Massive IoT over satellite with direct-to-device 5G NR Market Insights

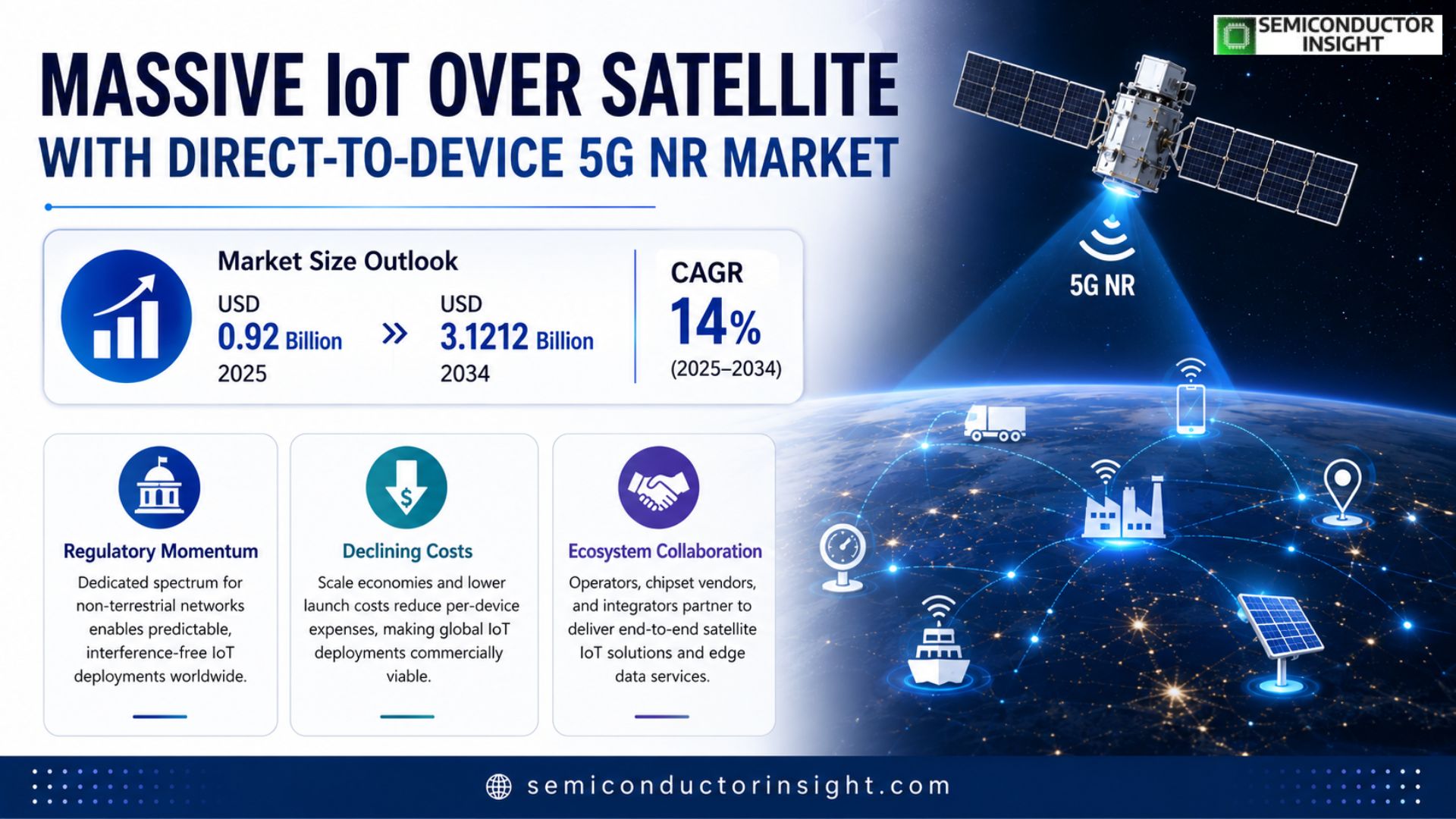

Global Massive IoT over satellite with direct‑to‑device 5G NR market size was valued at USD 0.85 billion in 2025.The market is projected to grow from USD 0.92 billion in 2025 to USD 3.1212 billion by 2034, exhibiting a CAGR of 14 % during the forecast period.

Massive IoT over satellite with direct‑to‑device 5G NR refers to ultra‑low‑power sensor nodes that connect directly to low‑Earth‑orbit (LEO) satellites using the New Radio (NR) air interface, bypassing traditional terrestrial gateways. This architecture enables seamless global coverage for applications such as asset tracking, environmental monitoring and maritime telemetry. The market is experiencing rapid growth because operators are deploying dense LEO constellations that lower latency below 30 ms and reduce per‑device costs.

Furthermore, regulatory bodies are allocating dedicated spectrum bands for non‑terrestrial networks, while industries such as agriculture, logistics and oil & gas are demanding reliable connectivity in remote locations.

MARKET DRIVERS

Expanding Connectivity in Remote Regions

Massive IoT over satellite with direct-to-device 5G NR Market is being propelled by the need to connect remote assets such as agriculture sensors, maritime vessels, and oil‑rig equipment. Satellite constellations now offer latency under 50 ms, making real‑time telemetry feasible for large‑scale deployments.

Policy Support and Spectrum Allocation

Governments worldwide are allocating dedicated 5G NR bands for satellite use, reducing regulatory uncertainty and encouraging operators to invest in satellite‑based IoT infrastructure. This policy environment accelerates network roll‑outs and fosters ecosystem partnerships.

➤ Satellite operators report a 35 % year‑over‑year increase in IoT traffic, reflecting strong market momentum.

Enterprise adoption is further driven by cost‑effective device pricing and the ability to manage millions of low‑power nodes from a single platform, unlocking new business models in logistics, environmental monitoring, and smart city extensions.

MARKET CHALLENGES

Limited Battery Life for High‑Frequency Reporting

IoT devices that transmit large volumes of data via satellite consume more power, shortening battery life and increasing maintenance costs. Manufacturers must balance data granularity with energy efficiency to remain viable in the field.

Other Challenges

Regulatory Fragmentation

Different regions impose varying licensing requirements for satellite‑based 5G NR, creating compliance complexities that can delay market entry and increase operational overhead.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying a satellite constellation equipped for massive IoT requires substantial upfront investment in launch services, ground stations, and network integration, which can deter smaller service providers.

Interference Management

Co‑existence between terrestrial 5G NR and satellite beams demands sophisticated interference mitigation techniques. Failure to address this can degrade performance and limit scalability.

MARKET OPPORTUNITIES

Edge‑Enabled Satellite IoT Services

Integrating edge computing capabilities directly on satellite platforms enables real‑time analytics at the edge, reducing backhaul requirements and unlocking value‑added services for industries such as mining and disaster response.

Hybrid Terrestrial‑Satellite Deployments

Combining terrestrial 5G with satellite backhaul creates resilient connectivity solutions for critical infrastructure, offering redundancy and broader coverage without additional spectrum costs.

Vertical‑Specific Solutions

Tailored satellite IoT offerings for sectors such as precision agriculture, maritime logistics, and utility grid monitoring present high‑growth niches, driven by the need for pervasive, low‑latency data collection.

Massive IoT over satellite with direct-to-device 5G NR Market Trends

Growth Driven by LEO Constellations

The rollout of dense low‑Earth‑orbit (LEO) satellite constellations is reshaping connectivity for ultra‑low‑power sensors. By positioning dozens of satellites in orbits below 2,000 km, latency is consistently pushed under 30 ms, a threshold that makes real‑time telemetry feasible for remote assets. Operators are leveraging the 5G New Radio (NR) air interface to enable direct links between devices and space, eliminating the need for terrestrial gateways. This architecture expands coverage to 100 % of the planet, allowing asset‑tracking, environmental monitoring, and maritime telemetry applications to operate without a ground‑based network footprint.

Other Trends

Regulatory Momentum

National spectrum authorities are carving out dedicated bands for non‑terrestrial networks, which creates a predictable framework for commercial deployment. Coordinated allocations across Europe, North America, and Asia reduce the risk of interference and accelerate the certification of satellite‑enabled IoT modules. As regulators formalize rules for coexistence with terrestrial 5G services, manufacturers can design devices with confidence that the radio parameters will remain stable over the product lifecycle.

Cost Compression and Ecosystem Expansion

Scale economies are beginning to lower the bill of materials for satellite‑compatible chipsets and antenna arrays. Mass production of flexible solar‑powered sensor nodes, combined with the decreasing launch cost per kilogram, translates into per‑device savings that make global IoT deployments financially viable. Partner ecosystems are also maturing: satellite operators, chipset vendors, and system integrators are forming joint ventures to deliver turnkey solutions. Notable collaborations include a satellite operator integrating a leading modem platform into its LEO fleet, and cloud providers offering edge‑compute services that ingest data directly from space‑borne endpoints.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Massive IoT over Satellite with Direct‑to‑Device 5G NR

SpaceX’s Starlink, OneWeb, Iridium Communications and Qualcomm’s Snapdragon Satellite platform dominate the early‑stage market, leveraging dense low‑Earth‑orbit constellations to deliver sub‑30 ms latency and ultra‑low‑cost connectivity for sensor nodes. These incumbents control the bulk of spectrum allocation in the non‑terrestrial network bands and have secured flagship contracts with logistics, agriculture and maritime firms seeking global coverage without terrestrial gateways. The market structure is rapidly consolidating around a few megaconstellation operators who combine satellite infrastructure with chipset manufacturers to create end‑to‑end solutions, driving volume discounts and enabling the projected CAGR of 14 % through 2034.

Beyond the tier‑one players, a diverse set of niche specialists is expanding the ecosystem. Airbus Defence & Space and Thales Group provide satellite payloads optimized for Massive IoT traffic, while Telesat and SES are launching LEO constellations focused on enterprise IoT services. Regional champions such as Huawei, Nokia and Samsung contribute 5G NR modem expertise, and Amazon’s Project Kuiper is positioning itself as a low‑cost alternative for uplink‑heavy IoT devices. Emerging pure‑play IoT providers like Loon (Alphabet) and Telenor are experimenting with hybrid terrestrial‑satellite backhaul to reach remote asset‑tracking use cases, further enriching the competitive landscape.

List of Key Massive IoT over Satellite with Direct‑to‑Device 5G NR Companies Profiled

- SpaceX (Starlink)

- OneWeb

- Iridium Communications

- Qualcomm Snapdragon Satellite

- Airbus Defence & Space

- Thales Group

- Telesat

- SES

- Huawei

- Nokia

- Samsung

- Amazon Project Kuiper

- Loon (Alphabet)

- Telenor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Direct‑to‑Device Sensors

|

| By Application |

|

Asset Tracking

|

| By End User |

|

Agriculture Enterprises

|

| By Connectivity Mode |

|

Pure Satellite Direct‑Link

|

| By Industry Vertical |

|

Marine Shipping

|

Regional Analysis: North America

The logistics sector is increasingly leveraging Massive IoT over satellite with direct-to-device 5G NR for real-time tracking of assets, optimizing delivery routes, and enhancing supply chain visibility. This technology enables businesses to monitor goods across vast distances, improving efficiency and reducing operational costs.

In agriculture, this technology facilitates precision farming by enabling the deployment of sensors for monitoring soil conditions, weather patterns, and livestock health. Remote asset monitoring in industries like energy and utilities benefits from the reliable connectivity offered by satellite, ensuring continuous data flow and proactive maintenance.

The defense and public safety sectors are exploring the potential of Massive IoT over satellite with direct-to-device 5G NR for secure communication, situational awareness, and remote surveillance. The technology’s ability to operate in challenging environments makes it ideal for critical applications.

Environmental agencies are utilizing this technology for remote monitoring of pollution levels, wildlife tracking, and disaster response efforts. The broad coverage of satellite networks allows for comprehensive data collection across geographically diverse areas.

Europe

Europe presents a diverse market landscape for Massive IoT over satellite with direct-to-device 5G NR. Various national regulations and infrastructure development stages influence the adoption pace. However, the region’s strong focus on sustainability and smart city initiatives creates a significant demand for IoT solutions. The development of secure and interoperable satellite communication networks will be crucial for market expansion.

Asia-Pacific

Asia-Pacific is expected to witness substantial growth Massive IoT over satellite with direct-to-device 5G NR Market, driven by rapid industrialization and the proliferation of smart devices. The region’s vast geography and remote areas present a strong use case for satellite-based IoT connectivity. Government initiatives supporting digital transformation and infrastructure development are further accelerating market growth.

South America

South America offers considerable potential for Massive IoT over satellite with direct-to-device 5G NR, particularly in sectors such as agriculture, mining, and logistics. The need for reliable connectivity in remote and sparsely populated regions creates a strong demand for satellite-based solutions. Addressing the challenges related to infrastructure investment and regulatory frameworks will be key to unlocking the market’s full potential.

Middle East & Africa

The Middle East & Africa region represents a promising, albeit nascent, market for Massive IoT over satellite with direct-to-device 5G NR. The region’s increasing investments in infrastructure, coupled with growing demand for smart city solutions and industrial automation, are expected to drive market growth. Satellite connectivity can play a vital role in bridging the connectivity gap in remote and underserved areas.

Report Scope

This market research report provides a comprehensive analysis of the Massive IoT over satellite with direct-to-device 5G NR Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Massive IoT over satellite with direct-to-device 5G NR Market?

-> Massive IoT over satellite with direct-to-device 5G NR Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 3.12 billion by 2034.

Which key companies operate Massive IoT over satellite with direct-to-device 5G NR Market?

-> Key players include SpaceX (Starlink), OneWeb, Iridium Communications, and Qualcomm (Snapdragon Satellite).

What are the key growth drivers?

-> Key growth drivers include deployment of dense low‑Earth‑orbit constellations reducing latency below 30 ms, allocation of dedicated NTN spectrum by regulators, and rising demand for reliable connectivity in agriculture, logistics, and oil & gas sectors.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include low‑power NR chipsets for sensor nodes, integration of AI/ML for satellite‑edge analytics, and development of standardized non‑terrestrial network (NTN) specifications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...