MARKET INSIGHTS

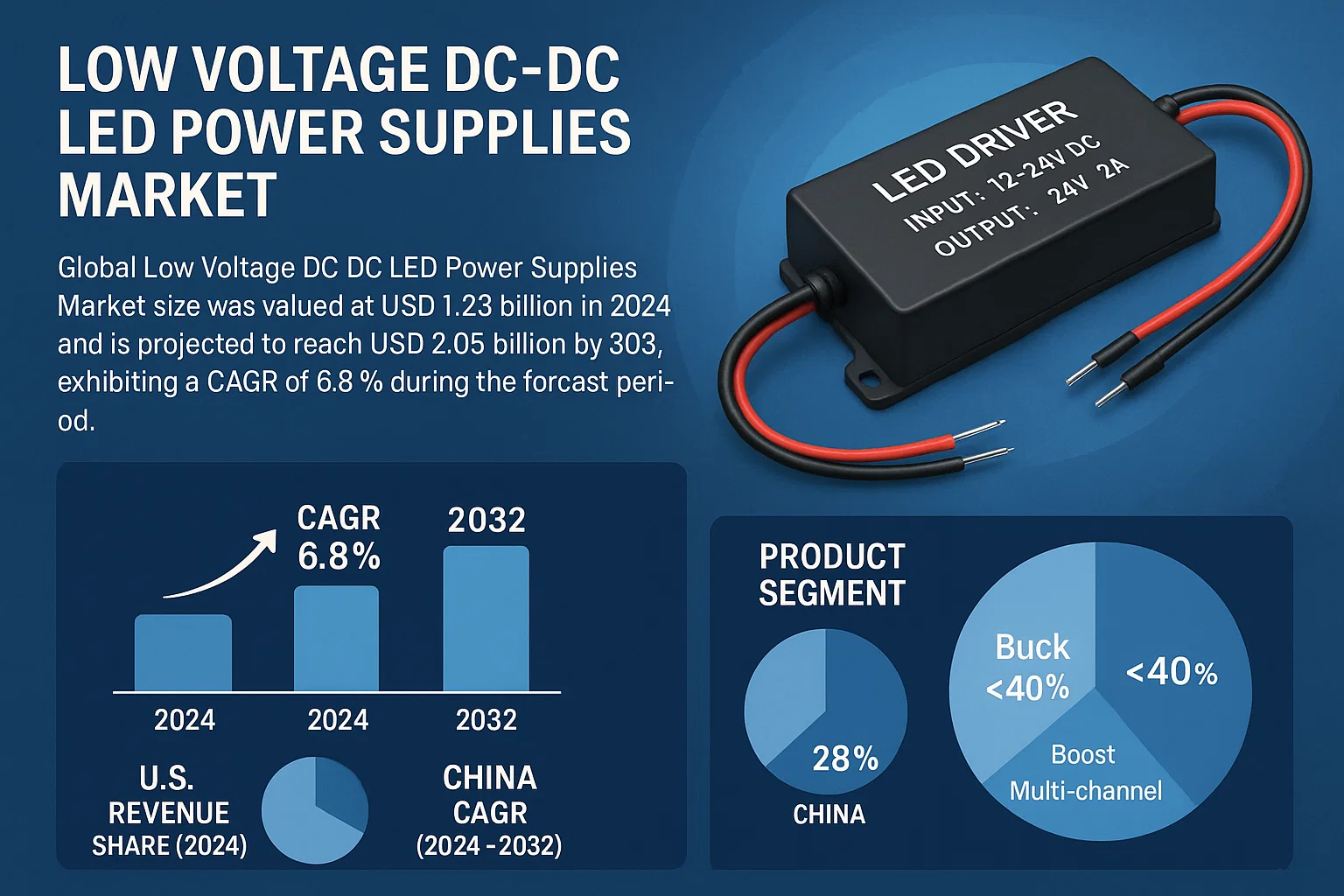

Global Low Voltage DC-DC LED Power Supplies Market size was valued at USD 1.23 billion in 2024 and is projected to reach USD 2.05 billion by 2032, exhibiting a CAGR of 6.8% during the forecast period. The U.S. market accounted for 28% of global revenue in 2024, while China is anticipated to grow at a faster CAGR of 8.2% through 2032.

Low Voltage DC-DC LED Power Supplies, commonly referred to as LED drivers, are electronic devices that regulate and supply constant current to LED lighting systems from a DC power source. These components are critical for converting and stabilizing input voltage (typically ranging from 5V to 48V) to match the specific requirements of LED arrays, ensuring optimal performance and longevity. The product segment includes Buck, Boost, Multi-channel, and other converter topologies, with Buck converters currently dominating over 40% of market share.

Market growth is driven by increasing adoption of energy-efficient lighting solutions, government regulations promoting LED usage, and expanding applications in automotive and consumer electronics. The Buck converter segment alone is projected to reach USD 890 million by 2032. Major players like Texas Instruments, STMicroelectronics, and Infineon collectively hold about 45% of the market, with recent developments including compact, high-efficiency drivers for smart lighting applications. However, price volatility of raw materials and design complexity for high-power applications remain key challenges for industry participants.

MARKET DYNAMICS

MARKET DRIVERS

Global Transition to Energy-Efficient Lighting Solutions Driving Market Expansion

The global shift towards energy-efficient lighting technologies represents a primary growth catalyst for the low voltage DC-DC LED power supplies market. Governments worldwide have implemented stringent energy efficiency regulations and phase-out programs for traditional incandescent and fluorescent lighting. These regulatory measures, coupled with rising electricity costs and environmental consciousness among consumers, have accelerated LED adoption across residential, commercial, and industrial sectors. The market has witnessed remarkable growth, with LED lighting penetration reaching approximately 60% in developed markets and showing rapid expansion in emerging economies. This transition creates sustained demand for reliable, efficient power conversion solutions that can optimize LED performance while minimizing energy consumption. The inherent advantages of DC-DC conversion—including higher efficiency, reduced electromagnetic interference, and better form factor optimization—position these power supplies as essential components in modern lighting systems.

Proliferation of Portable and Battery-Powered Devices Fueling Market Growth

The exponential growth in portable electronics and battery-operated devices represents another significant driver for low voltage DC-DC LED power supplies. With the consumer electronics market projected to maintain robust growth, manufacturers increasingly integrate LED lighting solutions into smartphones, tablets, laptops, wearables, and portable medical devices. These applications require compact, efficient power management solutions that can operate from battery voltages while maintaining precise current regulation for optimal LED performance. The trend toward miniaturization and increased functionality in portable devices has driven innovation in power supply design, with manufacturers developing increasingly sophisticated buck, boost, and multi-channel converters that offer higher power density and improved thermal management. The automotive sector’s rapid adoption of LED lighting for interior and exterior applications further amplifies this demand, as vehicles incorporate more sophisticated lighting systems requiring stable power delivery from variable battery voltages.

Advancements in Semiconductor Technology Enhancing Product Capabilities

Technological innovations in semiconductor manufacturing and power conversion topologies continue to drive market development. Recent advancements have enabled power supply manufacturers to achieve conversion efficiencies exceeding 95% while reducing component size and cost. The integration of sophisticated control algorithms, advanced packaging techniques, and improved thermal management solutions has resulted in power supplies that offer superior performance characteristics. These technological improvements have facilitated the development of intelligent lighting systems featuring dimming capabilities, color temperature adjustment, and network connectivity. The industry’s move toward higher switching frequencies has allowed for smaller passive components, enabling more compact power supply designs that meet the space constraints of modern electronic devices. Furthermore, enhanced electromagnetic compatibility and reduced audible noise have expanded application possibilities in sensitive environments such as medical facilities and audio-visual equipment.

MARKET CHALLENGES

Intense Price Competition and Margin Pressures Challenging Manufacturer Profitability

The low voltage DC-DC LED power supply market faces significant pricing challenges due to intense global competition and increasing cost sensitivity among end-users. While the market continues to grow, manufacturers encounter substantial pressure to reduce prices while maintaining or improving product quality and performance. This competitive environment has compressed profit margins, particularly for standard products where differentiation becomes increasingly difficult. The industry has witnessed consolidation as smaller players struggle to compete with larger manufacturers that benefit from economies of scale in component procurement and production. Additionally, fluctuating raw material costs, particularly for electronic components such as semiconductors and magnetic materials, create uncertainty in pricing strategies and inventory management. These economic pressures necessitate continuous operational optimization and supply chain management to maintain competitiveness.

Other Challenges

Technical Complexity in High-Density Applications

Designing power supplies for high-density LED arrays presents significant technical challenges. As LED lighting systems become more powerful and compact, power supplies must deliver higher currents while managing thermal dissipation effectively. The proximity of multiple LEDs in array configurations creates thermal management issues that can affect both LED performance and power supply reliability. Design engineers must balance efficiency, size, thermal performance, and cost constraints while meeting increasingly stringent safety and performance standards.

Rapid Technological Obsolescence

The rapid pace of technological advancement in both LED technology and power conversion creates challenges regarding product lifecycle management. Manufacturers must continuously invest in research and development to keep pace with evolving market requirements and technological improvements. This constant innovation cycle can render existing product designs obsolete within relatively short timeframes, requiring significant ongoing investment in new product development and manufacturing process updates.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Component Availability Impacting Market Stability

The global electronics supply chain’s vulnerability to disruptions represents a significant restraint for low voltage DC-DC LED power supply manufacturers. Recent events have highlighted the industry’s dependence on stable component supplies, with shortages of critical semiconductors and passive components causing production delays and increased costs. The concentration of semiconductor manufacturing capacity in specific geographic regions creates supply chain risks that can affect product availability and pricing stability. These challenges are particularly acute for specialized components required for high-efficiency power conversion, where alternative sources may be limited or non-existent. The industry’s just-in-time manufacturing practices, while efficient during stable conditions, amplify the impact of supply chain disruptions, leading to extended lead times and potential lost business opportunities.

Additionally, the complexity of global logistics and transportation networks introduces further uncertainties. Fluctuations in freight costs, customs regulations, and international trade policies can significantly impact the total cost of ownership and delivery reliability. These factors collectively restrain market growth by introducing unpredictability in both supply availability and product pricing, making long-term planning and commitment challenging for both manufacturers and their customers.

MARKET OPPORTUNITIES

Emerging Applications in Smart Infrastructure Creating New Growth Avenues

The rapid development of smart city infrastructure and Internet of Things applications presents substantial growth opportunities for low voltage DC-DC LED power supplies. Urban development initiatives worldwide increasingly incorporate intelligent lighting systems that require sophisticated power management solutions. These systems typically feature network connectivity, environmental sensing, adaptive lighting control, and energy management capabilities—all requiring reliable, efficient power conversion. The integration of renewable energy sources, particularly solar power, with LED lighting systems creates additional opportunities for DC-DC power supplies optimized for maximum power point tracking and battery management. The trend toward DC microgrids in commercial and industrial facilities further expands application possibilities, as these systems can benefit from the higher efficiency of DC-powered LED lighting without the losses associated with multiple AC-DC conversions.

Furthermore, the automotive industry’s transition toward electric vehicles represents another significant opportunity. Modern vehicles incorporate numerous LED lighting applications—from interior mood lighting to advanced driver assistance system indicators—all requiring specialized power supplies that can operate reliably in the challenging automotive environment. The increasing adoption of autonomous driving features and enhanced safety systems will likely drive further innovation and demand for automotive-grade power management solutions.

Additionally, the medical and healthcare sectors offer promising growth prospects. The critical nature of medical lighting applications demands power supplies with exceptional reliability, precise current regulation, and low electromagnetic interference. As medical facilities worldwide upgrade their equipment and incorporate more LED-based diagnostic and surgical lighting, the demand for medically certified power supplies continues to grow.

LOW VOLTAGE DC-DC LED POWER SUPPLIES MARKET TRENDS

Increasing Adoption of Energy-Efficient Lighting Solutions to Propel Market Growth

The global shift toward energy-efficient lighting solutions has significantly boosted the demand for low-voltage DC-DC LED power supplies. With LED lighting gaining prominence in residential, commercial, and industrial applications due to its lower energy consumption and longer lifespan, the need for reliable power conversion solutions has intensified. Buck converters, a key segment, are projected to grow at a CAGR of 7.5% from 2024 to 2032, driven by their ability to efficiently step down input voltages while maintaining high efficiency. Moreover, advancements in semiconductor technology have led to the development of compact, high-efficiency power supplies that cater to modern LED applications.

Other Trends

Expansion in Smart Lighting and IoT Integration

The integration of smart lighting solutions with IoT has created new opportunities for low-voltage DC-DC LED drivers. These power supplies facilitate precise current regulation, enabling dynamic brightness control, color tuning, and wireless connectivity in smart lighting systems. The smart lighting market is expected to exceed $38 billion by 2027, further accelerating demand for efficient power management solutions. Additionally, increasing adoption in automotive lighting—particularly for interior and exterior LED applications—has reinforced the market growth trajectory. Power supply manufacturers are increasingly focusing on designs that incorporate thermal management and electromagnetic interference (EMI) suppression to meet evolving industry standards.

Rise in Demand for Consumer Electronics and Miniaturized Power Solutions

The consumer electronics sector continues to be a major driver for the low-voltage DC-DC LED power supply market, with products such as smartphones, tablets, and wearable devices requiring compact, efficient power conversion solutions. The demand for multi-channel LED drivers has surged, particularly in applications requiring synchronized lighting controls in displays and backlighting. Meanwhile, the trend toward miniaturization has prompted manufacturers to develop ultra-compact power supply modules with high power density, catering to space-constrained applications. With the Asia-Pacific region leading in electronics manufacturing, key players are expanding production capacities to meet the growing market demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Brands Accelerate Innovation in Power Efficiency Solutions

The global Low Voltage DC-DC LED Power Supplies market demonstrates a dynamic competitive environment where established semiconductor giants compete with specialized power electronics firms. Texas Instruments leads the sector with a 2024 market share of approximately 18%, leveraging its proprietary Buck converter technology and extensive manufacturing capabilities across three continents. The company’s December 2023 launch of the TPS9266x series featuring 95% power conversion efficiency exemplifies its innovation strategy.

STMicroelectronics and Infineon Technologies collectively command about 25% of the global revenue, with their strength rooted in automotive-grade power solutions. Both companies recently expanded their portfolios with multi-channel drivers compliant with the latest Zhaga Book 25 standards, responding to the growing demand for modular lighting systems in smart city applications.

The competitive intensity continues rising as Asian manufacturers like Richtek and ISSI capture market share through cost-optimized solutions. These players are particularly successful in the APAC region, where price sensitivity remains a key purchase driver. Their 2023-2024 product refresh cycles incorporated advanced thermal management features, bridging the performance gap with Western competitors.

Meanwhile, ON Semiconductor strengthened its position through strategic acquisitions, including the Q1 2024 purchase of a niche LED driver specialist to bolster its IoT lighting solutions. This move highlights how industry leaders are diversifying beyond traditional lighting applications into smart building ecosystems.

List of Key Low Voltage DC-DC LED Power Supply Manufacturers

- Texas Instruments (U.S.)

- STMicroelectronics (Switzerland)

- Infineon Technologies (Germany)

- ON Semiconductor (U.S.)

- Monolithic Power Systems (U.S.)

- Richtek Technology Corporation (Taiwan)

- Integrated Silicon Solution Inc. (U.S.)

- Diodes Incorporated (U.S.)

- Mean Well Enterprises (Taiwan)

- XP Power (Singapore)

Segment Analysis:

By Type

Buck Converters Dominate the Market Due to High Efficiency in Step-Down Voltage Applications

The market is segmented based on type into:

- Buck

- Boost

- Multi-channel

- Others

By Application

LED Lighting Segment Leads Owing to Rising Demand for Energy-Efficient Lighting Solutions

The market is segmented based on application into:

- LED Lighting

- Consumer Electronics

- Others

By Input Voltage Range

3V-12V Segment Accounts for Significant Share Due to Compatibility with Common Battery Sources

The market is segmented based on input voltage range into:

- Below 3V

- 3V-12V

- 12V-24V

- Above 24V

By Output Current

350mA-700mA Range Holds Major Share for Standard LED Driving Applications

The market is segmented based on output current into:

- Below 350mA

- 350mA-700mA

- 700mA-1A

- Above 1A

Regional Analysis: Low Voltage DC-DC LED Power Supplies Market

Asia-Pacific

The Asia-Pacific region dominates the global Low Voltage DC-DC LED Power Supplies market, accounting for the highest consumption volume and manufacturing output. This leadership is driven by massive electronics manufacturing hubs in China, South Korea, and Taiwan, alongside rapidly expanding infrastructure and urbanization projects across India and Southeast Asia. The region’s robust demand stems from extensive adoption in LED lighting for commercial, industrial, and residential applications, as well as the colossal consumer electronics sector. While cost-competitive, standard-efficiency products remain prevalent due to high price sensitivity, there is a marked shift toward more energy-efficient and intelligent power management solutions, fueled by growing environmental awareness and supportive government policies promoting energy conservation. Local manufacturing capabilities, coupled with strong supply chain networks, position Asia-Pacific as both the largest market and the primary production center for these components.

North America

North America represents a significant and technologically advanced market for Low Voltage DC-DC LED Power Supplies, characterized by stringent energy efficiency standards and a strong emphasis on innovation. Regulations such as the U.S. Department of Energy’s efficiency requirements and California’s Title 24 drive demand for high-performance, reliable power supplies, particularly in smart lighting and architectural applications. The region’s mature consumer electronics market and the growing adoption of IoT-enabled devices further bolster demand. Key industry players, including Texas Instruments and ON Semiconductor, are headquartered here, fostering a climate of continuous R&D and leading to the early adoption of features like programmability, dimming capabilities, and enhanced thermal management. The market is defined by a preference for quality, reliability, and compliance over pure cost considerations.

Europe

Europe’s market is shaped by some of the world’s most rigorous environmental and efficiency directives, including the EU Ecodesign Directive and ErP Lot regulations, which mandate high energy efficiency and low standby power consumption for LED lighting products. This regulatory landscape strongly encourages the adoption of advanced, high-efficiency Low Voltage DC-DC LED drivers. The region exhibits strong demand from the automotive sector (for interior and exterior lighting), high-end architectural lighting projects, and the smart home market. European manufacturers and consumers prioritize sustainability, product longevity, and smart features, leading to a competitive environment where technological sophistication and environmental compliance are key differentiators. The presence of major semiconductor companies also contributes to a focus on innovation and quality.

South America

The South American market for Low Voltage DC-DC LED Power Supplies is in a growth phase, primarily driven by gradual infrastructure development and the ongoing replacement of traditional lighting with LED solutions in major urban centers. Countries like Brazil and Argentina are the main contributors to regional demand. However, market expansion is tempered by economic volatility and currency fluctuations, which impact investment in new construction and consumer purchasing power. This often leads to a higher reliance on imported, cost-effective products rather than premium, high-efficiency solutions. While the potential for long-term growth is acknowledged, the current market is characterized by a focus on essential functionality and affordability, with slower adoption of advanced technological features prevalent in more developed regions.

Middle East & Africa

The Middle East & Africa region presents an emerging market with potential driven by large-scale infrastructure and urban development projects, particularly in Gulf Cooperation Council (GCC) nations like the UAE and Saudi Arabia. These projects fuel demand for LED lighting in commercial buildings, hospitality, and municipal applications. However, the market’s progression is uneven. While wealthier Gulf states show a growing appetite for quality and reliable components, broader regional adoption is hindered by economic disparities, a lack of stringent enforcement of energy standards, and a price-sensitive consumer base. The market is currently dominated by basic, imported power supplies, but as awareness of energy savings and total cost of ownership increases, a gradual shift toward more efficient and durable solutions is anticipated over the long term.

Report Scope

This market research report provides a comprehensive analysis of the Global Low Voltage DC-DC LED Power Supplies Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Buck, Boost, Multi-channel, Others), application (LED Lighting, Consumer Electronics, Others), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies, efficiency improvements, and evolving industry standards in DC-DC conversion.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Low Voltage DC-DC LED Power Supplies Market?

-> Low Voltage DC-DC LED Power Supplies Market size was valued at USD 1.23 billion in 2024 and is projected to reach USD 2.05 billion by 2032, exhibiting a CAGR of 6.8% during the forecast period.

Which key companies operate in Global Low Voltage DC-DC LED Power Supplies Market?

-> Key players include Texas Instruments, Linear Technology, Diodes Incorporated, STMicroelectronics, Monolithic Power Systems, Meanwell, Infineon, ON Semiconductor, Richtek, and ISSI, among others.

What are the key growth drivers?

-> Key growth drivers include increasing LED adoption, energy efficiency regulations, and growth in smart lighting solutions.

Which region dominates the market?

-> Asia-Pacific leads in market share due to manufacturing hubs in China and growing LED demand, while North America shows strong technological advancements.

What are the emerging trends?

-> Emerging trends include higher efficiency converters, miniaturization, and integration with IoT-enabled lighting systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...