MARKET INSIGHTS

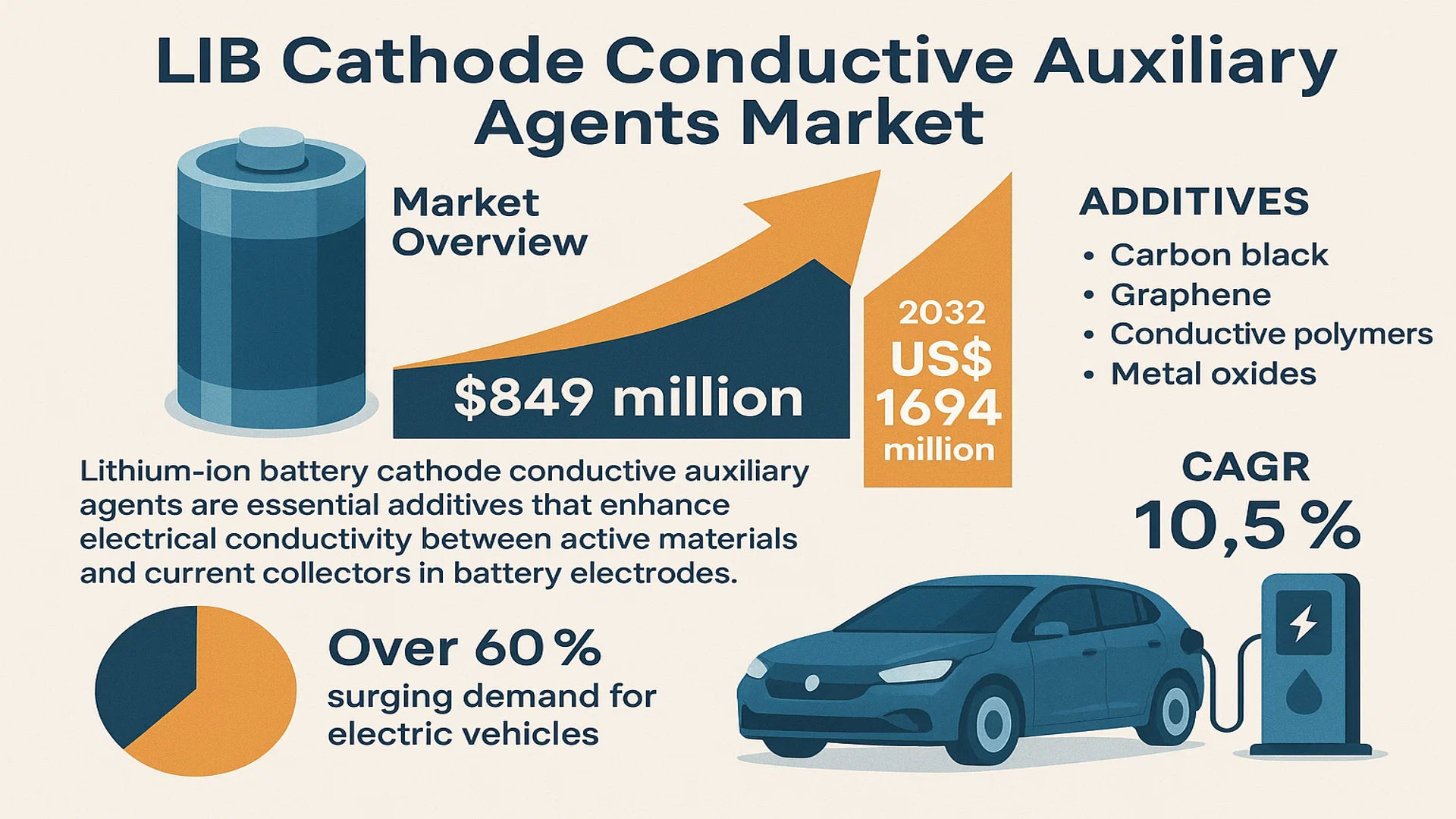

The global LIB Cathode Conductive Auxiliary Agents Market was valued at 849 million in 2024 and is projected to reach US$ 1694 million by 2032, at a CAGR of 10.5% during the forecast period.

Lithium-ion battery (LIB) cathode conductive auxiliary agents are essential additives that enhance electrical conductivity between active materials and current collectors in battery electrodes. These agents form conductive networks to improve battery performance metrics such as capacity, charge/discharge rates, and cycle life. Common types include carbon-based materials (carbon black, graphene), conductive polymers, and metal oxides, with carbon black currently dominating the market due to its cost-effectiveness and performance balance.

The market growth is primarily driven by surging demand for electric vehicles, which accounted for over 60% of conductive agent consumption in 2024. Furthermore, energy storage systems and 3C electronics are accelerating adoption, with the latter seeing 18% year-over-year growth in battery demand. Technological advancements in high-nickel cathodes, which require specialized conductive agents, and increasing investments in battery R&D (global spending exceeded USD 12 billion in 2023) are creating new opportunities. Key players like Cabot Corporation and LG Chem are expanding production capacities to meet the 140% projected increase in demand by 2030.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Lithium-Ion Batteries in Electric Vehicles Accelerates Market Growth

The global electric vehicle (EV) market is experiencing unprecedented growth, with projected sales exceeding 30 million units annually by 2030. This surge directly fuels demand for advanced lithium-ion batteries where cathode conductive additives play a critical role in enhancing performance. These additives improve electron transfer efficiency, increasing battery capacity by up to 15% and extending cycle life by approximately 20% compared to conventional formulations. Major automotive manufacturers are increasingly collaborating with battery material suppliers, creating a robust ecosystem for conductive auxiliary agent development.

Energy Storage System Expansion Creates New Application Horizons

Grid-scale energy storage installations are projected to grow at a compound annual rate exceeding 25% through 2030, driven by renewable energy integration needs. Lithium-ion batteries dominate this segment, accounting for over 80% of new storage capacity. Cathode conductive additives enable higher charge-discharge rates critical for frequency regulation applications, with specialized formulations now achieving conductivity improvements of 30-40% in high-load conditions. Recent product launches specifically targeting energy storage applications demonstrate manufacturers’ strategic focus on this high-growth sector.

Technological Advancements in Conductive Additive Formulations Drive Performance Improvements

Material science breakthroughs are enabling next-generation conductive additives with multi-functional capabilities. Carbon nanotube-based additives now demonstrate 50% higher conductivity than conventional carbon black while requiring 30% less material volume. Hybrid additive systems combining graphene with conductive polymers are showing particular promise, achieving simultaneous improvements in mechanical stability and electrochemical performance. These innovations are critical as battery manufacturers push energy densities beyond 300 Wh/kg while maintaining safety standards.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes Limit Market Penetration

Advanced conductive additives require specialized production facilities with capital expenditures often exceeding $50 million for medium-scale operations. The high-purity requirements for battery-grade materials drive production costs 40-60% above industrial-grade alternatives. This cost sensitivity is particularly acute in price-competitive markets like consumer electronics, where battery manufacturers operate on thin margins. While economies of scale are gradually reducing costs, the premium pricing remains a significant barrier for widespread adoption.

Stringent Certification Requirements Delay Time-to-Market

Battery material certification processes typically require 12-18 months for automotive-grade applications, creating significant lead times for new product commercialization. Regulatory requirements continue to evolve, with recent emphasis on sustainability credentials adding further complexity. These extended validation periods discourage smaller players from entering the market and slow the adoption of innovative formulations. The certification bottleneck is particularly problematic in Europe and North America, where standards are most rigorous.

Material Compatibility Challenges with Emerging Cathode Chemistries

The rapid development of new cathode materials such as high-nickel NCM and lithium manganese iron phosphate (LMFP) creates formulation challenges for conductive additive manufacturers. These advanced cathodes require customized additive solutions to maintain performance, with optimal dispersion characteristics varying significantly between chemistries. The industry faces a knowledge gap in understanding interface interactions, leading to trial-and-error development approaches that increase R&D expenditures.

MARKET CHALLENGES

Balancing Performance Enhancements with Sustainability Requirements

While conductive additives improve battery performance, their production often involves energy-intensive processes with significant carbon footprints. The industry faces increasing pressure to reduce greenhouse gas emissions by 30-40% across the value chain by 2030. This challenge is compounded by the use of petroleum-based precursors in many carbon additives. Developing bio-based alternatives without compromising performance characteristics remains an ongoing technical hurdle for material scientists.

Supply Chain Vulnerabilities for Critical Raw Materials

Graphite, a key raw material for many conductive additives, faces supply constraints with over 70% of global production concentrated in China. The recent export controls on graphite products have created uncertainty in the market, forcing manufacturers to diversify supply sources. Alternative materials like carbon nanotubes rely on specialized catalysts that themselves face supply chain risks. These vulnerabilities became particularly evident during recent global logistics disruptions, causing price volatility exceeding 25% for some additive types.

Intellectual Property Disputes in Advanced Material Formulations

The competitive landscape has seen a surge in patent litigation as companies protect their conductive additive innovations. Over 200 new patents were filed in this sector in 2023 alone, creating a complex web of intellectual property rights. Smaller innovators face particular challenges navigating this environment, with legal defense costs sometimes reaching 15-20% of R&D budgets. This IP thicket may inadvertently slow overall market innovation as companies become cautious about potential infringement risks.

MARKET OPPORTUNITIES

Next-Generation Solid-State Batteries Create New Material Requirements

The emerging solid-state battery market, projected to exceed $8 billion by 2030, requires fundamentally different conductive additive solutions. These systems need additives that maintain conductivity across solid-solid interfaces while withstanding higher operating temperatures. Early research indicates that specially-modified carbon allotropes show particular promise, with prototype batteries demonstrating 20% higher energy density than conventional lithium-ion systems. This represents a blue ocean opportunity for additive manufacturers to develop tailored solutions for this disruptive technology.

Regional Supply Chain Localization as Strategic Imperative

Growing emphasis on supply chain resilience is driving regional production initiatives, particularly in North America and Europe. Government incentives under programs like the U.S. Inflation Reduction Act are catalyzing over $2 billion in announced investments for local battery material production. This presents opportunities for additive manufacturers to establish partnerships with regional players, with several joint ventures already announced between Asian material suppliers and Western battery manufacturers to qualify localized supply chains.

Integration of AI in Material Discovery and Formulation Optimization

Artificial intelligence is transforming additive development cycles, reducing traditional formulation testing time from months to weeks. Machine learning models trained on electrochemical performance data are achieving 85% accuracy in predicting optimal additive combinations for specific cathode formulations. This acceleration in material discovery creates opportunities for first-mover advantage, with several companies already offering AI-optimized additive packages that promise performance improvements of 10-15% over conventional benchmarks.

LIB CATHODE CONDUCTIVE AUXILIARY AGENTS MARKET TRENDS

Rising Demand for High-Performance Lithium-Ion Batteries Drives Market Expansion

The global LIB cathode conductive auxiliary agents market is experiencing substantial growth, primarily driven by the increasing demand for high-performance lithium-ion batteries across electric vehicles (EVs), renewable energy storage, and consumer electronics. The market is projected to grow at a CAGR of 10.5%, expanding from $849 million in 2024 to $1.7 billion by 2032. Conductive additives play a pivotal role in enhancing electrode conductivity, improving battery life, charge-discharge efficiency, and thermal stability, which are critical for advanced battery applications. The surge in EV production, with a forecasted 30 million units sold annually by 2030, underscores the necessity for improved cathode materials.

Other Trends

Shift Toward Sustainable and High-Energy-Density Materials

Manufacturers are increasingly adopting carbon-based nanomaterials, such as carbon nanotubes (CNTs) and graphene, due to their superior conductivity and minimal weight addition. These materials enable higher energy density while reducing the overall battery weight—a key requirement for EVs and portable electronics. Additionally, strict environmental regulations are pushing companies to replace conventional conductive agents like acetylene black with eco-friendly alternatives, fostering innovation in this segment.

Growing Investments in Energy Storage Solutions

The rapid expansion of grid-scale energy storage systems is accelerating demand for long-lasting, high-efficiency lithium batteries, where cathode conductive additives play a crucial role. Governments worldwide are investing heavily in renewable energy integration, with global energy storage capacity expected to exceed 1,000 GWh by 2030. Leading players, including LG Chem and BTR New Material, are actively expanding production capacities to meet the increasing need for high-performance conductive agents in energy storage applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Innovation and Expansion to Maintain Market Position

The global LIB Cathode Conductive Auxiliary Agents market exhibits a competitive landscape with a mix of established chemical manufacturers and specialized battery materials producers. Market leaders are leveraging their technological expertise and production capacities to cater to the growing demand from lithium-ion battery manufacturers. Birla Carbon and Cabot Corporation have emerged as dominant players, collectively accounting for over 30% of the market share in 2024, primarily due to their extensive carbon black product portfolios and global distribution networks.

Asian players such as LG Chem and BTR New Material are gaining significant traction, driven by their proximity to major battery production hubs in China, South Korea, and Japan. These companies have been investing heavily in R&D to develop advanced conductive additives that enhance battery performance while reducing costs. Recent expansions in production capacity by these firms indicate their commitment to meeting the surging demand from electric vehicle manufacturers.

The market is witnessing increasing competition from emerging players specializing in next-generation conductive materials. Dynanonic and ADEKA have introduced innovative graphene-based conductive additives that offer superior performance characteristics, particularly in high-energy-density battery applications. These technological advancements are reshaping competitive dynamics as established players respond with their own product innovations.

Strategic partnerships and vertical integration have become key competitive strategies. Imerys recently entered into a joint venture with a major cathode producer to ensure stable supply chains, while Denka has vertically integrated its conductive additive production with carbon nanotube manufacturing. Such moves are expected to intensify competition while driving product standardization across the industry.

List of Key LIB Cathode Conductive Auxiliary Agents Companies Profiled

- Birla Carbon (India)

- Orion Engineered Carbons (Luxembourg)

- Cabot Corporation (U.S.)

- Imerys Graphite & Carbon (Switzerland)

- Denka Company Limited (Japan)

- LG Chem (South Korea)

- Resonac Holdings Corporation (Japan)

- BTR New Material Group (China)

- Zeon Corporation (Japan)

- ADEKA Corporation (Japan)

- Dynanonic (China)

Segment Analysis:

By Type

Lithium Nickel Cobalt Manganese Oxide Leads the Market Due to High Adoption in EV Batteries

The market is segmented based on type into:

- Lithium Carbonate

- Lithium Nickel Cobalt Manganese Oxide

- Lithium Iron Phosphate

- Lithium Manganese Phosphate

- Others

By Application

Power Battery Segment Dominates Due to Rising Electric Vehicle Demand

The market is segmented based on application into:

- Power Battery

- 3C Electronic Battery

- Energy Storage Battery

- Others

By End User

Automotive Sector Drives Market Growth with Increasing EV Production

The market is segmented based on end user into:

- Automotive

- Consumer Electronics

- Energy Storage Systems

- Industrial

Regional Analysis: LIB Cathode Conductive Auxiliary Agents Market

Asia-Pacific

The Asia-Pacific region dominates the global LIB Cathode Conductive Auxiliary Agents market, accounting for over 60% of total demand in 2024. This leadership position stems from China’s massive lithium-ion battery production capacity, which exceeds 1,200 GWh annually. The country’s “14th Five-Year Plan” actively promotes new energy vehicles and energy storage systems, creating sustained demand for high-performance conductive additives. Japan and South Korea follow closely, with major battery manufacturers like LG Chem and Panasonic driving innovation in cathode materials. Despite pricing pressures, the region benefits from established supply chains, government subsidies for electric vehicles, and rapid urbanization driving demand for consumer electronics.

North America

The North American market is experiencing accelerated growth due to strict emissions regulations and the Biden administration’s push for domestic battery manufacturing. The Inflation Reduction Act’s $369 billion clean energy investments are incentivizing localized production of battery components, including conductive additives. Canada’s rich lithium reserves and growing gigafactory projects (such as those by Tesla and Stellantis) present new opportunities for suppliers. However, the region faces challenges in competing with Asian producers on cost, with many manufacturers still dependent on imported conductive materials despite efforts to build domestic supply chains.

Europe

Europe’s market growth is propelled by the European Battery Alliance’s initiatives to establish a competitive battery value chain. Stringent EU regulations on battery sustainability (including the new Battery Passport requirements) are driving demand for advanced conductive additives that enhance energy density and lifecycle performance. Germany leads in technological development, with companies like BASF investing heavily in next-generation cathode materials. The region’s focus on circular economy principles is prompting innovation in recyclable conductive additives – though adoption remains slow due to higher costs compared to conventional options.

South America

South America represents an emerging market with Brazil and Argentina showing the most potential. Brazil’s growing electric vehicle adoption (with sales increasing 200% year-over-year in 2023) and Argentina’s lithium mining expansion create opportunities. However, market development is constrained by economic instability, limited local manufacturing capabilities, and reliance on imported battery components. The region shows promise as a future production hub due to abundant lithium resources, but currently lacks the infrastructure for large-scale conductive additive manufacturing.

Middle East & Africa

This region remains in early development stages for LIB conductive additives. While benefitting from renewable energy investments (particularly in solar-plus-storage projects), limited local battery production constrains market growth. The UAE and Saudi Arabia are making strategic investments in battery technology as part of energy diversification plans, but currently serve primarily as consumption markets for imported battery materials. The African continental free trade agreement could eventually stimulate regional value chains, though progress remains slow due to infrastructure gaps and investment challenges.

Report Scope

This market research report provides a comprehensive analysis of the global LIB Cathode Conductive Auxiliary Agents market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the lithium-ion battery industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, volume shipments, and market value across major regions and application segments.

- Segmentation Analysis: Detailed breakdown by material type (lithium carbonate, NCM, LFP, LMP), application (power batteries, 3C electronics, energy storage), and end-use industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading conductive additive manufacturers, including their product portfolios, production capacities, technological innovations, and strategic initiatives.

- Technology Trends: Assessment of emerging conductive additive formulations, nanotechnology applications, and performance enhancement solutions for next-gen batteries.

- Market Drivers & Challenges: Analysis of EV adoption rates, energy storage demand, raw material availability, and regulatory impacts on conductive additive requirements.

- Supply Chain Analysis: Examination of upstream material suppliers, manufacturing processes, and downstream battery producers in the value chain.

The research methodology combines primary interviews with industry experts and secondary data from authoritative sources to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LIB Cathode Conductive Auxiliary Agents Market?

-> LIB Cathode Conductive Auxiliary Agents Market was valued at 849 million in 2024 and is projected to reach US$ 1694 million by 2032, at a CAGR of 10.5% during the forecast period..

Which key companies operate in this market?

-> Major players include Birla Carbon, Cabot Corporation, Imerys, LG Chem, Denka, and BTR New Material, who collectively held over 65% market share in 2024.

What are the primary growth drivers?

-> Key drivers include rising EV production (projected 30 million units by 2030), grid-scale energy storage deployments, and demand for high-performance 3C batteries with faster charging capabilities.

Which region leads in market share?

-> Asia-Pacific dominates with 78% market share in 2024, driven by China’s battery manufacturing ecosystem, followed by North America and Europe.

What are the emerging material trends?

-> Emerging trends include carbon nanotube adoption, graphene-based additives, and hybrid conductive systems to enhance battery energy density and cycle life.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...