Linear-in-dB variable gain amplifier for phased-array beamformers Market Insights

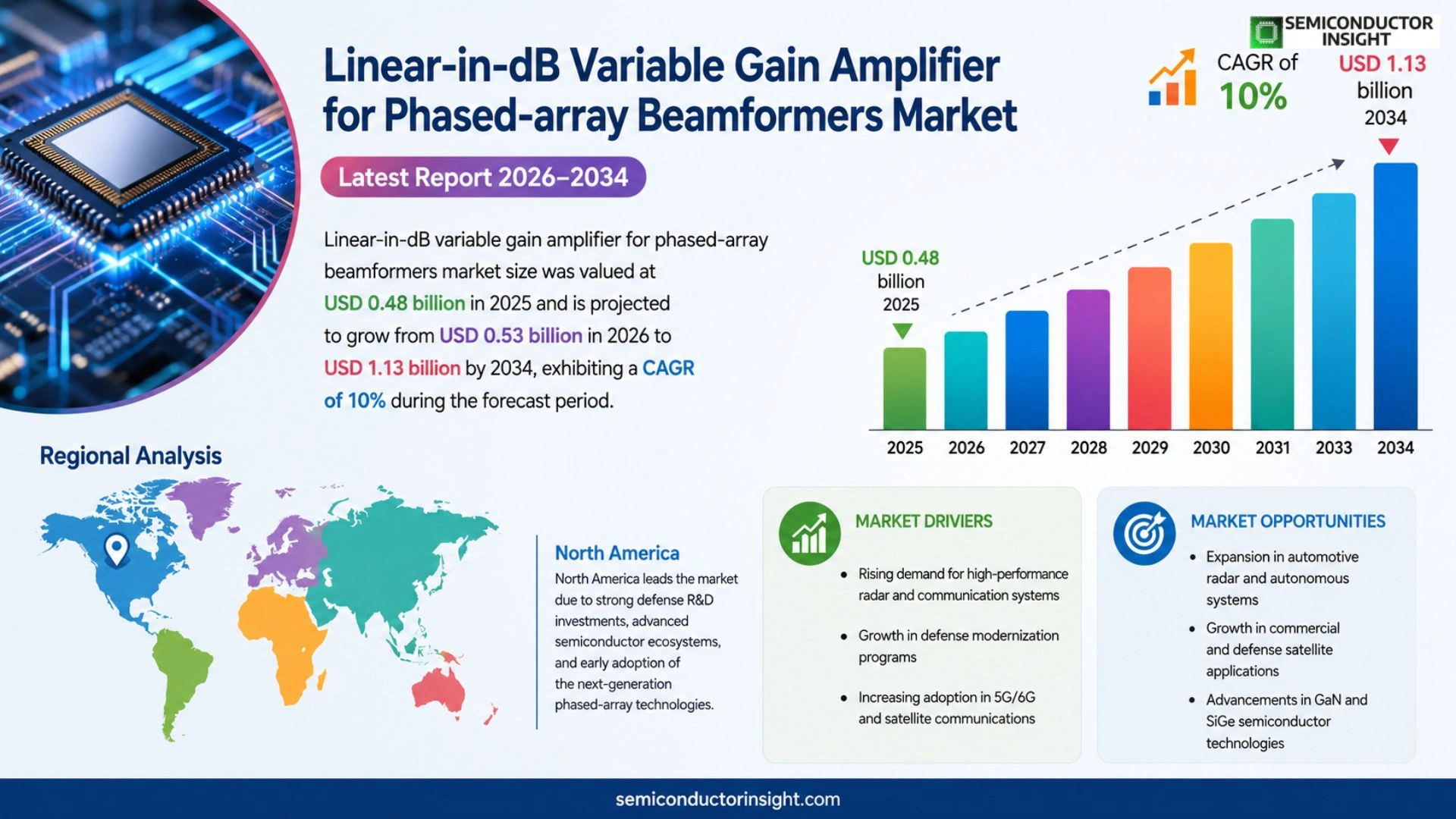

Global Linear-in-dB variable gain amplifier for phased-array beamformers market is projected to grow from USD 0.48 billion in 2025 to USD 1.13 billion by 2034, exhibiting a CAGR of 10% during the forecast period.

Linear‑in‑dB variable gain amplifiers (VGAs) are precision RF components that provide a controllable gain expressed directly in decibels, enabling fine‑grained amplitude adjustment across wide bandwidths required by modern phased‑array beamforming systems.

The market is gaining momentum because defense radar modernization programs demand higher‑resolution beam steering, while commercial telecommunications adopt massive MIMO architectures that rely on accurate gain control.

Furthermore, advances in silicon‑on‑insulator (SOI) processes reduce power consumption, making VGAs attractive for satellite payloads.

Key players such as Analog Devices, Texas Instruments, Qorvo and Skyworks are expanding their product portfolios through recent launches of ultra‑low‑noise linear‑in‑dB VGAs optimized for mmWave frequencies.

MARKET DRIVERS

Increasing Demand for High‑Performance Radar and 5G Systems

The rapid deployment of 5G infrastructure and advanced radar solutions for autonomous vehicles is driving the need for precise gain control. Linear‑in‑dB variable gain amplifiers enable seamless beam steering, which is critical for maintaining signal integrity across wide frequency bands.

Miniaturization and Power‑Efficiency Trends

Manufacturers are focusing on reducing the footprint of phased‑array modules while improving power efficiency. Modern CMOS and SiGe processes allow linear gain modulation with less heat dissipation, supporting longer operational lifetimes in airborne and space‑borne platforms.

➤ “The ability to achieve sub‑dB gain steps directly translates to finer angular resolution, a key competitive edge for defense and telecommunications suppliers.”

These technological advances, combined with government funding for next‑generation communication, are expected to raise the addressable market size by double‑digits over the next five years.

MARKET CHALLENGES

Complex Design Integration

Integrating linear‑in‑dB gain stages with existing RF front‑ends requires meticulous layout to avoid parasitic effects. The limited availability of designers proficient in both analog and digital calibration adds to project timelines and costs.

Other Challenges

Manufacturing Yield

Achieving consistent linearity across large wafer volumes remains a hurdle, especially for high‑frequency (>30 GHz) implementations where process variations can cause gain ripple.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying state‑of‑the‑art variable gain amplifiers in phased‑array platforms involves substantial upfront investment in design tools, test equipment, and low‑volume production runs, which can deter smaller OEMs from early adoption.

MARKET OPPORTUNITIES

Emerging Satellite Constellations

The surge in low‑Earth orbit (LEO) satellite constellations creates a demand for compact, high‑gain linear amplifiers capable of rapid beam re‑pointing. These systems benefit directly from the fine‑grained control offered by Linear-in-dB variable gain amplifier for phased‑array beamformers Market.

Advanced Calibration Algorithms

Machine‑learning‑based calibration techniques are emerging, allowing real‑time compensation of gain non‑linearity. Companies that integrate these algorithms with hardware can capture a sizable share of the growing market.

Linear-in-dB variable gain amplifier for phased-array beamformers Market Trends

Defense Radar Modernization Fuels Growth

Linear-in-dB variable gain amplifier for phased-array beamformers Market is experiencing a clear lift as defense radar modernization programs prioritize higher‑resolution beam steering. Modern phased‑array architectures require precise, decibel‑scaled gain control to maintain signal fidelity across wide bandwidths, and linear‑in‑dB VGAs meet this need without sacrificing linearity. Simultaneously, commercial telecommunications adopters are deploying massive MIMO systems that depend on accurate amplitude adjustment for each antenna element, further expanding demand. Advances in silicon‑on‑insulator (SOI) manufacturing have reduced power consumption, making these amplifiers attractive for satellite payloads where efficiency is critical. Collectively, these forces generate a sustained upward trajectory for the market.

Other Trends

Commercial Telecommunications Adoption

Within the commercial sector, operators are scaling up mmWave deployments to support 5G and beyond. The requirement for fine‑grained gain tuning aligns directly with the capabilities of linear‑in‑dB VGAs, enabling dense antenna arrays to achieve consistent coverage and reduced interference. Moreover, the shift toward open‑radio access networks encourages component standardization, prompting vendors to integrate low‑noise, high‑linearity amplifiers into reference designs. This trend not only accelerates time‑to‑market for new base stations but also drives competitive pricing, reinforcing the market’s expansion.

Technology Integration and Process Innovation

Process innovation is a secondary catalyst for Linear-in-dB variable gain amplifier for phased-array beamformers Market. The migration to SOI and other advanced semiconductor platforms lowers the voltage swing required for gain control, directly translating into lower heat dissipation and longer device lifetime. Leading suppliers such as Analog Devices, Texas Instruments, Qorvo, and Skyworks have recently introduced ultra‑low‑noise linear‑in‑dB VGAs optimized for mmWave frequencies, addressing both defense and commercial use cases. These product launches reflect a broader industry push toward integrating gain amplification with front‑end modules, simplifying system architecture and reducing bill‑of‑materials cost. As manufacturers continue to refine process nodes, the market is poised to benefit from incremental performance gains and broader application reach.

COMPETITIVE LANDSCAPE

Key Industry Players

Linear‑in‑dB Variable Gain Amplifiers for Phased‑Array Beamformers: Market Dynamics and Outlook

Analog Devices leads the market with its ultra‑low‑noise linear‑in‑dB VGA families that target mmWave radar and 5G massive‑MIMO platforms. Texas Instruments follows closely, leveraging its extensive RF portfolio and aggressive price‑to‑performance positioning. Qorvo and Skyworks have accelerated product introductions, focusing on silicon‑on‑insulator (SOI) processes that deliver reduced power consumption for satellite payloads and defense radar upgrades. The market, valued at USD 0.48 billion in 2025, is projected to reach USD 1.13 billion by 2034, reflecting a CAGR of 10 %. Collectively, these four tier‑1 vendors dominate more than 60 % of global shipments, setting technical roadmaps that dictate gain resolution, linearity, and integration with beamforming ICs.

Beyond the dominant quartet, a diverse set of niche innovators enrich the competitive landscape. NXP Semiconductors and Infineon Technologies provide SiGe‑based VGAs optimized for automotive radar, while STMicroelectronics and MACOM offer specialized mmWave devices for aerospace applications. RF Micro Devices (now part of Qorvo) continues to supply legacy product lines for established systems. Emerging players such as Peregrine Semiconductor (pSemi), Broadcom, and Murata Manufacturing contribute custom‑design services and vertically integrated modules. European specialist Rohde & Schwarz and Japanese firm Renesas expand the market with high‑precision, test‑qualified components. Additionally, smaller boutique firms like Analogic Corp and Silicon Labs are beginning to address niche segments, ensuring a robust supply chain for both defense and commercial deployments.

List of Key Linear-in-dB Variable Gain Amplifier for Phased-Array Beamformers Companies Profiled

- Analog Devices

- Texas Instruments

- Qorvo

- Skyworks Solutions

- NXP Semiconductors

- Infineon Technologies

- STMicroelectronics

- MACOM

- Broadcom Inc.

- Murata Manufacturing

- Rohde & Schwarz

- Renesas Electronics

- Peregrine Semiconductor (pSemi)

- RF Micro Devices

- Hittite Microwave (now part of Analog Devices)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Analog VGAs

|

| By Application |

|

Defense Radar

|

| By End User |

|

Defense Contractors

|

| By Frequency Band |

|

mmWave

|

| By Integration Approach |

|

MMIC

|

Regional Analysis: Linear-in-dB variable gain amplifier for phased-array beamformers Market

The region exhibits rapid adoption of linear‑in‑dB gain control techniques, driven by defense contracts that prioritize low‑power, high‑precision beamforming. Early integration in airborne radar suites and satellite communication payloads showcases confidence in the technology’s performance and scalability.

Major OEMs such as Lockheed Martin, Raytheon, and Northrop Grumman maintain strategic partnerships with semiconductor leaders, ensuring a steady pipeline of tailored amplifiers that meet stringent aerospace specifications and accelerate time‑to‑market.

A diversified supply chain, supported by domestic fabs and robust logistics networks, mitigates disruption risks. Investment in advanced packaging and silicon‑on‑insulator processes enhances component reliability for harsh operational environments.

Favorable regulatory frameworks and export‑control policies streamline prototype testing while protecting intellectual property. Initiatives such as the Defense Advanced Research Projects Agency (DARPA) programs provide clear pathways for commercialization.

Europe

Europe remains a strong contender in Linear-in-dB variable gain amplifier for phased-array beamformers Market, buoyed by coordinated defense initiatives across the EU and NATO members. Countries such as Germany, France, and the United Kingdom invest heavily in next‑generation radar and communication systems, encouraging the adoption of variable gain solutions within both military and civilian sectors. Collaborative research programs, like the European Defence Fund, foster joint development that reduces time‑to‑prototype and leverages shared testing facilities. Though the market size trails North America, Europe’s emphasis on sustainability and miniaturization drives innovative packaging approaches, increasing the appeal of linear‑in‑dB architectures for compact unmanned aerial systems and maritime surveillance platforms.

Asia‑Pacific

The Asia‑Pacific region is experiencing accelerating interest in Linear-in-dB variable gain amplifier for phased-array beamformers Market, propelled by rapid modernization of defense capabilities in China, Japan, South Korea, and India. Government‑backed programs focus on high‑frequency radar and 5G‑compatible phased arrays, creating demand for amplifiers that can deliver precise gain control while maintaining low power consumption. Local semiconductor firms are scaling production capacities, and strategic alliances with Western technology providers enable knowledge transfer. Emerging applications in autonomous transportation and high‑speed rail communications further diversify demand, positioning the region as a significant growth catalyst over the next decade.

South America

South America’s participation in Linear-in-dB variable gain amplifier for phased-array beamformers Market is modest but steadily growing, driven by Brazil’s and Argentina’s defense modernization plans. Nations are upgrading legacy radar installations and exploring cost‑effective solutions for border surveillance and maritime domain awareness. Regional aerospace programs emphasize indigenous development, encouraging partnerships with global component suppliers to integrate linear‑in‑dB gain amplifiers into locally assembled platforms. While budget constraints limit rapid expansion, increasing emphasis on regional security and participation in multinational exercises foster a conducive environment for gradual market adoption.

Middle East & Africa

Middle East & Africa exhibit niche yet strategic interest in Linear-in-dB variable gain amplifier for phased-array beamformers Market, primarily within the United Arab Emirates, Saudi Arabia, and Israel. These countries prioritize advanced radar and electronic warfare capabilities, allocating resources toward acquiring high‑performance phased‑array systems that benefit from linear‑in‑dB gain control. Collaborative ventures with Western OEMs and focused R&D centers accelerate technology transfer. In Africa, limited defense budgets restrain large‑scale procurement, but emerging partnerships aimed at critical infrastructure monitoring, such as border security and oil‑field surveillance, create modest demand for adaptable amplifier solutions.

Report Scope

This market research report provides a comprehensive analysis of the Linear-in-dB variable gain amplifier for phased-array beamformers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Linear-in-dB variable gain amplifier for phased-array beamformers Market?

-> Linear-in-dB variable gain amplifier for phased-array beamformers market is projected USD 1.13 billion by 2034, exhibiting a CAGR of 10%

Which key companies operate in Linear-in-dB variable gain amplifier for phased-array beamformers Market?

-> Key players include Analog Devices, Texas Instruments, Qorvo, and Skyworks.

What are the key growth drivers?

-> Key growth drivers include defense radar modernization programs, massive MIMO deployment in telecommunications, and advances in silicon‑on‑insulator (SOI) processes that reduce power consumption.

Which region dominates the market?

-> The reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include integration of ultra‑low‑noise linear‑in‑dB VGAs for mmWave frequencies, adoption in satellite payloads, and continued development of SOI technologies for power‑efficient designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...