MARKET INSIGHTS

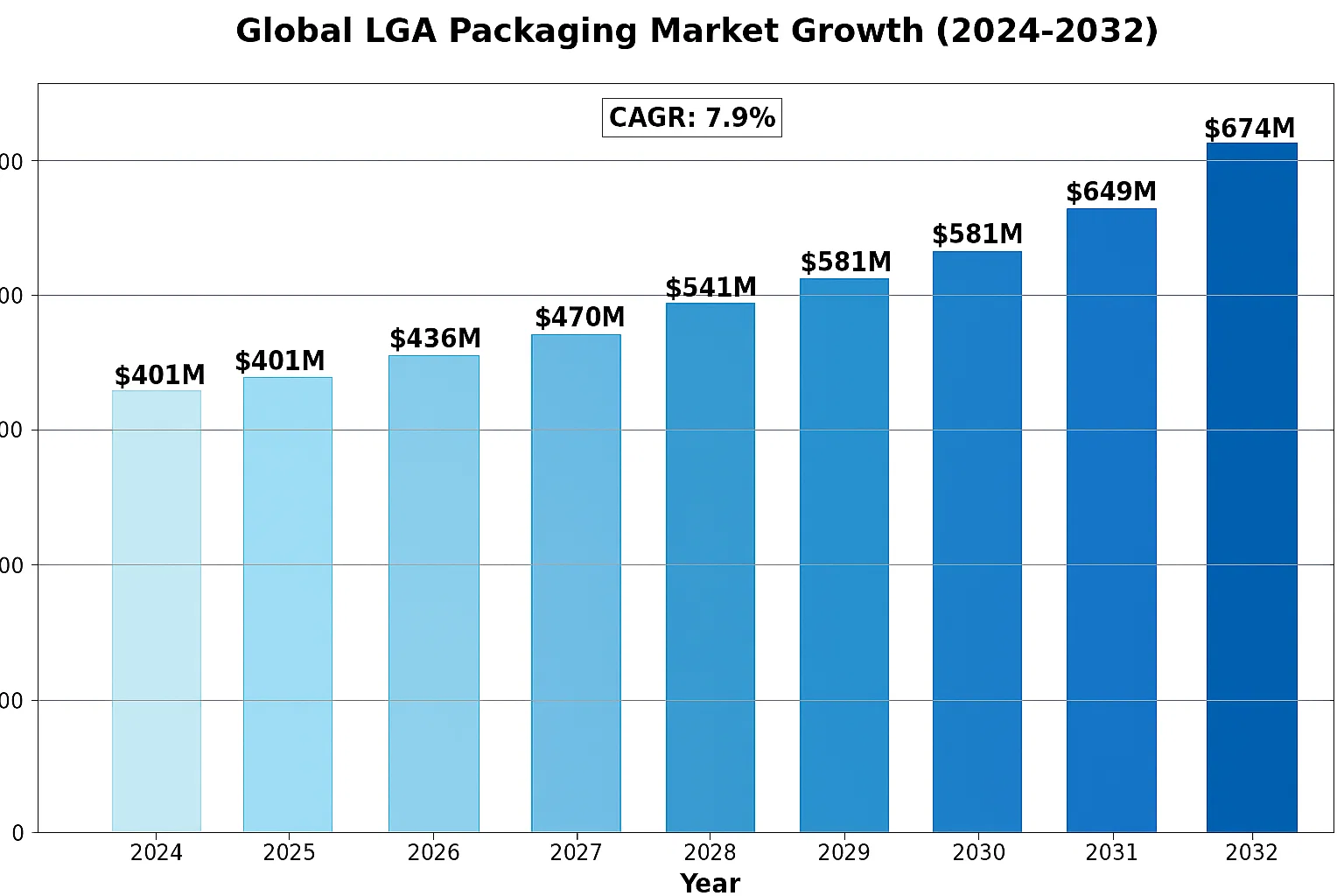

The global LGA Packaging Market was valued at 401 million in 2024 and is projected to reach US$ 674 million by 2032, at a CAGR of 7.9% during the forecast period.

LGA (Land Grid Array) Packaging is an advanced semiconductor packaging technology that offers a thinner and lighter profile compared to traditional BGA (Ball Grid Array) packages. By eliminating solder balls and using flat conductive pads instead, LGA provides superior electrical performance while reducing overall package height. This makes it particularly suitable for high-performance applications in consumer electronics, automotive systems, and optoelectronic components where space constraints and thermal management are critical considerations.

The market growth is driven by increasing demand for compact, high-performance semiconductor packaging across multiple industries. While the broader semiconductor market was valued at USD 579 billion in 2022 and projected to reach USD 790 billion by 2029 (6% CAGR), LGA packaging demonstrates faster growth due to its technical advantages. Key segments showing particular promise include automotive electronics and IoT devices, where LGA’s combination of miniaturization and reliability meets emerging design requirements. However, the market faces challenges from alternative packaging technologies and fluctuating raw material costs that may impact adoption rates.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Consumer Electronics to Accelerate LGA Packaging Demand

The global consumer electronics market continues to expand rapidly, driven by increasing disposable incomes and technological advancements. LGA packaging plays a critical role in this sector due to its compact form factor and superior electrical performance. With smartphone shipments projected to exceed 1.5 billion units annually by 2025, manufacturers are increasingly adopting LGA solutions for space-constrained applications. The technology’s ability to minimize package height while maintaining thermal efficiency makes it particularly valuable for next-generation mobile devices and wearables. This widespread adoption across consumer electronics is expected to remain a key growth driver for the LGA packaging market through the forecast period.

Automotive Semiconductor Boom to Fuel Market Expansion

The automotive semiconductor sector is experiencing unprecedented growth, with electronic components accounting for over 40% of a modern vehicle’s total cost. LGA packaging is gaining traction in automotive applications due to its reliability and performance in harsh environments. The technology is particularly favored for advanced driver assistance systems (ADAS) and vehicle electrification components, where its low-profile design and robust connectivity provide significant advantages. With autonomous vehicle development accelerating and electric vehicle production growing at nearly 30% CAGR, the demand for high-performance semiconductor packaging solutions like LGA is expected to surge in the coming years.

Miniaturization Trend in Semiconductor Packaging to Drive Innovation

The relentless push for smaller, more efficient electronic components continues to shape the semiconductor packaging landscape. LGA technology sits at the forefront of this trend, offering up to 30% size reduction compared to traditional BGA packages while maintaining comparable performance characteristics. This miniaturization advantage becomes increasingly critical as IoT devices proliferate and edge computing applications demand greater processing power in constrained spaces. Product development initiatives from leading manufacturers focus on pushing the boundaries of LGA packaging density while maintaining thermal and electrical performance benchmarks, creating new opportunities across multiple industry verticals.

MARKET RESTRAINTS

High Initial Investment Costs to Limit Market Penetration

While LGA packaging offers numerous technical advantages, the significant capital expenditure required for implementation poses a major barrier to widespread adoption. Establishing production lines capable of handling LGA packages requires specialized equipment for precision soldering and inspection, with setup costs often exceeding $5 million for mid-sized facilities. These financial requirements discourage smaller manufacturers and price-sensitive market segments from transitioning from established packaging technologies. Furthermore, the need for dedicated testing infrastructure adds to the total cost of ownership, particularly for applications requiring rigorous quality assurance protocols.

Other Restraints

Thermal Management Challenges

As LGA packages continue to shrink in size while processing power increases, effectively dissipating heat becomes increasingly difficult. The tightly packed contact array creates hot spots that can affect device reliability, particularly in high-performance computing applications. Designing adequate thermal solutions within the constrained package height remains an ongoing engineering challenge that limits adoption in certain use cases.

Supply Chain Vulnerabilities

The LGA packaging ecosystem relies on specialized materials and precision components that have experienced supply disruptions in recent years. Geopolitical tensions and raw material shortages have exposed vulnerabilities in the semiconductor supply chain, creating uncertainty for manufacturers considering adoption of LGA solutions. The lead times for critical packaging materials have extended significantly, making production planning more complex and increasing inventory carrying costs.

MARKET CHALLENGES

Technical Complexity in Manufacturing Processes to Constrain Output

LGA packaging introduces several manufacturing challenges that impact yield rates and production efficiency. The precise alignment required between the package and PCB demands advanced assembly equipment with micron-level accuracy. Even minor variations in solder paste application or reflow parameters can result in connection failures, requiring extensive rework. As package pitches continue to shrink below 0.5mm, maintaining acceptable yield rates becomes increasingly difficult. These manufacturing complexities contribute to higher unit costs and limit production scalability, particularly for volume-sensitive applications.

Other Challenges

Standardization Gaps

The LGA packaging market lacks unified industry standards across different applications and geographies. Varying specifications for pitch, pad configuration, and material composition create compatibility issues and increase design complexity. This fragmentation forces manufacturers to maintain multiple product variants, raising production costs and lead times while potentially limiting market growth.

Rework and Repair Difficulties

Unlike traditional packaging solutions, LGA components present significant challenges for rework and repair operations once installed. The solderless connection mechanism makes component replacement particularly difficult in field applications, potentially increasing total ownership costs for end-users. This limitation affects adoption in sectors where maintenance and upgradability are key considerations.

MARKET OPPORTUNITIES

Edge Computing Expansion to Create New Application Areas

The rapid growth of edge computing infrastructure presents significant opportunities for LGA packaging technology. As processing capabilities migrate closer to data sources, the demand for compact, high-performance computing modules increases. LGA’s combination of small form factor and robust electrical characteristics makes it ideally suited for edge devices that require reliable operation in space-constrained environments. The ongoing deployment of 5G networks and IoT ecosystems will further accelerate this trend, creating new adoption opportunities across industrial, commercial, and telecommunications applications.

Advanced Packaging Integration to Drive Innovation

The semiconductor industry’s shift toward heterogeneous integration and 3D packaging architectures opens new avenues for LGA technology development. By combining LGA interconnects with emerging packaging approaches like chiplets and silicon interposers, manufacturers can create solutions that deliver superior performance while maintaining compatibility with existing assembly processes. Several leading semiconductor companies are investing heavily in these hybrid approaches, recognizing their potential to address the growing need for optimized packaging solutions in high-performance computing applications.

Automotive Electrification to Fuel Long-Term Growth

The automotive industry’s transition to electrified powertrains represents a substantial growth opportunity for LGA packaging solutions. Modern electric vehicles incorporate dozens of specialized control modules that benefit from LGA’s combination of compact dimensions and vibration-resistant characteristics. As vehicle architectures evolve toward domain controllers and zonal architectures, the demand for reliable, high-density packaging will increase significantly. Industry analysts project that semiconductor content per vehicle could triple by 2030, with packaging innovations like LGA playing a crucial role in meeting these evolving requirements.

LGA PACKAGING MARKET TRENDS

Demand for Compact and High-Performance Semiconductor Packages Drives LGA Growth

The Land Grid Array (LGA) packaging market is experiencing robust growth, fueled by the increasing need for thinner, lighter, and high-performance semiconductor solutions in modern electronics. With a market valuation of $401 million in 2024, the sector is projected to reach $674 million by 2032, expanding at a CAGR of 7.9%. LGA technology, which eliminates solder balls to reduce package height, is particularly favored in applications requiring superior electrical performance, such as advanced microprocessors and IoT devices. The broader semiconductor market, valued at $579 billion in 2022 and expected to grow to $790 billion by 2029, further underscores the critical role of innovative packaging solutions like LGA in meeting evolving industry demands.

Other Trends

IoT and 5G Expansion

The rapid proliferation of IoT devices and 5G infrastructure is significantly boosting the adoption of LGA packaging. As IoT applications require compact yet powerful processors for real-time data processing, LGA’s ability to provide high-density interconnects without compromising performance makes it ideal for these use cases. Additionally, 5G network equipment leverages LGA packages for their enhanced signal integrity and thermal management, critical for high-frequency operation. The Analog IC segment, which supports these technologies, continues to witness steady growth, further driving demand for advanced packaging solutions like LGA.

Automotive Sector Embrace

The automotive industry’s shift toward electrification and autonomous driving is accelerating the use of LGA packaging for advanced driver-assistance systems (ADAS) and in-vehicle computing. Modern vehicles incorporate an increasing number of electronic control units (ECUs) and sensors, many of which rely on LGA packages for their balance of miniaturization and reliability. Furthermore, the rising adoption of hybrid MPUs and MCUs in automotive applications underscores the need for robust interconnect solutions that can withstand harsh operating conditions while delivering high performance. This trend is expected to sustain growth in the LGA packaging market through the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Semiconductor Giants Drive Innovation in LGA Packaging Through Technological Advancements

The LGA packaging competitive landscape is moderately fragmented, with several well-established semiconductor players dominating the market while smaller regional suppliers carve out specialized niches. ASE Holdings currently leads in market share due to its vertically integrated semiconductor packaging solutions and massive production capacity across Asia-Pacific facilities. The company accounted for approximately 18% of the global LGA packaging revenue in 2024.

Amkor Technology follows closely, particularly strong in automotive-grade LGA solutions, leveraging its stringent quality control systems and Tier-1 automotive supplier relationships. Meanwhile, GS Nanotech has emerged as a disruptive force with its patented nano-coating technologies that enhance LGA package durability in harsh environments.

The competitive intensity continues rising as these players invest heavily in R&D – particularly in fine-pitch LGA solutions below 0.5mm spacing to support next-generation processor packaging demands. Recent acquisitions have further reshaped the landscape, including Amkor’s 2023 purchase of a Japanese specialty packaging firm to bolster its advanced cooling solutions for high-performance computing applications.

List of Key LGA Packaging Companies Profiled

- ASE Holdings (Taiwan)

- Amkor Technology (U.S.)

- GS Nanotech (South Korea)

- Orient Semiconductor Electronics (Taiwan)

- NXP Semiconductors (Netherlands)

- Maxim Integrated (U.S.)

- Analog Devices (U.S.)

- Thales Group (France)

Segment Analysis:

By Type

Hot Air Soldering Dominates Due to Precision in High-Density Packaging

The market is segmented based on type into:

- Hot Air Soldering

- Subtypes: Convection, Vapor Phase, and others

- Infrared Soldering

By Application

Consumer Electronics Leads Market Adoption Due to IoT Device Proliferation

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphones, Wearables, Smart Home Devices

- Automotive

- Optoelectronic Components

- Industrial Applications

- Others

By Material

Copper-Based Substrates Preferred for High Thermal Performance

The market is segmented based on material into:

- Organic Substrates

- Ceramic Substrates

- Copper-Based

- Others

By End User

Semiconductor Manufacturers Drive Demand Through Advanced Packaging Needs

The market is segmented based on end user into:

- Semiconductor Manufacturers

- Electronics OEMs

- Contract Manufacturers

- Research Institutions

Regional Analysis: LGA Packaging Market

North America

The North American LGA packaging market is driven by robust demand from the semiconductor and electronics industries, particularly in the U.S. and Canada. The region benefits from strong R&D investments in advanced packaging technologies, supported by major players like Analog Devices and Maxim Integrated. With the semiconductor market projected to reach $790 billion by 2029, the adoption of LGA packaging is accelerating due to its high electrical performance and miniaturization advantages in IoT and automotive applications. However, supply chain constraints and regulatory compliance for semiconductor materials present challenges.

Europe

Europe’s LGA packaging market is characterized by stringent environmental regulations (e.g., EU RoHS) and a focus on sustainable semiconductor manufacturing. Germany and France lead the region, with strong demand for LGA in automotive and industrial IoT applications. The shift toward 5G infrastructure and smart manufacturing is further propelling growth. While competition from alternative packaging technologies like QFN exists, LGA remains preferred for high-reliability applications, such as aerospace (e.g., Thales Group). Nonetheless, economic uncertainties and energy-cost fluctuations pose risks to market stability.

Asia-Pacific

Asia-Pacific dominates the global LGA packaging market, accounting for over 50% of semiconductor demand, with China, Japan, and South Korea as key contributors. The region’s thriving consumer electronics sector, coupled with government initiatives like China’s “Made in China 2025,” drives demand for compact, high-performance packaging solutions. ASE Holdings and GS Nanotech are among the prominent suppliers leveraging cost-efficient manufacturing. However, price sensitivity and reliance on imported semiconductor materials constrain profit margins. The growing automotive electronics market (e.g., EVs in India and Southeast Asia) offers significant long-term potential.

South America

South America’s LGA packaging market is nascent but gradually expanding, primarily in Brazil and Argentina, where local electronics manufacturing is emerging. Limited domestic semiconductor production means heavy reliance on imports, making the market vulnerable to logistical disruptions. While demand for LGA in telecommunications and industrial automation is rising, economic instability and underdeveloped infrastructure slow adoption. Strategic partnerships with global suppliers like Amkor could unlock growth in niche applications, such as agricultural IoT devices.

Middle East & Africa

The MEA region presents a fragmented but growing market for LGA packaging, led by Israel and the UAE in high-tech applications like defense and telecommunications. Saudi Arabia’s Vision 2030 is fostering local semiconductor assembly, but the lack of wafer fabrication facilities limits scalability. Demand stems from optoelectronic components and renewable energy systems, though limited technical expertise and low consumer electronics penetration hinder rapid expansion. Long-term opportunities lie in smart city initiatives and regional collaborations with Asian and European suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional LGA Packaging markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global LGA Packaging market was valued at USD 401 million in 2024 and is projected to reach USD 674 million by 2032, growing at a CAGR of 7.9% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Hot Air Soldering, Infrared Soldering), application (Consumer Electronics, Automotive, Optoelectronic Components), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates the market due to strong semiconductor manufacturing presence.

- Competitive Landscape: Profiles of leading market participants including Orient Semiconductor Electronics, NXP, Maxim Integrated, Thales Group, Analog Devices, ASE Holdings, GS Nanotech, and Amkor, including their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging packaging technologies, integration with IoT devices, semiconductor design trends, and evolving industry standards for high-performance applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth including increasing demand for compact electronic devices, along with challenges like supply chain constraints and raw material price volatility.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving semiconductor packaging ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LGA Packaging Market?

-> LGA Packaging Market was valued at 401 million in 2024 and is projected to reach US$ 674 million by 2032, at a CAGR of 7.9% during the forecast period.

Which key companies operate in Global LGA Packaging Market?

-> Key players include Orient Semiconductor Electronics, NXP, Maxim Integrated, Thales Group, Analog Devices, ASE Holdings, GS Nanotech, and Amkor, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for compact electronics, growth in semiconductor industry (projected to reach USD 790 billion by 2029), and adoption in automotive and IoT applications.

Which region dominates the market?

-> Asia-Pacific is the dominant market due to strong semiconductor manufacturing presence, particularly in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of packages, advanced thermal management solutions, and integration with AI/ML processors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...