Lightfield Displays Market Insights

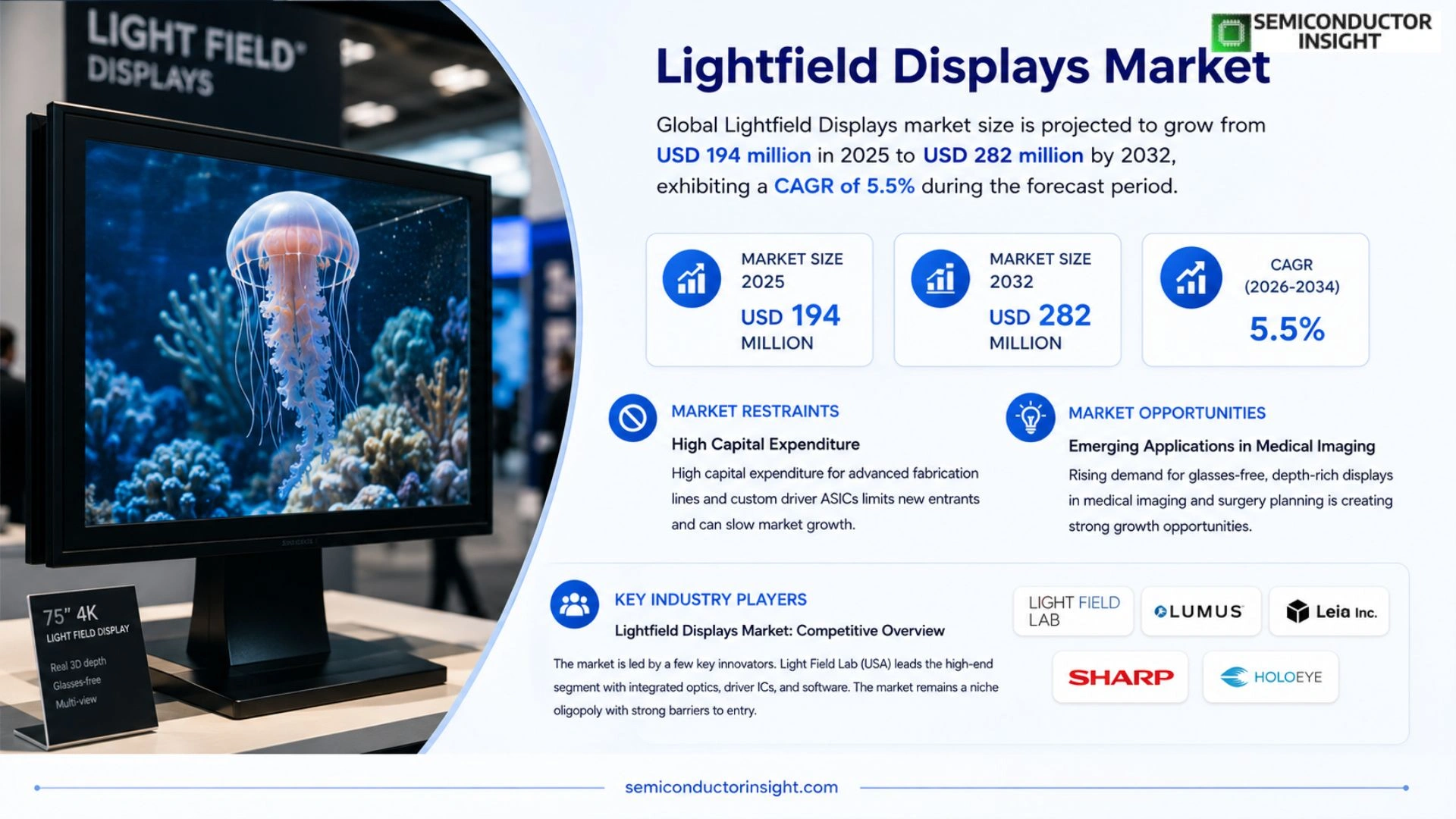

Global Lightfield Displays market size was valued at USD 194 million in 2025. The market is projected to grow from USD 194 million in 2025 to USD 282 million by 2034, exhibiting a CAGR of 5.5% during the forecast period.

Lightfield Displays are advanced display systems that reproduce the direction and intensity of light rays from a scene, allowing viewers to perceive three‑dimensional images with natural depth cues without necessarily wearing special glasses. Unlike traditional 2D displays or simple stereoscopic 3D displays, lightfield displays can present different views from different angles and create a more realistic sense of spatial depth, making them useful for medical imaging, industrial visualization, automotive displays, AR/VR/MR, digital content creation, and immersive exhibitions.

The market is experiencing growth due to several factors, including increasing demand for glasses‑free immersive experiences, advances in optical design and micro‑fabrication, and rising investment in AR/VR ecosystems. However, high system cost, complex optical architecture, limited content ecosystems and manufacturing scalability constrain broader adoption. Initiatives by key players such as CREAL, Light Field Lab and Looking Glass Factory include new high‑resolution modules and partnerships with automotive OEMs. Other notable participants include Magic Leap, Leia, Avegant and Sony.

MARKET DRIVERS

Advances in Computational Imaging

Lightfield Displays Market is gaining traction as new algorithms reduce the computational load required to render volumetric scenes. Researchers have leveraged neural‑based depth synthesis to cut rendering times by half, allowing manufacturers to embed lightfield engines in slimmer form factors. This technical leap translates into faster product cycles and a broader portfolio of consumer‑grade devices.

Growing Demand in AR/VR Ecosystems

Enterprise pilots in augmented‑reality training and virtual‑reality design studios are choosing lightfield panels for their ability to present multiple focal planes without vergence‑induced fatigue. As firms prioritize immersive experiences that retain visual comfort, procurement budgets are being redirected toward lightfield solutions, reinforcing a virtuous loop of adoption.

➤ Lightfield technology is redefining visual immersion by delivering true‑to‑life depth cues on a single screen.

Beyond entertainment, sectors such as automotive HUDs and industrial simulators are recognizing the strategic advantage of authentic depth representation. Companies that integrate these displays early will differentiate their product lines and command premium pricing.

MARKET CHALLENGES

Technical Complexity

Designing optical stacks that simultaneously manage diffraction, refraction, and pixel alignment remains a formidable engineering hurdle. The intricate calibration process inflates time‑to‑market and can deter smaller OEMs lacking dedicated R&D resources.

Other Challenges

Manufacturing Scale‑up

Mass production of microlens arrays at sub‑millimeter tolerances drives wafer‑level yield concerns. Even modest deviations lead to noticeable artifacts, compelling manufacturers to invest in high‑precision tooling that erodes profit margins.

MARKET RESTRAINTS

High Capital Expenditure

Establishing a dedicated lightfield fabrication line demands multi‑million‑dollar outlays for lithography, alignment machinery, and quality‑control instrumentation. This financial barrier filters out entrants that cannot justify the upfront spend against uncertain demand trajectories.

Furthermore, the need for custom driver ASICs adds another layer of cost, as each display resolution or field‑of‑view variant typically requires a tailored controller. Companies that cannot amortize these expenses across a sufficiently large order book may struggle to achieve economies of scale.

Capital intensity also influences partnership dynamics; many technology firms are opting for joint‑venture models to dilute risk, but such arrangements can complicate intellectual‑property ownership and slow decision‑making.

MARKET OPPORTUNITIES

Emerging Applications in Medical Imaging

Clinicians increasingly demand displays that convey depth without reliance on stereoscopic glasses, especially for minimally invasive surgery planning. Lightfield panels enable surgeons to visualize anatomical structures with natural focus cues, potentially reducing procedure time and error rates.

Parallel advances in tele‑presence diagnostics are opening channels for remote specialists to interact with 3D visual data in real time. Vendors that align their product roadmaps with hospital procurement cycles stand to capture a sizable share of this niche yet expanding segment.

Lightfield Displays Market Trends

Growth of Professional‑Grade Deployments

Lightfield Displays Market is seeing its most visible momentum in sectors that demand uncompromising visual fidelity,medical imaging suites, automotive cockpit prototypes, and high‑end industrial design studios. These environments value the glasses‑free three‑dimensional perception that lightfield technology provides, because it reduces visual fatigue and shortens the decision loop for engineers and clinicians. Adoption is accelerating as OEMs integrate customized optical stacks with existing display panels, turning what was once a research‑lab curiosity into a revenue‑generating asset. The shift is reinforced by early‑stage contracts that lock in multi‑year supply agreements, encouraging manufacturers to refine calibration workflows and to invest in higher‑resolution micro‑lens arrays. Consequently, the professional segment now accounts for the bulk of installed units, while the premium price point remains a barrier for mass‑market diffusion.

Other Trends

Manufacturing Complexity and Cost Pressures

The supply chain that underpins Lightfield Displays Market is densely layered, encompassing precision‑engineered diffractive optics, spatial light modulators, and bespoke image‑processing ASICs. Small‑batch production amplifies unit costs, pushing entry‑level devices into the several‑thousand‑dollar range. Moreover, alignment tolerances between lens arrays and pixel panels demand sub‑micron accuracy, limiting the number of foundries capable of volume output. Vendors are responding by consolidating optical component sourcing and by exploring silicon‑photonic integration, which could shave both material expense and assembly time. Yet, until these engineering breakthroughs translate into scalable fab lines, the cost curve will continue to shape the market’s segmentation, keeping high‑value applications at the forefront.

Hybrid Optical Architectures Expand Use Cases

A second wave of interest revolves around hybrid lightfield architectures that blend pixel‑based rendering with optical multiplexing. By coupling conventional high‑resolution panels with modest diffractive layers, manufacturers can deliver acceptable depth cues without the full optical stack’s expense. This compromise opens doors for mid‑range automotive displays and interactive museum installations, where budget constraints previously excluded pure lightfield solutions. The hybrid approach also eases content creation, as existing 2‑D pipelines can be repurposed with minor algorithmic adjustments. As the ecosystem of development tools matures, we anticipate a broader migration of lightfield concepts into product lines that sit between specialty workstations and everyday consumer electronics, gradually reshaping the competitive landscape of Lightfield Displays Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Lightfield Displays Market: Competitive Overview

Lightfield Displays market is still anchored by a handful of firms that have managed to translate complex optical engineering into commercially viable products. Light Field Lab, headquartered in the United States, dominates the high‑end segment with its multi‑view, glasses‑free panels that command premium prices for aerospace and medical imaging customers. Its vertical integration of micro‑optics, driver ICs, and proprietary rendering software gives it a cost advantage over newcomers that must outsource critical components. The market structure resembles a niche oligopoly: a few well‑funded innovators hold the bulk of revenue, while smaller specialists compete on application‑specific customization, such as automotive cockpit integration or portable AR devices.

Beyond the market leader, several niche players contribute depth to the ecosystem. CREAL in Japan specializes in diffractive optical elements that enable compact, vehicle‑mounted solutions. Looking Glass Factory focuses on desktop‑grade displays for designers and educators, leveraging an open‑source content pipeline. European firms such as Dimenco and Sony blend high‑resolution panels with proprietary eye‑tracking to target premium medical and exhibition markets. Emerging entrants like AYE3D and MOPIC are experimenting with hybrid light‑field architectures that combine pixel‑based and optical‑layer techniques, aiming to lower the price barrier for consumer‑grade devices. Collectively, these companies diversify the supply chain, push incremental performance gains, and create a competitive pressure that may accelerate standardization of content formats.

List of Key Lightfield Displays Companies Profiled

- Light Field Lab

- CREAL

- Looking Glass Factory

- Leia

- Dimenco

- Sony

- Magic Leap

- Huawei

- AYE3D

- MOPIC

- FoVI 3D

- NanoAR

- Pendu Technology

- SVG Tech Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Portable / Mobile Grade is emerging as the leading segment because:

|

| By Application |

|

Medical Imaging dominates this category because:

|

| By End User |

|

Healthcare Providers are the leading end‑user segment because:

|

| By Technology |

|

Optical Light Field leads because:

|

| By Viewing Mode |

|

Glasses‑free 3D Light Field is the dominant viewing mode because:

|

Regional Analysis: Lightfield Displays Market

Manufacturers embed light‑field modules into robotic vision stations, enabling operators to perceive depth without stereoscopic glasses. This integration shortens inspection cycles and reduces error rates, which firms tout as a competitive differentiator in high‑mix, low‑volume production environments.

Hospital networks experiment with light‑field displays for surgical planning, where three‑dimensional anatomical models replace flat scans. The tactile sense of depth supports multidisciplinary case reviews, improving consensus on procedural approaches.

Defense contractors leverage immersive light‑field simulators to replicate battlefield terrain, allowing trainees to develop spatial awareness without the logistical burden of live‑fire exercises.

Universities partner with industry to create open‑source toolkits for light‑field rendering, fostering a pipeline of talent that can translate research breakthroughs into viable commercial products.

Europe

European markets exhibit a cautious yet steady embrace of Lightfield Displays, driven by strong public‑sector funding for immersive education and cultural heritage preservation. Nations with mature optical engineering traditions are repurposing legacy photonics expertise toward light‑field manufacturing, creating niche players that specialize in museum installations and virtual tourism. The region’s fragmented regulatory landscape encourages cross‑border collaborations, as firms seek to harmonize standards that can unlock broader EU procurement opportunities. While adoption rates trail North America, the emphasis on design‑centric user experiences fuels a parallel development stream focused on aesthetic integration and ergonomic ergonomics, positioning Europe as a potential leader in consumer‑facing light‑field solutions.

Asia‑Pacific

In Asia‑Pacific, rapid digitization across manufacturing hubs and a burgeoning consumer electronics market lay the groundwork for Lightfield Displays to transition from laboratory curiosity to mainstream component. Countries with established display supply chains are experimenting with hybrid production lines that mix traditional LCD processes with volumetric light‑field layers, aiming to keep price points accessible for mass‑market devices. Simultaneously, regional governments are embedding immersive visualization into smart‑city initiatives, where public information kiosks benefit from depth‑enhanced signage. These dual pressures,cost efficiency and public‑service innovation,are compelling local firms to pursue modular designs that can be retrofitted onto existing infrastructure, a strategy that may accelerate regional market penetration.

South America

South America’s Lightfield Displays trajectory is shaped by a focus on niche applications such as remote agricultural monitoring and low‑cost medical outreach. Agricultural cooperatives are piloting light‑field visualizations to overlay soil health data onto three‑dimensional field maps, improving decision‑making for precision farming. In parallel, non‑governmental health organizations experiment with portable light‑field viewers to train clinicians in remote clinics, where conventional 3‑D imaging equipment is scarce. The limited scale of these projects encourages partnerships with multinational vendors that can supply turnkey solutions, fostering a collaborative ecosystem that leverages external expertise while cultivating local technical capacity.

Middle East & Africa

The Middle East & Africa region approaches Lightfield Displays through a lens of strategic diversification, particularly within the Gulf’s push toward knowledge‑based economies. Investment funds allocate capital to startups that blend light‑field technology with virtual tourism platforms, showcasing cultural sites to global audiences. In Africa, where mobile penetration outpaces fixed‑line infrastructure, there is growing interest in lightweight, battery‑efficient light‑field modules for educational tablets used in remote schools. These initiatives reflect a broader ambition to harness immersive visualization as a catalyst for skill development and tourism revenue, suggesting that the region could carve out a distinct value proposition anchored in accessibility and cultural storytelling.

Report Scope

This market research report provides a comprehensive analysis of the Lightfield Displays Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Lightfield Displays Market?

-> Lightfield Displays Market was valued at USD 194 million in 2025 and is expected to reach USD 282 million by 2034 with a CAGR of 5.5%.

Which key companies operate in Lightfield Displays Market?

-> Key players include CREAL, Light Field Lab, Looking Glass Factory, Magic Leap, Leia, Avegant, FoVI 3D, Dimenco, JDI, Sony, Google, Huawei, AYE3D, MOPIC, NanoAR, Pendu Technology, SVG Tech Group.

What are the key growth drivers?

-> Key growth drivers include increasing demand for glasses‑free 3D visualization, adoption in medical imaging, automotive cockpit design, AR/VR/MR applications, and the need for immersive digital content creation.

Which region dominates the market?

-> Asia‑Pacific is expected to be the largest market region, while North America shows rapid growth.

What are the emerging trends?

-> Emerging trends include advancements in optical design for higher resolution, cost reduction through mass‑production techniques, and integration with AI‑driven content rendering.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...