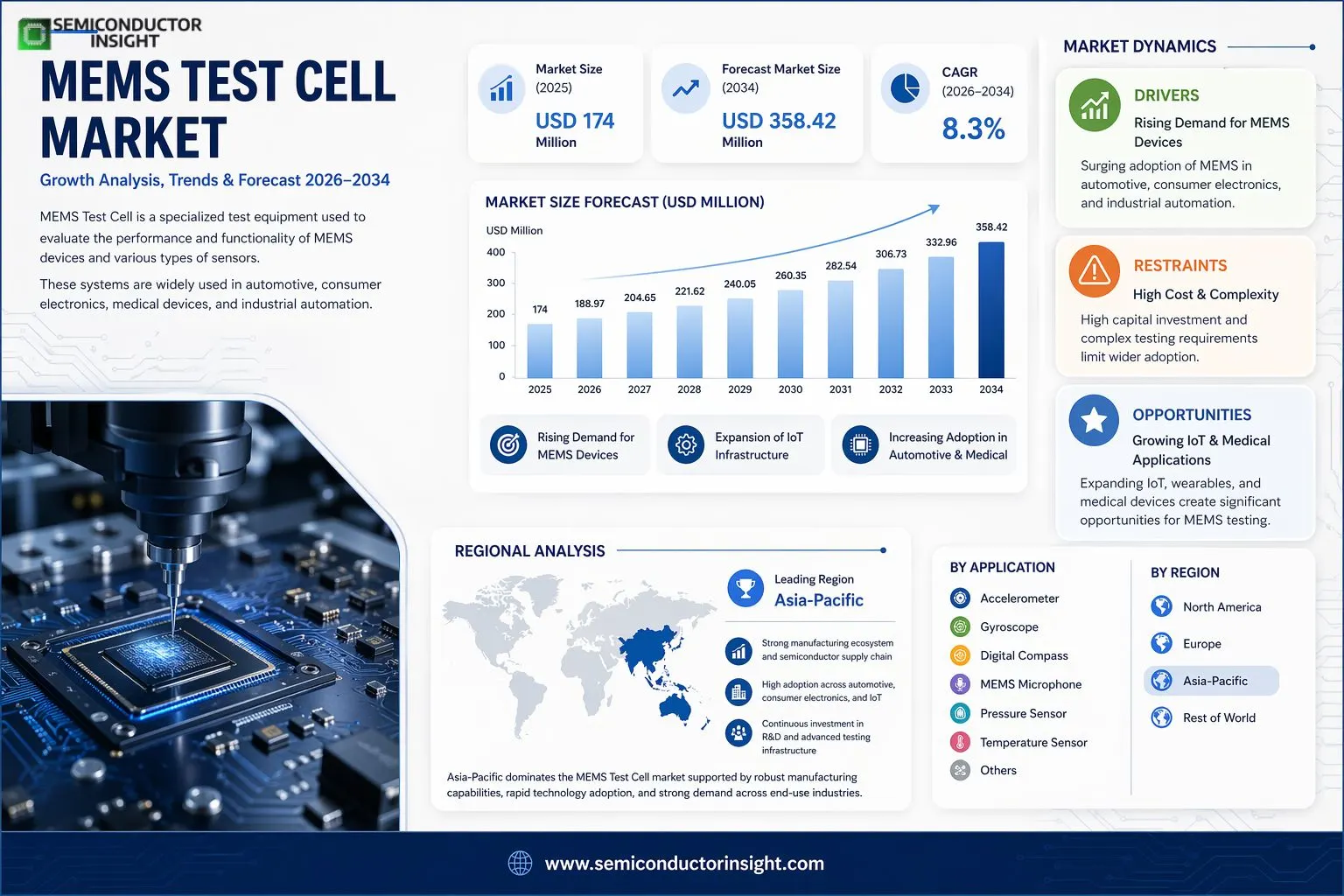

Global MEMS Test Cell market size was valued at USD 174 million in 2025. The market is projected to grow from USD 188.97 million in 2026 to USD 358.42 million by 2034, exhibiting a CAGR of 8.3% during the forecast period.

MEMS Test Cell is a specialized test equipment used to evaluate the performance and functionality of Micro-Electro-Mechanical Systems (MEMS) devices and various types of sensors. MEMS are tiny mechanical devices integrated with electronics, typically in the range of micrometers to millimeters in size, capable of performing tasks such as sensing, actuation, and signal processing. These systems find widespread application across automotive (e.g., airbag sensors), consumer electronics (e.g., accelerometers, gyroscopes), medical devices, and industrial automation sectors.

The market is gaining strong momentum because of the accelerating adoption of MEMS-based devices across high-growth end-use industries, combined with rising quality and reliability standards that demand rigorous pre-integration testing. MEMS Test Cell solutions are essential for validating electrical, mechanical, and environmental parameters of sensors , including accelerometers, gyroscopes, digital compasses, MEMS microphones, pressure sensors, and temperature sensors , to ensure they meet stringent performance specifications. Furthermore, the growing proliferation of Internet of Things (IoT) devices, autonomous vehicles, and wearable health technologies continues to generate substantial demand for advanced MEMS testing infrastructure. Advantest, Cohu, Inc., NI (SET GmbH), STATEC, SPEA S.p.A., and YTEC are among the key players operating in Global MEMS Test Cell market with comprehensive product portfolios.

MARKET DRIVERS

Rising Demand for MEMS Devices Across Consumer Electronics and Automotive Sectors

Global MEMS Test Cell Market is experiencing robust growth driven by the surging adoption of microelectromechanical systems (MEMS) in consumer electronics, automotive safety systems, and industrial automation. As MEMS sensors , including accelerometers, gyroscopes, pressure sensors, and microphones , become standard components in smartphones, wearables, and advanced driver-assistance systems (ADAS), manufacturers face mounting pressure to ensure high-precision testing at scale. MEMS test cells provide the controlled environments and automated characterization capabilities necessary to validate these devices before deployment, making them indispensable to modern semiconductor manufacturing workflows.

Expansion of IoT Infrastructure and Smart Device Ecosystems

The rapid proliferation of Internet of Things (IoT) applications has significantly amplified demand for reliable MEMS components, which in turn drives investment in dedicated MEMS test infrastructure. Smart home devices, industrial IoT sensors, and connected medical equipment all rely on MEMS technology, necessitating rigorous wafer-level and package-level testing protocols. MEMS test cells equipped with multi-axis stimulus capabilities, thermal chambers, and high-speed data acquisition systems enable manufacturers to meet increasingly stringent quality benchmarks while maintaining throughput. This alignment between IoT growth and testing infrastructure investment represents one of the most consequential demand-side drivers shaping the market landscape.

➤ The automotive sector’s transition toward electrification and autonomous driving is creating a sustained, long-term demand signal for advanced MEMS test cells capable of validating inertial sensors and environmental sensing modules to automotive-grade reliability standards.

Healthcare and medical device applications are emerging as another critical demand driver for MEMS Test Cell Market. MEMS-based pressure sensors, flow sensors, and lab-on-chip diagnostic platforms used in point-of-care devices and implantable systems require compliance with stringent medical-grade testing protocols. This is prompting specialized test cell manufacturers to develop solutions tailored to biomedical MEMS, incorporating cleanroom compatibility, biocompatibility validation, and traceability features that align with regulatory frameworks such as ISO 13485 and FDA quality system regulations.

MARKET CHALLENGES

Complexity of Testing Heterogeneous MEMS Device Architectures

One of the most significant challenges confronting MEMS Test Cell Market is the inherent complexity of testing devices that combine mechanical, electrical, optical, and fluidic functions within a single package. Unlike standard semiconductor devices, MEMS components require multi-domain stimulus and measurement , applying pressure, vibration, magnetic fields, or acoustic signals simultaneously while capturing electrical responses with high fidelity. Designing test cells that can accommodate this heterogeneity without compromising accuracy or throughput demands substantial engineering investment and deep domain expertise, creating barriers particularly for smaller test equipment vendors and end-users with limited in-house capability.

Other Challenges

High Capital Expenditure and Total Cost of Ownership

MEMS test cells represent a significant capital investment, often requiring customized fixturing, environmental control systems, and application-specific hardware configurations. The total cost of ownership extends well beyond initial procurement to include calibration, maintenance, software upgrades, and the need for highly trained metrology engineers. For fabless MEMS design companies and mid-tier manufacturers, these cost structures can limit access to state-of-the-art test solutions, potentially impacting device quality and time-to-market competitiveness.

Standardization Gaps Across the MEMS Testing Ecosystem

The absence of universally adopted test standards specific to MEMS devices presents an ongoing challenge for both equipment suppliers and device manufacturers. While organizations such as SEMI and IEEE have developed guidelines, the diversity of MEMS form factors, operating principles, and end-use environments makes comprehensive standardization difficult. This fragmentation results in duplicated test development efforts, interoperability issues between test platforms, and inconsistent quality benchmarks across supply chains, ultimately adding complexity and cost to the MEMS device qualification process.

MARKET RESTRAINTS

Limited Availability of Skilled Metrology and MEMS Testing Expertise

A persistent restraint on MEMS Test Cell Market is the constrained talent pool of engineers and technicians with specialized expertise in MEMS metrology and test system development. Effective deployment and operation of MEMS test cells requires cross-disciplinary knowledge spanning semiconductor physics, mechanical engineering, RF characterization, and software integration. Global semiconductor industry’s broader talent shortage is particularly acute in this specialized domain, slowing adoption rates among organizations that lack established MEMS testing competencies and limiting the speed at which test cell solutions can be customized and deployed for new device generations.

Supply Chain Vulnerabilities and Long Lead Times for Precision Test Components

MEMS Test Cell Market is also constrained by supply chain vulnerabilities affecting precision test components such as high-bandwidth signal analyzers, environmental chambers, and custom probe cards. Global disruptions to electronics supply chains have extended lead times for critical subsystems, delaying the delivery and commissioning of new test cell installations. For manufacturers operating under aggressive product launch schedules, these delays translate directly into delayed qualification timelines and increased program risk. Furthermore, the specialized nature of many MEMS test cell components limits the number of qualified suppliers, reducing procurement flexibility and creating concentration risk within the supply base.

Intellectual property considerations also function as a restraint within MEMS Test Cell Market, particularly for vertically integrated device manufacturers who develop proprietary test methodologies as a source of competitive differentiation. The reluctance to share test know-how with third-party equipment providers can slow collaboration and limit the pace of test technology innovation. Additionally, export control regulations applicable to certain precision measurement and semiconductor manufacturing equipment may restrict market access in specific geographies, further constraining the addressable market for MEMS test cell vendors operating internationally.

MARKET OPPORTUNITIES

Integration of AI and Machine Learning to Enhance MEMS Test Cell Efficiency

The integration of artificial intelligence and machine learning algorithms into MEMS test cell platforms represents a compelling growth opportunity for the market. AI-driven test optimization can reduce test time by intelligently selecting the most discriminating test sequences, predicting device failure modes based on early-stage parametric data, and enabling adaptive testing that adjusts stimulus parameters in real time. These capabilities directly address the throughput and cost pressures facing high-volume MEMS manufacturers, making AI-enhanced test cells an attractive value proposition that is gaining traction among leading semiconductor OSATs and integrated device manufacturers.

Growth in MEMS-Based Medical and Wearable Device Markets Driving Specialized Test Demand

The accelerating development of MEMS-based wearable health monitoring devices, implantable sensors, and minimally invasive diagnostic tools is opening significant new opportunities for specialized MEMS test cell solutions. Medical-grade MEMS devices demand test protocols that validate long-term reliability, biocompatibility, and performance under physiological conditions , requirements that are driving demand for purpose-built test cell configurations. Vendors who can demonstrate regulatory alignment and offer validated test methodologies for medical MEMS applications are well positioned to capture premium market segments as healthcare digitization continues to expand globally.The ongoing buildout of advanced semiconductor fabrication capacity across North America, Europe, and Asia presents a structural opportunity for MEMS test cell suppliers. Government-backed initiatives to establish domestic chip manufacturing ecosystems are stimulating investment in the full spectrum of semiconductor production infrastructure, including front-end wafer-level test and back-end package test solutions. New MEMS-capable fabs and test facilities entering operation over the next several years will require comprehensive test cell deployments, creating a sustained pipeline of procurement opportunities. Vendors who establish early relationships with greenfield fab programs and offer scalable, modular test cell architectures are likely to benefit disproportionately from this investment cycle.

MEMS Test Cell Market Trends

Rising Demand for MEMS Device Validation Driving Growth in MEMS Test Cell Market

MEMS Test Cell Market is witnessing sustained momentum as the proliferation of Micro-Electro-Mechanical Systems across automotive, consumer electronics, medical devices, and industrial automation continues to accelerate. MEMS test cells are purpose-built equipment designed to evaluate the electrical, mechanical, and environmental performance of MEMS devices and sensors before integration into end products. As MEMS components become increasingly embedded in safety-critical applications such as automotive airbag systems and medical diagnostics, the need for rigorous and reliable test validation has become a non-negotiable step in the product development lifecycle. Manufacturers and OEMs alike are prioritizing test cell investments to ensure that MEMS devices meet precise performance specifications and regulatory standards prior to mass deployment.

Other Trends

Expansion Across Diverse Sensor Applications

MEMS Test Cell Market is experiencing broad adoption across a wide spectrum of sensor types, including accelerometers, gyroscopes, digital compasses, MEMS microphones, pressure sensors, and temperature sensors. Each of these applications demands tailored test methodologies, prompting test cell manufacturers to develop flexible and multi-parameter platforms capable of addressing varied testing requirements within a single system. The accelerometer and gyroscope segments, in particular, are among the most active application areas, driven by strong demand from consumer electronics manufacturers integrating motion-sensing capabilities into smartphones, wearables, and gaming devices. This diversification of end-use applications is broadening the addressable market for MEMS test cell providers and encouraging product innovation.

Throughput Optimization and UPH Segmentation as a Competitive Differentiator

Within MEMS Test Cell Market, throughput capacity has emerged as a key competitive parameter. Solutions segmented by Units Per Hour (UPH), notably the Up to 20K UPH and Up to 30K UPH categories, reflect the industry’s emphasis on balancing testing accuracy with production efficiency. High-volume semiconductor and MEMS manufacturers are increasingly seeking test cell platforms that can sustain throughput targets without compromising measurement precision, particularly as component volumes scale in line with growing sensor demand across automotive and IoT applications. Vendors offering scalable UPH configurations are gaining preference among large-scale manufacturers looking to minimize test bottlenecks in high-output production environments.

Competitive Landscape and Regional Market Development Shaping Future Trajectories

The competitive landscape of MEMS Test Cell Market is defined by a concentrated group of global players, including Advantest, Cohu, Inc., NI (SET GmbH), STATEC, SPEA S.p.A., and YTEC, who collectively held a significant share of global revenue as of 2025. These companies are actively investing in product development, strategic partnerships, and geographic expansion to strengthen their market positions. Regionally, North America and Asia , particularly China, Japan, and South Korea , represent the most significant markets, supported by established semiconductor manufacturing ecosystems and high concentrations of MEMS device producers. Europe also maintains a steady presence, driven by automotive-sector demand. As global MEMS production volumes continue to rise, MEMS Test Cell Market is expected to see sustained investment in next-generation test infrastructure across all major regions.

COMPETITIVE LANDSCAPE

Key Industry Players

MEMS Test Cell Market , Global Competitive Dynamics and Leading Manufacturer Profiles

Global MEMS Test Cell market, valued at approximately USD 174 million in 2025 and projected to reach USD 305 million by 2032 at a CAGR of 8.6%, is characterized by a moderately consolidated competitive landscape. Advantest and Cohu, Inc. stand out as dominant forces in this space, leveraging decades of semiconductor and MEMS test expertise, extensive global distribution networks, and strong R&D investment to maintain their leadership positions. These established players command a significant share of Global revenue, with the top five manufacturers collectively accounting for a substantial portion of the market in 2025. Their competitive edge is reinforced by continuous innovation in high-throughput test solutions , particularly in the Up to 20K UPH and Up to 30K UPH segments , as well as their ability to address a broad spectrum of MEMS device types including accelerometers, gyroscopes, MEMS microphones, pressure sensors, digital compasses, and temperature sensors across automotive, consumer electronics, medical, and industrial automation end markets.

Beyond the market leaders, a number of specialized and regional players contribute meaningfully to the competitive ecosystem. Companies such as NI (SET GmbH), SPEA S.p.A., STATEC, and YTEC have carved out strong niches by offering highly configurable and application-specific MEMS test platforms tailored to precision sensor validation requirements. SPEA S.p.A., an Italian engineering firm, is particularly recognized for its innovative automatic test equipment (ATE) solutions for inertial MEMS sensors, while NI (SET GmbH) brings modular instrumentation expertise to the MEMS testing domain. As MEMS device complexity increases and quality assurance requirements tighten across regulated industries such as automotive safety systems and medical diagnostics, these niche innovators are expected to intensify competition through strategic partnerships, product launches, and geographic expansion, further shaping the evolving competitive contours of Global MEMS Test Cell market.

List of Key MEMS Test Cell Companies Profiled

- Advantest

- Cohu, Inc.

- NI (SET GmbH)

- SPEA S.p.A.

- STATEC

- YTEC

- Teradyne

- Astronics Test Systems

- Rasco GmbH

- Multitest Electronic Systems

- Xcerra Corporation

- Aehr Test Systems

- Chroma ATE

- Amkor Technology

- National Instruments (NI)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Up to 30K UPH is the leading segment in MEMS Test Cell Market by throughput capacity, driven by the growing demand for high-volume production testing across semiconductor and consumer electronics manufacturing environments.

|

| By Application |

|

Accelerometer represents the dominant application segment within MEMS Test Cell Market, owing to its widespread deployment across automotive safety systems, consumer electronics, and industrial motion sensing platforms.

|

| By End User |

|

Automotive Industry stands as the leading end-user segment for MEMS Test Cells, driven by the extensive integration of MEMS-based sensors in modern vehicle architectures for safety, navigation, and performance monitoring.

|

| By Testing Methodology |

|

Wafer-Level Testing is the dominant methodology segment, as it enables manufacturers to identify and eliminate defective MEMS devices early in the production cycle, reducing overall manufacturing costs and improving yield rates significantly.

|

| By Automation Level |

|

Fully Automated Test Cells lead this segment as manufacturers across the MEMS value chain increasingly prioritize automation to meet rising production demands, ensure consistent test quality, and reduce dependency on skilled manual labor.

|

Regional Analysis: MEMS Test Cell Market

Asia-Pacific

China’s MEMS test cell market is fueled by ambitious semiconductor localization goals and a thriving consumer electronics manufacturing base. Domestic MEMS foundries are scaling rapidly, necessitating robust test cell infrastructure to meet both domestic demand and export quality standards. Government initiatives targeting self-reliance in chip production are directly translating into increased capital expenditure on advanced testing equipment and methodologies across the region.

Japan remains a cornerstone of MEMS test cell innovation, with leading instrumentation and equipment manufacturers continuously refining wafer-level test solutions. The country’s deep expertise in precision engineering and its strong automotive electronics sector create sustained demand for highly accurate MEMS testing. Japanese firms are particularly focused on developing test cell technologies suitable for automotive-grade MEMS sensors, where reliability requirements are exceptionally stringent.

South Korea and Taiwan host world-class semiconductor ecosystems that are increasingly integrating MEMS components into advanced packaging and system-on-chip solutions. This convergence is elevating the complexity of test cell requirements as manufacturers seek solutions capable of validating multi-functional MEMS devices. Both markets benefit from strong collaboration between foundries and test equipment suppliers, fostering continuous advancement in MEMS test cell capabilities.

Southeast Asian nations including Vietnam, Malaysia, and Thailand are emerging as significant players in MEMS Test Cell Market as multinational manufacturers diversify supply chains away from concentration risk. The establishment of new semiconductor assembly and test facilities across the sub-region is generating fresh demand for scalable and cost-effective MEMS test cell solutions, presenting attractive opportunities for global equipment suppliers throughout the forecast period.

North America

North America represents one of the most technologically advanced markets for MEMS test cell solutions, underpinned by its world-leading semiconductor design ecosystem, aerospace and defense sector, and rapidly expanding automotive electronics industry. The United States is home to numerous MEMS device designers and fabless companies that rely on sophisticated test cell infrastructure to validate increasingly complex sensor arrays and inertial measurement units. The region’s defense and aerospace applications impose exceptionally rigorous reliability standards, driving demand for MEMS test cell technologies capable of environmental stress screening and mission-critical performance validation. Additionally, the surge in advanced driver-assistance systems and autonomous vehicle development across North America is creating a strong pull for high-precision MEMS test environments. The presence of major semiconductor equipment manufacturers and a robust research university network ensures continuous innovation in test cell methodologies, keeping the region at the technological frontier of Global MEMS test cell market through 2034.

Europe

Europe occupies a strategically significant position in Global MEMS test cell market, characterized by its strong automotive electronics heritage, industrial automation sector, and commitment to semiconductor sovereignty through initiatives such as the European Chips Act. Germany, France, and the Netherlands are key markets where MEMS sensors are extensively deployed in automotive, industrial, and medical applications, each demanding rigorous testing protocols that drive investment in advanced test cell solutions. The European automotive industry’s transition toward electrification and intelligent mobility is accelerating MEMS adoption in safety-critical systems, further elevating test cell requirements. European research institutions and Fraunhofer-affiliated organizations play a pivotal role in advancing MEMS test methodologies, bridging academic innovation and commercial deployment. The region’s emphasis on quality standards and regulatory compliance ensures that MEMS test cell investments remain a strategic priority for manufacturers operating within the European market landscape.

South America

South America presents a gradually developing market for MEMS test cell solutions, with growth primarily anchored in Brazil and, to a lesser extent, Mexico and Argentina. The region’s expanding telecommunications infrastructure, growing automotive assembly sector, and increasing adoption of smart industrial systems are beginning to create demand for MEMS devices and, consequently, test cell capabilities. However, South America’s MEMS test cell market remains constrained by limited local semiconductor manufacturing capacity and the predominantly import-dependent nature of advanced electronic components. Investment in higher education and technology parks in Brazil is slowly building a foundational talent base capable of supporting MEMS technology development. Over the forecast period, gradual industrialization and foreign direct investment in electronics manufacturing are expected to provide incremental growth opportunities for MEMS test cell solution providers targeting the South American market.

Middle East & Africa

The Middle East and Africa region represents an early-stage but increasingly noteworthy market within Global MEMS test cell landscape. The Middle East, particularly the Gulf Cooperation Council countries, is investing heavily in smart city infrastructure, oil and gas automation, and defense modernization programs, all of which incorporate MEMS-enabled sensing technologies and consequently require reliable test validation frameworks. The United Arab Emirates and Saudi Arabia are emerging as regional technology hubs with ambitions to develop domestic semiconductor and electronics manufacturing capabilities, which could incrementally boost demand for MEMS test cell solutions. Africa’s contribution to the market remains nascent, primarily reflecting adoption of MEMS-integrated consumer devices rather than indigenous manufacturing activity. Nonetheless, as telecommunications networks expand and industrial digitization accelerates across both sub-regions, the Middle East and Africa are poised to become progressively more relevant participants in Global MEMS test cell market through the 2026 to 2034 forecast window.

Report Scope

This market research report provides a comprehensive analysis of MEMS Test Cell Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MEMS Test Cell Market?

-> Global MEMS Test Cell Market was valued at USD 174 million in 2025 and is projected to reach USD 305 million by 2032, growing at a CAGR of 8.6% during the forecast period.

Which key companies operate in MEMS Test Cell Market?

-> Key players include Advantest, Cohu, Inc., NI (SET GmbH), STATEC, SPEA S.p.A., and YTEC, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for MEMS-enabled devices in automotive applications (e.g., airbag sensors), growing adoption of consumer electronics incorporating accelerometers and gyroscopes, expansion of medical devices using MEMS technology, and increasing industrial automation requiring reliable MEMS sensor validation.

Which region dominates the market?

-> Asia is a key growth region driven by strong manufacturing activity in China, Japan, South Korea, and Southeast Asia, while North America remains a significant market with the U.S. representing a major share of global MEMS Test Cell demand.

What are the emerging trends?

-> Emerging trends include higher throughput test solutions (Up to 20K UPH and Up to 30K UPH segments), increased testing complexity for multi-function MEMS sensors such as digital compasses and MEMS microphones, and growing integration of automated test environments to support expanding MEMS device portfolios across pressure, temperature, and inertial sensor applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...