Massive MIMO channel reciprocity calibration for TDD O-RU Market Insights

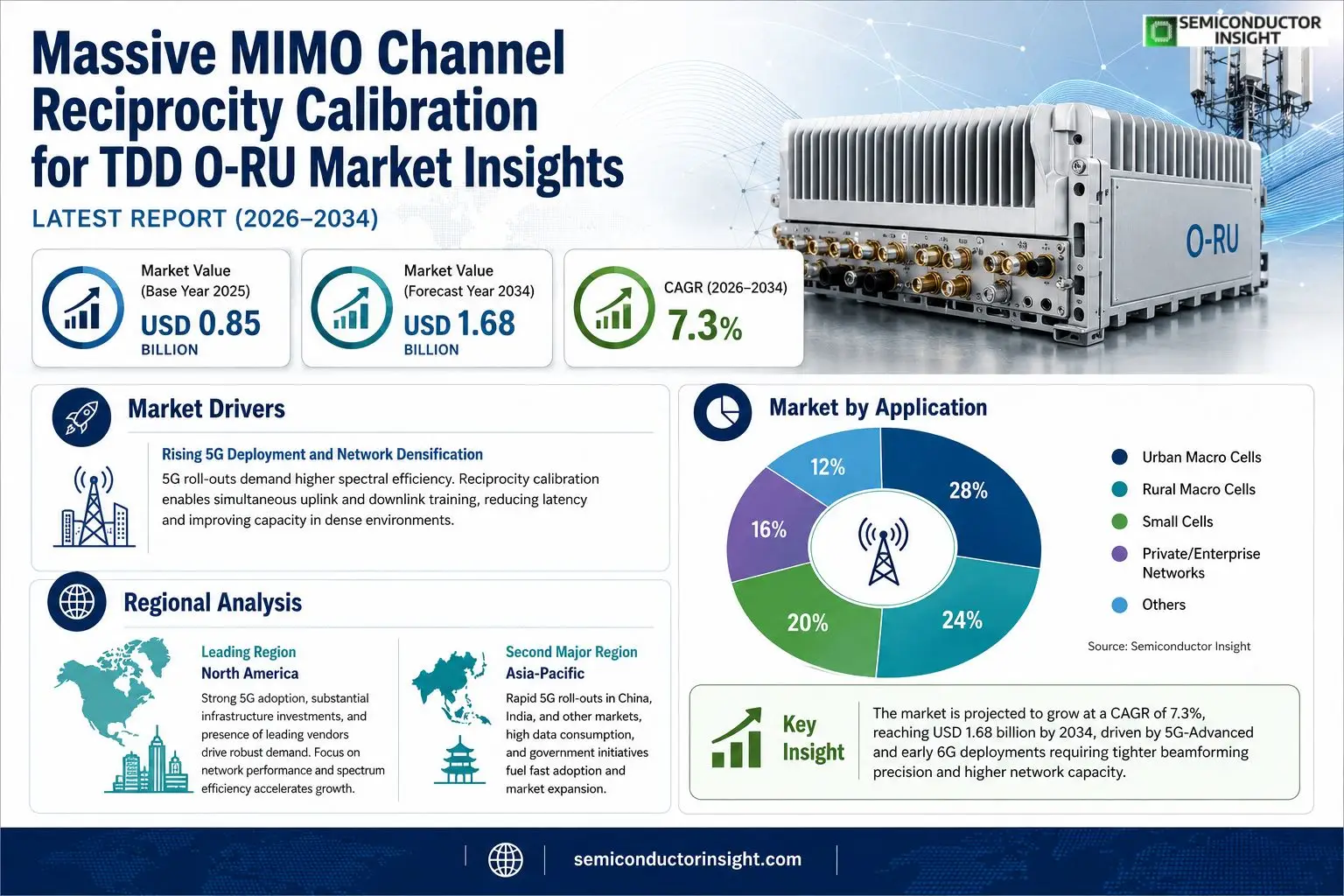

Massive MIMO channel reciprocity calibration for TDD O-RU market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.68 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period.

Massive MIMO channel reciprocity calibration refers to the set of algorithms and hardware procedures that align uplink and downlink radio‑frequency chains in Time‑Division Duplex (TDD) Open Radio Units (O‑RUs). By compensating for mismatches in gain and phase, it enables accurate channel state information exchange, which is essential for achieving the high spectral efficiency promised by massive MIMO deployments.The market is accelerating because network operators are rolling out 5G‑Advanced and early‑stage 6G trials that demand tighter beamforming precision. Furthermore, telecom equipment vendors such as Nokia, Ericsson, Huawei and Samsung are investing heavily in integrated calibration modules to meet emerging standards. Consequently, rising CAPEX on next‑generation base stations and regulatory pushes for higher throughput are driving robust demand for reliable reciprocity calibration solutions.

MARKET DRIVERS

Rising 5G Deployment and Network Densification

Telecom operators worldwide are accelerating 5G roll‑outs, which demands higher spectral efficiency. Massive MIMO channel reciprocity calibration for TDD O‑RU Market is a critical enabler that allows simultaneous uplink and downlink training, reducing latency and improving capacity in dense urban environments.

Cost Pressures and Energy Efficiency Goals

Operators seek to lower total cost of ownership (TCO). By leveraging reciprocity calibration, networks can minimize the number of pilot symbols, leading to significant energy savings and lower operational expenditures for base‑station sites.

➤ “Reciprocity calibration reduces calibration overhead by up to 40 %, delivering faster link establishment and higher throughput.”

In addition, the emergence of open‑radio units (O‑RU) promotes vendor‑agnostic deployments, further driving demand for standardized calibration solutions across the ecosystem.

MARKET CHALLENGES

Technical Complexity of Calibration Algorithms

Implementing accurate reciprocity calibration requires sophisticated signal‑processing techniques. Small errors in amplitude or phase alignment can degrade beamforming performance, creating a barrier for rapid adoption in legacy networks.

Other Challenges

Interoperability Across Vendor Platforms

The fragmented nature of O‑RU hardware leads to integration hurdles, as each vendor may employ proprietary interfaces that are not immediately compatible with uniform calibration standards.

MARKET RESTRAINTS

Regulatory and Spectrum Allocation Constraints

Regulatory bodies in several regions impose stringent emission limits, which restrict the usable power margins for advanced calibration sequences. These constraints can slow the rollout of full‑scale Massive MIMO deployments.Furthermore, the need for extensive field testing before certification adds time and cost, limiting the speed at which new calibration solutions reach the market.Limited availability of skilled engineers who understand both RF hardware and advanced DSP algorithms also restrains the pace of innovation.

MARKET OPPORTUNITIES

Emerging AI‑Driven Calibration Techniques

Artificial intelligence and machine‑learning models are being pilot‑tested to predict and correct reciprocity mismatches in real time. Early trials indicate potential throughput gains of 15 % compared with conventional methods.In parallel, the rollout of Open RAN (O‑RAN) frameworks creates a unified software‑defined environment, encouraging cross‑vendor collaboration and opening new revenue streams for calibration software providers.Geographically, emerging markets in Asia‑Pacific and Africa are investing heavily in 5G infrastructure, presenting a sizable adoption window for cost‑effective calibration solutions.

Massive MIMO channel reciprocity calibration for TDD O-RU Market Trends

Accelerated Adoption in 5G‑Advanced and Early 6G Deployments

The market recorded a valuation of USD 0.85 billion in 2025 and is projected to reach USD 1.68 billion by 2034, reflecting a compound annual growth rate of roughly 7 percent. This expansion is driven primarily by network operators upgrading to 5G‑Advanced and initiating 6G trial phases, both of which require tighter beam‑forming precision. The calibration process aligns uplink and downlink RF chains, ensuring the channel state information remains accurate across massive antenna arrays. As a result, spectral efficiency improves and capacity targets are met without additional spectrum.

Other Trends

Calibration Technology Evolution

Recent algorithmic advances incorporate machine‑learning‑assisted compensation, reducing the need for frequent manual recalibration. Hardware integration has moved toward monolithic RF modules that embed calibration circuits directly on the O‑RU board, shortening signal paths and minimizing phase drift. These technical refinements lower operational expenditures and shorten deployment cycles for carriers.

Vendor Investment Landscape

Key equipment manufacturers,including Nokia, Ericsson, Huawei, and Samsung,are allocating substantial R&D budgets toward integrated calibration solutions. Partnerships with semiconductor suppliers accelerate the availability of silicon‑based calibration blocks, while joint industry projects standardize interfaces across multiple vendors. The combined effect is a broader ecosystem that supports rapid rollout of next‑generation base stations.

Emerging Standards and Regulatory Influence

Regulatory bodies in major markets are updating technical specifications to mandate reciprocity calibration as a baseline requirement for TDD O‑RU deployments. The forthcoming releases of 3GPP Release 18 incorporate tighter tolerance limits, prompting manufacturers to certify compliance before product launch. This regulatory push, coupled with rising capital expenditures on advanced RAN infrastructure, sustains a robust demand pipeline for calibrated O‑RU platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Massive MIMO Reciprocity Calibration Landscape (2025‑2034)

The Massive MIMO channel reciprocity calibration segment for TDD Open Radio Units (O‑RUs) is currently led by a few telecom equipment giants that integrate calibration modules directly into their 5G‑Advanced and early‑6G base‑station portfolios. Nokia and Ericsson command the largest market share, leveraging extensive R&D budgets to deliver end‑to‑end calibration suites that combine hardware‑assisted linearization with AI‑driven self‑training algorithms. Huawei follows closely, differentiating itself through aggressive cost‑competitiveness and deep integration with its own O‑RU line‑up. Samsung rounds out the top tier, focusing on silicon‑photonic calibrators that target high‑frequency mmWave deployments. These incumbents dominate procurement cycles of tier‑1 operators, benefitting from long‑term contracts, comprehensive service ecosystems, and strong standard‑setting influence within 3GPP releases.Beyond the dominant four, a vibrant ecosystem of niche innovators enriches the calibration market with specialized expertise. Qualcomm supplies highly integrated RF front‑end chipsets that embed reciprocity correction at the silicon level, while Intel offers programmable FPGA‑based calibration accelerators for flexible deployments. Mavenir and MTS Systems provide software‑defined calibration frameworks that appeal to cloud‑native O‑RU architectures. CommScope, Rohde & Schwarz, and Keysight contribute precision test and measurement tools that validate calibration performance in field trials. Emerging players such as ADTRAN, Fujitsu, NEC, and Anartic focus on modular calibration cards and open‑source reference designs, enabling smaller vendors and private‑network operators to adopt advanced reciprocity techniques without extensive in‑house development.

List of Key Massive MIMO Calibration Companies Profiled

- Nokia

- Ericsson

- Huawei

- Samsung

- Qualcomm

- Intel

- Mavenir

- MTS Systems

- CommScope

- Rohde & Schwarz

- Keysight Technologies

- ADTRAN

- Fujitsu

- NEC

- Anartic

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hybrid Calibration

|

| By Application |

|

Urban Macro Cells

|

| By End User |

|

Mobile Network Operators

|

| By Standardization Phase |

|

Mainstream Deployment

|

| By Vendor Ecosystem |

|

Tier‑1 Vendors

|

Regional Analysis: North America

North America

The North American market is witnessing rapid advancements in Massive MIMO technology, including the development of more sophisticated calibration algorithms and hardware solutions. This is crucial for achieving optimal performance in TDD O-RU deployments.

The regulatory environment in North America is supportive of 5G deployment, which in turn is fueling the demand for Massive MIMO calibration solutions. Clear spectrum policies and streamlined regulatory processes are facilitating market growth.

The North American market features a mix of established telecommunications equipment vendors and emerging technology providers, leading to healthy competition and continuous innovation in Massive MIMO calibration.

Significant investments in network infrastructure across North America are driving the need for efficient and accurate Massive MIMO channel reciprocity calibration to optimize the performance of TDD O-RU deployments.

North America

The substantial investments in 5G infrastructure across North America are directly fueling the demand for advanced Massive MIMO channel reciprocity calibration solutions, particularly for TDD O-RU deployments. The emphasis on maximizing spectrum efficiency is a key market driver. Key players are focused on developing innovative software and hardware to address the complexities of channel reciprocity in TDD systems. The region’s mature telecommunications ecosystem and strong research and development capabilities further contribute to this growth. The integration of AI and machine learning for more accurate and automated calibration processes is gaining traction. Furthermore, the focus on private 5G networks is creating new opportunities for Massive MIMO calibration in industrial and enterprise settings.

Europe

Europe presents a strong and steadily growing market for Massive MIMO channel reciprocity calibration. The region’s commitment to 5G leadership and the ongoing network densification efforts are key drivers. While the deployment pace might be slightly more gradual than in North America, the focus on energy efficiency and advanced spectrum management continues to bolster demand. European regulations promoting open radio access networks are also influencing the calibration market. The development of interoperable solutions is a key trend in the European market.

Asia-Pacific

Asia-Pacific is poised to be the largest and fastest-growing market for Massive MIMO channel reciprocity calibration. The region’s rapid 5G rollout, particularly in China and India, is creating immense demand. The high population density and increasing data consumption are further accelerating market growth. The emphasis on cost-effective solutions and the development of localized calibration tools are prominent features of the Asia-Pacific market.

South America

South America is an emerging market for Massive MIMO channel reciprocity calibration. While 5G deployment is in its early stages, the region’s growing digital economy and increasing mobile data usage are expected to drive demand in the coming years. The focus is on providing affordable and scalable calibration solutions to support the expanding 5G networks.

Middle East & Africa

The Middle East & Africa represents a promising growth area for Massive MIMO channel reciprocity calibration. The region’s investments in network modernization and the increasing adoption of 5G are creating new opportunities. The focus is on deploying advanced solutions to meet the growing demand for high-bandwidth applications and improved network performance. Government initiatives supporting digital transformation are also contributing to market expansion.

Report Scope

This market research report provides a comprehensive analysis of the Massive MIMO channel reciprocity calibration for TDD O-RU Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Massive MIMO channel reciprocity calibration for TDD O-RU Market?

-> Massive MIMO channel reciprocity calibration for TDD O-RU Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.68 billion by 2034.

Which key companies operate in Massive MIMO channel reciprocity calibration for TDD O-RU Market?

-> Key players include Nokia, Ericsson, Huawei, Samsung, among others.

What are the key growth drivers?

-> Key growth drivers include rollout of 5G‑Advanced and early‑stage 6G trials, tighter beamforming precision requirements, rising CAPEX on next‑generation base stations, and regulatory pushes for higher throughput.

Which region dominates the market?

-> The reference does not specify a single dominant region; market activity is strong across North America, Europe, and Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include integration of AI/ML for calibration, development of integrated calibration modules, and ongoing standardization for 5G‑Advanced and 6G.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...