MARKET INSIGHTS

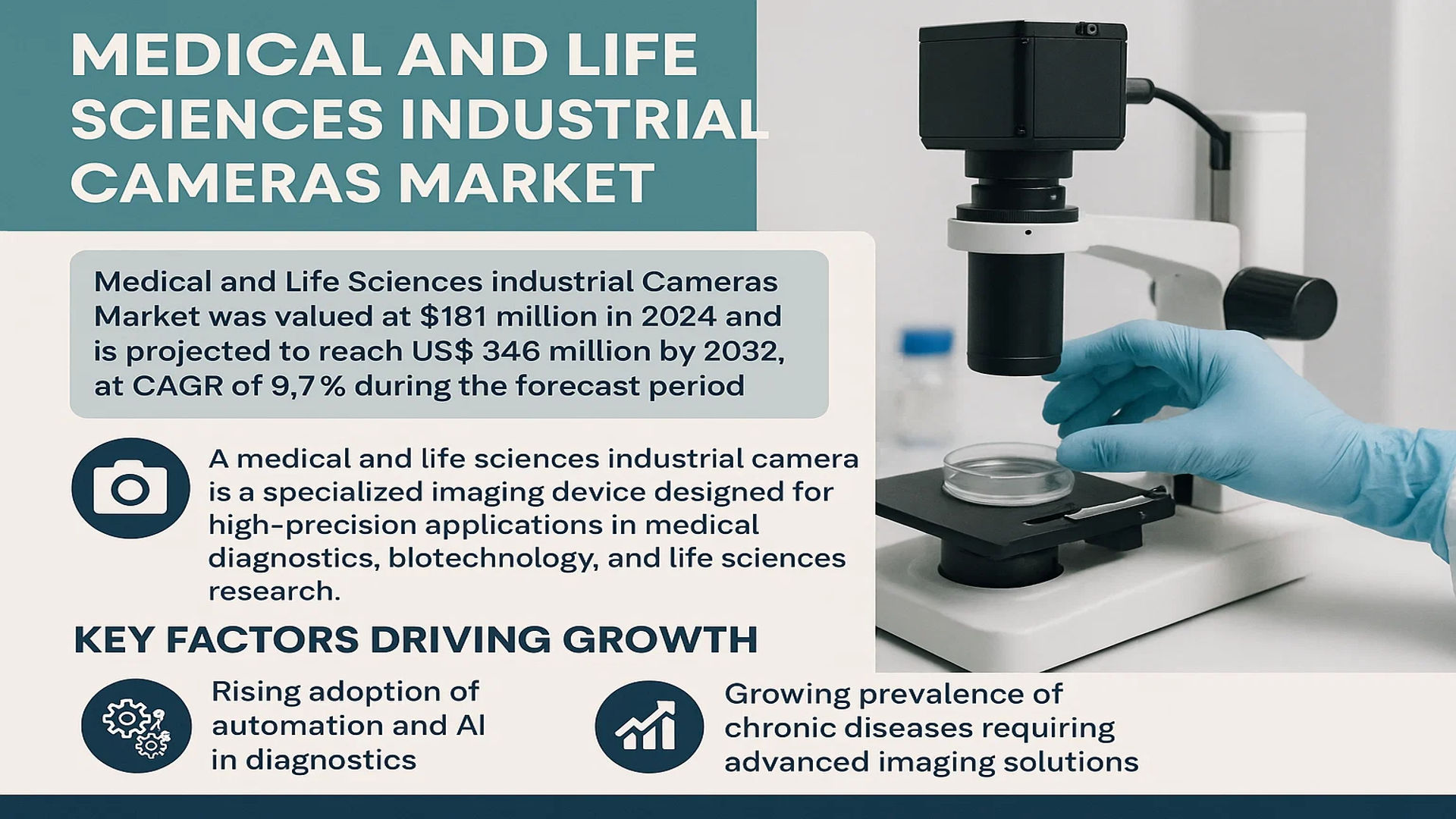

The global Medical and Life Sciences Industrial Cameras Market was valued at 181 million in 2024 and is projected to reach US$ 346 million by 2032, at a CAGR of 9.7% during the forecast period.

A medical and life sciences industrial camera is a specialized imaging device designed for high-precision applications in medical diagnostics, biotechnology, and life sciences research. These cameras provide high-resolution imaging, exceptional color accuracy, and advanced sensor technology to capture detailed biological and medical images. They are integral to processes in microscopy, digital pathology, ophthalmology, endoscopy, fluorescence imaging, and biomedical research.

The market is experiencing robust growth driven by several key factors, including the rising adoption of automation and AI in diagnostics, increasing investment in biomedical research, and the growing prevalence of chronic diseases requiring advanced imaging solutions. Furthermore, technological advancements in sensor design and the integration of machine learning for real-time image analysis are significantly contributing to market expansion. For instance, in 2023, Teledyne Technologies introduced a new series of high-sensitivity cameras with enhanced quantum efficiency for low-light fluorescence applications, catering to the expanding needs of research laboratories. Keyence, Cognex Corporation, and Basler AG are among the leading players operating in this market with extensive product portfolios.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Digital Pathology and AI Integration to Accelerate Market Expansion

The global shift toward digital pathology is significantly driving the demand for high-performance industrial cameras in medical and life sciences applications. Digital pathology systems require cameras capable of capturing ultra-high-resolution images of tissue samples for accurate diagnosis and telepathology. The integration of artificial intelligence and machine learning algorithms with these imaging systems has enhanced automated image analysis, pattern recognition, and diagnostic efficiency. The global digital pathology market has demonstrated robust growth, with an estimated compound annual growth rate exceeding 11% over the past five years, directly influencing camera demand. Furthermore, regulatory approvals for AI-based diagnostic systems have created substantial opportunities for camera manufacturers. For instance, recent approvals of AI-powered digital pathology platforms have accelerated the replacement of traditional microscopy with digital imaging systems, requiring advanced cameras with resolution capabilities exceeding 20 megapixels and frame rates optimized for whole-slide imaging.

Increasing Demand for Minimally Invasive Surgical Procedures to Fuel Camera Implementation

The growing preference for minimally invasive surgeries across various medical specialties is driving substantial demand for specialized endoscopic and surgical cameras. These procedures require cameras that provide exceptional image quality, real-time processing, and compatibility with sterilization protocols. The global minimally invasive surgical equipment market has experienced consistent growth, with endoscopic applications accounting for approximately 35% of the total market share. Medical industrial cameras designed for these applications feature advanced sensor technology, typically CMOS or CCD sensors with resolutions ranging from 4K to 8K, along with enhanced color reproduction capabilities. The expansion of robotic-assisted surgery platforms has further accelerated the need for precision imaging systems, with camera requirements including 3D imaging capabilities, minimal latency, and compatibility with augmented reality visualization systems. This trend is particularly evident in cardiovascular, orthopedic, and gastrointestinal surgical applications where imaging precision directly impacts procedural outcomes.

Advancements in Biomedical Research and Drug Discovery to Stimulate Market Growth

Biomedical research institutions and pharmaceutical companies are increasingly utilizing advanced imaging systems equipped with industrial cameras for drug discovery and development processes. These applications require cameras capable of capturing high-speed biological processes, fluorescence imaging, and real-time cellular analysis. The global investment in life sciences research and development has shown consistent annual growth, with imaging technologies representing a significant portion of capital equipment expenditures. Modern research cameras feature specialized capabilities including high quantum efficiency for low-light applications, precise temperature control for sensitive biological samples, and compatibility with automated laboratory systems. The development of high-content screening systems in pharmaceutical research has particularly driven demand for cameras with rapid frame rates exceeding 100 frames per second and resolution capabilities optimized for multi-well plate imaging. These technological requirements have pushed manufacturers to develop cameras specifically designed for research applications, creating sustained market growth opportunities.

MARKET CHALLENGES

High Implementation Costs and Budget Constraints to Impede Market Penetration

The medical and life sciences industrial camera market faces significant challenges related to the high costs associated with advanced imaging systems. These cameras incorporate sophisticated sensor technology, specialized optics, and complex image processing capabilities that substantially increase manufacturing expenses. The average cost of a medical-grade industrial camera can range from several thousand to tens of thousands of dollars, depending on resolution, frame rate, and specialized features. Healthcare institutions and research facilities often operate under constrained budgets, making capital investments in high-end imaging systems challenging. Additionally, the total cost of ownership includes not only the initial purchase but also maintenance, software licensing, and potential system integration expenses. This financial barrier is particularly pronounced in developing regions and smaller research institutions, where budget limitations may delay or prevent the adoption of advanced imaging technologies.

Other Challenges

Stringent Regulatory Compliance Requirements

Medical and life sciences cameras must comply with rigorous regulatory standards and certification processes across different regions. These include FDA regulations in the United States, CE marking in Europe, and other regional medical device approvals. The certification process can be time-consuming and expensive, often requiring extensive clinical validation and quality management system implementation. Regulatory requirements continue to evolve, particularly concerning software integration and cybersecurity aspects of connected medical devices.

Technical Integration Complexities

Integrating industrial cameras with existing medical systems and laboratory equipment presents significant technical challenges. Compatibility issues with legacy systems, data format standardization, and network infrastructure requirements can complicate implementation. The need for specialized IT support and ongoing technical maintenance adds layers of complexity that may deter potential users from adopting advanced imaging solutions.

MARKET RESTRAINTS

Data Management and Storage Limitations to Constrain Market Development

The increasing resolution and frame rates of medical industrial cameras generate enormous volumes of imaging data, creating significant challenges in data management, storage, and processing. A single high-resolution medical image can require storage capacity exceeding 500 megabytes, while continuous imaging applications may generate terabytes of data daily. Healthcare institutions face substantial infrastructure investments to handle this data deluge, including high-capacity storage systems, robust network infrastructure, and advanced data processing capabilities. The requirements for data retention compliance, particularly in clinical applications where images must be stored for extended periods according to regulatory guidelines, further compound these challenges. Additionally, the need for rapid image retrieval and processing in diagnostic applications demands sophisticated data management solutions that can be costly to implement and maintain.

Furthermore, data security concerns and privacy regulations impose additional constraints on medical imaging systems. The transmission and storage of patient-related imaging data must comply with strict privacy protection standards, requiring encrypted storage solutions and secure network protocols. These requirements add complexity and cost to imaging system implementations, potentially slowing adoption rates in resource-constrained environments.

MARKET OPPORTUNITIES

Emerging Applications in Telemedicine and Remote Diagnostics to Create Growth Prospects

The rapid expansion of telemedicine and remote diagnostic services presents substantial opportunities for medical industrial camera manufacturers. The global telemedicine market has demonstrated exceptional growth patterns, with adoption rates increasing significantly across various medical specialties. Remote diagnostic applications require high-quality imaging capabilities for dermatology, ophthalmology, radiology, and pathology consultations. Medical cameras designed for these applications must provide clinical-grade image quality while maintaining compatibility with telemedicine platforms and electronic health record systems. The development of specialized cameras for home-based medical monitoring and mobile health applications represents an additional growth avenue. These opportunities are particularly relevant in underserved regions and for chronic disease management programs where remote monitoring can significantly improve patient outcomes.

Additionally, the integration of medical cameras with IoT devices and cloud-based analytics platforms opens new possibilities for preventive healthcare and population health management. The ability to collect and analyze medical imaging data across large patient populations enables advanced pattern recognition and early disease detection capabilities. This convergence of imaging technology with big data analytics creates opportunities for camera manufacturers to develop solutions specifically optimized for large-scale medical data collection and analysis.

MEDICAL AND LIFE SCIENCES INDUSTRIAL CAMERAS MARKET TRENDS

Integration of Artificial Intelligence and Machine Learning to Emerge as a Dominant Trend

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally reshaping the capabilities and applications of industrial cameras in the medical and life sciences sectors. These technologies are moving beyond simple image capture to enable sophisticated, real-time image analysis, automated diagnostics, and predictive analytics. For instance, in digital pathology, AI-powered cameras can automatically detect and classify cancerous cells with an accuracy exceeding 95%, significantly reducing diagnostic time and human error. This trend is accelerating due to the vast amounts of imaging data generated in modern research and clinical settings, which require advanced computational power to process effectively. The demand for cameras with on-board processing capabilities that can run complex AI algorithms directly on the device is surging, as this reduces latency and ensures data security by minimizing reliance on external cloud servers. This shift towards intelligent imaging systems is a primary driver behind the projected market growth.

Other Trends

Rise of High-Throughput Screening and Automation

The expansion of high-throughput screening (HTS) in drug discovery and genomics is creating a substantial demand for high-speed, high-resolution industrial cameras. These systems require cameras capable of capturing thousands of images per second with exceptional clarity to analyze cellular reactions, protein interactions, and genetic material efficiently. The global push towards automating laboratory processes to increase reproducibility and speed is a key factor here. Automated systems integrated with advanced area scan and line scan cameras are now standard in pharmaceutical R&D, enabling the rapid analysis of compound libraries that can exceed several million samples. This trend is directly linked to the increasing R&D expenditure in the biopharmaceutical sector, which is estimated to grow annually, further fueling the need for sophisticated imaging solutions that can keep pace with automated workflows.

Advancements in Minimally Invasive Surgical Procedures

The rapid advancement of minimally invasive surgical (MIS) techniques, including robotic-assisted surgery, endoscopy, and laparoscopy, is a major catalyst for innovation in medical industrial cameras. These procedures rely on cameras to provide surgeons with a clear, magnified, and real-time view of the operative field. The current trend is towards cameras that offer higher resolutions, such as 4K and beyond, improved color fidelity, and enhanced 3D imaging capabilities. Furthermore, the miniaturization of camera sensors allows for their integration into increasingly smaller surgical instruments, enabling access to previously hard-to-reach anatomical areas. The global minimally invasive surgery market’s consistent growth directly correlates with the increased adoption of these advanced imaging systems, as improved visual guidance is paramount for surgical precision and patient safety.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Technological Innovation and Strategic Alliances to Secure Market Position

The global medical and life sciences industrial cameras market exhibits a fragmented yet dynamic competitive structure, characterized by the presence of established multinational corporations, specialized technology providers, and emerging innovators. While the market is populated by numerous players, a handful of companies have established significant influence through technological leadership, extensive distribution networks, and deep-rooted relationships with research institutions and healthcare providers. Teledyne Technologies Inc. stands as a dominant force, largely due to its comprehensive portfolio of high-performance scientific imaging solutions, including its acclaimed DALSA and FLIR brands, which are integral to advanced microscopy and diagnostic systems worldwide.

Basler AG and Sony Corporation also command substantial market shares, a position reinforced by their relentless focus on sensor innovation and image quality. Basler’s ace 2 and pulse series cameras are widely adopted in automated laboratory and diagnostic equipment, while Sony’s cutting-edge CMOS sensors set the industry standard for low-light sensitivity and resolution in demanding applications like fluorescence imaging. The growth trajectory of these companies is intrinsically linked to their ability to anticipate and meet the evolving needs of precision medicine and automated research workflows.

Furthermore, strategic initiatives such as mergers, acquisitions, and partnerships are pivotal for market expansion. For instance, recent acquisitions by key players have been aimed at integrating artificial intelligence and machine learning capabilities directly into camera firmware, creating smarter imaging systems that offer real-time analytics. These moves are expected to significantly consolidate market positions and drive value-added growth over the coming years.

Concurrently, companies like Cognex Corporation and Omron Corporation are strengthening their foothold by targeting specific application segments. Cognex’s deep expertise in machine vision is being tailored for pharmaceutical packaging inspection and lab automation, whereas Omron is focusing on developing compact, robust cameras for integrated medical devices. Their strategy involves significant R&D investment in enhancing data throughput and compatibility with laboratory information management systems (LIMS), ensuring their products remain indispensable in modernized healthcare and research environments.

List of Key Medical and Life Sciences Industrial Camera Companies Profiled

- Teledyne Technologies Inc. (U.S.)

- Basler AG (Germany)

- Sony Corporation (Japan)

- Cognex Corporation (U.S.)

- Keyence Corporation (Japan)

- IDS Imaging Development Systems GmbH (Germany)

- JAI A/S (Denmark)

- Omron Corporation (Japan)

- Baumer Holding AG (Switzerland)

Segment Analysis:

By Type

Area Scan Cameras Segment Dominates the Market Due to Their Versatility in High-Resolution Imaging Applications

The market is segmented based on type into:

- Area Scan Camera

- Subtypes: CCD (Charge-Coupled Device) and CMOS (Complementary Metal-Oxide-Semiconductor)

- Line Scan Camera

- 3D Cameras

- Infrared (IR) Cameras

- Others

By Application

Clinical Diagnosis Segment Leads Due to Critical Role in Medical Imaging and Diagnostic Procedures

The market is segmented based on application into:

- Clinical Diagnosis

- Sub-applications: Digital Pathology, Endoscopy, Ophthalmology

- Drug R&D

- Biological Research

- Sub-applications: Microscopy, Fluorescence Imaging, Cell Analysis

- Others

By Technology

CMOS Technology Gains Prominence Owing to Lower Power Consumption and Higher Integration Capabilities

The market is segmented based on technology into:

- CCD (Charge-Coupled Device)

- CMOS (Complementary Metal-Oxide-Semiconductor)

- sCMOS (Scientific CMOS)

By End User

Hospitals and Diagnostic Centers Represent the Largest End-User Segment Driven by Increasing Diagnostic Imaging Volumes

The market is segmented based on end user into:

- Hospitals and Diagnostic Centers

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutions

- Others

Regional Analysis: Medical and Life Sciences Industrial Cameras Market

North America

North America represents a mature and technologically advanced market, characterized by stringent regulatory oversight from the U.S. FDA and Health Canada, which drives demand for high-precision, compliant imaging solutions. The region’s dominance is fueled by substantial investments in healthcare R&D, with the National Institutes of Health (NIH) allocating over $45 billion annually. The adoption of AI-integrated cameras for digital pathology and advanced diagnostics is particularly high. However, the market faces challenges related to the high cost of advanced systems and complex data privacy regulations, such as HIPAA, which can slow implementation. Leading companies like Teledyne and Cognex Corporation have a strong presence, catering to a sophisticated customer base in pharmaceutical research and clinical diagnostics.

Europe

Europe is a significant market, driven by robust healthcare infrastructure, strong government funding for life sciences research through programs like Horizon Europe, and strict compliance with EU MDR (Medical Device Regulation). Countries such as Germany, the UK, and France are hubs for biomedical research, creating substantial demand for high-resolution cameras in applications like fluorescence imaging and automated microscopy. The region shows a strong trend towards sustainability and the development of energy-efficient imaging technologies. While the market is advanced, growth is sometimes tempered by lengthy product approval processes and economic pressures within national healthcare systems. Companies like Basler AG and IDS are key innovators in this region.

Asia-Pacific

Asia-Pacific is the fastest-growing region, propelled by expanding healthcare access, increasing government investments in medical infrastructure, and a booming biotechnology sector. China and Japan are the largest markets, with China’s domestic manufacturers like Hikvision and Dahua expanding their medical imaging portfolios. The region benefits from cost-effective manufacturing capabilities and a growing emphasis on local production. However, market growth is uneven, with advanced healthcare systems in countries like Japan and South Korea contrasting with emerging markets that prioritize affordability. The adoption of AI and machine learning in diagnostic imaging is accelerating, though it sometimes faces hurdles related to data standardization and regulatory harmonization across different countries.

South America

South America is an emerging market with growing potential, driven by gradual modernization of healthcare systems and increasing investment in medical research in countries like Brazil and Argentina. The demand for industrial cameras is primarily focused on clinical diagnostics and basic research applications, with cost sensitivity being a major factor. Market growth is challenged by economic volatility, limited healthcare budgets, and less developed regulatory frameworks compared to North America or Europe. Nonetheless, partnerships with global manufacturers and regional initiatives to improve healthcare infrastructure are creating new opportunities for market expansion in the long term.

Middle East & Africa

The market in the Middle East & Africa is nascent but shows promise, with growth concentrated in more developed economies such as Israel, Saudi Arabia, and the UAE. These countries are investing in healthcare modernization and telemedicine, driving demand for medical imaging solutions. However, the broader region faces significant challenges, including limited healthcare funding, infrastructure gaps, and political instability in some areas. The adoption of advanced industrial cameras is currently restricted to major urban centers and research institutions. Despite these hurdles, the focus on improving diagnostic capabilities and medical research indicates potential for gradual market development in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Medical and Life Sciences Industrial Cameras markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Medical and Life Sciences Industrial Cameras Market?

->Medical and Life Sciences Industrial Cameras Market was valued at 181 million in 2024 and is projected to reach US$ 346 million by 2032, at a CAGR of 9.7% during the forecast period.

Which key companies operate in Global Medical and Life Sciences Industrial Cameras Market?

-> Key players include Teledyne Technologies, Basler AG, Cognex Corporation, Sony Corporation, Keyence Corporation, Omron Corporation, Baumer Holding AG, and JAI A/S, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-resolution medical imaging, increasing adoption of AI-powered diagnostic systems, growth in pharmaceutical R&D, and expanding applications in digital pathology and microscopy.

Which region dominates the market?

-> North America currently holds the largest market share at approximately 38%, while Asia-Pacific is projected to be the fastest-growing region with an estimated CAGR of 11.2% during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of machine learning for automated image analysis, development of multispectral imaging cameras, increasing adoption of CMOS sensors over CCD, and growing demand for portable and wireless imaging solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...