MARKET INSIGHTS

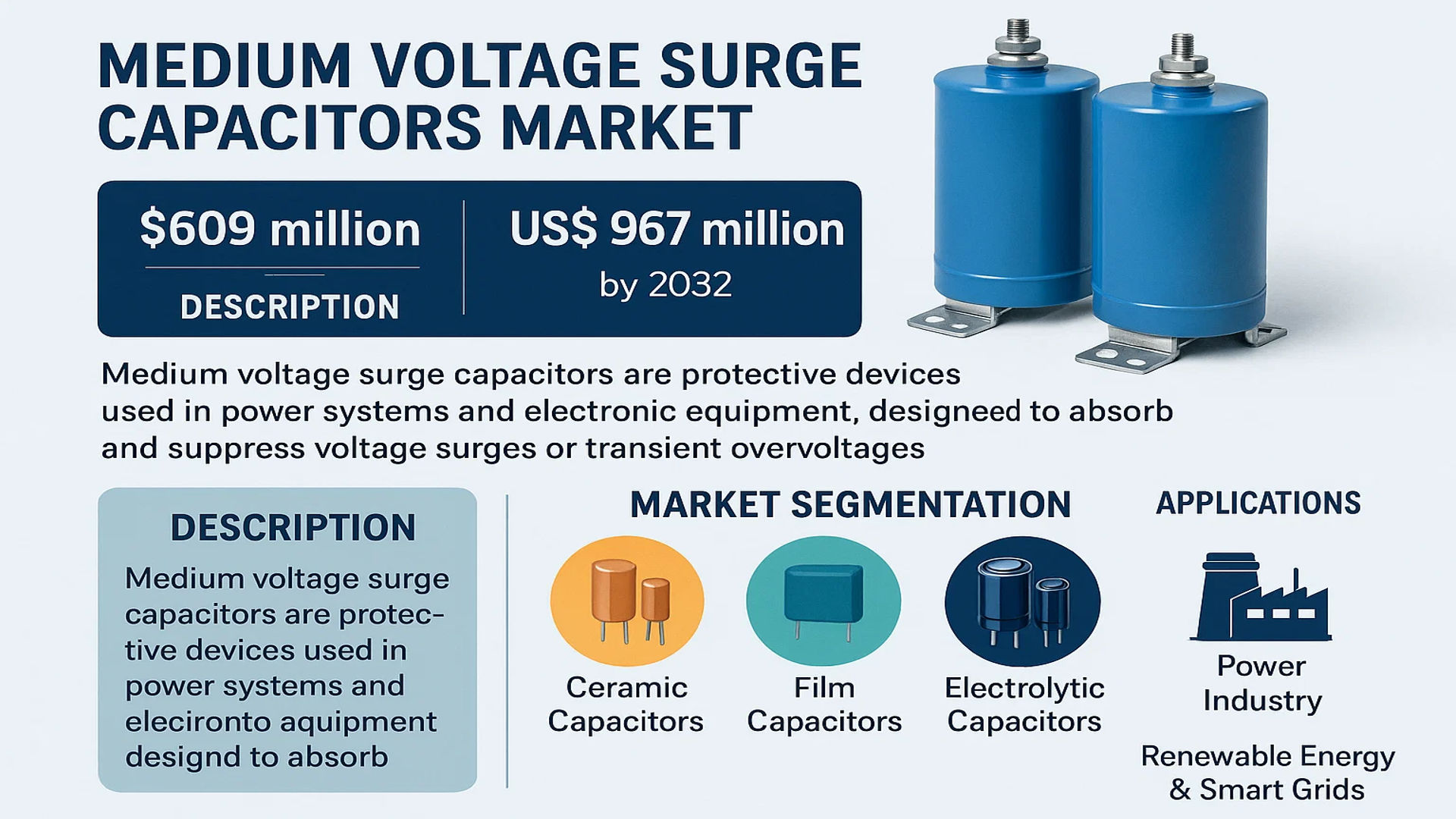

The global Medium Voltage Surge Capacitors Market was valued at 609 million in 2024 and is projected to reach US$ 967 million by 2032, at a CAGR of 6.8% during the forecast period.

Medium voltage surge capacitors are protective devices used in power systems and electronic equipment, designed to absorb and suppress voltage surges or transient overvoltages. These components play a critical role in safeguarding equipment from damage caused by lightning strikes, switching operations, or faults. With an operating voltage range typically between 1 kV and 36 kV, they are characterized by high voltage tolerance, low energy loss, and extended operational lifespan. The market segmentation includes ceramic capacitors, film capacitors, and electrolytic capacitors, with ceramic capacitors expected to witness significant growth due to their superior performance in high-voltage applications.

While the power industry remains the dominant application segment, the market is seeing increased adoption in emerging sectors like renewable energy and smart grids. Key players such as Siemens Energy, TDK Electronics, and Hitachi Energy are driving innovation through strategic collaborations and product enhancements. For instance, recent developments in advanced materials have improved capacitor efficiency, addressing the growing demand for reliable power protection solutions in industrial and commercial infrastructure projects.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Renewable Energy Projects Accelerate Demand for Medium Voltage Surge Capacitors

The global transition toward renewable energy is driving substantial growth in the medium voltage surge capacitors market. As wind and solar power installations expand, their sensitive electrical components require robust protection against voltage fluctuations caused by environmental factors and grid integration challenges. Recent data indicates that renewable energy capacity additions reached over 340 GW globally in recent years, creating parallel demand for protective devices. Surge capacitors play a critical role in mitigating transient overvoltages in solar inverters, wind turbine converters, and energy storage systems, ensuring operational reliability.

Grid Modernization Initiatives Worldwide Fuel Market Expansion

Government-led grid infrastructure modernization programs are significantly contributing to market growth. Aging power infrastructure in developed economies and rapid electrification in emerging markets necessitate upgraded protection systems. Medium voltage surge capacitors are increasingly specified in smart grid projects, substation upgrades, and distribution network expansions. Investments in grid modernization are projected to exceed $600 billion globally by 2030, with substantial portions allocated to protective equipment. The enhanced focus on grid resilience following extreme weather events further emphasizes the importance of reliable surge protection solutions.

Industrial Automation Boom Creates New Application Areas

The rapid advancement of Industry 4.0 technologies is generating additional demand for medium voltage surge protection. As factories increasingly incorporate sensitive electronic controls, robotics, and IoT devices, protection against electrical transients becomes paramount. Medium voltage surge capacitors are being adopted in motor drives, PLC systems, and process control equipment across manufacturing facilities. The industrial automation market is growing at approximately 8-10% annually, with corresponding increases in protective component requirements. Recent product developments focusing on compact designs and higher reliability specifically for industrial applications are further stimulating market uptake.

➤ The integration of surge capacitors with predictive maintenance systems represents a significant technological advancement, allowing for real-time monitoring of capacitor health and surge events.

MARKET RESTRAINTS

High Initial Costs and Budget Constraints Limit Adoption in Developing Regions

While medium voltage surge capacitors offer long-term protection benefits, their upfront costs present a significant barrier to widespread adoption, particularly in price-sensitive markets. Premium-grade surge capacitors incorporating advanced materials and monitoring capabilities can cost several times more than basic protective devices. This pricing differential becomes particularly challenging in developing economies where infrastructure projects face tight budget constraints. Additionally, the total cost of ownership considerations, including installation and maintenance, further complicates procurement decisions for many utilities and industrial operators.

Technical Complexity in High-Density Applications Creates Implementation Challenges

The increasing power density in modern electrical systems presents unique technical challenges for surge capacitor deployment. As equipment becomes more compact and operates at higher efficiencies, traditional surge protection solutions may not always integrate seamlessly. Space constraints in substations, switchgear, and power electronic cabinets often require custom capacitor solutions, increasing project complexity and lead times. Furthermore, the need to maintain consistent performance across varying environmental conditions and load profiles demands sophisticated design approaches, potentially slowing implementation timelines.

Supply Chain Disruptions Impact Component Availability

Recent global supply chain challenges have affected the availability of key materials used in medium voltage surge capacitors. Specialized dielectric materials, high-grade metallization, and precision components face periodic shortages, leading to extended delivery times. The industry’s reliance on select suppliers for critical materials creates vulnerabilities in production continuity. These supply chain constraints are particularly problematic for projects with fixed commissioning schedules, where delays in protective equipment delivery can impact entire project timelines.

MARKET OPPORTUNITIES

Emerging HVDC Transmission Projects Create New Growth Avenues

The expansion of high-voltage direct current (HVDC) transmission networks presents significant opportunities for medium voltage surge capacitor manufacturers. As countries invest in long-distance power transmission and grid interconnections, the need for specialized surge protection in converter stations and along transmission routes grows substantially. HVDC projects often incorporate multiple medium voltage levels within their architecture, each requiring tailored protection solutions. With the global HVDC market projected to maintain strong growth, manufacturers developing application-specific surge capacitors stand to benefit considerably.

Electric Vehicle Charging Infrastructure Demands Advanced Protection

The rapid deployment of high-power EV charging stations creates a promising new application area for medium voltage surge capacitors. Fast chargers operating at medium voltage levels require robust protection against both conducted and radiated electrical disturbances. As charging networks expand to support the anticipated growth in electric vehicles, the associated surge protection market is expected to grow proportionally. Manufacturers developing compact, high-reliability capacitor solutions specifically for charging infrastructure are well-positioned to capitalize on this emerging segment.

Smart City Developments Drive Innovative Protection Solutions

Global smart city initiatives are generating demand for next-generation surge protection integrating IoT capabilities. Medium voltage surge capacitors with embedded sensors and communication interfaces enable predictive maintenance and real-time performance monitoring, aligning with smart grid objectives. These intelligent protection systems are particularly valuable in urban environments where reliability requirements are stringent and outage impacts are significant. The convergence of surge protection with digital monitoring technologies represents a substantial growth opportunity, especially in regions prioritizing smart infrastructure development.

MARKET CHALLENGES

Standardization Gaps Hinder Widespread Adoption

The medium voltage surge capacitor market faces challenges related to inconsistent standards across regions and applications. While international standards exist for basic performance parameters, implementation guidelines often vary between utilities and industries. These discrepancies create complexity for manufacturers developing products for global markets and can delay project approvals. The lack of uniform testing and certification processes across jurisdictions adds another layer of complexity, potentially restricting market growth until greater harmonization emerges.

Technical Limitations in Extreme Operating Conditions

Certain industrial and utility applications push medium voltage surge capacitors to their performance limits. Harsh environments featuring extreme temperatures, high humidity, salt spray, or chemical exposure can accelerate degradation of capacitor components. Similarly, applications with frequent surge events or continuous harmonic distortion present durability challenges. While material science advancements have improved capacitor resilience, there remains ongoing demand for solutions capable of withstanding increasingly demanding operating conditions without compromising protection effectiveness or service life.

Competition from Alternative Protection Technologies

Medium voltage surge capacitors face competition from emerging protection technologies, including advanced metal-oxide varistors and hybrid protection devices. These alternatives sometimes offer advantages in terms of response time, energy handling capacity, or form factor for specific applications. While surge capacitors maintain distinct benefits for many use cases, the evolving competitive landscape requires continuous innovation to maintain market position. Manufacturers must carefully balance performance improvements with cost considerations to remain competitive against alternative protection solutions.

MEDIUM VOLTAGE SURGE CAPACITORS MARKET TRENDS

Increasing Renewable Energy Integration to Drive Market Growth

The global transition toward renewable energy has accelerated the demand for medium voltage surge capacitors, particularly in solar and wind power applications. Capacitors play a critical role in stabilizing power grids by mitigating voltage fluctuations caused by intermittent renewable energy sources. In 2024, renewable energy accounted for approximately 30% of global electricity generation, reinforcing the need for robust surge protection solutions. The rise in distributed energy resources, including microgrids and hybrid systems, has further intensified the deployment of medium voltage surge capacitors to enhance grid reliability and reduce equipment failure rates.

Other Trends

Smart Grid Infrastructure Expansion

The modernization of power grids, particularly in developed economies, is fueling demand for advanced surge protection systems. Governments worldwide are investing heavily in smart grid technologies, with global spending expected to surpass $100 billion annually by 2030. These investments prioritize grid resilience, where medium voltage surge capacitors serve as essential components in substations and transmission networks. The integration of IoT-enabled monitoring systems has also improved predictive maintenance for these capacitors, ensuring prolonged operational efficiency.

Growing Industrial Automation and Electrification

The rapid electrification of industrial processes and increasing automation in manufacturing are creating substantial opportunities for medium voltage surge capacitor suppliers. Industries such as automotive, steel, and semiconductor manufacturing rely on precise power conditioning to prevent costly disruptions from voltage spikes. For instance, semiconductor fabs experience annual losses exceeding $10 billion due to power-related outages, making surge protection indispensable. Additionally, government mandates for energy-efficient industrial equipment are pushing manufacturers to adopt capacitors with higher energy absorption capabilities and lower losses.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansions and Innovation Drive Market Competition

The global Medium Voltage Surge Capacitors Market features a dynamic competitive landscape, with a mix of established multinational corporations and specialized regional players. Siemens Energy and Hitachi Energy dominate the market, leveraging their extensive expertise in power systems and strong global distribution networks. These industry giants collectively held a significant revenue share in 2024, driven by their comprehensive product portfolios and strategic investments in emerging markets.

Meanwhile, TDK Electronics and Eaton have been gaining traction through continuous technological advancements, particularly in ceramic and film capacitor segments. Their focus on R&D has enabled them to introduce high-efficiency surge protection solutions for renewable energy and smart grid applications, creating competitive differentiation.

Regional players such as HILKAR and ZEZ SILKO are strengthening their positions through cost-effective manufacturing and localized supply chains. Their ability to cater to specific regional requirements in Asia and Europe provides them with a competitive edge in price-sensitive markets.

The market is witnessing increased competition as companies expand through mergers, acquisitions, and partnerships. For instance, ABB recently enhanced its surge protection portfolio by acquiring specialized manufacturers, while Mitsubishi Electric has been investing in next-generation capacitor technologies to address growing demand from the transportation sector.

List of Key Medium Voltage Surge Capacitor Manufacturers

- Siemens Energy (Germany)

- TDK Electronics (Germany)

- HILKAR (Turkey)

- Surge Components (U.S.)

- Hitachi Energy (Japan)

- Eaton (Ireland)

- Mitsubishi Electric (Japan)

- GE Vernova (U.S.)

- Magnewin Energy Pvt.Ltd. (India)

- Marxelec (China)

- Bree (Germany)

- Ducati Energia (Italy)

- ELECTRONICON (Germany)

- ZEZ SILKO (Slovakia)

- ABB (Switzerland)

Segment Analysis:

By Type

Ceramic Capacitors Segment Dominates Due to High Durability and Energy Efficiency

The market is segmented based on type into:

- Ceramic Capacitors

- Film Capacitors

- Electrolytic Capacitors

By Application

Power Industry Segment Leads Due to Critical Need for Voltage Protection

The market is segmented based on application into:

- Power Industry

- Communication Industry

- New Energy Industry

- Transportation Industry

By Voltage Range

1kV-10kV Segment Holds Significant Market Share for Industrial Applications

The market is segmented based on voltage range into:

- 1kV-10kV

- 10kV-20kV

- 20kV-36kV

By End User

Utilities Segment Dominates Due to Large-Scale Power Infrastructure Requirements

The market is segmented based on end user into:

- Utilities

- Industrial

- Commercial

- Residential

Regional Analysis: Medium Voltage Surge Capacitors Market

Asia-Pacific

The Asia-Pacific region dominates the global medium voltage surge capacitors market, accounting for approximately 42% of revenue share in 2024. This leadership position is driven by rapid industrialization, expanding power infrastructure, and increasing investments in renewable energy projects across China, India, and Southeast Asia. China alone contributes more than 60% of regional demand due to massive grid modernization initiatives and the world’s largest high-voltage transmission network. The region exhibits strong preference for cost-effective ceramic capacitors, though Japanese manufacturers like TDK Electronics and Mitsubishi Electric are driving innovation in high-efficiency film capacitors. Ongoing smart grid deployments and urbanization projects ensure sustained growth, with India’s UDAY scheme and China’s 14th Five-Year Plan providing additional momentum.

North America

North America represents the second-largest market, characterized by stringent electrical safety standards and aging infrastructure replacement programs. The U.S. accounts for 78% of regional demand, where Eaton and GE Vernova lead in supplying capacitors for utility-scale applications. The Infrastructure Investment and Jobs Act has allocated $73 billion for power infrastructure upgrades, creating robust demand for surge protection solutions. Medium voltage applications are increasingly shifting toward smart capacitor banks with IoT capabilities, particularly in renewable energy integration projects. Canada’s focus on grid resilience against extreme weather events further propels market growth, with ceramic capacitors remaining predominant due to their reliability in harsh conditions.

Europe

Europe’s mature market is driven by renewable energy expansion and strict EU directives on power quality (EN 50522). Germany and France collectively hold over 50% market share, with Siemens Energy and ABB being key suppliers for industrial and utility applications. The region shows strong preference for environmentally sustainable film capacitors, aligned with circular economy principles. Eastern European countries are emerging as growth hotspots due to grid interconnection projects and increasing FDI in energy infrastructure. The REPowerEU plan’s emphasis on energy independence is accelerating capacitor deployments in solar and wind farms, though supply chain disruptions remain a challenge for local manufacturers.

South America

South America presents moderate growth opportunities, with Brazil constituting 65% of regional demand. Mining operations and hydropower plants generate steady demand for rugged surge protection solutions. However, economic volatility and inadequate grid infrastructure in rural areas constrain market expansion. Argentina shows potential with recent Vaca Muerta shale gas developments requiring specialized capacitor banks. Local manufacturers face intense competition from Chinese imports, though Ducati Energia maintains strong presence in industrial applications. The region’s growth is further hindered by limited technical expertise in advanced surge protection technologies.

Middle East & Africa

This region demonstrates nascent but promising growth, led by GCC countries’ investments in smart cities and renewable energy. Saudi Arabia accounts for 40% of regional demand, driven by NEOM and other gigaprojects requiring advanced power conditioning solutions. South Africa remains the second-largest market, though hampered by Eskom’s financial challenges. The region shows increasing preference for hybrid capacitor solutions that combine surge protection with power factor correction. While market penetration remains low compared to global standards, growing electrification rates and oil-to-power diversification strategies suggest long-term potential, particularly for medium voltage applications in oil/gas and desalination plants.

Report Scope

This market research report provides a comprehensive analysis of the Global Medium Voltage Surge Capacitors Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 609 million in 2024 and is projected to reach USD 967 million by 2032 at a CAGR of 6.8%.

- Segmentation Analysis: Detailed breakdown by product type (Ceramic Capacitors, Film Capacitors, Electrolytic Capacitors), application (Power Industry, Communication Industry, New Energy Industry, Transportation Industry), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific showing the highest growth potential.

- Competitive Landscape: Profiles of leading market participants including Siemens Energy, TDK Electronics, Hitachi Energy, Eaton, and Mitsubishi Electric, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging capacitor technologies, material advancements, and integration with smart grid systems.

- Market Drivers & Restraints: Evaluation of factors such as increasing power infrastructure investments, renewable energy adoption, and grid modernization, along with supply chain challenges and raw material price volatility.

- Stakeholder Analysis: Strategic insights for capacitor manufacturers, power utilities, system integrators, and investors regarding market opportunities and challenges.

The report employs both primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Medium Voltage Surge Capacitors Market?

-> Medium Voltage Surge Capacitors Market was valued at 609 million in 2024 and is projected to reach US$ 967 million by 2032, at a CAGR of 6.8% during the forecast period.

Which key companies operate in this market?

-> Key players include Siemens Energy, TDK Electronics, Hitachi Energy, Eaton, Mitsubishi Electric, GE Vernova, and ABB.

What are the key growth drivers?

-> Growth is driven by increasing power infrastructure investments, renewable energy integration, and demand for grid reliability solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing market, while North America and Europe remain significant markets due to grid modernization initiatives.

What are the emerging trends?

-> Emerging trends include development of eco-friendly capacitors, integration with smart grid technologies, and miniaturization of components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...