MARKET INSIGHTS

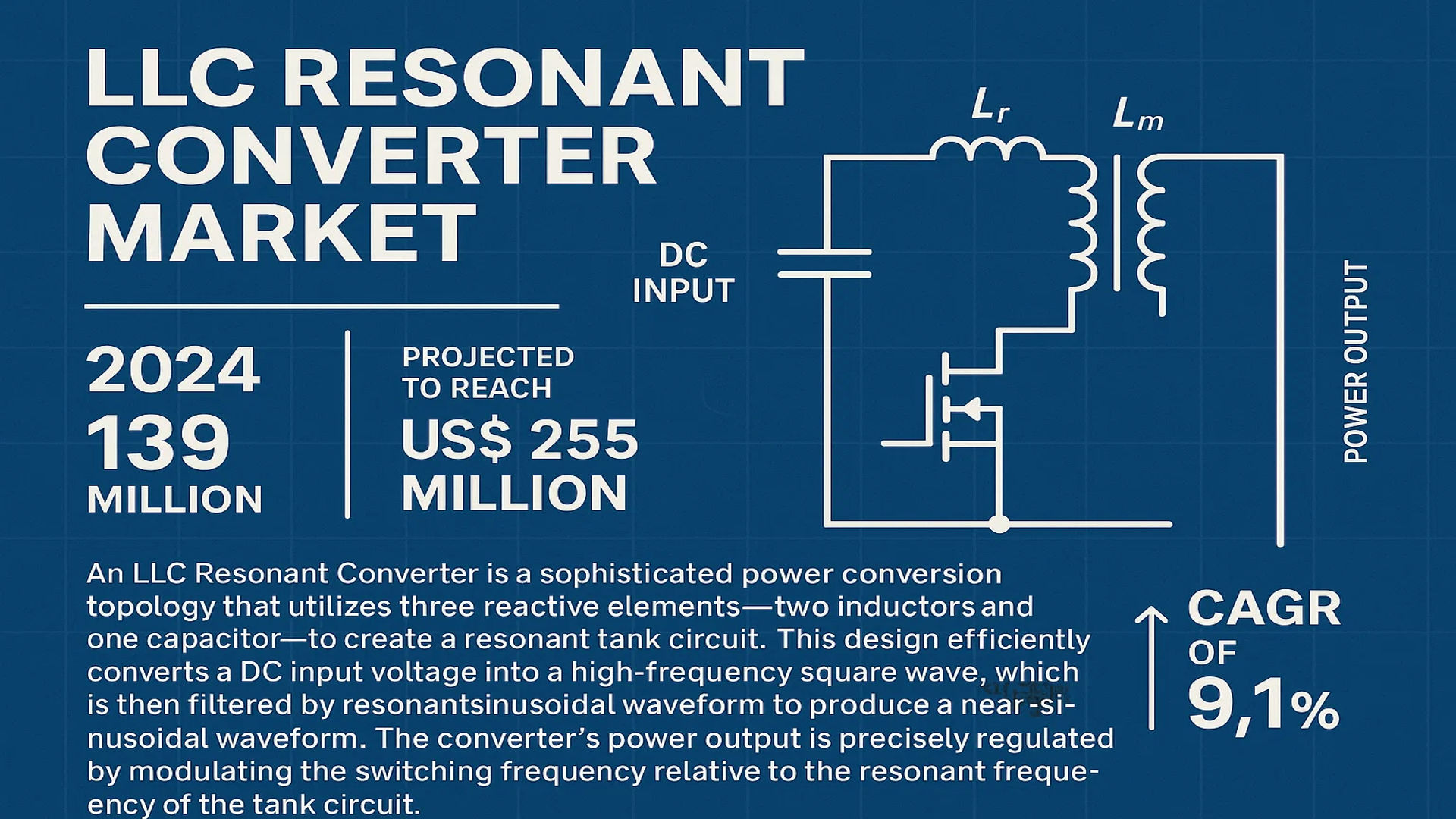

The global LLC Resonant Converter Market was valued at 139 million in 2024 and is projected to reach US$ 255 million by 2032, at a CAGR of 9.1% during the forecast period.

An LLC Resonant Converter is a sophisticated power conversion topology that utilizes three reactive elements—two inductors and one capacitor—to create a resonant tank circuit. This design efficiently converts a DC input voltage into a high-frequency square wave, which is then filtered by the resonant network to produce a near-sinusoidal waveform. This waveform feeds an isolation transformer, enabling both voltage scaling and critical safety isolation. The converter’s power output is precisely regulated by modulating the switching frequency relative to the resonant frequency of the tank circuit.

The market’s robust growth is primarily driven by the escalating demand for high-efficiency, high-power-density power supplies across several key industries. The rapid expansion of the electric vehicle (EV) sector, which requires efficient onboard chargers and auxiliary power modules, is a major contributor. Furthermore, the relentless growth of data centers and 5G communication infrastructure necessitates advanced server and telecom power supplies where LLC converters excel due to their superior efficiency and low electromagnetic interference (EMI). While adoption is slower in mature segments like lighting and industrial power, the overall market trajectory remains strongly positive, supported by continuous technological advancements from leading semiconductor manufacturers.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Efficiency Power Conversion Solutions to Propel Market Growth

The global LLC resonant converter market is experiencing robust growth driven by the increasing demand for high-efficiency power conversion solutions across multiple industries. LLC resonant converters offer superior performance with efficiencies reaching up to 98%, significantly higher than traditional hard-switching converters which typically operate at 85-92% efficiency. This efficiency advantage translates to reduced energy losses and lower operating costs, making them particularly attractive for applications where energy conservation is critical. The electric vehicle sector, which requires highly efficient onboard chargers and DC-DC converters, represents one of the fastest-growing application segments, with global electric vehicle sales projected to exceed 17 million units annually by 2024. Additionally, the expanding data center infrastructure, driven by cloud computing and digital transformation initiatives, demands power supplies with higher power density and improved thermal management, further accelerating adoption of LLC resonant converter technology.

Growing Adoption in Renewable Energy Systems to Boost Market Expansion

The renewable energy sector’s rapid expansion is creating substantial opportunities for LLC resonant converters, particularly in solar inverters and energy storage systems. With global solar photovoltaic capacity expected to reach 2.3 terawatts by 2030, the demand for efficient power conversion solutions has never been greater. LLC resonant converters provide excellent performance in maximum power point tracking (MPPT) applications and offer reduced electromagnetic interference, which is crucial for grid-connected systems. The technology’s ability to maintain high efficiency across wide input voltage ranges makes it ideal for solar applications where input voltage can vary significantly based on environmental conditions. Furthermore, the increasing deployment of energy storage systems, projected to grow at a compound annual growth rate of over 20% through 2030, requires advanced power conversion technologies that can handle bidirectional power flow with minimal losses, positioning LLC resonant converters as a preferred solution.

Advancements in Semiconductor Technology to Drive Performance Improvements

Recent advancements in wide-bandgap semiconductors, particularly silicon carbide (SiC) and gallium nitride (GaN) technologies, are significantly enhancing the performance capabilities of LLC resonant converters. These materials enable operation at higher switching frequencies, typically ranging from 100 kHz to 1 MHz, compared to traditional silicon-based converters that operate at 50-100 kHz. The higher switching frequencies allow for reduced size of magnetic components, with power density improvements of up to 30-40% compared to conventional designs. The global market for SiC power devices is growing at approximately 25% annually, driven by their superior thermal performance and reduced switching losses. Manufacturers are increasingly integrating these advanced semiconductor technologies into LLC resonant converter designs, resulting in products that offer higher efficiency, smaller form factors, and improved thermal management. This technological evolution is particularly important for applications such as server power supplies and electric vehicle charging systems, where space constraints and thermal performance are critical design considerations.

MARKET RESTRAINTS

Complex Design and Implementation Challenges to Hinder Market Penetration

Despite their performance advantages, LLC resonant converters face significant design and implementation challenges that restrain market growth. The complex control requirements and precise component selection needed for optimal operation present substantial barriers to widespread adoption. Designing an LLC resonant converter requires careful consideration of multiple parameters including transformer turns ratio, resonant inductance, and magnetizing inductance, with even minor deviations potentially leading to suboptimal performance or operational instability. The need for specialized magnetic components with tight tolerances increases manufacturing complexity and cost, with custom magnetics typically accounting for 20-30% of the total converter cost. Additionally, the nonlinear behavior of the resonant tank necessitates advanced control algorithms and sophisticated gate drive circuits, requiring engineering expertise that is not always readily available in the market. These technical complexities often lead to longer development cycles and higher engineering costs, particularly for small and medium-sized manufacturers who may lack the necessary resources and expertise.

Higher Component Costs and Supply Chain Constraints to Limit Market Expansion

The LLC resonant converter market faces significant cost-related restraints due to the premium components required for optimal performance. The technology typically utilizes higher-quality capacitors, specialized magnetic materials, and advanced semiconductor devices that command price premiums of 15-40% compared to components used in conventional converters. The global semiconductor shortage that began in 2020 has particularly affected the availability and pricing of MOSFETs and controllers specifically designed for resonant converter applications, with lead times extending to 40-50 weeks in some cases. This supply chain disruption has increased manufacturing costs and delayed product development timelines across the industry. Furthermore, the ongoing transition to wide-bandgap semiconductors, while offering performance benefits, introduces additional cost pressures as these materials currently carry price premiums of 2-3 times compared to silicon-based alternatives. These cost factors make LLC resonant converters less competitive in price-sensitive applications and emerging markets where cost considerations often outweigh performance advantages.

Limited Standardization and Compatibility Issues to Restrain Market Growth

The lack of industry-wide standardization presents a significant restraint for the LLC resonant converter market. Unlike traditional PWM converters that have established design guidelines and component standards, LLC resonant converter designs vary considerably between manufacturers and applications. This variability creates compatibility issues and increases the engineering effort required for system integration. The absence of standardized control interfaces and communication protocols makes it challenging to implement advanced features such as digital control, monitoring, and system-level optimization. Additionally, the wide range of operating requirements across different applications—from low-power consumer electronics to high-power industrial systems—has led to fragmented product offerings that lack interoperability. This lack of standardization not only increases development costs but also limits the ability to achieve economies of scale in component manufacturing, ultimately keeping prices higher than they might be in a more standardized market environment.

MARKET CHALLENGES

Thermal Management and Reliability Concerns to Challenge Widespread Adoption

The market faces significant thermal management challenges despite the inherent efficiency advantages of LLC resonant converters. While soft-switching operation reduces switching losses, the converters still generate substantial heat during operation, particularly in high-power applications. The power density improvements achieved through higher switching frequencies often come at the cost of increased thermal challenges, with heat flux densities reaching 50-100 W/cm² in advanced designs. Managing these thermal loads requires sophisticated cooling solutions that can account for 20-35% of the total system cost. Reliability concerns also present challenges, as the complex interaction between resonant components and semiconductor devices can lead to unexpected failure modes. The operating lifetime of electrolytic capacitors used in resonant converters remains a particular concern, with typical lifetimes of 5-7 years compared to 10-15 years for the overall system. These reliability issues become especially critical in applications such as data centers and medical equipment where uninterrupted operation is essential.

Other Challenges

Electromagnetic Compatibility Requirements

Meeting stringent electromagnetic compatibility (EMC) standards presents ongoing challenges for LLC resonant converter manufacturers. While resonant converters generally produce lower electromagnetic interference than hard-switching alternatives, the high-frequency operation and complex waveforms still require careful filtering and shielding. Compliance with international standards such as CISPR 32 and FCC Part 15 often necessitates additional components and design modifications that increase cost and complexity. The evolving regulatory landscape, particularly for automotive and medical applications, requires continuous design updates and retesting, adding to development costs and time-to-market.

Software and Control Algorithm Complexity

The sophisticated control algorithms required for optimal LLC resonant converter operation present significant software development challenges. Implementing advanced features such as frequency modulation, burst mode operation, and adaptive dead-time control requires specialized digital signal processing expertise. The development and validation of these control algorithms typically account for 30-40% of the total engineering effort in converter design. Additionally, the need for real-time performance optimization across varying load conditions demands continuous algorithm refinement and testing, creating ongoing engineering challenges even after product release.

MARKET OPPORTUNITIES

Expansion in Electric Vehicle Infrastructure to Create Substantial Growth Opportunities

The rapid global expansion of electric vehicle infrastructure presents significant opportunities for LLC resonant converter manufacturers. The growing network of EV charging stations, particularly fast-charging infrastructure requiring power levels of 150-350 kW, demands highly efficient and compact power conversion solutions. LLC resonant converters are particularly well-suited for these applications due to their high efficiency across wide load ranges and excellent thermal performance. With global investments in EV charging infrastructure projected to exceed $90 billion by 2027, the demand for advanced power conversion technologies is expected to grow substantially. Additionally, the increasing adoption of wireless charging systems for electric vehicles, which typically operate at 85-90% efficiency, represents another promising application area where LLC resonant converter technology can provide performance advantages. The development of bidirectional charging capabilities, enabling vehicle-to-grid applications, further expands the potential market for advanced resonant converter solutions that can efficiently handle power flow in both directions.

5G Infrastructure Deployment to Drive Demand for Advanced Power Solutions

The global rollout of 5G networks is creating substantial opportunities for LLC resonant converters in telecommunications power supplies. 5G infrastructure requires power systems that can deliver higher power density, improved efficiency, and enhanced thermal performance compared to previous generations. Base station power requirements have increased to 5-10 kW per unit, with efficiency targets exceeding 96% to reduce operational costs and environmental impact. LLC resonant converters are ideally positioned to meet these requirements, offering the necessary combination of high efficiency and power density. The global 5G infrastructure market is expected to grow at a compound annual growth rate of over 45% through 2030, driving corresponding demand for advanced power conversion solutions. Additionally, the deployment of edge computing infrastructure and small cell networks as part of 5G implementation creates further opportunities for compact, efficient power supplies utilizing LLC resonant technology.

Industrial Automation and IoT Expansion to Fuel Market Growth

The ongoing expansion of industrial automation and Internet of Things (IoT) applications presents significant growth opportunities for LLC resonant converters. Industrial equipment increasingly requires power supplies that can operate reliably in harsh environments while maintaining high efficiency across varying load conditions. The global industrial automation market is projected to grow at approximately 9% annually, driven by Industry 4.0 initiatives and smart manufacturing adoption. LLC resonant converters offer advantages in these applications due to their robust operation, reduced electromagnetic interference, and ability to maintain efficiency across wide input voltage ranges. Similarly, the proliferation of IoT devices, expected to exceed 30 billion connected devices globally by 2025, requires efficient power management solutions that can extend battery life and reduce energy consumption. While many IoT applications currently use simpler converter topologies, the increasing power requirements of advanced IoT devices are creating opportunities for more efficient solutions, including LLC resonant converters in higher-power edge computing applications.

LLC RESONANT CONVERTER MARKET TRENDS

Rising Demand for High-Efficiency Power Conversion in Electric Vehicles and Data Centers

The global LLC resonant converter market is experiencing significant growth driven primarily by the escalating demand for high-efficiency power conversion solutions in electric vehicles (EVs) and data center infrastructure. The inherent advantages of LLC topologies, such as zero-voltage switching (ZVS) and zero-current switching (ZCS), result in exceptionally high efficiency, often exceeding 95%, and reduced electromagnetic interference (EMI). This is critically important for EV onboard chargers (OBCs) and server power supplies, where thermal management and power density are paramount constraints. The global EV market, projected to surpass 30 million units annually by 2030, is a primary catalyst, as automakers seek to minimize charging losses and extend vehicle range. Concurrently, the exponential growth in data consumption, necessitating more powerful and denser server racks, is pushing the adoption of these converters in communication power supplies. This trend is further amplified by global initiatives for energy efficiency, making the high-performance characteristics of LLC resonant converters not just preferable but essential for next-generation power electronics.

Other Trends

Technological Miniaturization and Integration

A pivotal trend shaping the market is the relentless drive towards miniaturization and higher levels of integration. Manufacturers are increasingly developing high-frequency GaN (Gallium Nitride) and SiC (Silicon Carbide) based LLC converters that operate efficiently at switching frequencies above 500 kHz. This allows for a dramatic reduction in the size of passive magnetic components, such as transformers and inductors, which are traditionally the bulkiest parts of a power supply. The ability to achieve power densities greater than 100 W/in³ is becoming a standard requirement in advanced applications, particularly in telecommunications and computing hardware. This miniaturization is crucial for modern electronics, enabling sleeker EV designs and more compact, high-capacity server blades that can fit within existing infrastructure footprints without compromising on performance or thermal output.

Expansion into Industrial Automation and Renewable Energy Systems

Beyond consumer electronics and IT, the LLC resonant converter is finding robust new applications in industrial automation and renewable energy systems. The industrial sector’s shift towards Industry 4.0 and smart manufacturing relies on highly reliable and efficient power conversion for motor drives, robotics, and PLC systems. The soft-switching特性 of LLC converters significantly reduces stress on components, leading to longer lifespans and higher reliability in harsh industrial environments. Furthermore, the renewable energy sector, particularly solar microinverters and energy storage systems (ESS), presents a substantial growth opportunity. These systems require inverters and converters that can handle wide input voltage ranges with high efficiency to maximize energy harvest and storage effectiveness. The capability of LLC topologies to maintain high efficiency across a load range aligns perfectly with the variable nature of solar power generation, making them an increasingly favored technology in this green transition.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Expansion to Maintain Market Position

The global LLC Resonant Converter market exhibits a semi-consolidated competitive structure, characterized by the presence of established semiconductor giants alongside specialized power electronics firms. Infineon Technologies AG and Texas Instruments Incorporated are recognized as dominant forces, collectively accounting for a significant portion of the market share. Their leadership is underpinned by extensive R&D investments, broad product portfolios covering both half-bridge and full-bridge topologies, and robust global distribution networks that serve key high-growth sectors like electric vehicles and data center power supplies.

ON Semiconductor and STMicroelectronics also command considerable market influence, driven by their focus on energy-efficient solutions and strong relationships with automotive and industrial OEMs. These companies have successfully leveraged the transition towards higher efficiency power conversion, with their LLC resonant converter ICs and modules being widely adopted in applications requiring high power density and low electromagnetic interference (EMI).

Growth strategies in this market are predominantly centered on technological differentiation and geographic expansion. Recent developments include the introduction of integrated solutions that combine controllers, gate drivers, and MOSFETs into single packages, reducing system size and complexity for customers. Furthermore, companies are actively forming strategic partnerships with automotive tier-1 suppliers and server manufacturers to design-in their components for next-generation platforms.

Meanwhile, players like ROHM Semiconductor and Power Integrations, Inc. are strengthening their positions through specialized, high-performance product lines. ROHM’s focus on silicon carbide (SiC) technology enhances the efficiency of LLC converters in high-power applications, while Power Integrations’ innovative FluxLink feedback technology simplifies isolated power supply designs. These focused innovations allow them to compete effectively despite the scale of larger rivals, particularly in niche segments requiring ultra-high efficiency or specific form factors.

List of Key LLC Resonant Converter Companies Profiled

- Infineon Technologies AG (Germany)

- Texas Instruments Incorporated (U.S.)

- ON Semiconductor (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Wolfspeed, Inc. (U.S.)

- ROHM Semiconductor (Japan)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Efficient Power Conversion Corporation (EPC) (U.S.)

- Power Integrations, Inc. (U.S.)

Segment Analysis:

By Type

Half-Bridge Topology Dominates the Market Due to Cost-Effectiveness in Medium-Power Applications

The market is segmented based on type into:

- Full-bridge

- Half-bridge

By Application

Electric Vehicle Power Supply Segment Leads Due to Rapid Electrification and Demand for High-Efficiency Converters

The market is segmented based on application into:

- Electric Vehicle Power Supply

- Communication Power Supply

- Lighting Power Supply

- Industrial Power Supply

- Others

By Power Rating

High-Power Segment Shows Strong Growth Driven by Demands from Data Centers and Industrial Automation

The market is segmented based on power rating into:

- Low Power (<1kW)

- Medium Power (1kW-3kW)

- High Power (>3kW)

By End-User Industry

Automotive and Telecommunications Sectors Exhibit Highest Adoption Rates for LLC Resonant Converters

The market is segmented based on end-user industry into:

- Automotive

- Telecommunications

- Industrial Manufacturing

- Consumer Electronics

- Others

Regional Analysis: LLC Resonant Converter Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global LLC Resonant Converter market, accounting for over 45% of the total market share by volume. This leadership is primarily driven by the massive manufacturing hubs in China, Taiwan, and South Korea, which serve the world’s consumer electronics and communication equipment sectors. The rapid proliferation of 5G infrastructure, with China alone deploying over 2.17 million 5G base stations by the end of 2023, creates immense demand for high-efficiency communication power supplies utilizing LLC topologies. Furthermore, the region is the epicenter of electric vehicle production, with leading battery and charger manufacturers integrating LLC converters to achieve the high power density and efficiency required for fast-charging applications. While cost-competitive half-bridge designs prevail for mid-power applications, the push towards higher power levels in servers and EVs is steadily increasing the adoption of full-bridge configurations. The concentration of major semiconductor fabs and passive component manufacturers within the region also provides a robust and integrated supply chain, fostering innovation and cost-effectiveness.

North America

North America represents a highly advanced and innovation-driven market for LLC Resonant Converters, characterized by a strong emphasis on research and development. The region’s growth is heavily fueled by the expansive data center and cloud computing industry, where power efficiency and density are paramount. Major hyperscalers’ commitments to carbon neutrality are accelerating the adoption of advanced power conversion technologies like LLC resonant converters in server power supplies. The electric vehicle revolution, led by companies like Tesla and supported by government incentives under policies such as the Inflation Reduction Act, is another critical driver. North American design centers are at the forefront of developing high-power, full-bridge LLC solutions for EV charging infrastructure and onboard chargers. Stringent energy efficiency standards, such as the U.S. Department of Energy’s regulations for external power supplies, further mandate the use of such high-efficiency topologies, ensuring sustained market demand.

Europe

The European market for LLC Resonant Converters is shaped by rigorous environmental regulations and a strong industrial base. The EU’s Ecodesign Directive and energy efficiency standards compel manufacturers to adopt topologies that minimize energy loss, making the LLC converter a preferred choice for consumer electronics, industrial power supplies, and lighting applications. The region’s ambitious green deal and focus on renewable energy integration are driving the need for efficient power conversion in solar inverters and energy storage systems, where LLC converters are increasingly being evaluated. Furthermore, Europe’s automotive industry, with its rapid transition to electric mobility, presents a significant opportunity. German and French automotive OEMs and tier-1 suppliers are integrating LLC converters into their powertrains and charging systems to meet high performance and reliability standards. While the market is mature and values quality over cost, it shows steady growth aligned with the region’s sustainability goals.

South America

The South American market for LLC Resonant Converters is nascent but shows potential for gradual growth. The primary demand stems from the consumer electronics sector and the gradual modernization of industrial equipment. However, economic volatility and currency fluctuations often prioritize cost-effective solutions, which can slow the adoption of newer, sometimes more expensive, power conversion technologies. The industrial power supply segment offers the most stable demand, as manufacturers seek to improve efficiency to reduce operational costs. The adoption in high-growth areas like electric vehicles and data centers is still in very early stages, limited by slower infrastructure development and investment compared to other regions. Market growth is therefore expected to be moderate, following the broader economic recovery and industrial development trends across key countries like Brazil and Argentina.

Middle East & Africa

The market in the Middle East and Africa is emerging, with development currently focused on specific sectors and nations. Investments in telecommunications infrastructure, particularly in Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE, are generating demand for efficient power supplies for 5G network equipment, which utilizes LLC converters. The region’s push towards economic diversification and smart city initiatives also creates long-term opportunities in the industrial and commercial sectors. However, the market faces challenges, including a reliance on imported technology, limited local manufacturing capabilities for advanced electronics, and budget constraints that often favor lower-cost alternatives. While the overall penetration of LLC resonant technology is low, the region’s ongoing infrastructure development projects present a future growth avenue, albeit one that will evolve slowly compared to global trends.

Report Scope

This market research report provides a comprehensive analysis of the global LLC Resonant Converter market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LLC Resonant Converter Market?

-> LLC Resonant Converter Market was valued at 139 million in 2024 and is projected to reach US$ 255 million by 2032, at a CAGR of 9.1% during the forecast period.

Which key companies operate in Global LLC Resonant Converter Market?

-> Key players include ON Semiconductor, Wolfspeed, STMicroelectronics, Infineon, Texas Instruments, ROHM, Toshiba, EPC, and Power Integrations, Inc., among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-efficiency power supplies in electric vehicles, expansion of data centers and communication infrastructure, and the need for compact, high-power-density solutions.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing region, driven by manufacturing hubs and strong demand from the electric vehicle and consumer electronics sectors.

What are the emerging trends?

-> Emerging trends include integration of wide-bandgap semiconductors (SiC and GaN), development of digital control ICs for enhanced performance, and increasing adoption in renewable energy systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...