Low-loss Dielectrics Market Insights

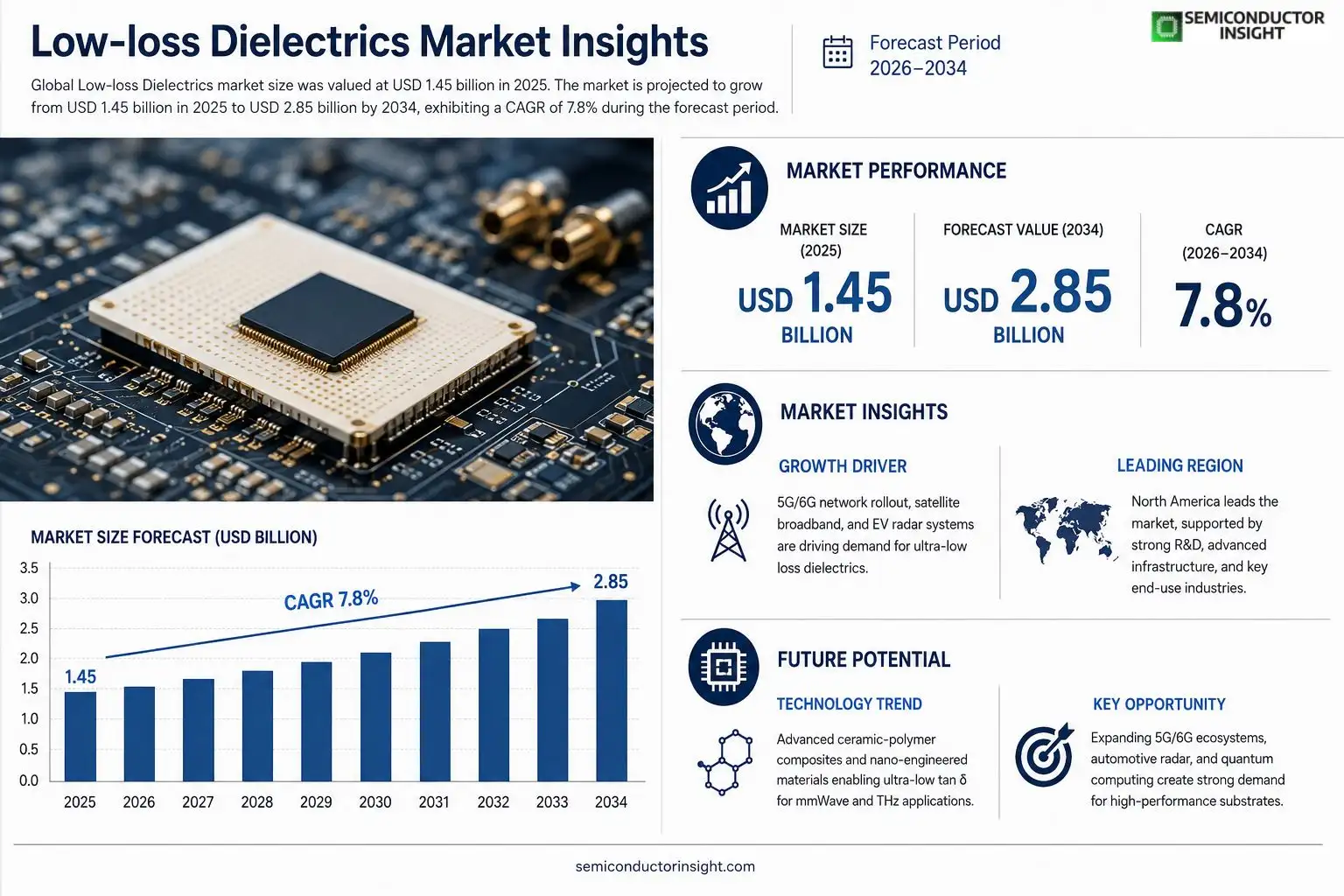

Low-loss Dielectrics market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.45 billion in 2025 to USD 2.85 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period.

Low‑loss dielectrics are engineered insulating materials characterized by a very low dielectric loss tangent (tan δ), enabling minimal signal attenuation at microwave and millimeter‑wave frequencies. They are essential for high‑frequency substrates, antenna radomes, resonators, and advanced capacitors used in telecommunications, aerospace, automotive radar and emerging quantum‑computing hardware.The market is accelerating because the rollout of 5G/6G networks, increasing demand for satellite broadband and electric‑vehicle radar systems drive the need for ultra‑low loss substrates. Furthermore, miniaturization of RF modules and stricter performance standards push manufacturers toward advanced ceramic‑polymer composites. Key players such as Rogers Corporation, TDK Corporation, Murata Manufacturing and Kyocera are expanding their portfolios through R&D investments and strategic partnerships.

MARKET DRIVERS

Growing Demand for High‑Frequency Devices

The rapid expansion of 5G infrastructure and satellite communications is driving high‑performance dielectric materials that can operate at gigahertz frequencies with minimal signal loss. Manufacturers are increasingly specifying low‑loss dielectrics to meet the stringent insertion‑loss requirements of modern RF modules, directly boosting Low‑loss Dielectrics market.

Advancements in Telecommunications Infrastructure

Network operators are deploying dense small‑cell networks, which rely on compact, low‑loss ceramic filters to maintain signal integrity. This technical shift creates a steady pipeline of orders for specialized dielectric compounds, reinforcing market growth across North America, Europe, and Asia‑Pacific.

➤ Industry analysts project a double‑digit CAGR for Low‑loss Dielectrics market through 2032, anchored by telecom and automotive electrification trends.

In parallel, the automotive sector’s transition to electric and autonomous vehicles demands high‑Q resonators for radar and lidar systems. The need for reliable, low‑thermal‑drift materials adds another robust driver to the market’s trajectory.

MARKET CHALLENGES

Stringent Material Certification Requirements

Regulatory bodies in aerospace and medical device manufacturing impose rigorous testing protocols for dielectric materials. Compliance costs can extend product development cycles, discouraging smaller suppliers from entering Low‑loss Dielectrics market.

Other Challenges

Cost Sensitivity

The advanced processing techniques required to achieve ultra‑low loss (e.g., high‑temperature sintering, precision doping) raise the unit cost of dielectric components. End‑users often prioritize cost over marginal performance gains, limiting broader adoption in price‑conscious segments.

MARKET RESTRAINTS

Limited Availability of Ultra‑Pure Raw Materials

Production of low‑loss ceramics relies on high‑purity silica, alumina, and specialty dopants. supply constraints for these feedstocks can slow manufacturing throughput, creating a bottleneck that restrains Low‑loss Dielectrics market, especially during periods of heightened demand.

MARKET OPPORTUNITIES

Emergence of 5G and Beyond

The rollout of 5G, followed by future 6G research, opens a substantial opportunity for low‑loss dielectric components in massive MIMO arrays, phased‑array antennas, and millimeter‑wave filters. Companies that invest in scalable production methods stand to capture a significant share of this expanding demand.

Low-loss Dielectrics Market Trends

Surge in High‑Frequency Connectivity Drives Demand

The rollout of 5G and early 6G pilots is reshaping the telecommunications landscape, creating a robust need for substrates that preserve signal integrity at millimeter‑wave frequencies. Low‑loss dielectrics, with dielectric loss tangents well below 0.001, meet this requirement by minimizing attenuation across the 24 GHz to 100 GHz bands. Market data shows that the sector grew from USD 1.45 billion in 2025 to a projected USD 2.85 billion by 2034, reflecting a compound annual growth of roughly 7.8 percent. This expansion is anchored by the migration of mobile operators toward dense small‑cell deployments and the parallel rise of satellite broadband constellations, both of which rely on ultra‑low loss materials for antenna radomes and high‑performance filters.

Other Trends

Material Innovation and Composite Engineering

Manufacturers are accelerating R&D on ceramic‑polymer hybrid composites that combine the thermal stability of ceramics with the processing flexibility of polymers. Companies such as Rogers Corporation and TDK have announced new product lines that incorporate nano‑structured alumina particles, delivering dielectric constants between 3.5 and 4.5 while keeping tan δ below 0.0008. These advances enable thinner, lighter RF modules for automotive radar and emerging quantum‑computing hardware, where loss budgets are extremely tight.

Strategic Partnerships and Portfolio Diversification

Key players are extending their market reach through alliances with chipset manufacturers and defense contractors. Murata Manufacturing and Kyocera have entered joint development agreements to co‑design dielectric substrates that are compatible with next‑generation silicon‑photonic transceivers. The strategic focus on co‑optimization of material properties and device architecture reduces time‑to‑market and reinforces the competitive advantage of firms that can deliver turnkey solutions for high‑frequency applications.

COMPETITIVE LANDSCAPEKey Industry Players

Low‑loss Dielectrics Market Competitive Overview

Low‑loss Dielectrics market is dominated by a handful of large technology manufacturers that have built extensive RF‑substrate and advanced ceramic‑polymer portfolios. Rogers Corporation leads with a strong presence in 5G antenna radomes and aerospace‑grade resonators, leveraging its proprietary “Rogers RT” family to capture premium pricing. TDK Corporation, through its EPCOS subsidiary, offers a broad spectrum of ceramic and polymer dielectrics, anchoring its market share in automotive radar and satellite communications. Murata Manufacturing and Kyocera Corp. complement the top tier with aggressive R&D pipelines focused on ultra‑low tan δ materials, enabling high‑frequency modules for quantum‑computing and millimeter‑wave applications. Collectively, these four firms account for roughly 55 % of revenue, and their strategic partnerships with chipset producers reinforce a consolidated supply chain that shapes pricing and technology standards.Niche yet strategically important players enrich the competitive landscape with specialised chemistries and regional strengths. AVX Corporation supplies low‑loss polymer blends for consumer electronics, while Sumitomo Chemical and Mitsubishi Gas Chemical differentiate through proprietary fluoropolymer formulations targeting automotive radar. CeramTec GmbH and Cooper Advanced Materials excel in high‑performance ceramic composites for aerospace radomes. Additional contributors such as Taiyo Yuden, Fujitsu, Arlon LLC, and 3M provide niche portfolio extensions that support miniaturised RF modules and emerging 6G prototypes, ensuring a diversified ecosystem that can respond quickly to evolving performance specifications.

List of Key Low-loss Dielectrics Companies Profiled

- Rogers Corporation

- TDK Corporation

- Murata Manufacturing

- Kyocera Corp.

- AVX Corporation

- EPCOS (TDK Group)

- Sumitomo Chemical Co., Ltd.

- CeramTec GmbH

- Cooper Advanced Materials

- Mitsubishi Gas Chemical Company

- Taiyo Yuden Co., Ltd.

- Fujitsu Limited

- Arlon LLC

- 3M Company

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ceramic‑Polymer Composites are the primary growth driver because they marry the ultra‑low loss of ceramics with the processing flexibility of polymers.

|

| By Application |

|

High‑Frequency Substrates dominate application focus as they are indispensable for the next‑generation telecom infrastructure.

|

| By End User |

|

Telecommunications Infrastructure remains the leading end‑user segment, reflecting the massive rollout of high‑frequency networks.

|

| By Material Composition |

|

Oxide‑Based Ceramics are the most established composition, valued for intrinsic low loss and thermal resilience.

|

| By Frequency Range |

|

Millimeter‑Wave applications are emerging as the key demand catalyst, especially for next‑gen radar and wireless links.

|

Regional Analysis: North America

United States

The telecommunications sector remains a primary driver for low-loss dielectrics, fueled by the ongoing rollout of 5G networks and the increasing bandwidth demands. This necessitates materials with exceptionally low signal loss at higher frequencies.

The aerospace and defense industries utilize low-loss dielectrics in radar systems, avionics, and satellite communication equipment. The stringent performance requirements and reliability demands of these applications are key market drivers.

Advancements in consumer electronics, including smartphones, tablets, and wireless devices, are driving demand for miniaturized and high-performance low-loss dielectrics to enhance device functionality and energy efficiency.

The growing complexity of automotive electronic systems, particularly with the rise of electric vehicles and advanced driver-assistance systems (ADAS), is creating new opportunities for low-loss dielectrics in power electronics and sensor applications.

Europe

Europe exhibits a steady demand for low-loss dielectrics, driven by established industries and a focus on technological advancements. The automotive sector, particularly in Germany and France, is a significant consumer. Furthermore, the strong presence of aerospace and telecommunications companies in several European countries contributes to the market’s sustained growth. Regulatory initiatives promoting energy efficiency and sustainable technologies are also influencing the adoption of low-loss dielectric materials. Business strategies in Europe often emphasize collaboration with research institutions and a focus on developing eco-friendly and high-performance solutions. The market is characterized by a mature and competitive landscape, with key players focusing on innovation and customized offerings to cater to specific regional needs. Low-loss Dielectrics Market in Europe presents a stable, albeit moderate, growth opportunity.

Asia-Pacific

Asia-Pacific is emerging as a high-growth region for Low-loss Dielectrics Market. Rapid industrialization, particularly in China and Southeast Asia, coupled with increasing investments in telecommunications infrastructure and electronics manufacturing, are fueling demand. The burgeoning consumer electronics market and the strong growth of the electric vehicle industry in countries like China are further contributing to this expansion. Business strategies in the Asia-Pacific region often involve cost-effective manufacturing and catering to the needs of local electronics manufacturers. While competition is intensifying, the large and expanding market offers significant potential for growth. The focus is on providing competitively priced solutions while maintaining quality standards. Low-loss Dielectrics Market in Asia-Pacific is anticipated to witness robust growth over the coming years.

South America

South America represents a smaller but gradually expanding market for low-loss dielectrics. The growth is primarily driven by the increasing adoption of telecommunications technologies and the expansion of the electronics sector in countries like Brazil and Argentina. Investments in infrastructure development and the rising demand for consumer electronics are key market drivers. Business strategies in South America often focus on establishing local partnerships and providing tailored solutions to meet the specific needs of regional industries. While the market is still relatively nascent, it presents opportunities for growth as the region continues to develop and industrialize.

Middle East & Africa

The Middle East and Africa represent a developing market for low-loss dielectrics, with growth driven by infrastructure development projects, particularly in telecommunications and energy sectors. Increasing investments in 5G networks and the expansion of the consumer electronics market are contributing to demand. The region’s focus on technological advancement and increasing government spending on infrastructure are expected to further drive market growth. Business strategies in this region often involve adapting to local regulations and building strong relationships with key stakeholders. While the market is currently smaller compared to other regions, it holds significant potential for future expansion.

Report Scope

This market research report provides a comprehensive analysis of the Low-loss Dielectrics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Low-loss Dielectrics Market?

-> Low-loss Dielectrics Market was valued at USD 1.45 billion in 2025 and is expected to reach USD 2.85 billion by 2034, exhibiting a CAGR of 7.8% during the forecast period.

Which key companies operate in Low-loss Dielectrics Market?

-> Key players include Rogers Corporation, TDK Corporation, Murata Manufacturing, and Kyocera, among others.

What are the key growth drivers?

-> Key growth drivers include the rollout of 5G/6G networks, increasing demand for satellite broadband, electric‑vehicle radar systems, miniaturization of RF modules, and stricter performance standards.

Which region dominates the market?

-> North America and Europe remain leading markets, while Asia‑Pacific is experiencing rapid growth due to strong telecommunications investments.

What are the emerging trends?

-> Emerging trends include advanced ceramic‑polymer composite substrates, continued module miniaturization, and heightened performance specifications for ultra‑low loss applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...